Emerging market equities have been shunned by many investors over the last decade, perhaps understandably so. Between January 2010 and January 2020 the S&P 500 rose by 308% while the MSCI Emerging Market index rose just 74.93%. It even underperformed the FSTE 100 which rose 103.98% (i.e doubled in value).

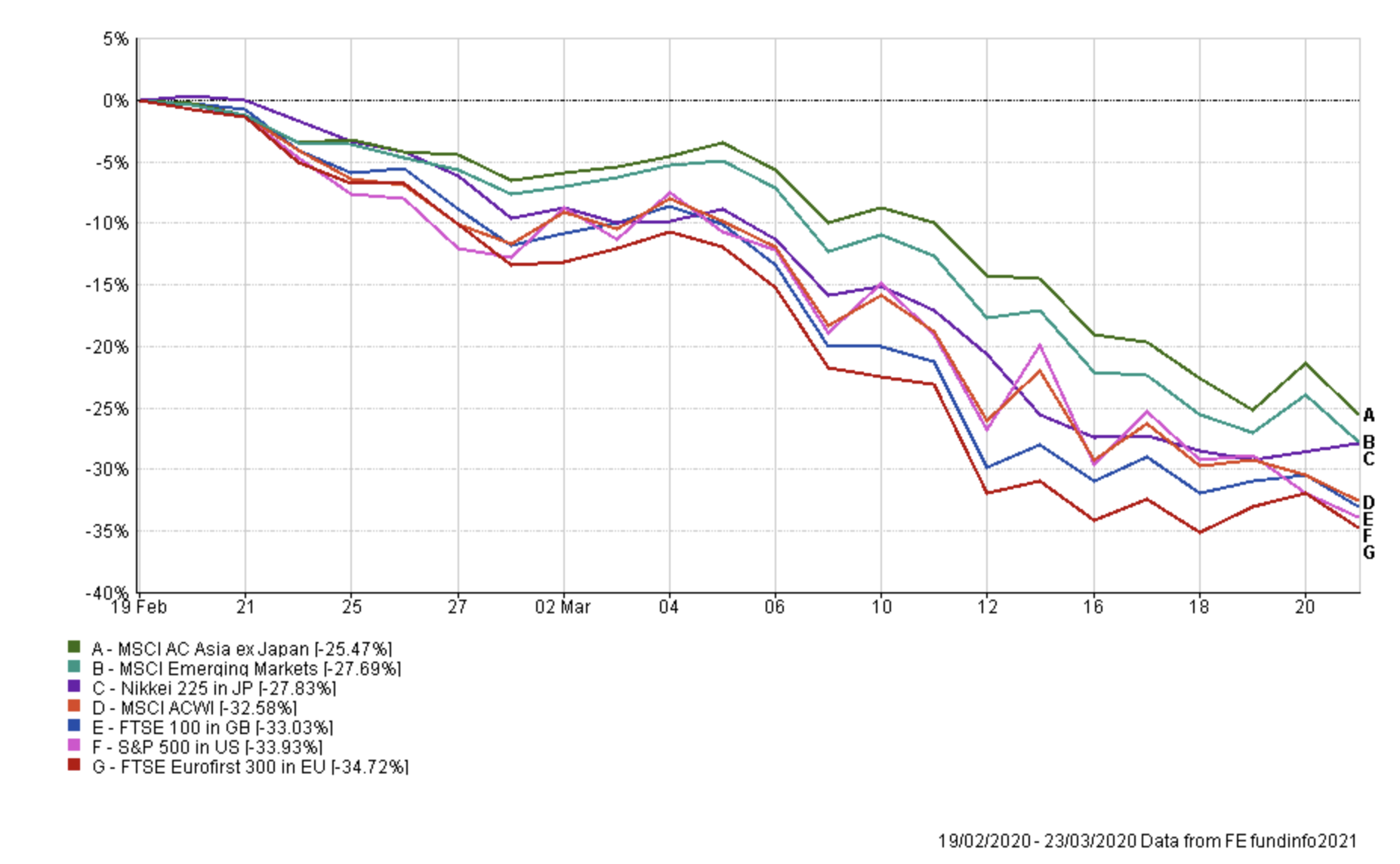

But while it may have passed many investors by, those of you who have been following my weekly newsletters and my £50,000 portfolio reviews will be well aware that developed markets underperformed emerging markets in 2020. The first chart below shows the performance of key world stock indices during the initial stock market slump following the initial Covid-19 outbreak.

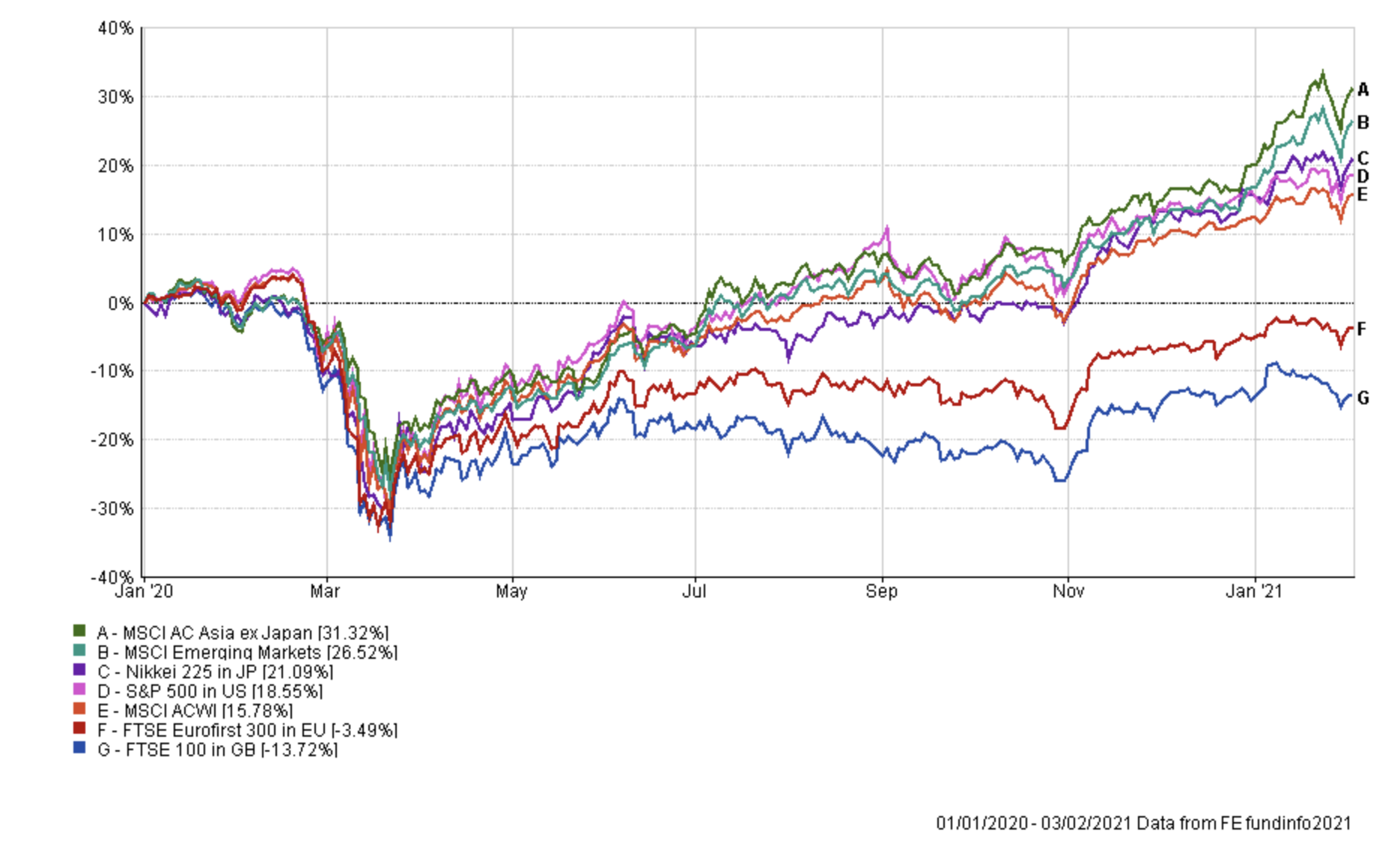

The second chart shows the performance from the start of 2020 to date:

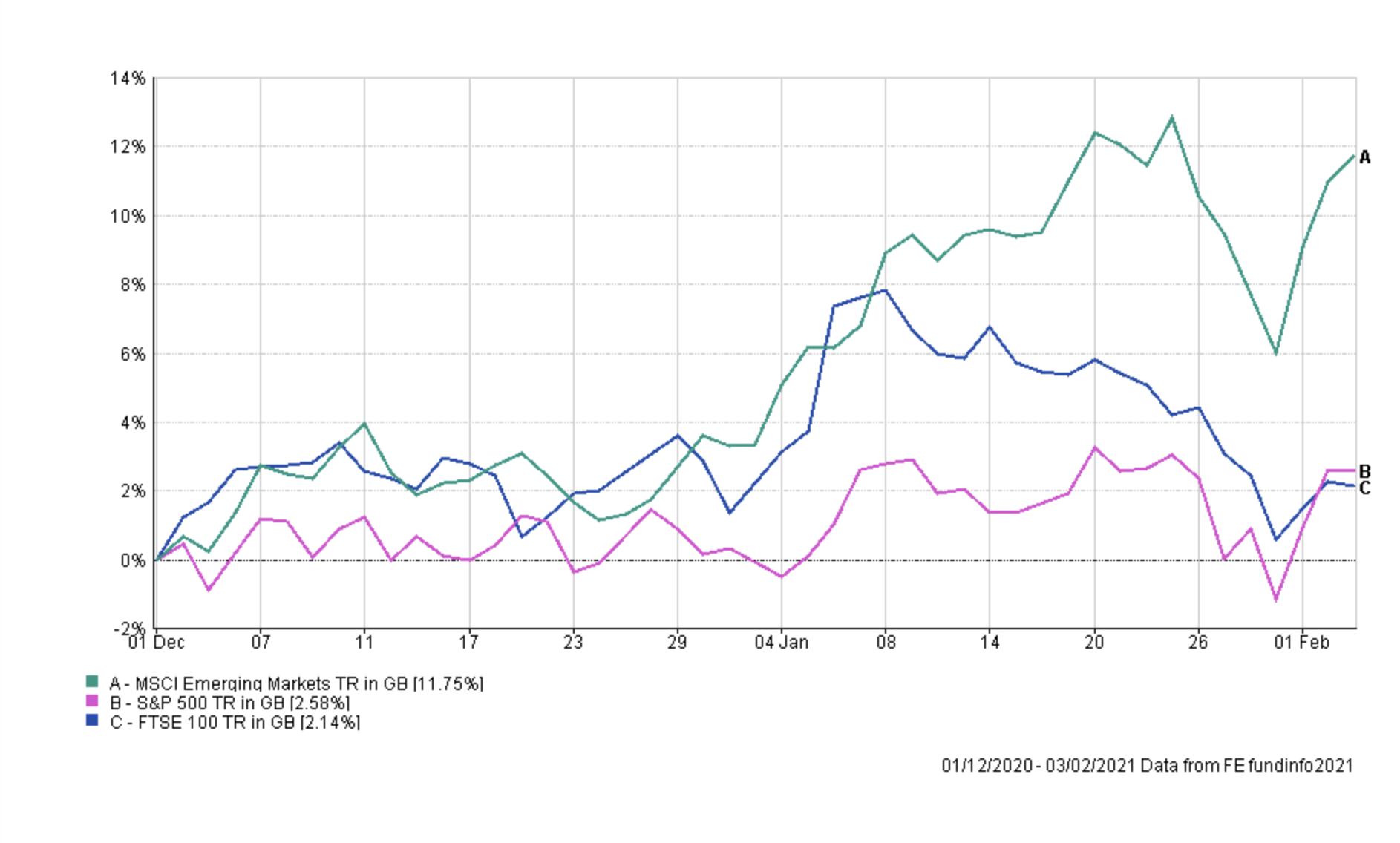

Not investing in emerging market equities would have been a missed opportunity, especially since the start of December 2020 (as shown below), which happened to be when I introduced a significant exposure to emerging market equities into my own portfolio.

Of course, investing in emerging market equities is a volatile pursuit but as has the tide finally turned in favour of developing world equities versus developed world equities following the lost decade shown earlier. But just viewing emerging market equities as a catch-all asset class hides an interesting story. Emerging market equities haven't performed in perfect synchronisation, with some faring significantly better than others in dealing with the challenges of the Covid-19 pandemic. In terms of their outlook too, there are pockets of opportunities in different of the markets, but also obstacles to watch out for. The table below shows the performance of some of the best performing emerging market equity markets since the start of 2020, taking into account currency movements. I have also included some of the best performers since the vaccine trade began. A good example of the latter is Russian equities, which have benefited from a surge in the price of oil.

| Name | % return 1/11/20 to 3/2/21 | % return 1/1/2020 to 3/2/21 |

| MSCI Korea | 38.68 | 49.58 |

| MSCI Taiwan | 29.32 | 53.67 |

| MSCI Russia | 24.24 | -16.25 |

| MSCI Emerging Markets | 19.99 | 24.01 |

| MSCI India | 18.8 | 17.51 |

| FTSE 100 | 17.28 | -10.87 |

| MSCI China | 13.38 | 42.42 |

| S&P 500 | 11.31 | 16.66 |

For some of these emerging markets the bullish trend has been underway for almost a year, while others have only recently enjoyed an uptick in fortunes.

So below we have looked in detail at each of the five emerging markets we've highlighted and discussed the opportunities within them. But as investors, it is difficult to gain exposure to some of these markets without buying ETFs directly invested in them. For most investors wanting to invest using investment trusts or unit trusts it is a more difficult task, especially if they want to gain that exposure via a diversified fund. So we have analysed over 2,500 funds to identify a selection of unit trusts and investment trusts with the largest exposure to each market. No doubt many of you will have noticed some of these creeping into the BOTB and BFBS tables over the last month.

Russia

The Russian economy is no stranger to volatility, with a record of being hard-hit by global and national crises but, ultimately, staging strong recoveries. Recent examples include the period following the collapse of the Soviet Union, which culminated in the devaluation of the Russian ruble in 1998, which, coupled with a rising oil price, laid the foundations for a solid recovery into the new millennium. Similarly, Russia was one of the hardest hit economies in the financial crisis in 2008-09 but, again, was dragged out of the doldrums by decisive monetary policy decisions by the government.

Meanwhile, the Covid-19 pandemic also had a marked effect on Russia, with the tumble in the oil price seeing its economy shrink at the fastest rate in a decade, before it started to recover on the back of the development of its own vaccine and the development of accommodative monetary and fiscal policy to help balance the growing unemployment rate in the country. The World Bank predicts the Russian economy shrank by around 4% in 2020, but anticipates growth of 2.6% and 3% in 2021 and 2022, respectively, dependent on the pandemic easing and a successful rollout of the vaccine.

Russia's greatest strength and weakness is oil: its economy is skewed heavily towards it, with crude oil, petroleum products and natural gas making up around 58% of its exports. It has served to create a good fiscal buffer to help the country ride out the many ups and downs it has faced, as well as tempting investors to put aside their misgivings around corporate governance and geopolitical risk associated with the country. However, the flipside of its reliance on oil is it leaves it exposed to a move to a low-carbon environment and looks set to hamper its participation in the widely anticipated "green recovery".

Ultimately, Russia is an obvious way to gain exposure to the oil price in your portfolio if, like many, you anticipate an uptick this year as manufacturing picks up and a resurgence in things like air travel becomes more likely. While there are definite obstacles in its path over the mid-to-long term unless it implements a transition away from the energy sector and embraces sustainability and low-carbon trends, in the short term it has potential to outperform if the price of oil, in particular, continues to rally.

| Fund | ISIN code | Type of fund | % exposure to Russian equities |

| JPM - JP Morgan Russian Securities plc | GB0032164732 | Investment trust | 98.7 |

| Liontrust - Russia | GB00B86WB793 | OEIC/UT | 98 |

| Invesco - Emerging European (UK) | GB00B28J0Z75 | OEIC/UT | 75.61 |

| JPM - Emerging Europe Equity | GB0001655124 | OEIC/UT | 69.6 |

| Baring Asset Mgt - Baring Emerging EMEA Opportunities PLC | GB0032273343 | Investment trust | 67.7 |

| ASI - Eastern European Equity | GB00B3MPT513 | OEIC/UT | 63.3 |

| Jupiter - Emerging European Opportunities | GB0031862534 | OEIC/UT | 56.4 |

| Fidelity - Emerging Europe Middle East and Africa | GB00B87Z7808 | OEIC/UT | 33.2 |

South Korea

In a universally challenging year, South Korea emerged as the strongest-performing global market in 2020, with the KOSPI index up over 30%. This impressive performance was mainly driven by two factors: a hugely efficient response to the pandemic, which meant it remained closely contained and enabled society to continue to function relatively normally while others were plunged into lockdowns, and the overwhelming strength of some of its big-name tech stocks, particularly in the semiconductor space.

Its outperformance last year was no fluke and it is widely anticipated South Korea will continue to lead the pack, with JP Morgan Chase forecasting the KOSPI will rise another 15% in 2021. Certainly, it is proving popular with global fund managers, with inflows of over $5bn in the final two months of 2020 alone. The main drivers at a stock level are the desire to ride the wave of popularity of players such as Samsung Electronics, SK Hynix and LG Electronics, which are all benefitting from the global trend of people staying at home more and needing access to technology to facilitate that.

Looking forward, South Korea is positioning itself at the heart of the trend towards sustainability, partnering with the World Bank to create a global hub for innovation and technology for sustainable development. This aims to share ideas and funding to developing countries to help them engage with projects that promote low-carbon and sustainable projects. It is, therefore, excellently placed to benefit from increasing global demand for sustainable solutions but also global economic growth.

Moreover, many Korean companies are also undertaking their own overhaul, improving corporate governance practices, as well as developing a culture of higher dividend payouts and more robust shareholder returns policies. This will only serve to encourage further inflows in the future.

On the downside, valuations are starting to look a little stretched, the KOSPI trading at around 14 times projected earnings for the next 12 months, although this is nowhere near the 26 times we are seeing from the S&P 500. On the currency side too, a strengthening of the South Korean won could begin to put pressure on exports as the year goes on, particularly with key trading partner China.

| Fund | ISIN code | Type of fund | % exposure to Korean equities |

| Weiss Asset Management LP - Weiss Korea Opportunity Ltd | GG00B933LL68 | Investment trust | 100 |

| Barings - Korea Trust | GB0000840719 | OEIC/UT | 99.2 |

| L&G - Pacific Index Trust | GB00B0CNGY27 | OEIC/UT | 23.7 |

| iShares - Pacific ex Japan Equity Index (UK) | GB00B849FB47 | OEIC/UT | 23.57 |

| Janus Henderson - Henderson Far East Income Ltd | JE00B1GXH751 | Investment trust | 22.4 |

| Templeton - Global Emerging Markets | GB00B7MZ0J00 | OEIC/UT | 22.26 |

| HSBC - Pacific Index | GB0000150713 | OEIC/UT | 20.86 |

| Franklin - Templeton Emerging Markets Investment Trust Plc | GB0008829292 | Investment trust | 20.2 |

| Legg Mason - IF Martin Currie Emerging Markets | GB00BVZ6TX52 | OEIC/UT | 20.04 |

Taiwan

As with South Korea, Taiwan's fate is closely tied to near-neighbour China. Indeed, although it thrived last year, with its GDP up over 2%, this represents a dramatic turnaround from even three or four years ago when it was in the doldrums. At that point it was suffering from mass migration to China as it struggled to compete with the opportunities present for people on the mainland. In fact, even now, 2% of its population lives across the Taiwan Strait. However, like South Korea, its handling of the pandemic - with successful test and trace and mask-wearing strategies meaning day-to-day life was largely unaffected for the Taiwanese - gave its economy a real boost.

As well as its relative success in its management of the Covid-19 crisis, it has also witnessed a shift over recent years brought about by the fraught relationship between China and the US. Taiwanese companies that had moved to China found themselves hit with tariffs, which ultimately encouraged them to return to Taiwan. This has represented a boon for Taiwan, although there are some misgivings now about the impact of Joe Biden's presidency, who, while currently talking the talk on a tough stance on China, is unlikely to be as uncompromising as his predecessor.

A core strength of the Taiwanese market is its expertise in electronics, with company Taiwan Semiconductor (TSMC) - which makes up a staggering 30% of the Morningstar Taiwan index - making the world's most advanced semiconductors. Overall, electronics make up a third of the country's exports, which were up 5% last year, compared with a fall in global trade of 10%. These exports are going to continue to be vital in the upcoming year, allowing Taiwan to be a central player in the unfolding recovery story.

| Fund | ISIN code | Type of fund | % exposure to Taiwan equities |

| FSSA - Greater China Growth | GB0033874321 | OEIC/UT | 28.8 |

| iShares - Pacific ex Japan Equity Index (UK) | GB00B849FB47 | OEIC/UT | 23.04 |

| HSBC - Pacific Index | GB0000150713 | OEIC/UT | 22.9 |

| L&G - Pacific Index Trust | GB00B0CNGY27 | OEIC/UT | 22.9 |

| JPM - JP Morgan Global Emerging Markets Income Trust plc | GB00B5ZZY915 | Investment trust | 21.5 |

| Fidelity - Asian Dividend | GB00B8W5M023 | OEIC/UT | 20.8 |

| Schroder Investment Management Ltd - Schroder Oriental Income | GB00B0CRWN59 | Investment trust | 20.8 |

| JPM - Emerging Markets Income | GB00B56DF680 | OEIC/UT | 20.6 |

| Invesco - Asian Equity Income (UK) | GB00B4JR4R48 | OEIC/UT | 20.08 |

India

India experienced extreme volatility in 2020, in terms of both the impact of the pandemic and the introduction of a national lockdown in March and the implementation of far-reaching economic and social reforms by the government, which has resulted in ongoing protests from farmers and a further squeeze on the already beleaguered labourers and shopkeepers who form a key part of the economy. The two main indices - the Sensex and the Nifty50 - hit a low in March before rebounding to meet all-time highs by the end of the year. Moreover, foreign investors have piled into the market, investing $14bn in the final two months of the year alone.

Looking forward, analysts widely anticipate a higher-than-average level of resilience from the market, particularly if the rollout of the vaccine, which will pose its own challenges in a country with such a large population, is successful. Moody's predicts GDP growth of 10.8% for the fiscal year April 1, 2021 to March 31, 2022, largely driven by the dominant private banking, energy and consumer discretionary sectors. For the latter, pent-up demand from domestic consumers looks set to provide a boost to the economy as retail begins to open up again.

There are some commentators who are sceptical of the short-term prospects for the Indian economy, with Goldman Sachs predicting an overall contraction of 10.3% in GDP in 2021, before it goes on to deliver double-digit growth in 2022. A lot will ride on whether the government's commitment of $50bn - 2% of the country's annual economic output - to help small businesses through this difficult period will have an impact, as well as how quickly the government reacts to future changes in its monetary policy strategy.

A final question mark hangs over whether India continues to offer good value for investors. With p/e multiples edging up, India is certainly no longer a cheap option and as a net importer of oil rising oil price could prove problematic.

| Fund | ISIN code | Type of fund | % exposure to Indian equities |

| Liontrust - India | GB00B1L6DV51 | OEIC/UT | 100.56 |

| Aberdeen - New India Investment Trust PLC | GB0006048770 | Investment trust | 99.7 |

| Jupiter - India | GB00B2NHJ040 | OEIC/UT | 98.67 |

| Ocean Dial Asset Management - India Capital Growth Ld | GB00B0P8RJ60 | Investment trust | 98 |

| JPM - JP Morgan Indian IT plc | GB0003450359 | Investment trust | 94 |

| FSSA - Indian Subcontinent All-Cap | GB00BDG1BM66 | OEIC/UT | 92.3 |

| Stewart Investors - Indian Subcontinent Sustainability | GB00B1FXTG93 | OEIC/UT | 90.3 |

| Fundsmith - Emerging Equities Trust PLC ORD | GB00BLSNND18 | Investment trust | 42.9 |

| Stewart Investors - Asia Pcfic and Japan Sustblty | GB0030184088 | OEIC/UT | 42.3 |

| Frostrow Capital LLP - Pacific Assets Trust plc | GB0006674385 | Investment trust | 39.5 |

| Stewart Investors - Asia Pacific Leaders Sustainability | GB0033874768 | OEIC/UT | 37.9 |

| First State Investments IT - Scottish Oriental Smaller Companies | GB0007836132 | Investment trust | 37.12 |

| Stewart Investors - Asia Pacific Sustainab. | GB00B0TY6V50 | OEIC/UT | 36.9 |

| Stewart Investors - Global Emerging Markets Sustainability | GB00B64TS998 | OEIC/UT | 31.6 |

China

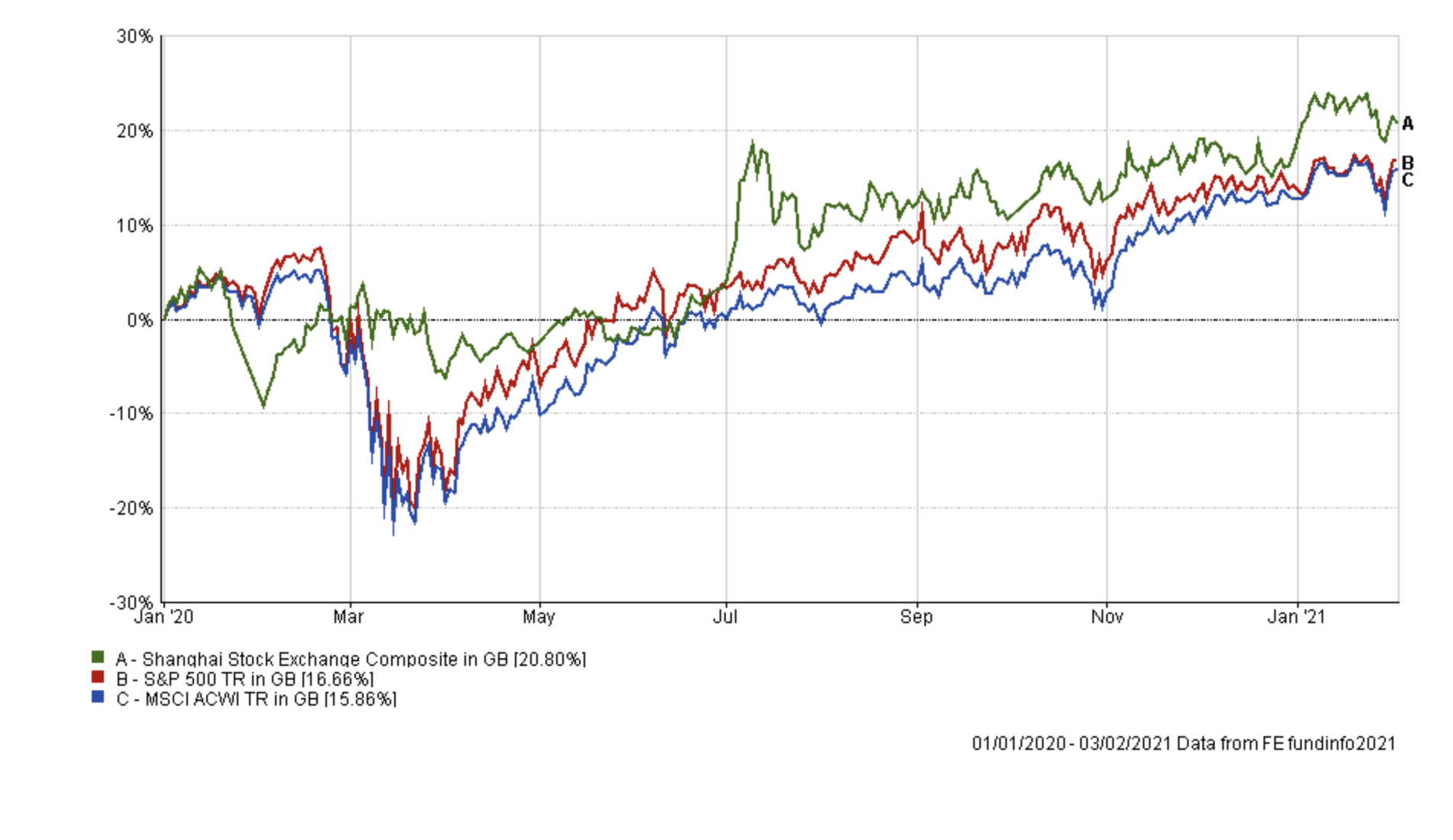

The outlook for China this year is somewhat counterintuitive when compared with other emerging markets. While for many economies the development and delivery of an efficient vaccine is a central factor in how well they are likely to recover this year, for China the fact that it has managed to control the virus so well through societal restrictions and other measures means this is not as big an issue. Indeed, after the initial shock to the market at the outset of 2020, China was largely immune from the global market sell-off and continues to exist almost in its own bubble. This can be witnessed in the performance of the Shanghai Composite index, which bottomed out at the end of March but had largely recovered by July. The chart below shows the Shanghai Composite index versus the MSCI All World index and the S&P 500 since the start of 2020.

Overall, the Chinese economy grew by 2.3% last year, boosted by a particularly strong Q4, which saw year-on-year growth of 6.5%. The Morningstar China index, meanwhile, was up over 30% in dollar terms across the year. This trend is likely to continue, with the effect of stimulus measures filtering through likely to show in the Q1 2021 figures. The general consensus is that we can expect to see economic growth of around 8-9% this year.

A key factor for China continues to be its relationship with the US and that is an issue that is unlikely to be resolved in the near future. While most commentary centres on the more favourable conditions for China that will be brought about by having Biden in the White House, sceptics wonder if a more measured and strategic approach by the new president in managing its rival could, ultimately, be more dangerous than the bluff and bluster of Trump.

| Fund | ISIN code | Type of fund | % exposure to Chinese equities |

| Baillie Gifford - China | GB00B39RMM81 | OEIC/UT | 98.4 |

| JPM - JPMorgan China Growth & Income plc | GB0003435012 | Investment trust | 95.2 |

| Liontrust - China | GB00B5Q38588 | OEIC/UT | 93.62 |

| Fidelity - China Consumer | GB00B82ZSC67 | OEIC/UT | 87.7 |

| Threadneedle - China Opportunities | GB00B1PRW734 | OEIC/UT | 77.93 |

| Janus Henderson - China Opportunities | GB00BJ0LF884 | OEIC/UT | 75.2 |

| Jupiter - China | GB00B1DTDX49 | OEIC/UT | 75.03 |

| Invesco - China Equity (UK) | GB00B3RW8C79 | OEIC/UT | 74.86 |

| FSSA - All China | GB00BZCCYL77 | OEIC/UT | 74.3 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay