I was asked the following question via Chatterbox and promised to produce an explanatory article:

How to build a global multi asset/diversified income portfolio” - I, for one, would be really interested to read your take on this subject. In particular, it would be very interesting if you combined momentum strategy together with a desire for the portfolio to produce an income.

Types of asset to produce an income

If I was to build an income portfolio I would want the portfolio to produce an income that kept pace with inflation, or at least had a decent chance of doing so. While capital growth in addition to income would be wonderful it wouldn't be my key focus. You can of course target both but in my experience if you want an income you are better off focusing on building a portfolio that can generate a reliable income stream and treat capital growth as a bonus. That might seem odd but to explain my reasoning let's take an extreme example. Assume that you invested all your money (£100,000) in 10,000 shares of one company. Each share costs £10. Remember this is just an extreme example to illustrate a point as you'd never really do that. Let's say that the company paid a dividend of 30p per share (i.e. 3% of what you paid). That equates to £3,000 ignoring tax. Now let's say the company is well run and has historically always had a progressive dividend policy and grown its dividend every year. Next year its divided is 31p. So you receive an income of £3,100 (i.e 10,000 shares x 31p). That's a 3.33% increase in your income from the previous year. That's pretty good and more than the current rate of inflation. However, prevailing market conditions mean that the share price has fallen 10%. So your £100,000 investment is worth £90,000 but your income has actually gone up. In theory the share price could continue to fall but as long as the company could afford to pay a dividend your income is safe. So in reality the value of your portfolio is of little consequence to the income you enjoy. In the long run share prices will tend to rise especially if the company is well run and profitable. Of course investing in the shares of just one company is incredibly risky so to minimise the risk of the company not paying a dividend it is best to invest in several companies or better still invest in equity income funds.

Bonds

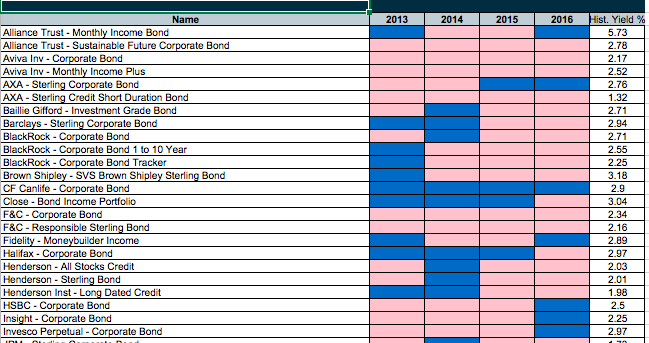

The original question raises an interesting point about building a multi-asset income portfolio. Logically it makes sense as by investing in a range of asset types you diversify your income stream which will hopefully make it more secure. However, in reality it is very difficult to build an income stream from alternative assets. First of all bonds tend to offer a fixed income (hence the name) which won't keep pace with inflation. I covered this in detail in a previous article Are bonds funds a good source of income? If so which ones?. Bonds are an unreliable source of income, plus they tend to perform badly in an inflationary environment from a capital standpoint. In any event I've analysed the payouts of every Sterling Corporate Bond fund that has been around for at least 5 years. The chart below (click to enlarge) shows whether the payout increased (in blue) or decreased/remained static (in red) for each year. As you can see the chart is a wave of red. You can use the chart to see that there are only a couple of funds that have managed to grow their payouts and the average yield is 2.52%. This compares to 1.82% for the average Global Bond fund, 2.73% for the average Global equity income fund and 4.06% for the average UK equity income fund.

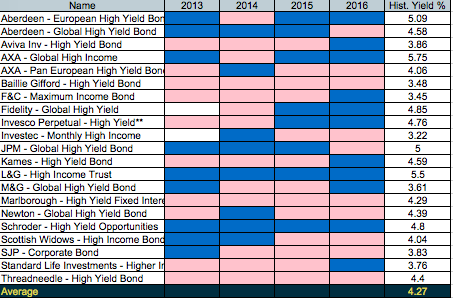

The average UK High Yield bond fund has a yield of 5.06% and I've carried out the same payout analysis for this sector below:

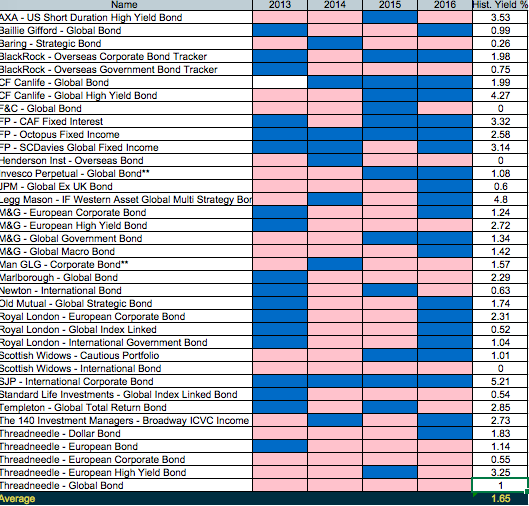

For completeness here's the same analysis for global bond funds:

Property

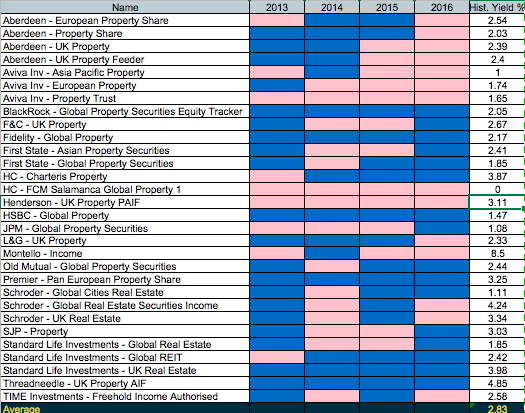

Commercial property is one other potential asset which could produce an income with the average yield being 2.83%. I carried out the same payout analysis as for the bond sectors and the result is more positive. There a number of funds which in recent history have managed to grow their payouts consistently. This makes sense as their payouts will be driven mostly by rental income. There has been a number of new income property fund launches in recent years which aren't included in the table as they don't have a long enough track record of paying an income.

Equities

However without a doubt if I were to build an income portfolio I would focus on equity income funds. Not only are the yields generally more attractive but equity income funds are far better at producing a growing income stream. You can quickly see the best UK equity income funds and Global equity income funds, for growing their payouts, by using our income heatmaps below:

Multi asset income funds

Interestingly there are now a few multi-asset income funds available run by the likes of Premier and M&G. However when you dig deeper their asset mix is almost exclusively bonds and equities. That's the trouble with the multi-asset label as technically if you just hold two asset types then you are multi-asset. So if you want a globally diversified multi-asset portfolio then you would be better off building it from scratch.

The making of a multi-asset globally diversified momentum income portfolio

As I've said, technically I would build an income portfolio with UK and global equity income funds using the 80-20 Investor income heatmaps. However assuming I did pick a multi asset portfolio how could I then add a momentum spin? It's a difficult one because to produce an income portfolio you need to hold the funds for the long term (certainly at least a year or two) to receive the income. That makes it difficult to find momentum that will still be prevalent in a year or more's time. The research behind the 80-20 Investor algorithm showed that momentum wanes considerably past the 12 month point and ideally you wouldn't want to hold funds for more than 6 months if you are trying to take advantage of momentum. For that reason I wouldn't explicitly try to apply momentum to an income portfolio. However, let's assume I do then this is how I'd pick the funds.

- Focus on equity income funds both globally and from the UK

- With perhaps a selection from UK bonds, global bonds and commercial property

- I would likely avoid direct emerging market exposure initially at least (much like the 80-20 Investor algorithm has of late)

- To determine the exact asset mix I might bear in mind the rough asset mix for the last few months of 80-20 Investor.

- To chose the funds themselves I would pick those with a strong record of growing payouts with attractive yields.

- Where possible I'd also try and pick funds that have been regulars in the 80-20 Investor BOTB or BFBS lists.

So taking all of this into account here is a list of possible funds using all the analysis listed above, alongside their current yields.

| Fund | Sector | Yield% |

| Fidelity - Global Dividend | Global Equity Income | 2.4 |

| Standard Life Investments - UK Real Estate | Property | 3.41 |

| Threadneedle - UK Property | Property | 4.3 |

| CF Canlife - Corporate Bond | Sterling Corporate Bond | 3.8 |

| Fidelity - Global High Yield | Sterling High Yield | 5.93 |

| BlackRock - UK Income | UK Equity Income | 3.8 |

| JOHCM - UK Equity Income | UK Equity Income | 4.30 |

| Average | 3.99 |

*the average yield is higher than the FTSE 100 average yield of 3.78% despite the multi-asset approach.

One final thing to note is that I've not concerned myself with the frequency of the payouts (i.e monthly, six monthly etc). That's because if I were to build an income portfolio I would put one year's notional income in cash and use that to live off. In the meantime the portfolio could top up the cash buffer as each payout is received from individual funds. By next year the cash pot would be replenished ready for me to withdraw from it.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay