To give you a sense of the strength of the recent rally in Chinese equities the chart below compares the returns a UK investor would have achieved had they invested in Chinese equities versus those in the US and the UK over the last year.

Now there is a reason why I have benchmarked it against the US stock market. Firstly because the US stock market was the best performing market in 2014.

Secondly, in order to illustrate how severe the rally in Chinese equities has been. The size of the rally actually distorts the vertical scale on the chart. So much so that the incredible 15% return from the S&P 500 in the last 6 weeks of 2014 is barely noticeable!

What is driving the rally in Chinese equities

The chart below shows the performance of the MSCI China Index over the last 3 years. You can clearly see that at the end of 2014 the Chinese stock market rally gathered momentum. So what was the trigger?

To explain what is going on I need to give you a bit of background to set the scene. There are two ways of investing in the shares of Chinese companies, firstly via the Shanghai stock exchange in mainland China (buying what are known as A-shares) and secondly via the Hong Kong Stock Exchange (buying what are known as H-shares).

Historically investors outside of China could only buy H-shares while Chinese investors could only buy the A-shares. So many companies are listed on both exchanges with the A-shares usually trading at a premium to their H-share counterparts..

Back in November Chinese authorities launched the Shanghai-Hong Kong Stock Connect, a pilot scheme to allow very limited trading between both exchanges, effectively opening up the Chinese domestic stock market to the world’s investors and vice versa.

Despite the long wait for such a tie-up (it had been set back and cancelled numerous times over the previous 7 years) investor demand didn’t live up to the pre-launch hype. Part of the reason was that only wealthy domestic Chinese retail investors (when I say ‘retail’ that means ordinary investors not companies) could take advantage of it. Yet they had already been trading in overseas shares via other creative methods. So there was little appetite for the new scheme. The long and short of all this is that flows of investment money in and out of China had been effectively frozen but things begun to thaw at the end of 2014.

Then in April 2015 the Chinese regulators extended the tie-up so China’s professional fund managers could now start buying H-shares which also paved the way for international investors and hedge funds to get stuck into A-shares. So in a sense the flood gates were propped slightly ajar.

But there is another wall of demand that is fuelling the current rally, On the back of a soaring domestic Chinese stock market (A-shares) Chinese investors began rushing to buy into the rally. In the first week of April alone 1.67 million new trading accounts were opened and the trend is continuing.

There are anecdotes of people in China queuing around the block to buy shares, no matter what the company, in the belief that they are almost certain to make a killing.

As I pointed out in my recent research piece, Finding Value: The cheapest stock markets to invest in now, China equities are actually cheap by historical standards – and buying cheap can lead to profits further down the line. Yet as I pointed out at the time, the ‘value’ of a market as a whole only gives you an overall temperature and says nothing about individual hotspots.

One measure of a company’s value is the simple P/E ratio (price to earnings). As a very loose rule of thumb anything around 10 is pretty good. So it’s shocking to see that over a third of the stocks on the Shanghai exchange have a P/E ratio of over 50! That means their price is completely disengaged from the actual earnings the company is expected to make over the coming year. Or in other words reality has well and truly left the building! In the tech sector there are valuation levels not seen since the US dotcom bubble. On top of that 1 in 17 shares have at least doubled in value in this year alone according to the FT.

It is these sorts of figures that are driving the frenzy among Chinese retail investors with the initial spark that ignited the rally being the property downturn in China.

Yet the improved tie-up between the Shanghai stock exchange and Hong Kong’s exchange has meant there has been a rotation from the overheated higher valued A-shares into cheaper H-shares, so driving up the Hong-Kong market. Remember, previously Chinese investors could only buy in China (A-shares) so values soared versus H-shares. So why hold A-shares in a company when you can buy the cheaper H-share version? Just look at the chart below to get a sense of how A shares (the red line) have become overheated versus H shares (the blue line) over the last year.

Chinese investors are looking for a home for their huge profits from A-shares and given that the Chinese currency is tightly controlled they can’t send it overseas. So the Hong Kong stock exchange is the natural beneficiary. So from a UK investor’s perspective as the Hong Kong stock exchange has rallied so have the value of Chinese funds that we can invest in.

Chinese money printing?

You will have seen in my weekly newsletters that Chinese economic growth is one of the BIG worries for global markets. China’s economy grew at its lowest rate in 6 years, during the first 3 months of this year. While the actual rate is 7% it needs to be taken with a pinch of salt given the secrecy of Chinese economic data and the fact that it is bang on the Government’s stated target. The point is that China’s economy is slowing and ahead lies a difficult transition period.

China needs to do something to prop up its economic growth and that inevitably means some form of monetary policy loosening (i.e. interest rate reductions and the like). Yet investors have learned from the US and Europe that easy money means higher share prices. So the market has rallied even more as a result.

China has already taken steps along this path by effectively allowing banks to lend more easily. But there was a fly in the ointment. China tightened the rules which allow investors to borrow money and invest it (called ‘margin lending’). This prompted the market to sell off and trigger 80-20 Investor stop loss alerts this week on 2 funds within the 80-20 Best of the Best selection.

Should you buy Chinese equities now?

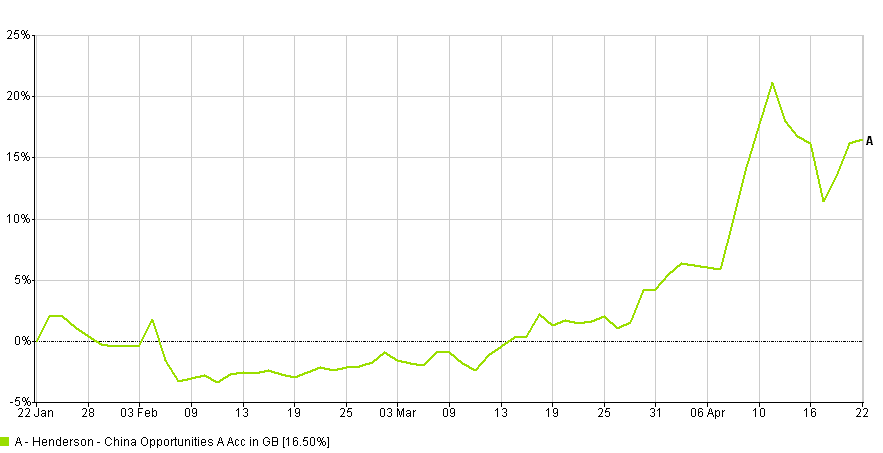

As you know, unlike most investment experts I actually invest £50,000 of my own money live for 80-20 Investor subscribers to see. In my last update (Damien’s portfolio: I made back the cost of an 80-20 Investor subscription in just 2 weeks) I sold out of US technology stocks (because I thought they were expensive) and bought Chinese equities. Interestingly the point at which I bought into Henderson China Opportunities was right at the bottom of the latest spike on 7th April 2015 (see chart below showing the fund's performance over the past 3 months ) and the fund made 14% in a week before selling off slightly. While it only makes up 7% of my portfolio it contributed to the portfolio making 4.8% (net of charges) in just 6 weeks.

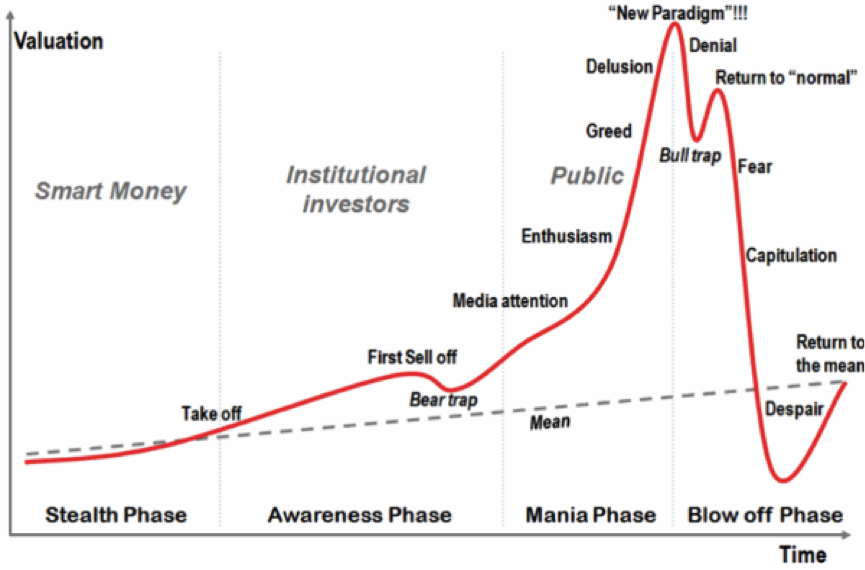

However, as I mentioned in last week’s newsletter, the scale of the jump makes me nervous. Let’s make no bones about it, Chinese equities are in a bubble and remember bubbles pop. The graph below shows the various stages of a bubble and right now the mainland China stock market bubble is inflating another bubble on the Hong Kong stock exchange.

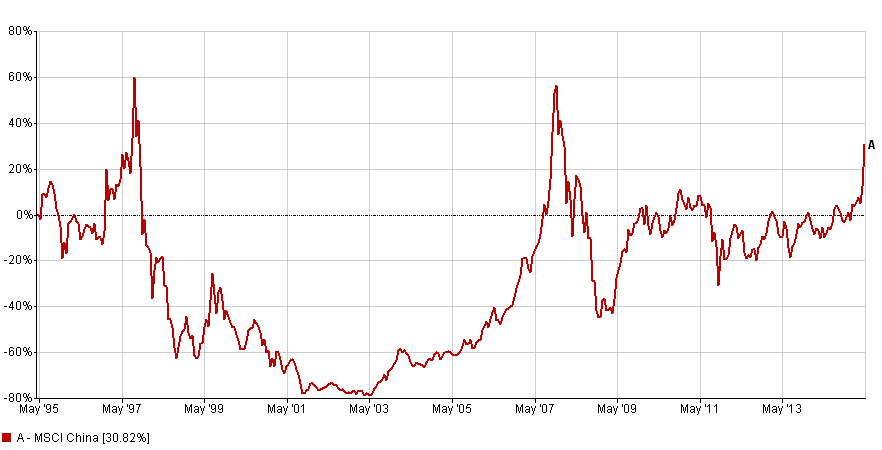

Interestingly you can see the same pattern if we look at what happened with Chinese shares between May 2003 and March 2009 - see below.

Yet what the current rally does emphasise is the untapped wealth in China. To put the 1.67 million new trading accounts opened by Chinese investors in a single week into context that number only equates to a 1% increase in accounts per week due to sheer size of China.

On top of that, according to Forbes, Chinese households still have between 60-70% of their assets in cash compared to 40% for Korea and Taiwan.

While valuation methods are debatable and mask a multitude of sins the fact remains that Chinese equities on the Hong Kong exchange remain cheap by historical standards.

There is also the conundrum of the Chinese Government’s attempts to cool its stock market. While it clamped down on margin lending, just a week previously it had increased the number of trading accounts retail investor are allowed to 20… up from the previous limit of 1?! That doesn’t sound like a Government trying too hard to burst an equity bubble. Plus regulators limit short selling of Chinese shares, i.e. making bets that the market will crash.

What is likely to dictate the top performing fund managers in 2015 is how they play China. Sit on the sidelines and you could be left behind, over commit and you risk getting caught when the bubble bursts.

There remain huge risks with investing in China and we will never get the exit right. So how am I going to play it with my £50,000 portfolio?

Looking at the bubble chart above mainland China is in the grip of the Greed phase. Yet there remains some support for it and the Hong Kong's rally could feasibly continue for a time. Also, in June mainland Chinese shares may make it into key MSCI Emerging Market Indices. So what? With the rise in popularity of passive investing (index trackers and ETFs) if they are included then some tracker funds will have to buy Chinese equities whether they like it or not. It is estimated that around $360 billion worth will have to be bought. That’s a lot. Although their inclusion is unlikely to happen in June it will conceivably happen in the future.

So to sum up…

- Chinese equities are looking like a bubble

- It will burst

- We just don’t know when

That is why I’m entrusting my allocation to the 80-20 Investor algorithm which has been backing China since the end of 2014, well before the current rally. When it comes to market timing you need a process as you won’t get it right. The 80-20 stop losses can help avert disaster but for now I’ve chosen to stay in with a view to reduce my allocation over time and take profits.

The journey will be bumpy yet Morgan Stanley believe the Hong Kong’s Hang Seng Index could hit 30,000 by the end of the year. Which means there’s another 8% upside in their view

But to put that into context they said the same thing at the start of 2008 (look at the peak in the chart above) predicting a 22% rise. In fact by the end of that year it had fallen 48.27%!

Therein lies the danger of Chinese equities.

Which funds to buy?

If you are brave enough to invest in China then only do so with your eyes wide open, knowing that you could be sitting on a heavy loss when the market bursts.

Keep your allocation small and monitor our 80-20 Investor stop losses if you are nervous. I’d opt for Henderson China Opportunities or the less volatile Threadneedle China Opportunities – both identified as having momentum via the 80-20 Investor algorithm. If you are looking for a cheaper investment trust then Fidelity China Special Situations is an option although it is very high risk and borrows to invest, called leveraging. Despite being up 46% in the last six months it still trades a 12% discount to NAV.

Alternatively opt for a broader unit trust fund which invests across Asia and that has some exposure to China. Baring Eastern Trust (currently in our Best of the Best Selection) has 27% exposure to China with the rest of its assets exposed to countries such as India, Taiwan, Indonesia and Korea. Also have a look at Fidelity South East Asia which has a similar mix.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay