At Money to the Masses we monitor the best savings accounts available in the UK. It is worth bookmarking our article "Best savings accounts in the UK" which we update every week for future reference. But in a world where you can now get as much as 8% on a regular savings account and 6.2% on a NS&I 1 year fixed-rate bond, understandably investors are starting to look at cash not just as a haven asset or portfolio diversifier but also as a source of positive returns within their investment portfolios.

The issue is that investment platforms have historically not paid much (if any) interest on uninvested cash sitting with them. There are a number of reasons for this. Firstly, platforms often boost their profit margins by not paying interest (or very little) on cash you hold with them, while at the same time pocketing more generous interest payments they earn elsewhere on customer deposits.

Of course, some products, such as insured pensions, don't usually offer the ability to hold money as cash in associated cash management accounts, even temporarily.

In addition, platforms take the view that cash is intended to be invested, which has the added benefit of then allowing the platforms to charge management fees. However, there is also a separate issue that's been caused by regulation, whereby investment platforms have to maintain significantly higher reserves to safeguard clients’ funds invested in what are known as “non-standard” assets. Unfortunately fixed-term deposit accounts (with fixed-terms over 30 days) are usually classified as non-standard assets, meaning that many SIPP providers have decided not to offer these products and their more attractive interest rates to customers.

So assuming that your investment platform doesn't offer fixed-term savings products the aim of this article is to explore some of the potential "cash" options open to investors, the potential returns they might expect as well as the associated risks.

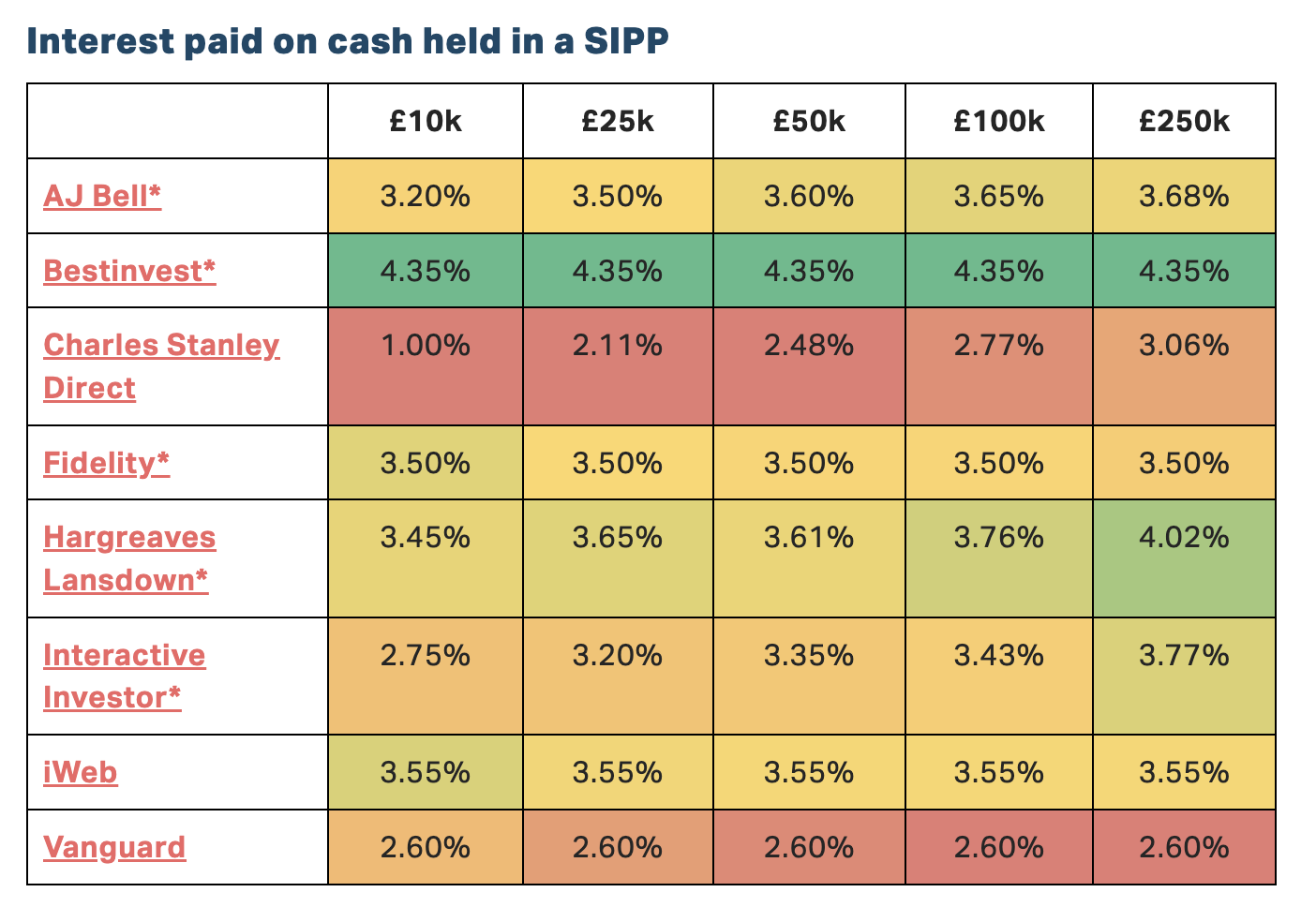

Interest rates paid by investment platforms on cash

The good news is that there has been a movement by established investment platforms to stop charging management fees on cash but also to start paying interest on cash held on deposit within their ISAs and SIPPs. For example in July 2023 Fidelity announced that it would start paying interest on its Cash Management Account and also made a one-off back payment to cover any cash held between July 2022 and June 2023.

However, the rate of interest you earn varies significantly depending on the platform you use, the amount you have invested and whether it is held in an ISA or SIPP. Our tables below summarise the current position for the main investment platforms. I suggest that you bookmark our article "Investment platforms paying the highest interest rate on cash", from which I pulled these tables, as it is regularly updated with the latest interest rates.

The cash rates quoted are the effective interest rate you would receive for the deposit amount stated. Many platforms offer tiered interest rates meaning that you don't receive the same interest rate on your entire deposit. Each column is colour-coded with the most generous interest rate in dark-green and the least generous in dark-red.

So it is possible to earn interest on cash with a number of platforms, with some far more generous than others. However, in many instances the rate remains unattractive.

Money market funds

You may use a platform or investment product that doesn't offer the ability to hold cash or pay interest on deposits. Or your platforms of choice may pay a very low level of interest. For these reasons money market funds have increased in popularity over the last year, particularly in the US where the flood of savers pulling cash from regional banks to invest the cash into money market funds was blamed for the mini-banking crisis earlier in 2023. Likewise in the UK, money market funds have become a much more attractive option for UK investors.

What are money market funds?

Money market funds are collective investment vehicles (unit trusts or OEICs) that focus on short-term debt instruments, such as treasury bills, commercial paper, and certificates of deposit to generate their return. Their aim is provide returns that are competitive with bank deposit rates while ensuring capital preservation and liquidity. However, it is important to understand that they are not the same as cash on deposit and as such there is a small element of investment risk that you can get back less than you paid in.

Pros and Cons of Money Market funds (MMFS)

Pros:

- Stability - MMFs aim for capital preservation, making them less volatile than many other types of investment.

- Liquidity - Investors can usually redeem their stake in MMFs promptly, ensuring quicker access to their money than a fixed-term cash deposit.

- Diversification: - MMFs invest in a variety of short-term debt instruments, reducing the risk of issuer default.

- Competitive "cash-like" returns - MMFs often offer returns that are competitive with, if not better than, traditional bank savings rates.

- Tax - if there are capital gains produced by the fund these will be subject to capital gains tax rather than income tax (as with deposits outside of ISAs or SIPPs).

Cons:

- Interest Rate Sensitivity - MMFs can be affected by sudden fluctuations in interest rates.

- Lower Potential Returns - MMFs are likely to offer lower returns than riskier investment options such as bonds and shares over the long term

- Credit Risk - There's always a risk of issuer default with the underlying cash-like investments, which can impact the MMF's value.

- Market Conditions - Extreme market volatility can pose challenges for MMFs, especially if there's a rush of redemptions (which is a very real risk following their surge in popularity).

How can you lose money with an MMF?

While MMFs strive for stability, there are scenarios where investors might face losses:

- Issuer Default - If a major portion of the MMF's portfolio is in an instrument and the issuer defaults, it can impact the fund's value.

- Market Volatility - Extreme market conditions can lead to a decline in the value of the instruments the MMF holds.

- Rising Interest Rates - A sudden spike in interest rates can decrease the value of existing short-term debt instruments, affecting MMFs.

Is money in a Money Market fund safe?

For UK investors, the Financial Services Compensation Scheme (FSCS) offers a layer of protection. If a financial firm offering MMFs goes under or can't meet its financial obligations, the FSCS can step in to compensate investors. It's crucial for investors to ensure their investments lie with institutions covered by the FSCS, which currently offers protection up to £85,000 per person, per firm.

Which are best Money Market funds

The choice of Money Market funds is relatively limited in the UK, with many platforms only offering one or two options. MMFs reside in one of two Investment Sectors, namely the Short Term Money Market and the Standard Money Market.

The table below shows the performance of the widely available money market funds over different timeframes. The data includes the actual % return over 1 month, 6 months and 1 year. I also include the average annual return over the last 3, 5 and 10 years. Obviously, the annualised numbers are significantly lower than the 1 year % return number as they reflect a period when interest rates were still near record lows. Each column is colour-coded from green to red, with dark green representing the best value for that metric while dark red represents the worst.

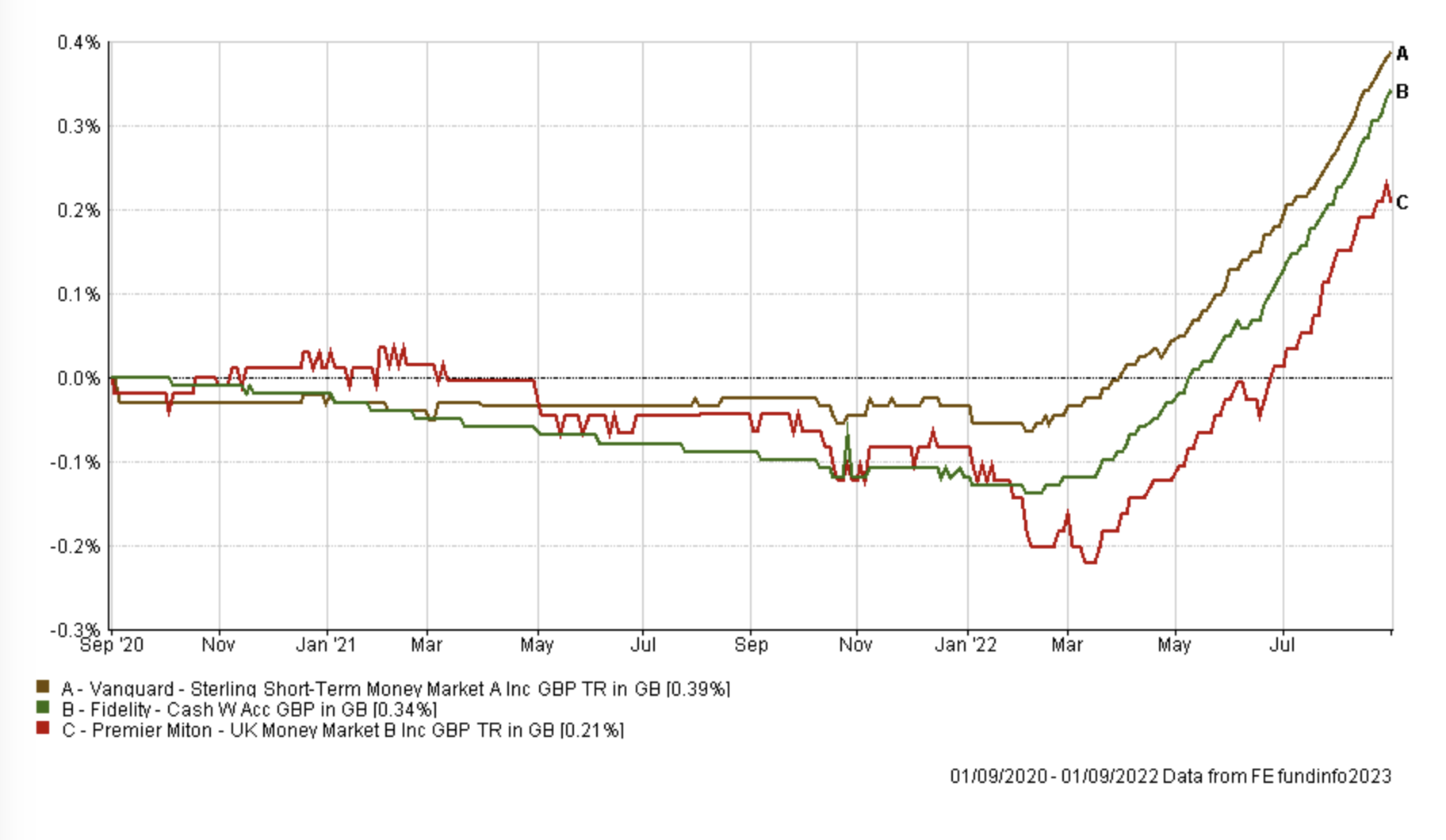

In the table I have also included details of the volatility and number of negative periods to highlight the risks involved when investing in money market funds. Or in other words, unlike true deposits at a bank or building society the value of a money market fund can go down as well as up. In May 2022 the UK financial regulator, the FCA, published a paper looking into the resilience of money market funds. The paper highlighted the stress experienced by MMFs during the market turmoil in March 2020. There were significant outflows from MMFs, and some funds faced challenges in selling assets to meet redemptions. The chart below shows the performance of three of the biggest money market funds, including the one producing the best return in the chart above. As you can see they all fell in value, albeit not significantly. But it serves as a warning to not just focus on the fact that some money market funds have produced better returns than the deposit rates offered by most investment platforms.

For balance, the chart below shows the 3 year performance for the same three cash funds. As you can see the performance has significantly improved over the last three years, as central banks increased interest rates.

Gilts

For those looking for a guaranteed return on cash, directly investing into short-term gilts has also now become an attractive proposition. Gilts are essentially IOUs issued by the UK government, a promise that they will repay your money with interest. They’ve always been considered a safe investment option because the likelihood of a UK government default is small. However, beyond their security, they can offer attractive short-term returns when held to maturity.

A real example of a short-term gilt issued a few years ago with a face value of £100 is due to mature in 2025. It provides a modest interest or 'coupon' of 0.625%. During the summer of 2023, and due to the fluctuating interest rate environment, the gilt's market price dropped to £91.35. This meant that if someone had invested (purchased) the gilt at that price and then held it until maturity in 2025 they would have effectively locked in an annual yield of 5.4%, once they factor in the small coupon and the final repayment of the original £100 face value.

Hargreaves Lansdown for example has responded to the surge in interest in short-term gilts by making them more readily available to invest in on their platform.

However, gilts are particularly interesting to higher-rate income tax payers when held outside of tax-wrappers such as a SIPP because capital gains from gilts are tax-free. In the above example because the majority of the return comes via the untaxed capital gain, as opposed to the income taxable interest payments, a higher-rate income tax payer can achieve a guaranteed post-tax return of around 5.15%.

Of course the price of gilts fluctuates and the volatility can be daunting, but for those who are able and willing to hold onto their investment until maturity, it is possible to achieve an attractive post-tax return which is 100% backed by the UK government.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay