It's been quite some time since I've written about ethical investment funds. In fact, it's almost four years since I wrote the research article Are ethical funds any good? The best ethical funds to invest in.

As well as identifying strong performing ethical funds, at the time, the research drew a number of conclusions, including:

- Ethical funds can give decent returns but it is often a result of underlying biases that the ethical fund manager's choices create.

- A bias towards smaller companies or a skew towards financial and technology firms boosted performance. This limits the upside potential in an environment which doesn't favour these biases. Equally during periods which do favour the overweight positions ethical funds outperform, as they did in the UK All Companies sector between 2012 and 2015.

- The number of ethical funds was limited back then.

In the four years since, the demand for ethical investments has seen investor choice grow substantially. For example, the number of unit trust funds that have an ethical mandate has grown from around 84 (back in 2016) to 134 today. If you expand that number to include ETFs with an ethical/sustainable focus then you can add another 249 to the total.

So I thought it was time to review this subset of the investment universe and see how ethical funds have fared. Plus given their often inherent biases how did they perform during the coronavirus sell-off, the fastest bear market in history.

For the purposes of this research, I analysed the long term and short term performance of unit trusts with an ethical/sustainable investment focus. You can see a full list here of all the funds along with the name of the sector in which they reside.

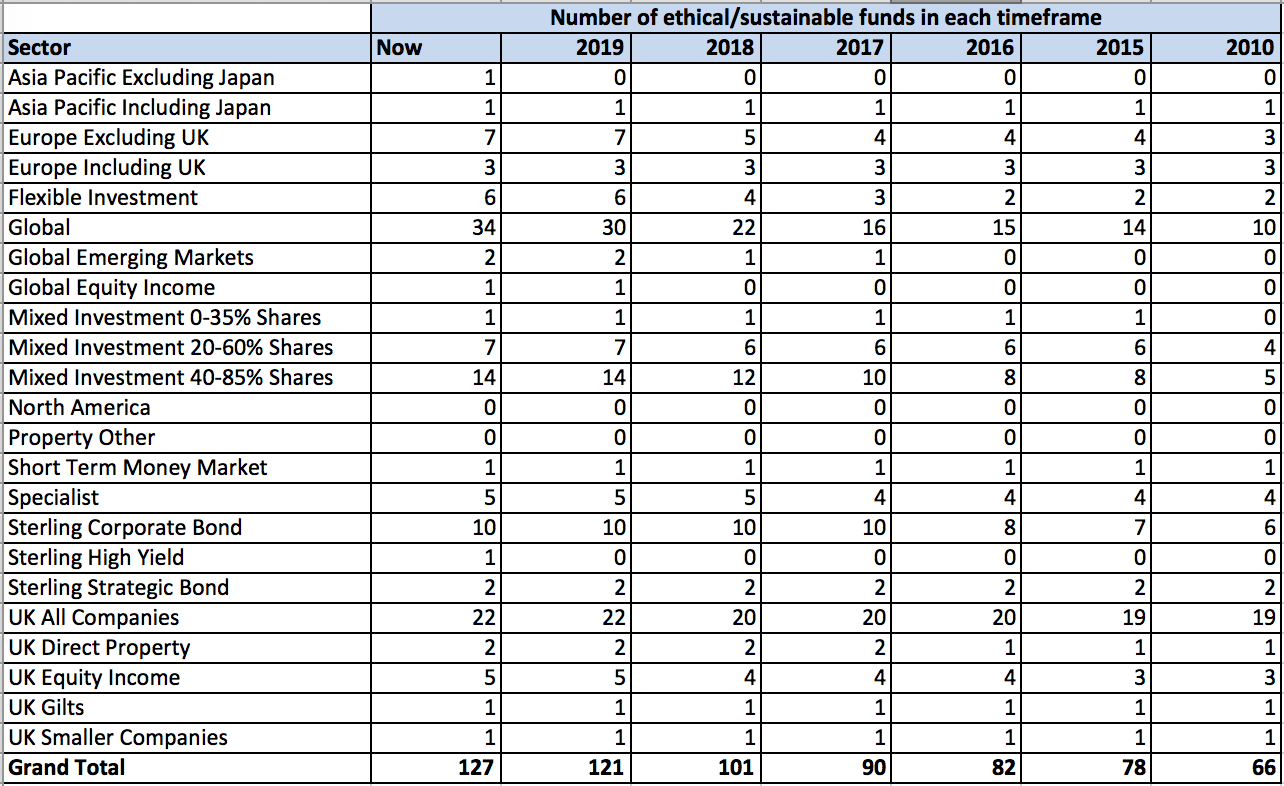

Before I look at the performance of the ethical funds versus non-ethical funds, on a sector by sector basis, the table shows how many ethical funds reside in each sector, and have done over time.

As you can see, some sectors only have one or two ethical/sustainable funds which means that the sample size in those instances is small and therefore any conclusions drawn from analysing the data has far less statistical significance.

Having identified the ethical funds available in each timeframe I analysed the performance of them versus their non-ethical peers over the following time periods:

- The 2020 COVID equity market sell-off (20th February 2020 to 23rd March 2020)

- 1-year cumulative performance

- 2-year cumulative performance

- 3-year cumulative performance

- 4-year cumulative performance

- 5-year cumulative performance

- 10-year cumulative performance

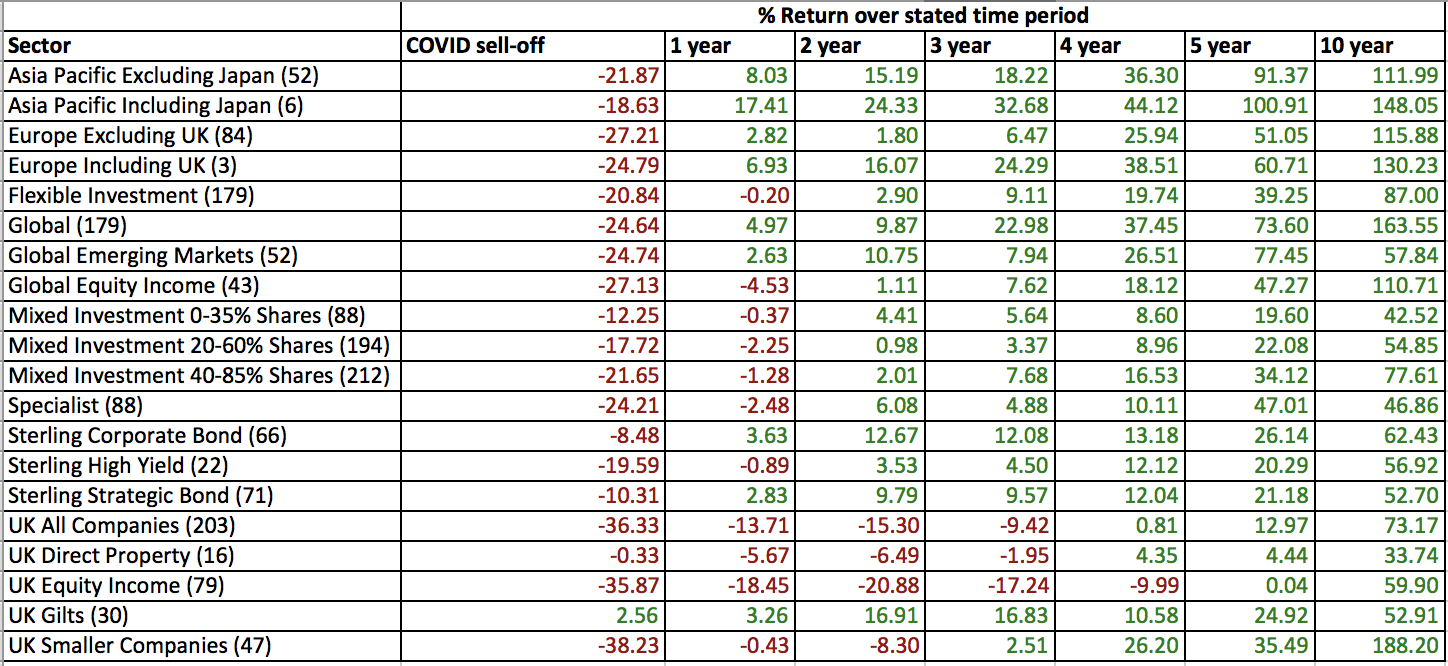

The first chart shows the average performance, across the various time periods for all the non-ethical funds within each sector. The number in brackets beside each sector name represents the number of non-ethical funds currently present in each sector.

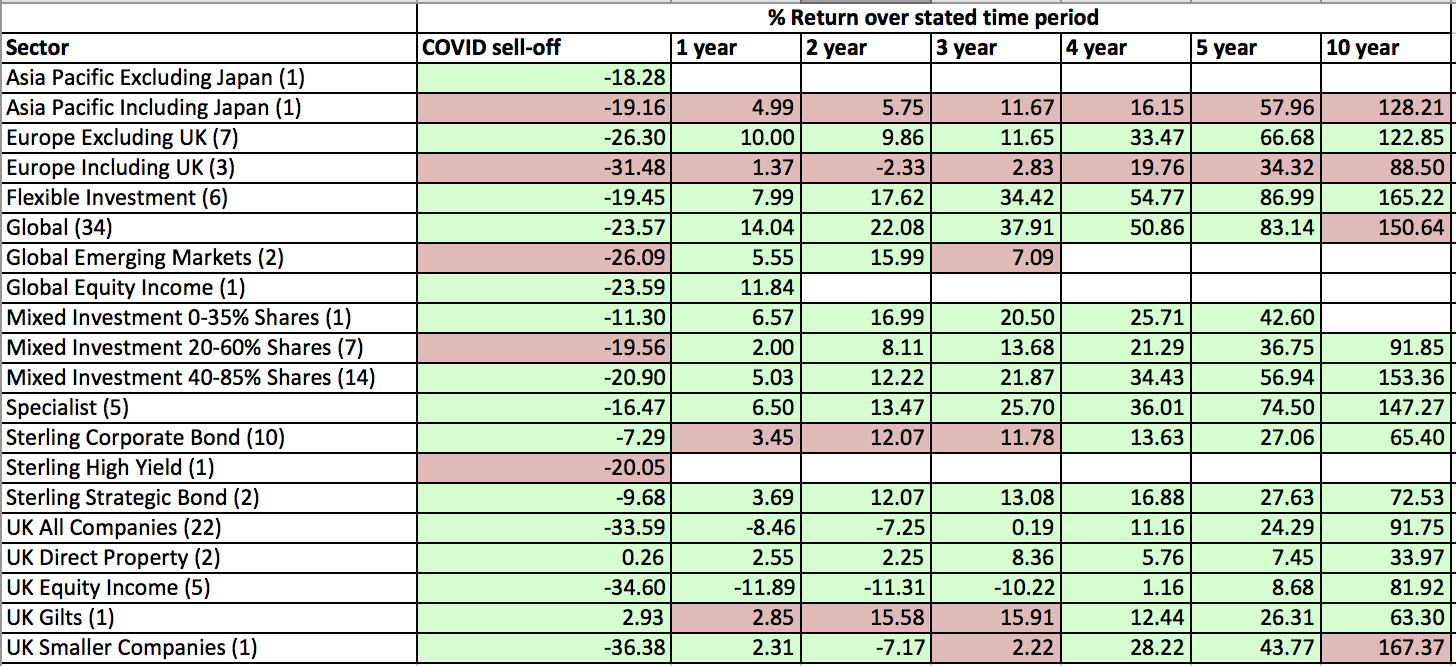

The second table below shows the average performance of the ethical funds over the same time periods for each sector, but where the average ethical performance has bettered the non-ethical peer group performance it is highlighted in green. Conversely, where ethical funds have underperformed this is highlighted in red. The number in brackets beside each sector name represents the number of ethical funds currently present in each sector.

What leaps out immediately is that ethical funds have shown a strong outperformance over their non-ethical peers across all time periods. Where this occasionally isn't true is in sectors where there are only a small number of ethical funds (i.e. one or two). In these instances, it is really a coin toss as to whether ethical funds would outperform or not, so we can almost dismiss them from the conclusions we draw. But if you focus in on those sectors (listed below) where there are a significant number of ethical funds the outperformance is stark (it's almost a sea of green). You can compare the actual performance percentages with the equivalent line in the previous table. The sectors to focus on are:

- Europe excluding UK

- Mixed Investment 40-85% Shares

- Global

- UK All Companies

Only the Sterling Corporate Bond, which has a significant number of ethical funds disappoints. What is interesting is the ethical outperformance during the COVID sell-off as well as the 1-year performance figures. The latter, in turn, helped boost the performance for the other cumulative time periods. If you browse the previously published research pieces below they help to shed some light on why this outperformance might have occurred.

- Are ethical funds any good? The best ethical funds to invest in

- Funds for the pandemic

- Funds for a COVID-19 vaccine

Once again it's the inherent biases within ethical funds that are coming into play. For example, the chart below shows the performance year to date of various UK equity sectors within the UK stock market.

| Sector |

Year to date return %

|

| Electronic Technology | 37.55% |

| Technology Services | 30.19% |

| Retail Trade | 19.74% |

| Health Technology | 13.40% |

| Non-Energy Minerals | 9.67% |

| Miscellaneous | 9.46% |

| Distribution Services | 8.35% |

| Producer Manufacturing | 6.55% |

| Commercial Services | 4.51% |

| Process Industries | −1.18% |

| Consumer Non-Durables | −1.48% |

| Utilities | −6.44% |

| Health Services | −9.35% |

| Consumer Durables | −12.02% |

| Consumer Services | −18.62% |

| Finance | −20.87% |

| Communications | −26.20% |

| Energy Minerals (Oil and Gas) | −26.60% |

| Industrial Services | −30.19% |

| Transportation | −33.17% |

Notice how oil and gas companies as a group are down -26.6% year to date. By contrast, technology-based sectors top the chart with strong performances. The health technology sector also contains pharmaceutical companies like GlaxoSmithKline (GSK) and AstraZeneca. AstraZeneca and GSK are often the largest holdings in many ethical UK equity funds. Take Royal London Sustainable Leaders Trust for example, AstraZeneca is its largest holding and the AstraZeneca share price is up 11% year to date. The impact of COVID-19 on the table above is pretty stark. The price of oil crashed as the coronavirus caused the global economy to stall, which in turn sent the share prices of oil and gas companies crashing. Technology stocks benefited from lockdown and the WFH movement while supermarkets benefited from the increased demand for food (shown by the retail trade sector). Meanwhile, pharmaceuticals benefited from the increased investment in trying to find a vaccine. Transportation (airlines etc) inevitably underperformed as global travel was shut down.

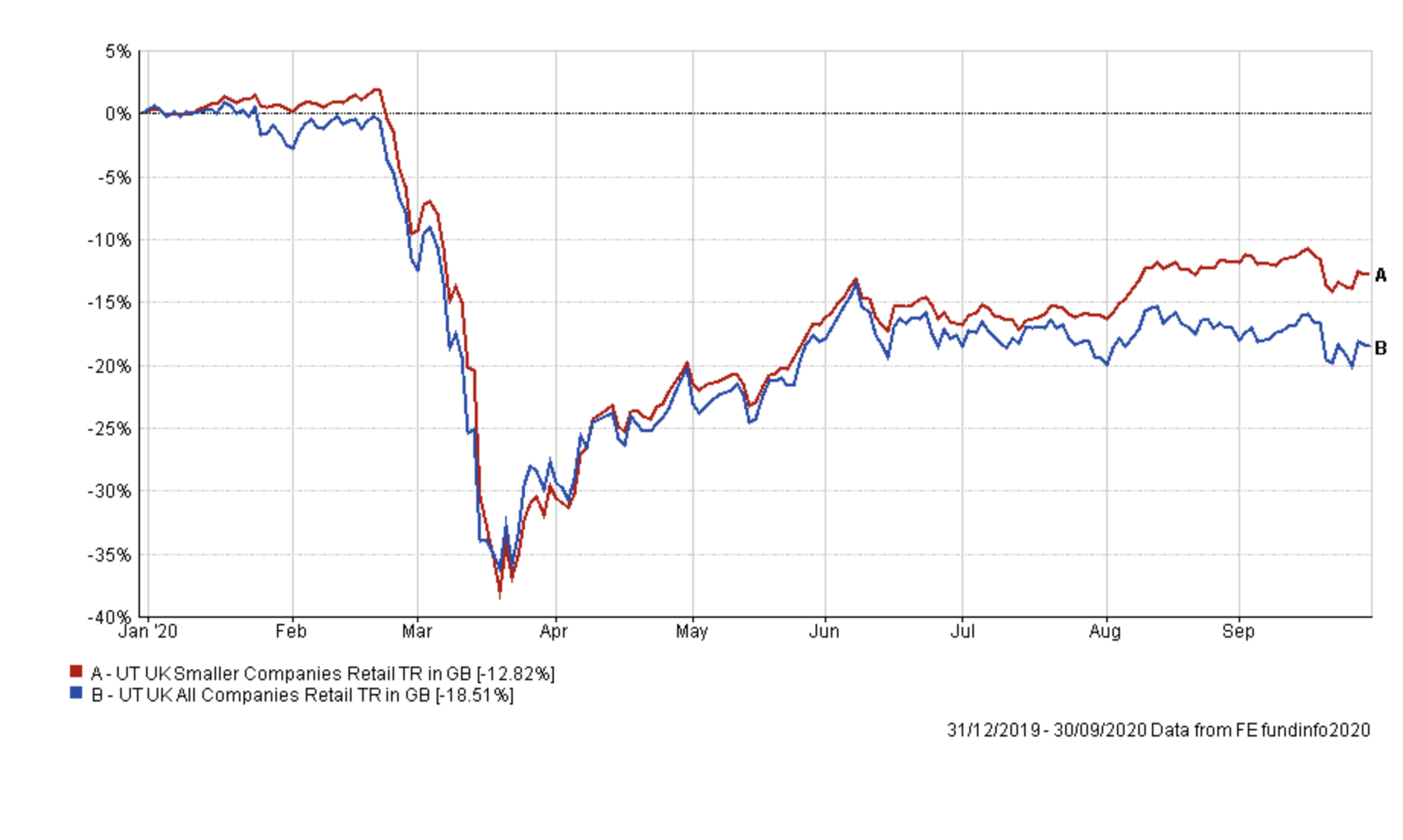

The point is that ethical funds by their nature have favoured sectors that benefited from the pandemic (or were less affected by it). They tend to avoid oil and gas stocks while some funds also avoid airlines. As mentioned in my previous research piece into ethical funds, they tend to also favour small-cap stocks over large-cap stocks. As the chart below demonstrates, UK smaller companies funds have outperformed their larger-cap peers year to date. They performed in line with each other during the COVID crash but smaller companies rebounded as green shoots of economic recovery started to appear. Interestingly, UK smaller companies funds have outperformed the larger cap UK All Companies sector in 7 out of the last 11 calendar years. Again this is another reason why ethical funds have outperformed over the long term too. Also, throw into the mix the fiscal stimulus being announced by global governments worldwide, which has often focused on producing a 'green' recovery, the tailwinds for ethical funds have been kind.

Even in the Mixed Shares sectors, ethical funds have tended to outperform, sometimes by investing in alternative assets. Take the Troy Trojan Ethical fund which I currently hold in my own portfolio, its largest holding is in a Physical Gold ETF.

So to sum up, ethical funds have generally been stronger performers than their non-ethical peers over the short term and longer-term, and have provided a certain amount of resilience to portfolios during 2020. In fact, I have two ethical funds in my own 50k portfolio. The above evidence confirms that the two funds I hold are not isolated incidents of strong performance, but indicative of a wider pattern. Back in 2016, the evidence showed that we should not overlook ethical funds, although their performance is influenced by their inherent style biases. Now in 2020, the environment has benefited these biases and rather than simply trying to not overlook ethical funds, there's an argument for actively choosing them, for now at least. Not because they are 'ethical' but because the investment backdrop has been favouring them.

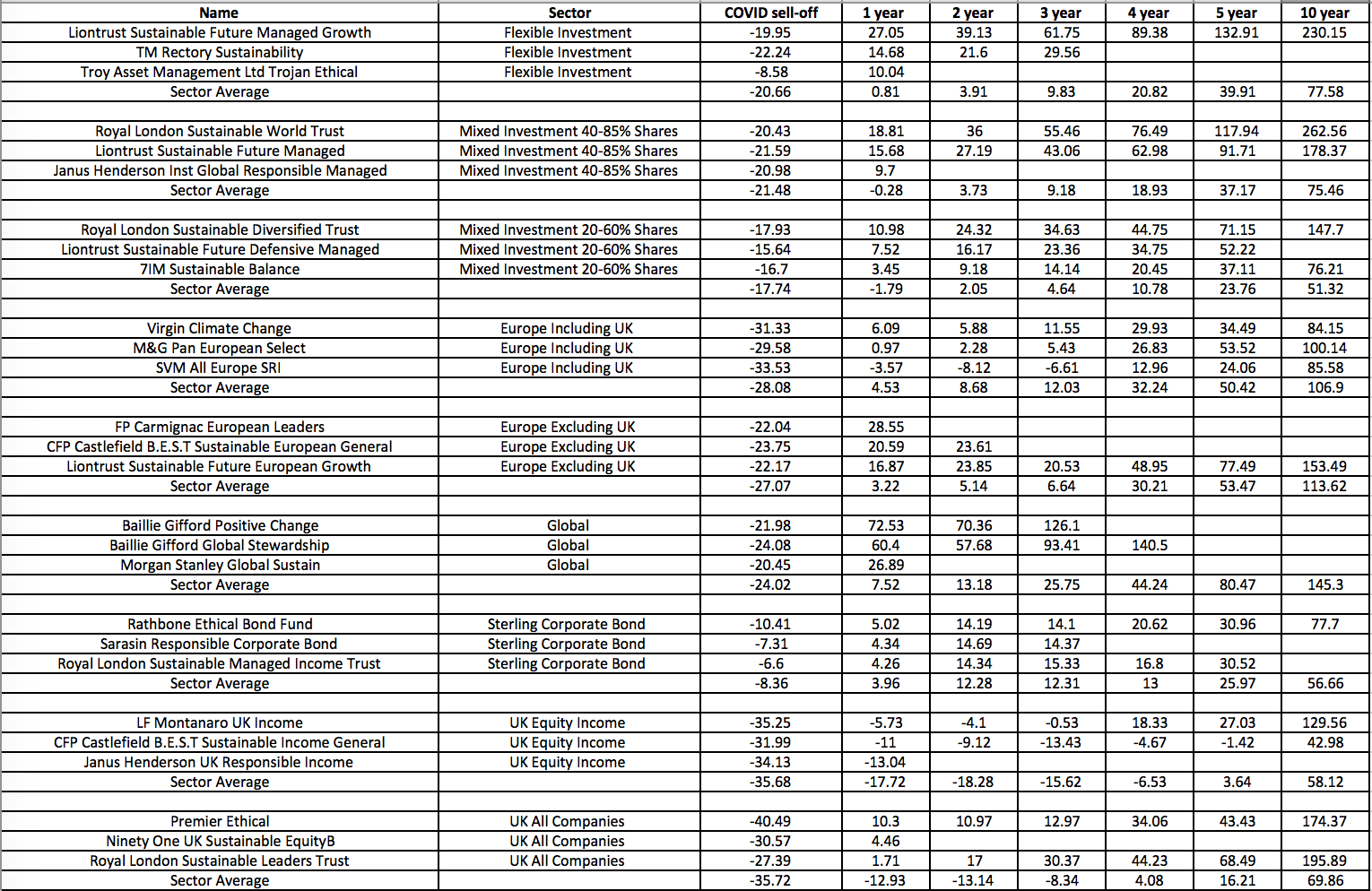

Best performing ethical funds over the last year

Finally, for reference, I highlight the performance of the top 3 performing ethical funds (over the last year) in the sectors that contained three or more ethical/sustainable funds.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay