So the UK voted to leave the European Union and it sent financial markets into a tailspin. Below is just a small sample of Friday's headlines to give you a sense of the scale of the moves:

- Italian stocks suffer worst ever day with 11% fall

- the FTSE 100 tumbled more than 8% within the first few minutes of trading on Friday, its biggest fall since the collapse of the US investment bank Lehman Brothers in 2008

- Pound suffers biggest one day fall ever (down over 8%)

- Wall Street ‘fear gauge’ surges 40%

- Bank shares fall by 30%

... I could go on.

Yet that was just the markets. A Financial Times journalist summed up the chaos when they said:

"It's a rather strange day. The Prime Minister resigning is only our third most important story".

One thing is for certain and that is that Friday was an historic day in investment markets and one that will be talked about for decades. Yet the scale of the market reaction has surprised many commentators. That in itself was surprising. Over the last week the market had convinced itself that the UK would remain in the EU. So much so, that ahead of the vote the FTSE 100 rallied by almost 7% from last week's low. City traders began unwinding all their positions that they'd previously put in place to protect themselves from a potential Brexit. This so called "smart" money (the big institutional investors) got it completely wrong as their fear of missing out on potential profits surpassed their fear of losing money in the event of a Brexit. That's why markets reacted so violently.

You will recall that in last week's newsletter I gave my response to those asking how to profit from the EU referendum. In that piece I explained how I'd increased my cash weighting in my £50,000 portfolio and also wrote:

Yet as DIY investors we all have to take responsibility for our decisions. Those who want to try and play the referendum could make a significant profit if they call it right. Get it wrong and they will be trying to make up lost ground for a long time to come. Those who err on the side of caution and diversify to minimise the impact of either outcome will likely not make much money either way and will probably underperform in the short term versus those who gambled and lucked out. But that may be a more preferable risk to take.

So to all those who are looking to me to tell them how to make a quick profit from the referendum I would quote Clint Eastwood in Dirty Harry and say...

"You've got to ask yourself one question. Do I feel lucky? Well, do ya, punk?"

What to do, stick or twist?

The media is now full of people running around yelling that the sky is falling in. However, simply regurgitating the problem isn't that helpful. Investors are looking for answers. Is the market going to carry on falling? What is the best thing to do, stick or twist.? While the answer to the second question is a personal decision it is better to make that decision from an informed perspective. So it makes sense to look at the past to gain some insight into what we could expect from the future.

Exclusively for 80-20 Investor members I analysed every trading day on the FTSE 100 since its launch in 1984 (that's a total of over 8,000 trading days) to see how the market reacts following a sell-off. You can read the full research piece here - The best strategy in a stock market crash – Stick or Twist?

To summarise the research showed that:

- the worst ever trading day was the day after Black Monday (20th October 1987) when the index fell 12.22% in a single day

- the best and worst days don't happen independently of one another

- when markets suddenly sell-off typically they will bounce back strongly around 6 days later

- typically the bounce after a sell-off will take you 1.8-2% above where the FTSE 100 closed on the initial bad day

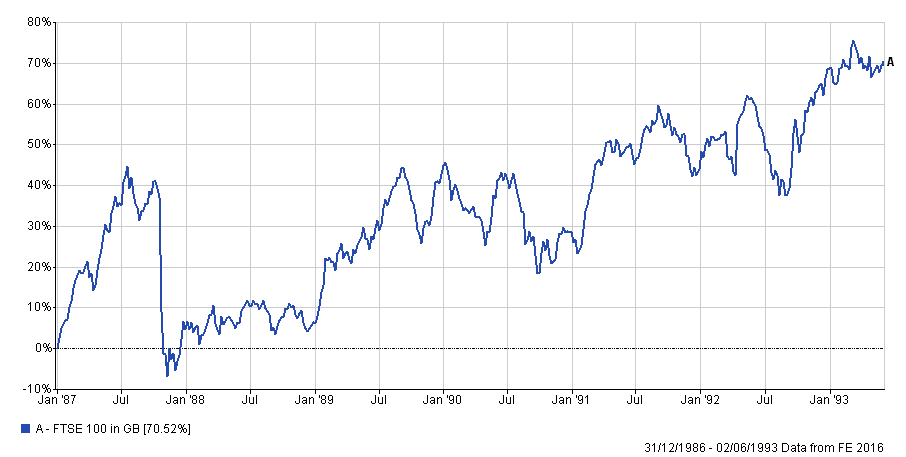

Of course there is no guarantee that there will be a significant bounce or that it will occur in the next week or so. It also doesn't mean that things can't get worse before they get better and in a scenario such as the Brexit we are in unchartered territory. Yet when the post-Brexit sell-off was at its peak, in the hours immediately after the result, there was talk of it possibly eclipsing the falls seen following Black Monday in 1987. This didn't actually happen, in fact the FTSE 100 finished down 3.15%. Yet 1987 is interesting because of the severity of the fall. Despite the market rallying over 7% immediately after the sell-off this had little impact because it followed days of double-digit declines. In fact it took nearly two years for the market to recover to its previous level.

Indeed before Black Monday there were tremors in the months beforehand when the market fell, but recovered somewhat. Today's market falls are almost certainly not the end of things but more likely the beginning of something a bit nasty. In fact following the 20 worst trading days ever on the FTSE All Share index the index was even lower 10 days afterwards on 14 occasions.

So what does this all mean?

- Well it would suggest that we shouldn't be surprised if we get more falls in equity markets in the coming days and weeks

- If you attempt to time the market you will likely miss the bounces having already suffered the loses.

- For those nervous about markets, today's slight rebound from -8% to -3.15% on the FTSE 100 might be an exit opportunity

However, I prefer to take a long term view...

What halted the initial Brexit sell-off?

As events unfolded after the referendum result was announced Mark Carney, the Governor of the Bank of England, made a speech in which he promised that 'the Bank will not hesitate to take additional measures as required as markets adjust and the UK economy moves forward'. The European Central Bank (ECB) also issued similar assurances.

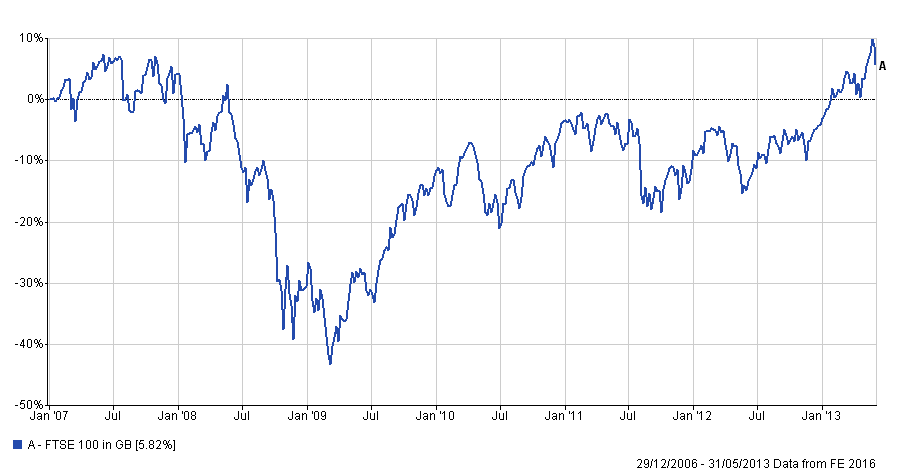

Suddenly rather than central banks attempting to extricate themselves from manipulating financial markets they have issued a new call to arms. If you take a look at how the market behaved during the credit crisis, immediately after Lehman Brothers collapsed (see chart below - click to enlarge) you can see that the rebound was sharper than in 1987. While it took the market 4 years to regain it's pre-crisis level most of the loses were recouped in 12 months, a direct result of central banks launching Quantitative Easing (QE).

It is now expected that the next interest rate move by the Bank of England will be a cut rather than a rise and even more money printing. It's a similar story with the ECB. Interestingly the Bank of Japan (BOJ), which has been reticent about printing more money (QE), may now have its hand forced. That's because in market sell-offs investors buy the Japanese yen. For an export led economy such as Japan a strong currency is bad news as it makes your exports expensive to buy so the BOJ will likely have to take some action which includes more QE.

If things markets continue to fall then the likely source of a new rally could be more central bank action, which is exactly what has driven markets since 2009. If central banks once again start intervening in markets in a sustained way then we may look back on this period of history as a buying opportunity, yet we will only know with the value of hindsight.

80-20 Investor made me 3.6% while global equity markets crashed 7%

You may recall that over the last few months I've deliberately removed the direct European and UK equity exposure in my £50,000 portfolio, instead favouring gaining equity exposure via global funds. I've also been clear about not picking currency hedged funds. Currency hedged funds remove the impact of currency movements from the fund's returns. This can be a positive thing if the pound is strengthening versus other currencies. Yet today's equity market collapse was combined with a collapse in the value of the pound. That means that holdings in unhedged global funds are suddenly worth a lot more overnight when converted back into sterling. My portfolio has been the beneficiary of this (along with the sudden demand for bonds), which was intentional. What that means is that a number of the funds in my portfolio jumped by over 6% on Friday while the FTSE 100 fell 3.15% and European stock markets fell by nearly 7%. Overall by following 80-20 Investor my portfolio gained over 3.6% on the day! Taking that into account and my research above that is why I'll certainly remain invested the market. We are still in the early stages of this bout of turmoil so I appreciate that things can change quickly and the market move against you.

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay