As promised in my last weekly newsletter I will answer the following question in detail. It was asked by an 80-20 Investor member in November's Chatterbox but warranted a greater explanation and a wider airing. The question was:

Within my portfolio I have quite a high allocation to non UK investments. As the dollar has appreciated against sterling these investments have done pretty well. Trouble is I’m now reluctant to invest in overseas funds as I fear sterling will likely recover some of its lost value.

How do you see the best way of dealing with this?

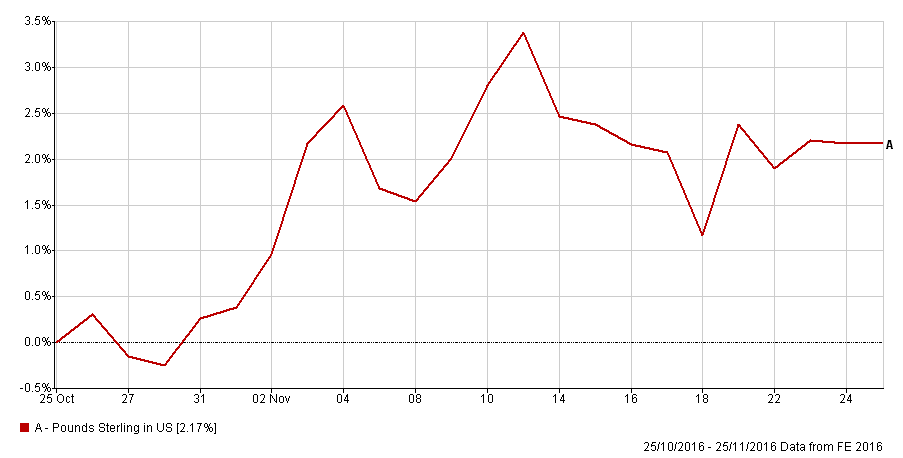

Many of you may be wondering why anyone would be concerned given that we are seeing headlines stating that the dollar has hit 13 year highs. However the dollar strength in this instance is being measured against a basket of currency market peers. As a UK investor we are most interested in the direct relationship between sterling and the US dollar. The chart below shows the spectacular 17% fall in the value of the pound versus the dollar over the last 12 months thanks to the EU referendum. Click the image to enlarge it.

If we zoom into the last month you can see that despite the headlines the pound has actually strengthened by over 2%.

In this article I am not going to speculate over the future direction of the GBP/USD exchange rate but suffice to say that at some point the downward trend will have gone too far before it finds a new state of equilibrium and possibly rallies. Whether that will be soon or in the future is the topic for another time. However, 80-20 Investors have enjoyed the profitable ride downwards but how do you avoid losing those profits if the pound suddenly bounces?

Go native

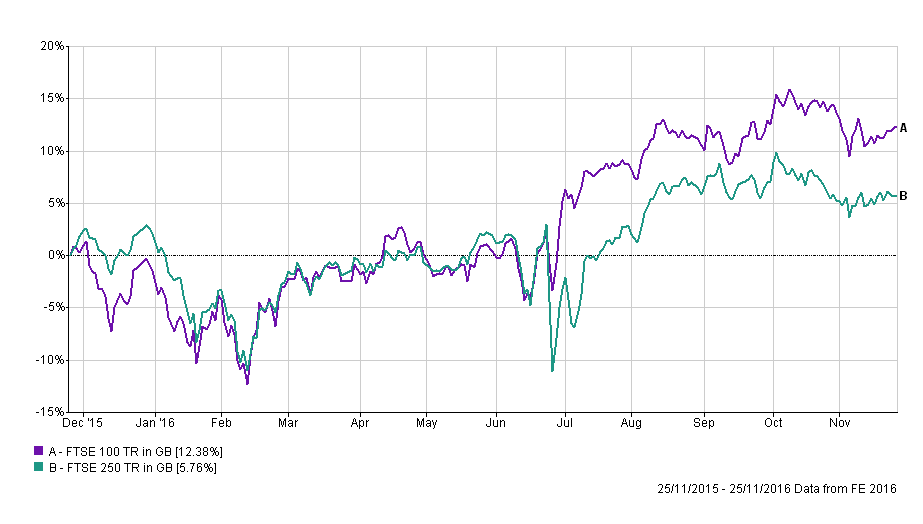

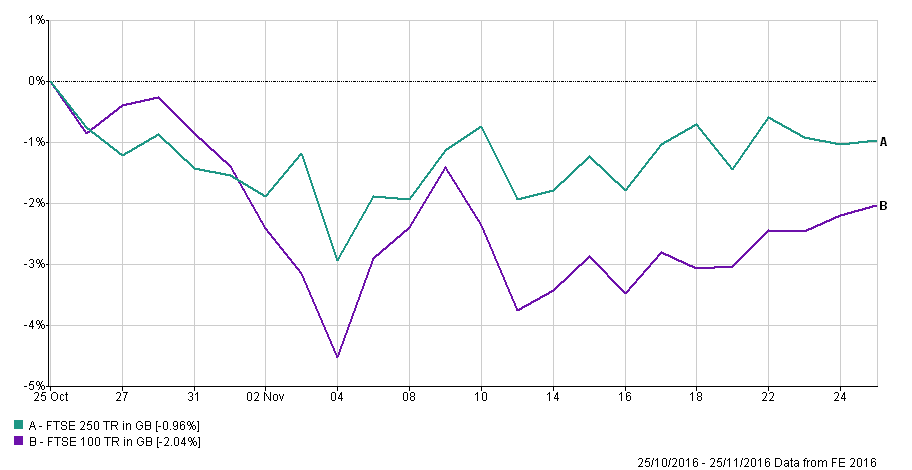

You can never completely remove the impact of currency moves as they have both direct and indirect consequences. If we consider the direct consequence first of all logic dictates that you do not want to hold anything denominated in dollars if you think that the pound is going to rally. That is because when you convert the dollar denominated asset back into pounds it will have fallen in value. One tactic is to only hold sterling denominated assets. So in terms of equity exposure that will mean investing in UK equities. However the indirect impact of a weak pound is that it favours exporters or those companies that earn money in dollars. So conversely if you think that the pound will weaken you are predicting that we will see outperformance of large cap stocks (FTSE 100) over more domestically focused UK smaller cap stocks (think FTSE 250 and below). The first chart below (click to enlarge) shows the outperformance of the FTSE 100 over the last year (when the pound weakened) while the second chart shows the reverse during last month's sterling recovery:

FTSE 100 vs FTSE 250 over 1 year

FTSE 100 vs FTSE 250 over 1 month

So one strategic move would be to focus more on UK smaller companies funds. Unsurprisingly if you rank the average performance for every fund sector over the last month UK smaller companies funds lie third and are the only sector outside of the US to be in positive territory.

| Sector | 1 month return |

| North American Smaller Companies | 5.23 |

| North America | 1.1 |

| UK Smaller Companies | 0.03 |

| Cash | 0.01 |

| Targeted Absolute Return | -0.88 |

| Sterling High Yield | -1.2 |

| UK All Companies | -1.46 |

| Sterling Strategic Bond | -1.72 |

| UK Equity Income | -1.74 |

| Sterling Corporate Bond | -1.97 |

Sterling's rally also helps explain why so many UK focused sectors inhabit the top spots. Over the last year at the same time as the fall in the value of the pound bonds have rallied. Now this isn't a simple case of cause and effect. A weak pound might suggest concerns around the outlook for the UK economy which is ultimately good for bond investors. The problem is that at some point the market narrative flips over to 'a weak pound means that the cost of imports will rise and inflation will spike which will require the Bank of England to raise interest rates, which of course is bad for bonds and their fixed interest payments'. These indirect relationships are often muddied by the narrative currently accepted by market participants. As I've pointed out in recent newsletters narratives are subject to sudden change without any warning. Think of investment markets like a pile of coloured ropes. The only thing you know for sure is that if you pull one end of a coloured rope the other end of the same coloured rope will move. This is like the GBP/USD exchange rate. However when you pull the rope hard the whole knotted pile shifts because all the ropes are interwoven. This is similar to the indirect relationships between currencies and all other assets including equities. It's impossible to untangle. It also highlights that currency pairs don't move independently of each other. The EUR/USD rate will have some bearing on the GBP/USD rate.

Hedge

So if we forget about indirect exposure to currencies, in this case the pound, another way of mitigating its influence on your returns, without going native as described above, is to hedge your portfolio. The simplest way to do that is to buy hedged funds. By way of example the Legg Mason IF Japan Equity fund has a hedged and unhedged version of the same fund and the impact of currency on returns is clear to see over the last year.

However a lot of funds don't offer a hedged version of their fund, or if they do then UK platforms don't give access to it. Then of course there is the issue of funds that do hedge all or part of their currency exposure but you have no way of knowing. One such example is Neptune Japan Opportunities. Ask most professional fund commentators and they wouldn't be able to tell you whether a fund is currency hedged or not. As a rule most funds investing outside of the UK don't hedge currency risk, especially global funds, because the cost of hedging out multiple currencies becomes too prohibitive. So you tend to only see it in funds with a single geographical focus. The issue is muddied further as there is no easy way to see whether a fund is currency hedged. The fund manager seldom even mentions it on their fund factsheets. Historically the only way to find out is to call up the fund house and ask if they hedge out currency risk, which isn't feasible when there are around 2,000 funds available to the UK investor.

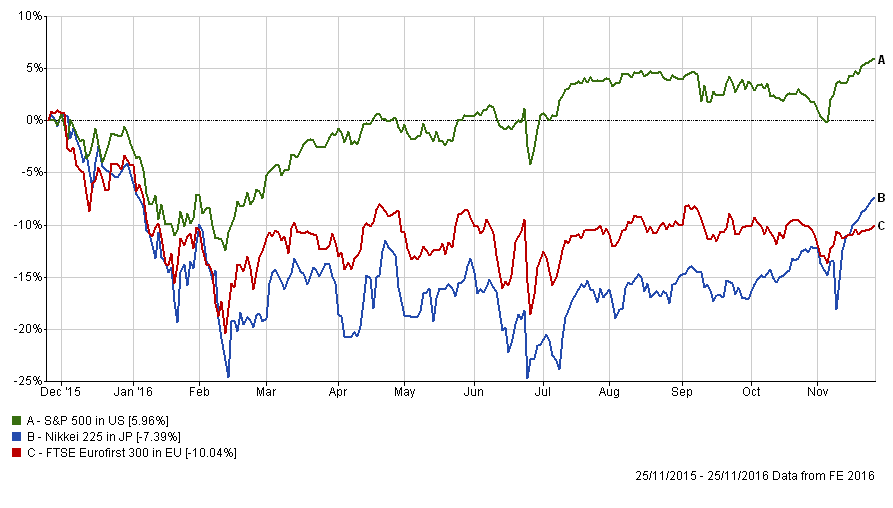

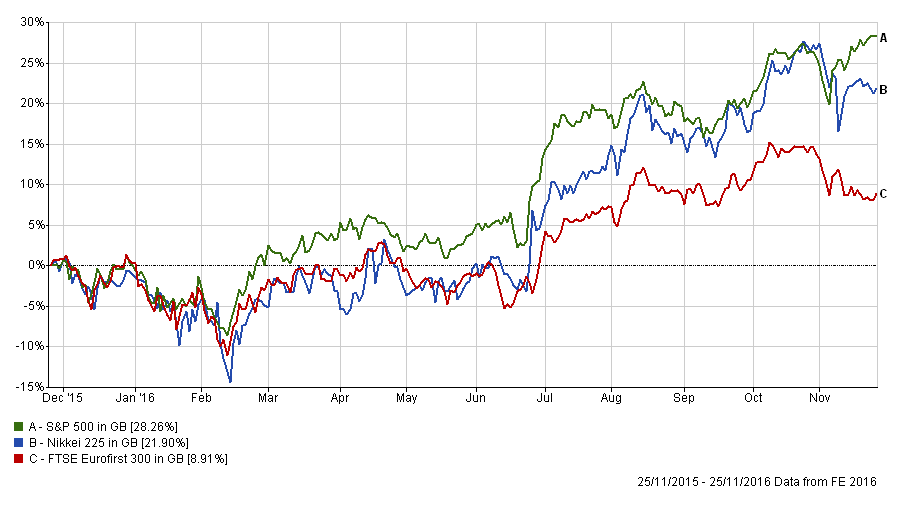

However I am going to give you a tip to quickly work out whether a fund is currency hedged or not. Firstly if you look at the chart below it shows three key stock market indices based in their own currencies (namely the dollar, euro and the yen).

Now here's the same chart but this time with it rebased into pounds (as it would be for a UK investor)

You will notice that in the second chart (which is repriced back into pounds) there is a big spike at the time of the UK referendum. This is because sterling fell by around 10% in the immediate aftermath. In essence the first chart shows what would happen if you'd invested in the stock markets and hedged out the currency exposure. The second chart is unhedged.

This spike in June is repeated on the charts of investment fund performance. Ordinarily you can't tell if a fund is currency hedged by looking at a single chart of its performance. You'd need numerous charts like the above to compare. However so extreme was the reaction to the EU referendum that the main contributor to investment returns at the end of June, when investing overseas, was the fall in the pound. So if you chart the performance of the Neptune Japan Opportunities fund vs AXA Framlington Japan you can see the former is currency hedged while the latter isn't.

So going back to your question, if you want to reduce your exposure to a weak pound versus the dollar then use your platform (Hargreaves Lansdown etc) to chart a fund's performance over the Brexit vote period. Then chose one where there wasn't a spike in returns coinciding with sterling's collapse. One thing to bear in mind is that just because you put out the GBP/USD fire another might spring up elsewhere in terms of the GBP/yen exchange rate. So you could find you are chasing your tail trying to reduce the impact of the pound's move against the dollar.

The downside to currency hedging is that it costs the fund managers money to implement so it drags on your returns. For those investors who in the short term want a cheap tracker fund that hedges out the currency exposure to a given market then you can buy ETFs that do this. Here is a list of some from ishares.

Bet on it

If you are strong in your belief that the pound is going to rally against the dollar then you can even profit from the move from buying a currency ETF long GBP / short USD. This is incredibly risky but can be used as an insurance policy against a sudden rally in the pound. How you determine the size of your holding will depend on your exposure to the GBP/USD exchange rate. Of course there are leveraged versions of most currency ETF's such as - 3x Short USD Long GBP for example which would enable you to reduce the size of your hedge holding required. The problem is that you would also then magnify your losses if you are wrong about the path of the GBP/dollar exchange rate. I always suggest that DIY investors steer clear of trying to directly play the currency markets as they can quickly move against you and destroy your portfolio

Roll with it

Ultimately you are never going to predict the currency exchange rate accurately. Also there is the age old problem:

If you do hedge out your exposure to the pound versus the dollar, how do you know when to remove the hedge

The above strategies are pre-emptive measures which DIY investors can use. As I run my £50,000 portfolio based upon the 80-20 Investor algorithm it means that I hedge and unhedge my currency exposure when the momentum is with either strategy. This is not hypothetical, you can read exactly how earlier this year I removed the yen currency hedge in my article Damien Portfolio update: The first year & some changes. For ease I've replicated it below including the chart

----

...A big theme in the coming months will be currency exposure. Often it is best to hedge out currency exposure so you only get exposure to the underlying asset and not any currency moves. For example in Japan the main equity indices tend to move in the opposite direction to the strength of the yen. So when the Yen weakens the Japanese stock market rallies because exporters have a strong influence on the economy. A weaker yen makes their exports cheaper in 'foreigners' eyes and so they will buy more - hence the Japanese stock market tends to rally. The problem is that normally if you have an unhedged Japanese equities fund then what you make on the stock market you lose on the falling currency. Think about it..... lets say you bought 100 yen's worth of Japanese equities by converting your english pounds in yen. Now lets say the value of those shares in yen terms remained the same but the yen fell against the pound. When you sell your 100 yen's worth of shares and convert the proceeds back into pounds you will lose money as your yen will buy less pounds. So even if your shares go up in value in yen terms, if the currency depreciates more quickly you will still make a loss.

However, the impending UK EU referendum has caused the pound to tumble against most major currencies. Therefore those who had unhedged Japan funds made greater profits. The chart below shows how the unhedged version of the same Japan fund, which I've switched into, has outperformed the hedged version. Obviously this differential won't necessarily always persist and when it's better to hedge once again the 80-20 Investor algorithm will pick this up.

----

This chart below shows how that trade played out for the rest of 2016 and why unhedged Japanese equity exposure has been a very profitable trade for my £50,000 portfolio. So you can see that I will hedge out my exposure to the pound as of when the trend is picked up by the 80-20 Investor algorithm. It will mean that I won't necessarily catch the start of the trend but hopefully it will mean I avoid any false dawns. Interestingly since the US election the strong dollar vs yen has meant that the Japanese stock market has rallied, however UK investors would have been better off hedging out their currency exposure. Over the last month in yen terms the Nikkei 225 is up 5.2% but unhedged UK investors are down -3.3%. So the time for hedging may be close at hand.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay