An 80-20 Investor recently asked a question via Chatterbox about selecting multi-asset funds as part of a buy and hold strategy. The member posed the interesting question of whether they could assume that all multi-asset funds have a good geographical spread?

My knee-jerk answer would be no, but having said that I have not researched the geographical spread of multi-asset funds to give a definitive answer. After all we should always favour facts over opinions. So I decided to look into the geographical spread and diversification of multi-asset funds because after all they are often marketed as a fund for buy and hold investors. But how diversified are they really?

What is a multi-asset fund?

A multi-asset fund is a fund that holds more than one asset type. Technically an equity fund that holds cash could be deemed as having more than one asset. While this is an extreme example it does show the dilemma investors face in determining what constitutes a multi-asset fund. Modern portfolio theory results in most managed funds being a combination of bonds and equities. In effect, they are duel-asset but would fall under the umbrella of multi-asset as they hold more than one asset type. However, in the last decade the term multi-asset became a marketing buzzword which translated into investment funds deliberately labelling themselves as multi-asset and being run as such. These funds typically branched out from the usual bond/equity mix and included assets such as property. However, fund labels are notoriously misleading and some multi-asset funds aren't explicitly marketed as such.

The first problem you face is how do you identify multi-asset funds given that they don't have their own sector? A good starting point for sourcing multi-asset funds are the following sectors as multi-asset funds almost exclusively reside in them:

- Flexible Investment

- Mixed Investment 0-35% Shares

- Mixed Investment 40-85% Shares

- Mixed Investment 20-60% Shares

There is the odd multi-asset fund in the Targeted Absolute Return sector but usually the fund factsheets are not explicit about the types of assets they hold. In most cases the asset classes remain limited and they instead apply investment strategies aimed at managing downside risk, which is a different proposition to normal multi-asset funds.

The above sectors contain a total of 656 funds. I then analysed the asset mix of each fund to determine what percentage of the fund is held in each of the following asset classes

- Alternative Assets

- Commodities

- Equities (but split by how much is in American Emerging Equities, North American Equities, Asia Pacific Equities, Asia Pacific Emerging Equities, Japanese Equities, European Equities, European Emerging Equities, UK Equities, International Equities, and Global Emerging Market Equities)

- Fixed Interest (split by American Emerging Fixed Interest, Asia Pacific Emerging Fixed Interest, European Emerging Fixed Interest, UK Fixed Interest, UK Corporate Fixed Interest, UK Gilts, UK Index-Linked, and Global Fixed Interest)

- Property

- Cash

These categorisations are what fund managers use when reporting how they invest their assets. For the purposes of defining what constitutes a multi-asset fund I grouped certain asset categories together. So all equity classes are put together and so are all the respective bonds categories. The reason I did this is because a fund that invests 100% in equities across the globe may be diversified but it only holds one asset type, namely equities. So it is not multi-asset. This explains why I only have 6 asset classes highlighted above in bold.

Furthermore, when considering what defines a multi-asset fund I discounted cash as an asset class. While I do view cash as an asset class and invest in it myself (as you have seen from my own £50,000 portfolio) fund managers typically only hold a tiny portion of cash for transactional/liquidity purposes. It rarely rises above 5-6% of a fund's assets. So because most funds are not using cash to diversify their portfolios I only considered the other 5 asset classes listed above namely Alternatives, Commodities, Equities, Fixed Interest and Property when determining whether a fund is multi-asset or not.

In order for a fund to meet my definition of multi-asset it had to invest in 3 or more of these asset classes. That left 350 funds, which means almost a half of my original universe was removed. Interestingly the funds listed below are marketed as multi-asset but in reality are just a mix of bonds and equities. It goes to show, never trust a fund name or the associated marketing.

- City Financial Multi Asset Dynamic

- BlackRock Global Multi Asset Income

- MI Charles Stanley Multi Asset 1 Defensive

- Investec Global Multi-Asset Total Return

- Zurich Horizon Multi-Asset V

- Aberdeen Multi Manager Multi Asset Distribution Portfolio

- Schroder Dynamic Multi Asset

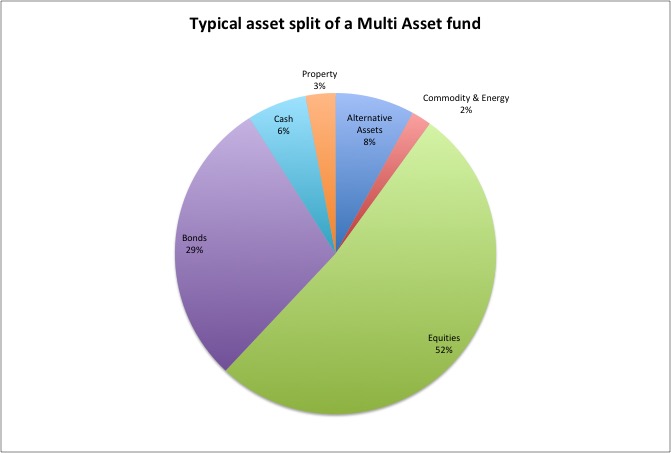

Of those multi-asset funds that are left, you can start to build up a picture of how a typical multi-asset fund is invested. I analysed each fund to determine an overall average asset mix for a typical multi-asset fund. Or in other words, the chart below shows the asset mix if you invested equally across all 350 of my multi-asset funds (click on the image to enlarge it).

What the pie chart demonstrates is that multi-asset funds are typically just bond/equity funds with only around 13% of the fund invested in other assets. I've ignored the cash component from this 13% because as I highlighted earlier a lot of funds hold the level of cash shown above for liquidity reasons. For example, CFP SDL UK Buffettology Fund (which is an equity-only fund currently in the BOTB) has around 9% in cash. Admittedly that is fairly high but it illustrates my point.

With most multi-asset funds you are typically getting a balanced managed portfolio but rather than a 60/40 bond/equity split they invest a small portion in other assets, mostly commodities and absolute return strategies (alternative assets). That will be disappointing to a lot of investors and does little to dispel the view that most multi-asset funds are just tinkering at the edges of their portfolio.

Having said that, the above chart does mask the range of asset mixes that do exist. While most multi-asset funds have an asset mix reminiscent of the above chart there are outliers. The maximum exposure a single fund has to UK Fixed Interest is 78% while the largest cash weighting of any fund is 38% (which seems slightly unbelievable). The largest single exposure to commodities is 19% as is the largest exposure to property. The message is that before you invest in a multi-asset fund look under the bonnet (i.e. read the factsheet) to see where it is invested. You can't just assume that they all invest in the same way. The above chart will prove useful as a benchmark when looking at any multi-asset fund. By using it you can see whether a fund manager is backing their convictions or simply hugging the benchmark asset mix.

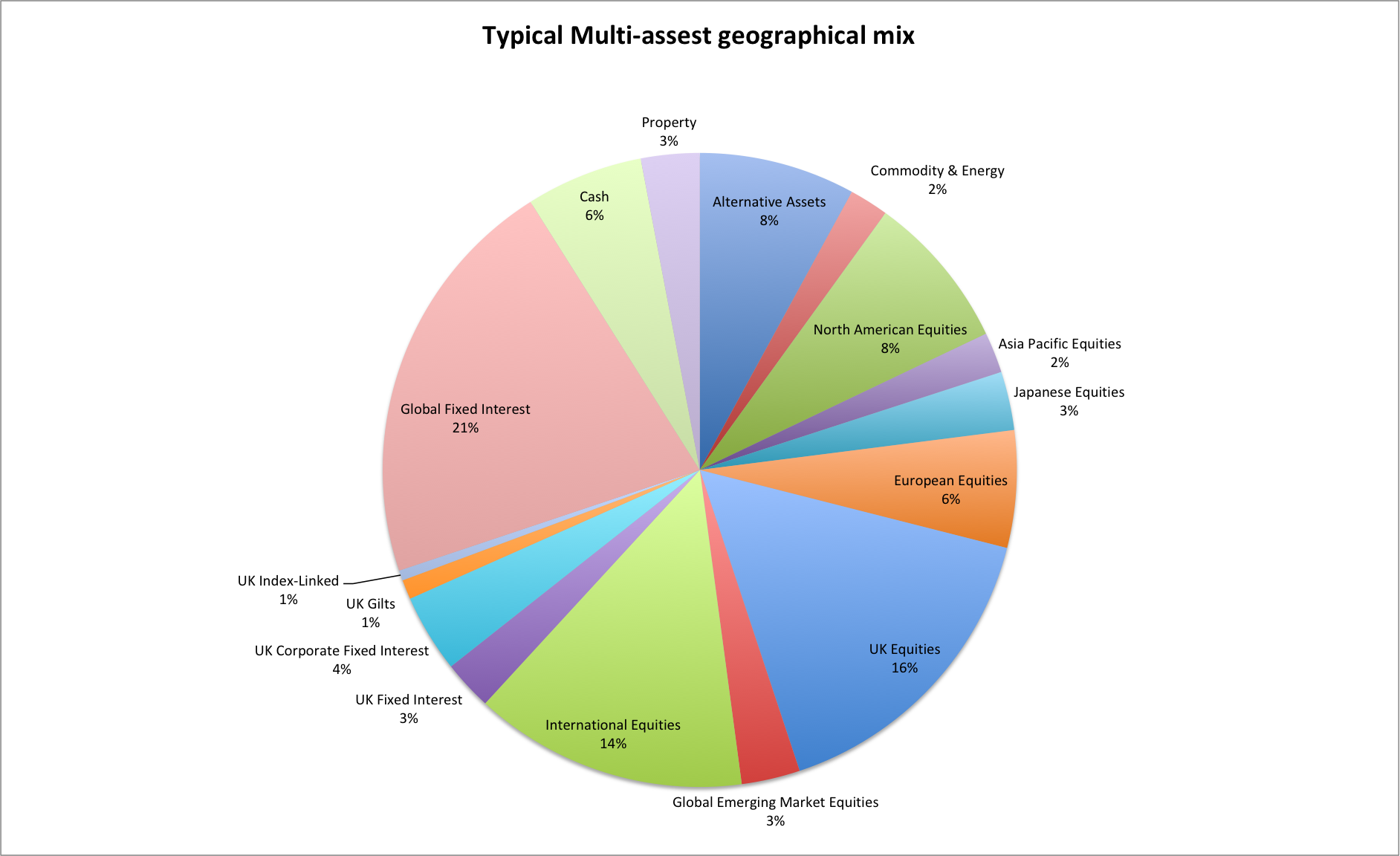

The next question is how globally diversified are multi-asset funds? Taking the above analysis further I drilled down into the geographical mix of each asset class. Once again I produced a typical geographical/asset mix as shown in the chart below, you can click on the image to enlarge it.

Geographically a typical multi-asset fund has a wide global spread, however, there are a few observations to be made:

- they typically favour UK equities and UK assets over global assets

- they have almost no exposure at all to emerging market assets (fixed interest or equities) which is surprising

- they have very limited exposure to Asian equities

- they favour developed world equities

- Outside of the UK, US assets are the next port of call. Presumably, a fair chunk of what is classed as 'International equities' will, in fact, be US equities.

The overarching sense you get from multi-asset funds is the lack of conviction in their portfolio construction. That could partly be a result of the way they are marketed as being focused on capital preservation. It also explains why multi-asset funds don't make regular members of the BOTB, they just aren't dynamic enough. However, there are always exceptions to every rule.

How to find a well diversified multi-asset fund to buy and hold

- The first step would be to look at the 80-20 Investor BOTB and BFBS tables for the sectors mentioned earlier. Alternatively, you could use your investment platform or a service like Morningstar to rank funds within these sectors by a metric you choose, such as performance. This will give you a shortlist of top performing funds.

- Now download this spreadsheet which I produced as part of this research article. It shows those funds within the aforementioned sectors that invest in at least 3 asset classes (excluding cash). The spreadsheet also tells you how many different asset classes each fund invests in as well as which ones. You can then cross-reference this list with the shortlist that you produced in the last step to select the multi-asset funds. If a fund is not in the spreadsheet it is not truly multi-asset but just a mix of bonds and equities (or doesn't disclose sufficient asset data to analyse).

- By this point, you will likely have a shortlist of funds you are interested in or perhaps none at all. If it's the latter it highlights the fact that multi-asset funds' lack of dynamism often means that their performance is found wanting. Assuming that you do have a shortlist of funds, now look at each fund's asset mix (via your fund platform or by searching for its fund factsheet) and compare the asset mix and geographical spread to that shown in the pie charts above. This will give you a steer as to how well diversified the fund is and whether the manager is strategically positioned.

- Finally, multi-asset funds are popular as they are seen as a simple way to diversify a portfolio in order to minimise downside risks. So I suggest that you input your chosen funds into the newly updated 80-20 Investor stress test tool to see how they have performed versus their peers in periods of market stress and to see the risk/return metrics (i.e the sharpe ratio).

- Finally, if you are wondering whether there is multi-asset fund that has produced consistent returns then, unfortunately, the answer is 'no' as shown by their absence from my research piece 'funds for consistent returns'. It just goes to show that despite the heavy marketing there is not a multi-asset fund that provides a single fund solution to investing over the long term.

Ultimately if you want a portfolio that is diversified and multi-asset you are better off, from a performance perspective, choosing individual funds for each asset type yourself, much as I do for my own £50,000 portfolio. Also, a lot of the best performing funds from the four sectors I analysed above are just a mixture of bonds, cash and equities (i.e. they are not true multi-asset funds). Many of these have been consistent members of the 80-20 Investor tables. In fact, I hold some in my current portfolio as core holdings. Premier Diversified has historically been a great case in point.

As a result of this research, I have seen little to convince me that most multi-asset funds aren't just expensive marketing products. If not that, then they certainly aren't living up to the hype.

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions, Privacy Policy and Disclaimer. Neither MoneytotheMasses.com or 80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested. Information provided by MoneytotheMasses.com and 80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions. Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com and 80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions. The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay