2022 has been a tough year for investors to navigate as bond and equity markets have tumbled globally. Given that both assets are often the full extent of portfolio diversification for many investors and fund managers, they have struggled in 2022 and the latter group in particular has struggled to add value. Perhaps against this backdrop we could reasonably expect active funds (those with a fund manager making investment decisions) to outperform their passive peers. By definition passive funds such as trackers will keep tracking their designated index or indices into oblivion if markets implode. But surely active fund managers have been able to be more selective in their approach, to the benefit of their investors?

To answer this question I analysed the performance of funds across 9 asset types which also coincide with 9 similarly named IMA unit trust sectors. These assets were:

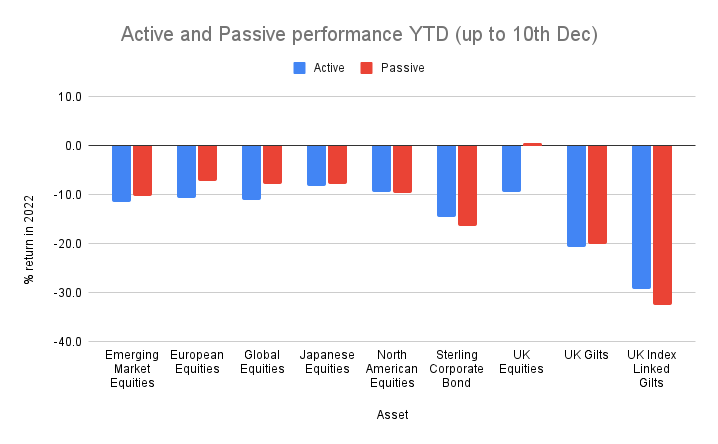

- Emerging Market Equities

- European Equities

- Global Equities

- Japanese Equities

- North American Equities

- Sterling Corporate Bond

- UK Equities

- UK Gilts

- UK Index Linked Gilts

I analysed over 1,300 unit trusts and split them into those funds that are actively managed and those that are passively managed before calculating the average year to date performance for active and passive funds within each asset class. The table below summarises these results, with the best performing type (Active or Passive) for each asset class highlighted in bold.

|

Asset

|

2022 % return (up to 10th Dec) | |

| Active fund (average) | Passive fund (average) | |

| Emerging Market Equities | -11.6 | -10.2 |

| European Equities | -10.6 | -7.2 |

| Global Equities | -11.1 | -7.9 |

| Japanese Equities | -8.3 | -7.8 |

| North American Equities | -9.4 | -9.6 |

| Sterling Corporate Bond | -14.6 | -16.4 |

| UK Equities | -9.4 | 0.5 |

| UK Gilts | -20.7 | -20.0 |

| UK Index Linked Gilts | -29.3 | -32.6 |

This data is perhaps better presented in the chart below:

Back in 2017 I carried out a piece of research titled "Do active funds really outperform passives in sideways or falling markets?". It is worth going back and reading this article. While the findings weren't conclusive, given the data set, there was no evidence to suggest that active funds do outperform in a falling market. In the New Year, I may revisit this research and update it to take account of the significant market swings we've seen over the last five years and expand it to look at other markets and not just UK equities.

Despite the fact that active funds typically underperformed in 2022, a year where you'd hope that they might outperform, it is interesting to note that active funds were more likely to outperform in bond sectors. As you can see, active funds only outperformed passive funds in three asset classes, namely North American Equities, Sterling Corporate Bond and UK Index Linked Gilts. This is interesting when viewed in conjunction with another piece of research from 2019 titled "The sectors where active funds beat passives".

A key takeaway from that piece of research is that when it comes to active versus passive investing "which strategy outperforms depends on the asset, the market and the competition. It also depends on the macro backdrop". In that research article I didn't just look at the performance over a 20 year period but also the consistency of any outperformance or underperformance. Interestingly actively managed North American equities funds consistently underperformed their passive benchmark of the S&P 500. Meanwhile active funds investing in European or UK equities consistently outperformed their passive peers.

While these findings seem at odds with what we've seen in 2022 if you take both former pieces of research together perhaps we should have expected active funds, on average, to underperform their passive peers in 2022. As mentioned the backdrop in markets and the economy have a decisive bearing. In 2022, for example, a rapid rise in inflation sent interest rates and bond yields higher. Those assets that were hurt the most were those most impacted by interest rate risk. At the top of that list are long duration bonds and technology stocks. I explained bond duration in detail in my research article "Funds for a bond market rebound… or a further crash", but in simple terms the higher a bond fund's duration the greater the fund's sensitivity to changes in interest rates. Don't forget that when interest rates rise, bond prices fall. UK Index Linked Gilts are long duration assets, even more so than ordinary UK Gilts. Perhaps this helps explain why active managers outperformed in this asset class. Passive funds will not usually manage duration risk, as they will simply track their chosen index. Whereas there is the potential for a fund manager to choose their level of duration risk.

The outperformance of active North American equities funds versus their passive counterparts in 2022 bucks the historical trend, where the reverse is usually true. But one explanation could be again related to interest rate risk. US technology stocks are one of the worst performing equity sector classes in 2022 due to the rapid rise in interest rates. The equivalent year to date performance of the average technology unit trust fund, which mostly invests in large US technology stocks, is -27.78%. One thing to bear in mind is that many passive US equity funds track US equity market indices such as the S&P 500 which is a market cap-weighted index. This means that the larger a company's capitalisation the greater its allocation in the index. Therefore technology stocks make up a significant portion of the index. The top 5 constituents of the S&P 500 are Apple, Microsoft, Amazon, Tesla and Alphabet (Google) which make up almost 24% of the S&P 500 index due to their size. Therefore when these stocks struggle, as they have in 2022, so does the S&P 500.

The chart below shows how the S&P 500 (in its normal cap-weighted form) massively underperformed the S&P 500 if it was equal-weighted (i.e. every stock accounted for the same allocation in the index).

Technology stocks have accounted for the lion's share of the S&P 500's performance over the last decade, hence why passive strategies have outperformed as they are overweight in technology stocks. On the other hand, active US equity fund managers would reasonably pick from the entire universe of US stocks. However, deviating from the big winners (tech) would lead to you underperforming an index such as the S&P 500 and therefore the passive funds that are based on it. However, in a backdrop such as 2022, when the biggest constituents of a cap-weighted index are hammered it favours active fund managers, whose portfolios are expected to be sufficiently different from the S&P 500 in order to justify their fees.

This likely explains why at the moment, active fund managers of UK equity funds have underperformed their passive counterparts, again contrary to recent history. The FTSE 100 is down just -0.38% year to date, which is comparable to the return seen on passive UK equity funds above. Once again, the FTSE 100 is a cap-weighted index with the largest constituents including Shell plc (at 9.38%), AstraZeneca plc (8.08%) and BP (4.75%). All three are up over 35% so far in 2022. It means that fund managers, who deviate from the FTSE 100's overweight oil/gas and mining companies inevitably underperformed in a year where the Ukraine war had a significant influence.

This highlights an issue that most passive investors don't appreciate, the hidden biases in their portfolios if their funds of choice track weighted indices. 2022 was a bad year for some active funds, but certainly not all. It shows there is more nuance to investing and raises the interesting question of whether, we are now in a period where active managers in certain areas, such as the US are likely to outperform in 2023 given the market backdrop. It certainly suggests that until the economic backdrop changes many of the passive vs active conventional wisdoms will be invalid.

But the above findings show that once again, as DIY investors we shouldn't blindly follow one strategy (active or passive), as there is merit in using both. It is not a binary choice, instead it pays to invest in what is working, as we do with 80-20 Investor, rather than what we think should be working, which is how my own £50k portfolio has outperformed this year.

Top performing funds of 2022

Below I've listed the top 3 performing funds in five of the equity sectors and highlighted whether they are active or passive. Interestingly only two passive funds make the lists and you will also notice a number of funds which I hold in my £50k portfolio or have been regulars in the 80-20 Investor shortlists.

UK Equities - top performing funds of 2022

| Name | Active or Passive | Year to date performance % |

| UBS MSCI United Kingdom UCITS ETF | Passive | 22.84 |

| UBS FTSE 100 UCITS ETF | Passive | 20.13 |

| Invesco UK Opportunities (UK) | Active | 8.78 |

Global Equities - top performing funds of 2022

| Name | Active or Passive | Year to date performance % |

| Jupiter Global Value Equity | Active | 13.41 |

| Scottish Widows Fundamental Low Volatility Index Global (ExUK) Equity | Active | 11.37 |

| MI Thornbridge Global Opportunities | Active | 9.28 |

European Equities - top performing funds of 2022

| Name | Active or Passive | Year to date performance % |

| LF Brook Continental European | Active | 10.76 |

| LF Lightman European | Active | 5.7 |

| VT Argonaut Equity Income | Active | 5.62 |

US Equities - top performing funds of 2022

| Name | Active or Passive | Year to date performance % |

| Quilter Investors US Equity Income | Active | 14.33 |

| BNY Mellon US Equity Income | Active | 14.07 |

| Fidelity American Special Situations | Active | 7.62 |

Japan Equities - top performing funds of 2022

| Name | Active or Passive | Year to date performance % |

| Man GLG Japan Core Alpha | Active | 12.08 |

| Quilter Investors Japanese Equity | Active | 4.15 |

| M&G Japan | Active | 4.08 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay