In last week's newsletter I wrote to ask members if there were any particular areas of interest that they would like me to explore. Among the many responses (please keep them coming in) was the following question:

"I've been reading recently about Chinese shares being opened up more widely to outside investment. Your view on it would be great plus the implications for our investments as I've noticed China making the Best of the Best list. I see China as a good very long term bet. Is this proof of China's arrival as a staple part of investors' portfolio? Loving your work"

This is a really interesting question and I’ve broken down my response into sections in order to make it easier to follow.

Chinese equities hit the big-time?

Last week the MSCI finally decided, after years of procrastination, to allow Chinese A-shares to be included in their MSCI Emerging Market Index for the first time. MSCI have been making research based indexes for 40 years and these form the basis of portfolio management and investment selection around the world. As passive tracking investment solutions grow in popularity it means that billions of pounds of investor money mirrors these indexes and their constituent parts. Around $10 trillion is benchmarked against MSCI indexes in total.

The MSCI Emerging Market Index alone has $2 trillion of active and passive assets benchmarked against it. The decision to include Chinese A-shares means that passive trackers in particular will now be forced to buy Chinese A-shares, in line with the MSCI index. For years traders and commentators have speculated that any inclusion by the MSCI will send a flood of international money into the region, driving up Chinese share prices. Yet the eagle-eyed among you will have noticed that Chinese shares barely gained 1% in the wake of last week's announcement. That may seem surprising but there are a number of reasons that help explain it.

Firstly the changes to the MSCI Emerging Market Index won’t take place for another year, plus the decision was widely expected. It means that there is no imminent wall of passive money on its way to China as I type this. Yet you may be forgiven for thinking ‘hang on, I thought Chinese equities were already in the MSCI Emerging Market index?’ In that case you’d only be half right. There are two ways of investing in the shares of Chinese companies, firstly via the Shanghai and Shenzhen stock exchanges in mainland China (buying what are known as A-shares) and secondly via the Hong Kong Stock Exchange (buying what are known as H-shares). Historically investors outside of China could only buy H-shares while Chinese investors could only buy the A-shares.

The MSCI Emerging Market Index does not invest in A-shares in mainland China but nonetheless as the pie chart below shows, Chinese equities (via Hong Kong) account for around 28% of the asset allocation:

But let's give the MSCI announcement some context, it's only akin to the MSCI dipping its toe in the water of Chinese shares traded on the mainland. There are many reasons why they are right to be nervous which I will come onto later.

China is the second largest economy in the world and the second largest stock market. Yet the inclusion of Chinese A-shares will initially bump up the asset allocation in the MSCI index from 28% to 28.6%. That's barely noticeable. So you can see why the MSCI announcement didn’t move the Chinese stock market all that much, it’s minuscule on a relative basis. However, it is only the thin edge of a potentially big wedge because while China remains underrepresented in the index (and will still be when the MSCI opens the gates) this is likely to change dramatically in the coming years.

In my article from two years ago I explained how the new Shanghai-Hong Kong Stock Connect opened up the Chinese domestic stock market to the world. All that the MSCI has now done is to allow a portion of the stocks tradable via the Connect to be included in their index. Think of it like someone recommending a bunch of UK shares to benchmark against. The shortcut way they could do this it is to quickly pick a bunch of FTSE 100 firms because they can assume the corporate governance isn’t a complete accident waiting to happen and that they in some way represent the UK stock market. MSCI have done something similar with Chinese equities.

Inevitably MSCI will almost certainly broaden the list of Chinese stocks it includes to cover most of the 1500 firms that are tradable via the Shanghai-Hong Kong Stock Connect. What this means for you and I is that the Emerging Market Index fund allocation to China will slowly move from 28% (where it is now) to around 40%. In terms of global positioning, China's exposure in the MSCI All Country World Index will increase from 3%t to 4%. There is a wall of money heading to China, but it’s going to be a very slow build and ultimately DIY investors will have larger exposures to China whether we actively decide to or not.

The impact for the region

This raises the interesting question of how the move could impact other markets. Asia ex Japan funds in time will need to alter their allocations as China increasingly becomes the centre of the region. Australia’s stock market will likely be the biggest casualty. Previously investors have made ‘China plays’ which involve not actually investing in the country itself (as it wasn’t possible) but investing in countries that export commodities to China. In truth it’s probably time for us all to move on from the simple assumptions of the past concerning China and EM’s (emerging markets) generally….

Chinese and Emerging market myth & opportunity

The commonly held view is that emerging market equities (including China) are just a commodity or cyclical play. So if global growth is great then emerging markets are a good place to be as demand increases for the natural resources that many EM countries have in abundance. In addition China’s factories demand increasing amounts of commodities in order to keep China's juggernaut economy going.

However, that view is outdated. In recent weeks I have highlighted how technology stocks have been driving US equities. But many investors will be surprised to learn that tech account for 23% of the MSCI EM equity index which is more than the tech share of the S&P 500. Emerging markets have their own equivalents of US tech giants with firms such as Alibaba (China's Amazon) and Samsung. Interestingly the commodity component of the index has fallen by half and now equates to just 14% of the index. The chart below shows this dramatic change over time.

Clearly EM and China are still susceptible to tumbling commodity prices but their growth is not just a function of Chinese commodity demand as it was 10 years ago. Consumer discretionary and financials make up the rest of the index which points to EMs finally progressing to being a play on untapped consumer spending. This is something that has been predicted but never seen in reality.

For China the growth of its middle class and the government’s desire to move their economy away from its dependency on exports and instead focus on consumer demand is providing huge opportunities. China, for example, is Germany’s 5th largest importer. This is will continue to grow as Chinese consumers increasingly demand higher quality goods and services. In addition, based upon history Chinese equities now represent good value, especially since the market correction of 2015.

Indeed, since the global equity market low at the start 2016 emerging market funds have outperformed their developed world counterparts (click on the chart below to enlarge). This might come as a surprise to most investors, but 80-20 Investor members will have been accustomed to seeing them in our shortlists. Of course there are periods of underperformance such as at the end of 2016 but the summer of 2016 was good for EMs.

The fly in the ointment

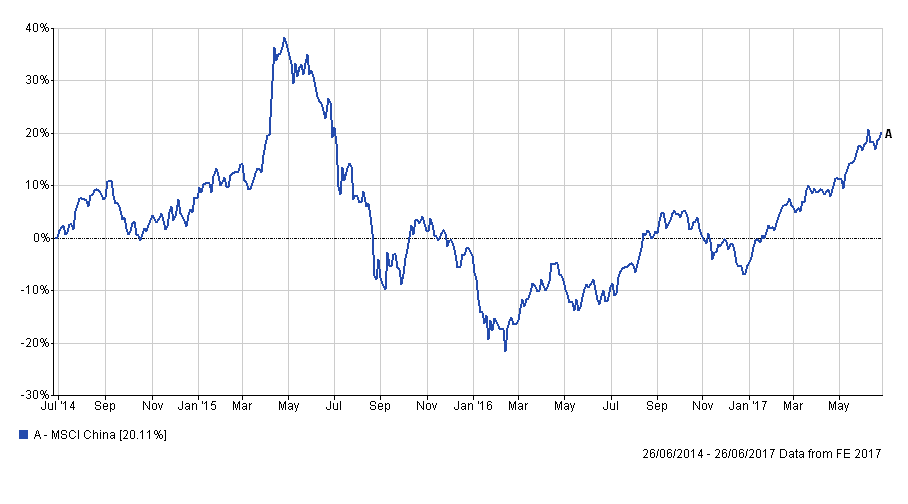

The stock market bubble that burst in 2015 (see chart below) was a result of forms of stimulus, poor regulation and ease of leveraging which encouraged Chinese consumers to speculate on the stock market.

Those of you who have been following my own £50,000 over the last two years will remember how I managed to ride the up wave and limit the impact of the eventual bubble pop. Chinese regulators have since clamped down (rather heavy handedly) on some of these excesses to try and avoid a repeat but investors should still be weary of corporate governance issues. China is dogged with opaque company ownerships, huge corruption scandals and state ownership (or meddling) in companies that often leave shareholders out of pocket.

Stock markets work when there is strong corporate governance and transparency. Shareholders can exert influence over board members for the benefit of investors. In China transparent corporate governance is often a pipe dream. MSCI's inclusion of Chinese shares makes no allowance for corporate governance issues when choosing which shares to include. In fact around two-thirds of the shares that will be initially included by MSCI are controlled by the government one way or another, which puts its demands ahead of company shareholders.

Yet it’s not just about how the companies are run but how they are traded. In the market sell-off of 2015 short selling was banned in China and around half of the Chinese stock market was excluded from trading. Such actions are unheard of in normally operating stock markets in developed countries and getting caught the wrong side can be costly.

In summary

Chinese equities will become an increasing part of global portfolios in the future as a result of moves by the likes of MSCI to include them in their indexes. Passive trackers (of which there are many ETF versions) will be forced to follow where the index makers lead. Yet active managers will do too as they benchmark themselves against many of these indexes. In the short term the MSCI move will probably have little impact on Chinese share prices. However the move does highlight to most DIY and professional investors that they should be considering investing in the world's second biggest economy and stock market.

The China story is far more than a simple commodity play when you dig beneath the surface but this in turn raises similar questions over the influence tech stocks have on stock markets, much like in America.

Emerging market equities (including China) have outperformed developed world equities (as a group) over the last 18 months and those that invested benefited (including 80-20 Investor members) while those that didn't missed out. While there's no guarantee of how well these markets will perform in the future, one thing is for certain and that's those who play Chinese equities right will likely outperform those (including professional) fund managers who continue to ignore this asset class. There will be plenty of bumps along the way but it could be that active managers will be able to exert their expertise on the ground to navigate the many 'Chinese;' minefields (corruption and corporate governance issues) that index trackers could blindly walk into. Of course there is no guarantee that they will, after all fund manager legend Anthony Bolton famously got caught out. The point is that you need an objective mind when investing in China, limit your exposure and ride the momentum before an almost inevitable correction (reset).

How to gain exposure to Chinese equities

While I have been running my own £50,000 portfolio on 80-20 Investor I have invested directly into Chinese equity funds, yet these typically only invest around 10% of their asset via shares in mainland China, the rest is via Hong Kong. I tend to choose these funds using the Best Funds by Sector Section. However, right now I gain my Chinese exposure via Baillie Gifford Pacific which has around a third of its assets invested in Chinese equities. One final point, when I invested in Chinese equity funds previously I kept an eye on the stop loss alerts as well as dripped out of the market when things looked frothy. I don't think I'd do anything differently two years on.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay