With two weeks to go until the UK general election markets are getting twitchy about its potential impact on assets. Two and a half years ago Theresa May called a snap election in an attempt to secure a parliamentary majority. It sounds oddly similar to what Boris Johnson is now doing in 2019. Ultimately Theresa May's decision backfired and resulted in a hung parliament. Ahead of the 2017 election, I pulled together a research article looking at the potential impact of that general election. With the benefit of hindsight, I thought now is an opportune moment to dust down the research and update it. What does history tell us to expect?

Pre-election equity rally

The table below, adapted from one produced by IG Index, shows how the UK stock market has reacted in the lead up to each general election since 1987.

| Year | Polling prediction | Winning party |

FTSE 100 gain or drop

|

| 1987 | Conservative majority | Conservative | +9.70% |

| 1992 | Hung parliament | Conservative | -4.90% |

| 1997 | Labour majority | Labour | +4.40% |

| 2001 | Labour majority | Labour | +1.40% |

| 2005 | Labour majority | Labour | -0.40% |

| 2010 | Hung parliament | Conservative coalition | -8.15% |

| 2015 | Either party could win a majority | Conservative | -0.10% |

| 2017 | Conservative majority | Conservative coalition | +2.94% |

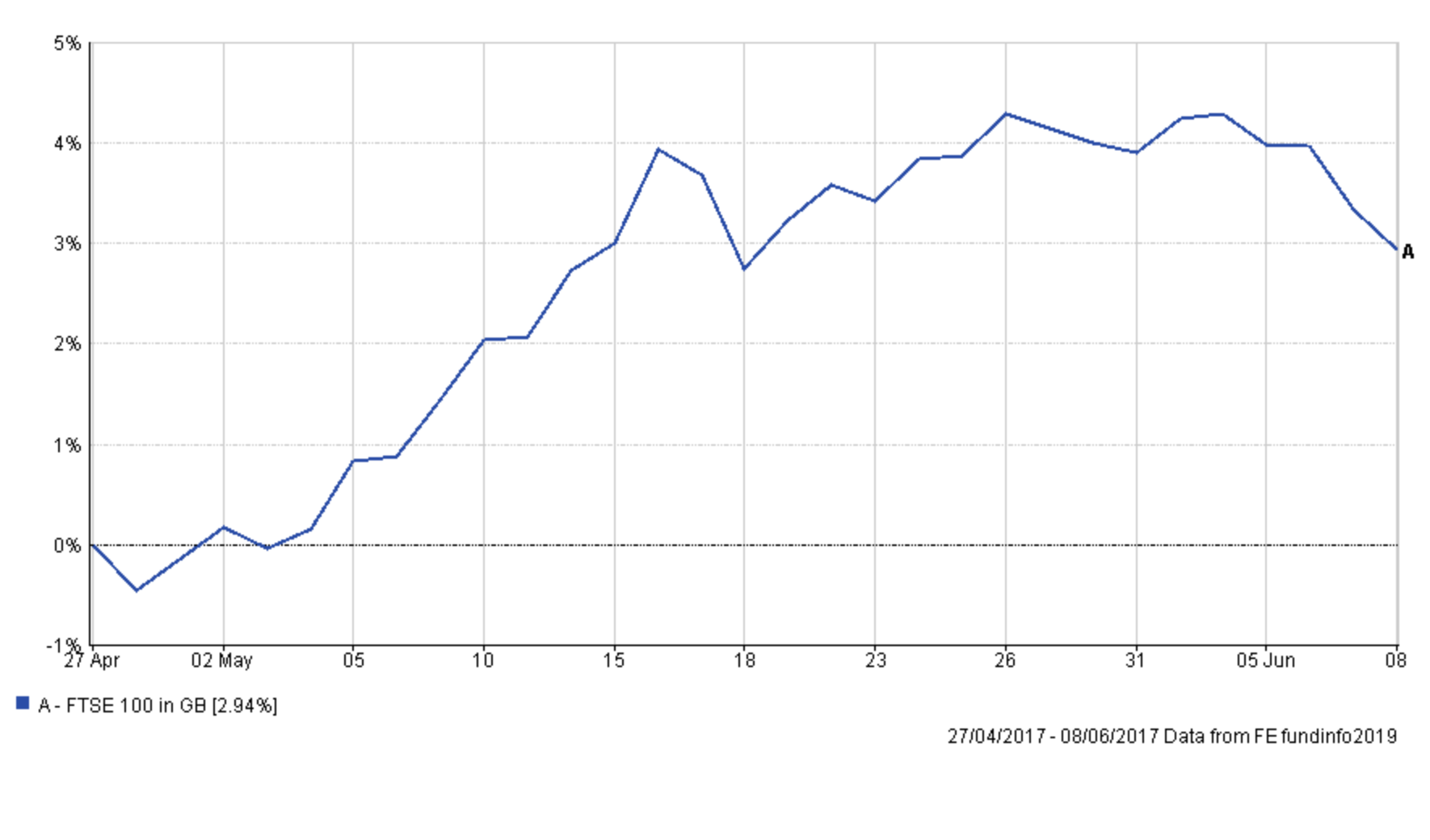

Ahead of the 2017 election, I suggested that the FTSE 100 tends to do well in the lead up to a general election if there is a widely expected outcome. Back then Theresa May called the general election based upon the polls' suggestion that she would win a clear majority. With the benefit of hindsight, the chart below shows how 2017 followed the historic pattern, as predicted, with the FTSE 100 rallying in the 6 weeks ahead of the election based upon an assumption that Theresa May would secure a majority.

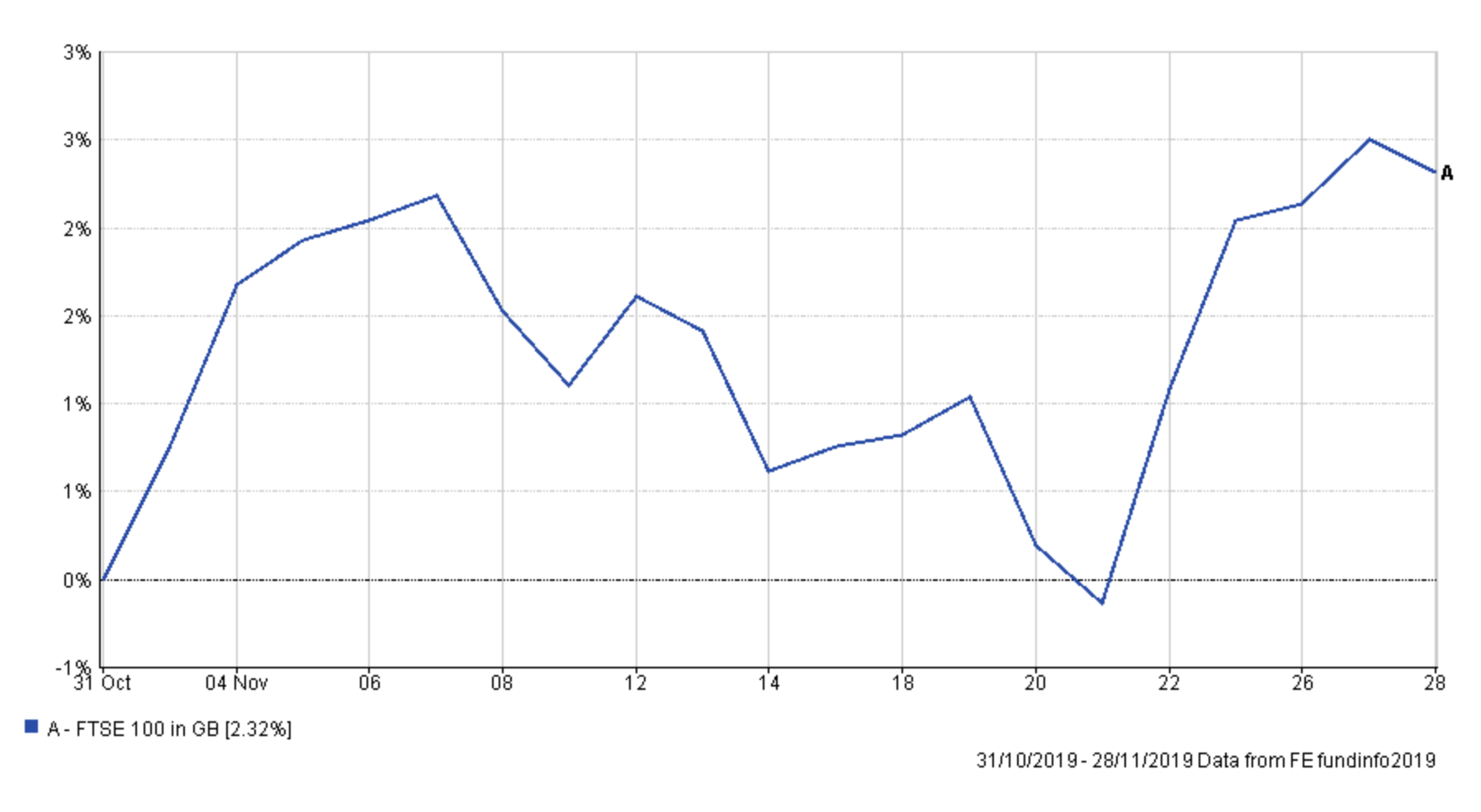

Of course, we now know that she didn't achieve a majority. But the key point is that in the lead up to an election the market likes certainty (and doesn't like predictions of a hung parliament as we had in 2010). Fast forward to 2019 and with only two weeks to go until the election the chart below shows how the FTSE 100 has fared over the last four weeks.

The FTSE 100 is currently up but the index has behaved rather erratically. Uncertainty over the outcome (some polls are suggesting that Boris might not secure a majority) has had some impact but ironically the biggest influence has been the value of the pound. Unlike 2017, the Conservatives now have a Brexit deal which could potentially be implemented if they secure a parliamentary majority. Therefore whenever poll predictions favour the Conservatives it causes the pound to rally, which has hampered the FTSE 100. Having said that, the market reaction since the 21st November has been so strong that even the normal inverse relationship between the value of the pound and the value of the FTSE 100 has snapped. The FTSE 100 rallied at the same time as the pound because the market is anticipating Boris to win comfortably. We saw something similar ahead of the 2017 election.

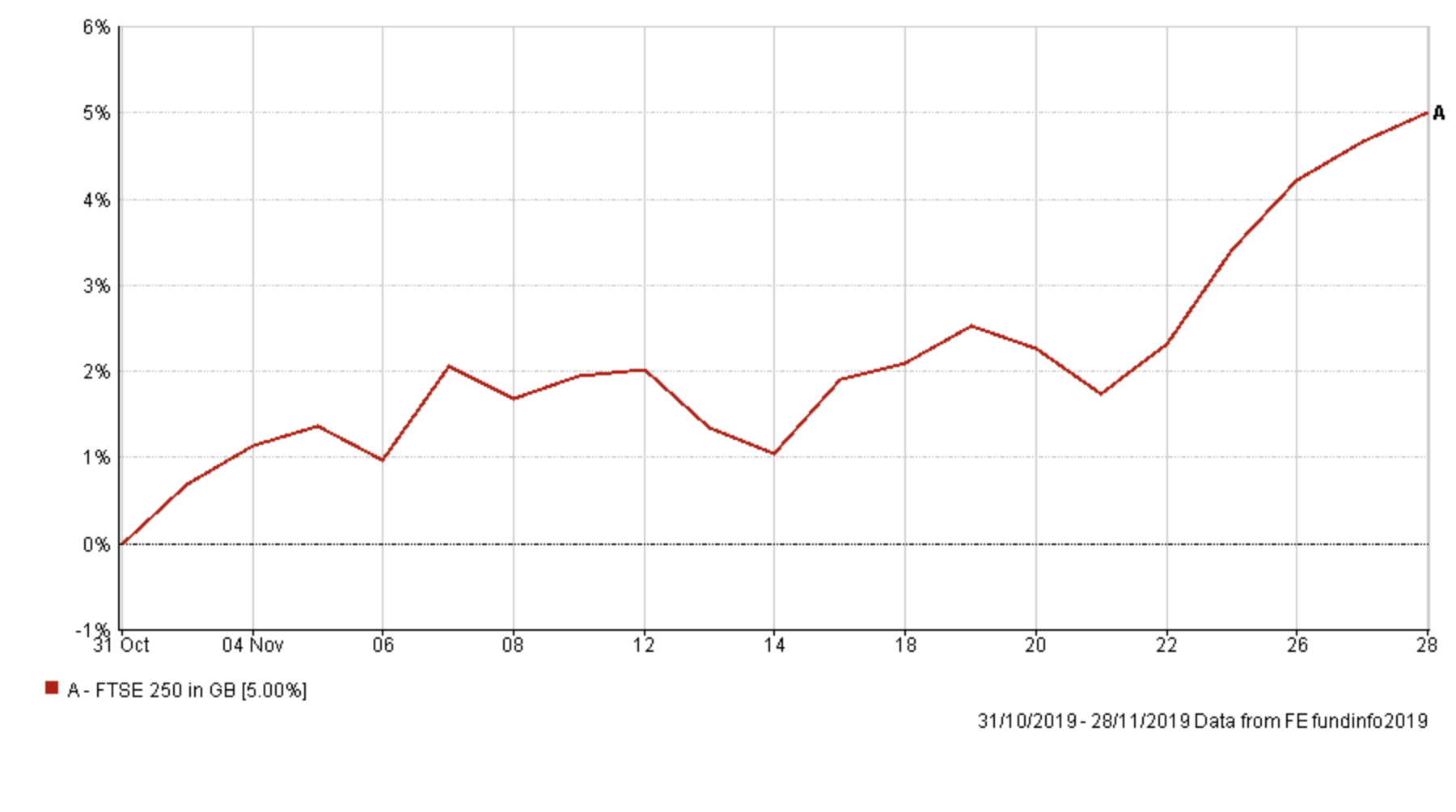

Interestingly if we look at the performance of the more domestically orientated FTSE 250 over the last month (which is less impacted by currency moves) it tells a much clearer story of conviction over the outcome of the 2019 election. The upshot is that the UK stock market has so far stuck to the historical script pre-election.

Post-election equity slump?

What happens post-election often has little to do with what goes on before it, or indeed during it. Last time I produced a table showing that historically landslide election victories don’t necessarily translate into further equity profits.

| Year | Landslide winner | Notes |

| 2015 | Conservatives | While not expected, it was an outright victory for the Conservatives. Markets immediately jumped 2% after the surprise result before fading. Ended the year over 9% down from the election date, mainly due to China induced sell-off in the summer |

| 1997 | Labour | Preceded by stock market gains and a further 15% gain in the second half of the year, after a 10%+ correction |

| 1987 | Conservatives | Preceded by stock market gains but soon followed by Black Monday and 30% sell-off |

| 2001 | Labour | Dotcom bubble implosion was underway & preceded 9/11 attacks - stock market was already in decline and continued |

Even if investors get the outcome they want, having rallied in the lead-up to election day in anticipation, once the result is confirmed global macro events can quickly overwhelm and dictate the direction of stock markets.

In the three months after the 2017 election the FTSE 100 fell 0.97%, underperforming global stocks by 1.8%. Global stocks were unfazed by what was going on in Little Britain, continuing their indifference to the outcome of most global elections. This underperformance of UK stocks isn't unusual. In fact, the average amount UK stocks underperform global stocks in the three months after each election between 1970 and 2017 is -3.28%.

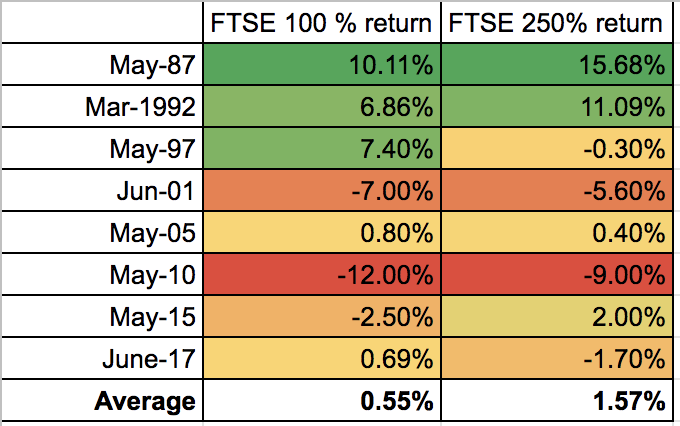

With a UK stock market rally likely in the lead up to an election, depending on the consensus predicted outcome, matched with a likely post-election slump it explains why the average return of the FTSE 100 since 1987, across an election, is just 0.55%. The table below shows the performance of the UK stock market during the two months across each UK election.

Performance of UK stocks from 1 month before an election to 1 month afterwards

While the averages suggest that UK stocks tend to take a pause across an election this does mask some big variations. With the exception of 2001 when the bursting of the dotcom bubble was underway, the data indicates that what the market hates most is a hung parliament, as we had in 2010 and 2017. Equity markets clearly prefer certainty and political stability.

How will the election affect the pound?

The value of the pound has had a huge impact on UK investors' portfolio returns since the referendum back in 2016. When the pound weakens, particularly against the dollar, it usually provides a boost to the FTSE 100 as well as overseas holdings. So how does a UK election impact the value of the pound?

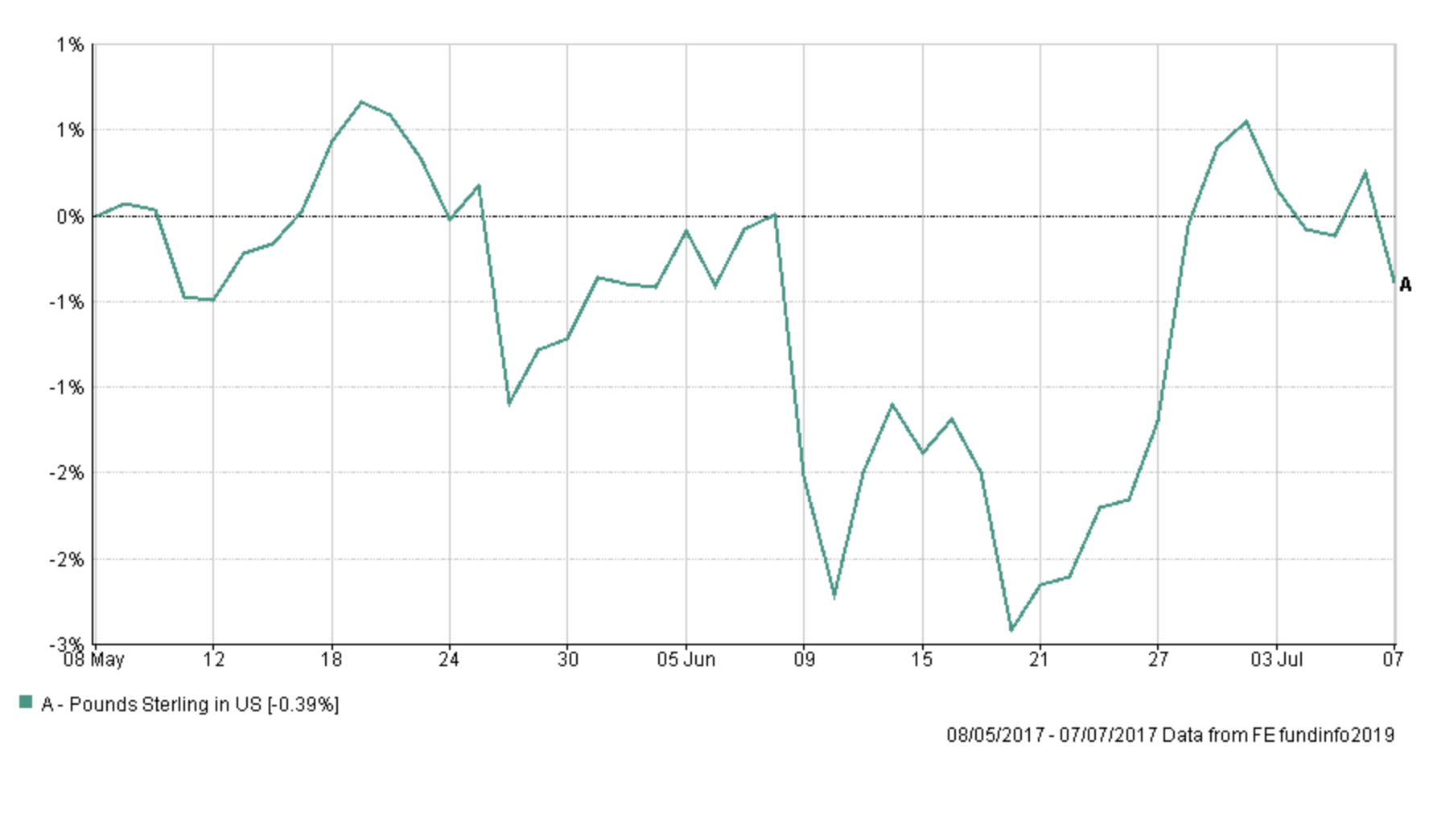

An unexpectedly strong election result (as in 2015) tends to be positive for the pound. Conversely, a result that isn't in line with consensus predictions, just like in 2017, is usually negative for the pound. The chart below shows how the pound fell 2.22% after the 2017 election result was announced on the 8/9th June as Brexit uncertainty was priced back into currency markets. However, the decline was short-lived with the pound recouping the losses against the dollar within 30 days of the election result. Interestingly after past landslide election wins (in 2001 and 1997) where the pound strengthened the rally again faded within a month.

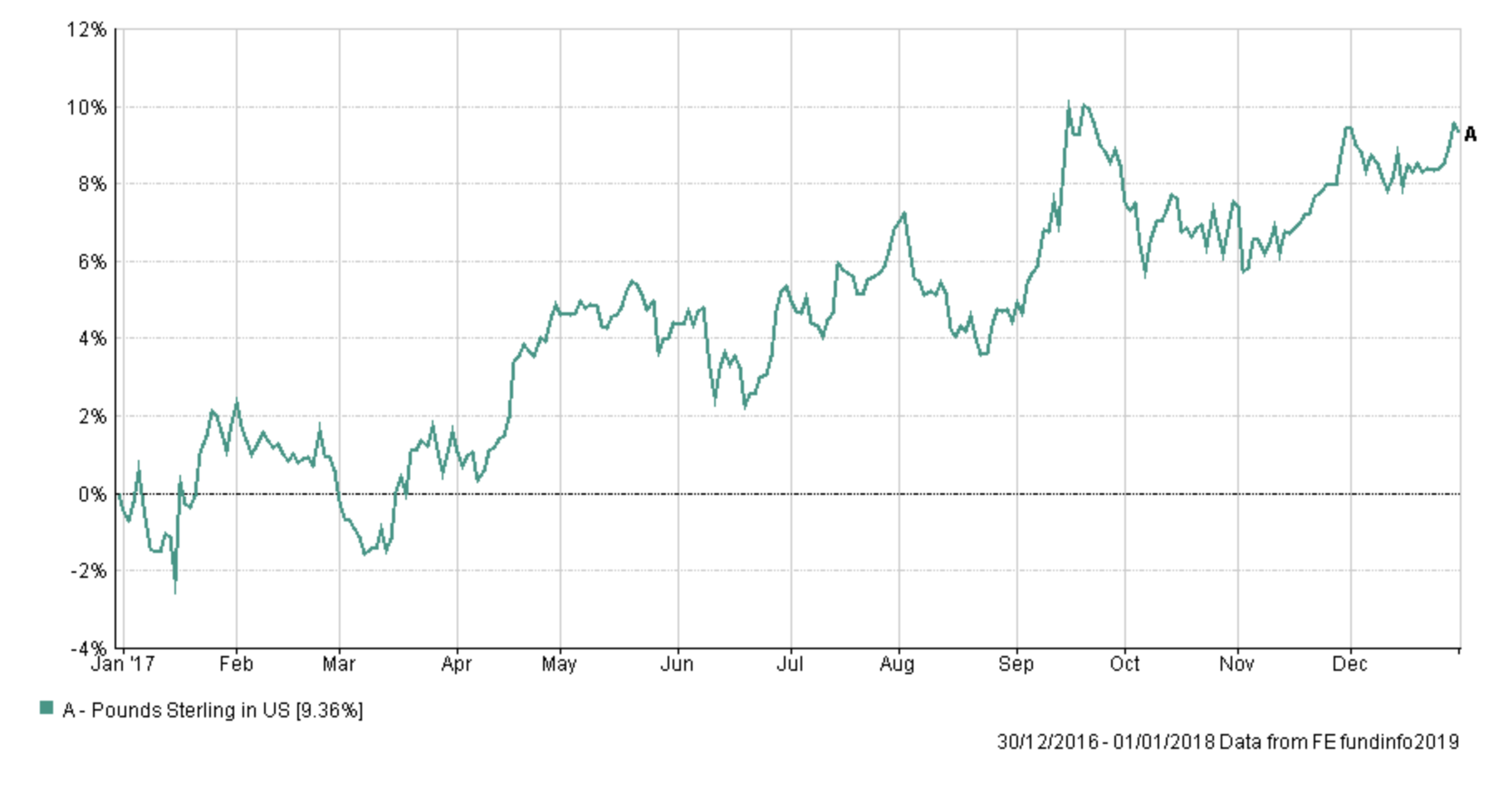

The post-2017 election slump in the value of the pound actually occurred within in a much wider rally for sterling in 2017, as shown below, which continued until April 2018. Much like the impact on the stock market, historically the UK general election's impact on the value of the pound is often fleeting. Typically across an election, you can expect the pound to fall more than 1% based on history.

Of course with a potential Brexit deal already on the table if the Conservatives win analysts are predicting a marked impact on the value of sterling. A Conservative majority is widely being predicted to drive the pound up from $1.29, where it is now, to $1.35-$1.40 as the Conservatives move to push through Brexit by early 2020. Conversely, a Labour win and the eventual implementation of their manifesto promises (and another referendum) could see the pound weaken down through $1.25. A hung parliament is a complete unknown as an eventual coalition which included the Brexit Party and the DUP (just one possibility admittedly) could see the odds of a no-deal Brexit rise. In this instance, some analysts are predicting the pound would fall below $1.25 and possibly towards $1.20. However, all this is pure speculation.

Summary

The upshot is that we can expect an increase in volatility in equity and currency markets whatever happens on the 12th December and as a long term investor history suggests that knee-jerk reactions should be avoided. Market reactions can be strong but they are often fleeting, before being overwhelmed by other macro events.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay