At the start of a new year, I like to write an investment outlook for the year ahead as well as glance back at the year that has passed.

Summary of 2021 - a year of rotations

It was hoped that 2021 might be a year of recovery, but at the time of writing last year’s investment outlook, the UK was once again in a national lockdown as covid continued to spread. However as the vaccination programme gathered pace, particularly in the UK, there was a sense of optimism for 2022. Indeed, the average prediction by investment banks of where the S&P 500 would finish 2021 was 4142, which equated to a predicted annual return of 11.97%. That was almost twice the return predicted for 2020, which showed just how optimistic investment banks were, despite the fact that the economic fallout from the pandemic was far from over.

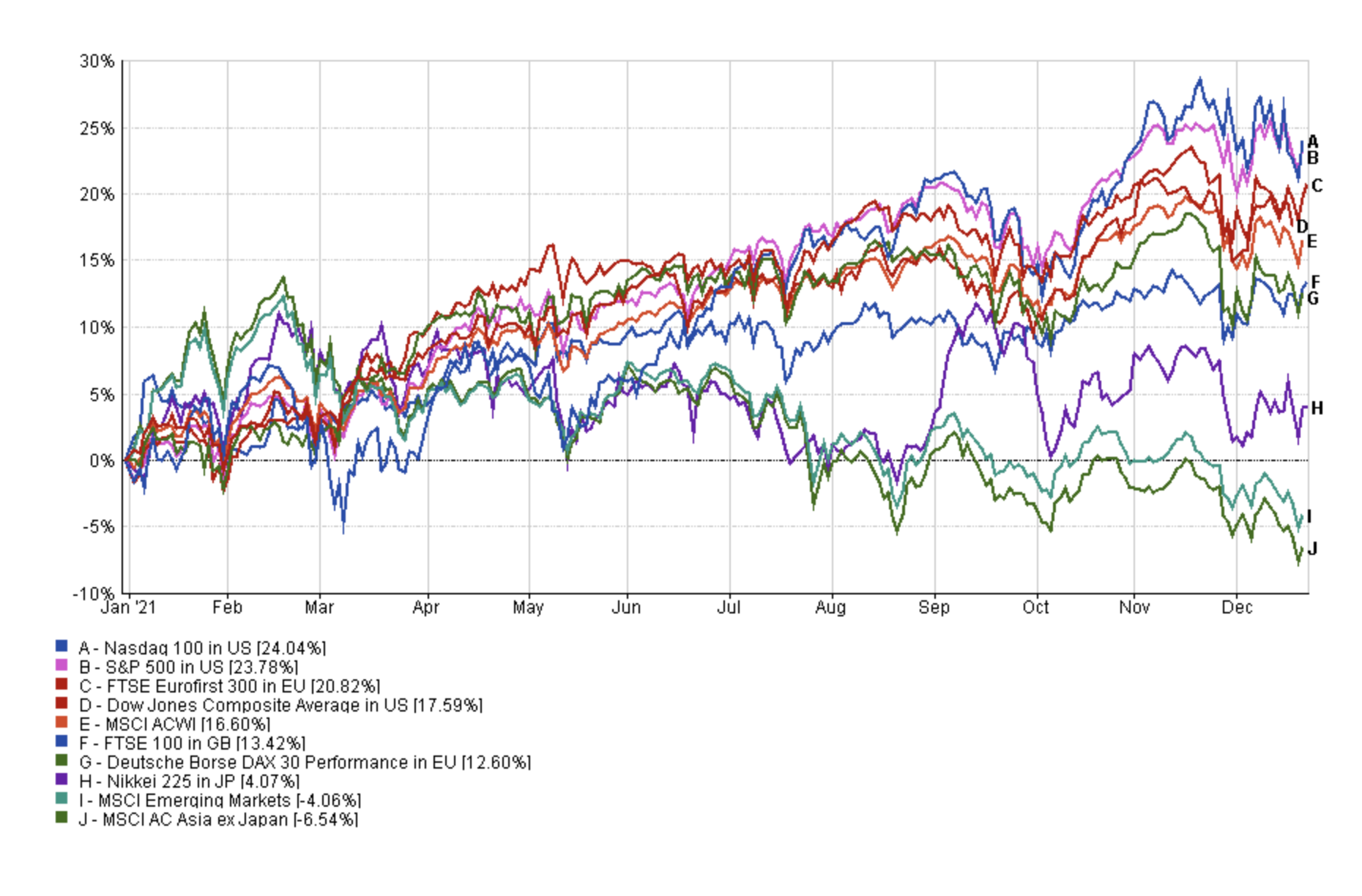

It turns out that they weren't optimistic enough with the S&P 500 having secured 68 new all-time highs so far in 2021 (at the time of writing on 23rd December) and sitting at 4681. The S&P 500 has so far returned a staggering 23.78% in 2021. But once again it was a year where investing in US equities was one of the most profitable trades, with the benefit of hindsight. But as the chart below shows, there was a divergence in fortunes for global equity markets.

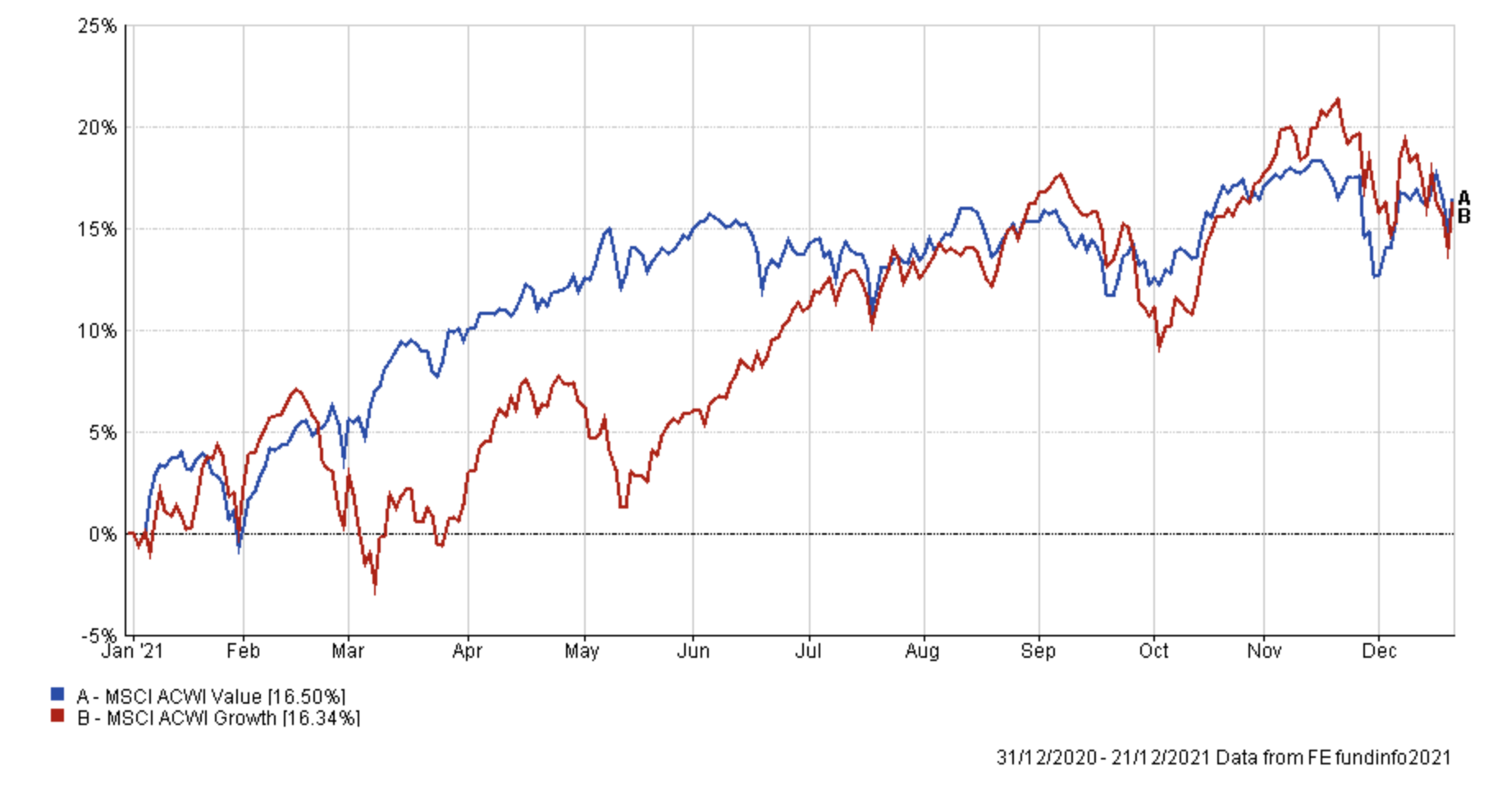

The biggest winners were ultimately large US tech stocks, but in the first quarter of 2021 they were the biggest laggards as value plays outperformed growth stocks as shown in the chart below, thanks to the reflation trade. During this period investors piled into cyclical sectors such as financials as well as indices with greater exposure to these areas, such as the Dow Jones and the German DAX while shunning tech stocks.

By April concerns started to grow over the health of the economic rebound as well as stubbornly high inflation. The stagflation trade rose to prominence which meant that tech stocks (and other growth stocks) received a boost alongside sectors such as REITs (real estate investment trusts) and utilities. You can see that in the chart above. But by mid-May the market view changed again and we saw a rotation out of growth back into value stocks. These constant rotations were the hallmarks of 2021 as investors remained troubled by covid, persistent inflation, mixed economic growth signals and potential central bank monetary tightening. Broadly speaking, those assets out of the blocks in 2021 (which included emerging market equities and Asian equities) were the biggest laggards in 2021, with the MSCI Emerging Market Index and the MSCI Asia ex-Japan Index actually falling into negative territory for the year. Big tech continued to outperform, but to a lesser degree as UK equities and European markets finally began rewarding investors for their patience.

Outlook for 2022

As I explained last year, while I usually pay little attention to investment bank predictions of where the markets will end up at the end of the following year, some people are interested in what these institutions believe will happen. Below is a round-up of the end of 2022 S&P 500 predictions from some of the main investment banks and research organisations. At the time of writing, the index sits at 4,681.

| Institution | S&P Forecast |

| Morgan Stanley | 4,400 |

| Wells Fargo | 5,100-5,300 |

| Goldman Sachs | 5,100 |

| RBC | 5,050 |

| BofA Global Research | 4,600 |

| Credit Suisse | 5,200 |

Low average: 4908.3

High average: 4941.6

Taking into account Wells Fargo’s two separate forecasts, the low average prediction for the S&P 500 at the end of 2022 is 4,908 while the high average is 4,943. Compared to where the S&P 500 sits at the time of writing, that suggests an almost 7% rally in 2022, which is just below the long term annual average return of 8% for the S&P 500.

Morgan Stanley, one of the least optimistic banks predicts that in 2022, “while earnings for the overall index remain durable, there will be greater dispersion of winners and losers and growth rates will slow materially”. With the exception of Morgan Stanley, the forecasts for the S&P 500 at the end of 2022 are positive, but many of the predictions come with notes of caution. Goldman Sachs says that "decelerating economic growth, a tightening Fed, and rising real yields suggest investors should expect modestly below-average returns next year”. However, it did add that "in contrast with our expectation during the past year, corporate tax rates will likely remain unchanged in 2022 and rise in 2023. Corporate earnings will grow and lift share prices. The equity bull market will continue”.

Below I look at some of the investment themes that are likely to influence investment markets in 2022.

Covid-19

The 11th March 2022 will mark 2 years since the World Health Organisation (WHO) declared a global pandemic. Unfortunately, the pandemic is not over and the arrival of Omicron has muddied the waters. Scientists are still trying to discern the threat posed by Omicron, and depending on what they discover the range of outcomes is varied. If the threat to the NHS, for example, is significant then we could face a national lockdown in the UK, similar to what we've already seen in parts of Europe. If that is the case then we may already have the playbook for 2022, if we look back to 2020. In the unlikely event that global economies are shut down once again then governments and central banks are likely to provide new fiscal and monetary stimulus. If you recall, it was the original pandemic stimulus measures (quantitative easing and low interest rates) that drove the bull market in equities over the last 2 years.

If the risks posed by Omicron are less severe than feared and we begin to tackle the pandemic on a global scale through mass vaccination programmes then investment markets might move beyond covid-19 in 2022.

Inflation/central banks

One of the big themes of 2021 was inflation, yet ironically it was not on most investors' radars at the start of the year. As we closed out 2021 UK inflation had hit 5.1% in November - the highest level since September 2011 - while inflation in the US reached 6.8%, the highest level since the 1980s.

As inflation began to rise in 2021 central banks (and especially the US Federal Reserve) described it as transitory, a result of the temporary imbalance in the supply and demand of goods and services as the global economy recovered from the pandemic. High inflation usually demands a strong response from central banks, but major central banks sat on their hands in 2021. But ultimately the US Federal Reserve (the Fed) and the Bank of England (BOE) had to admit that inflation was proving stubborn and so dropped the transitory line. In December, both the Fed and the BOE took a more hawkish turn with the former accelerating the tapering of its quantitative easing programme while the latter raised its base rate from 0.1% to 0.25%. They join other central banks such as those in Mexico, Hungary, New Zealand, Chile and South Korea which have already made adjustments to their monetary policy.

But there is the possibility of seeing a divergence in 2022 between the monetary policy of key central banks, namely the Fed, the BOE and the European Central Bank (ECB). The ECB has signalled that it is unlikely to raise interest rates at all in 2022. But how long can it continue to ignore rising inflation?

Current forecasts for 2022 are for inflation to continue to prove stubborn in the short term. The BOE's latest forecast is for inflation to peak at 6% in April, which is a level not seen since the early 1990s. In the US, the Wells Fargo Investment Institute stated in its 2022 Investment Outlook that it expects “inflation to moderate from current levels in 2022 but to remain above recent historical norms”. If inflation proves stubborn central banks in the UK and the US have already shown that they will not be afraid to act. A tightening of monetary policy will be a fine balancing act to ensure that they don't snuff out the economic recovery. A rising interest rate environment makes bonds, defensive equity sectors and growth stocks less attractive.

In its 2022 Economic and Market Outlook, Vanguard stated that it believes "that central banks will largely try to avoid sharp and unexpected shifts in the timing of policy changes, particularly of policy rate increases, but that conditions will force them to act in 2022 and quite possibly by more than markets are anticipating”. Or in other words, investors could get caught out by central bank action in 2022.

Stagflation/Reflation/Recession/Yield curve

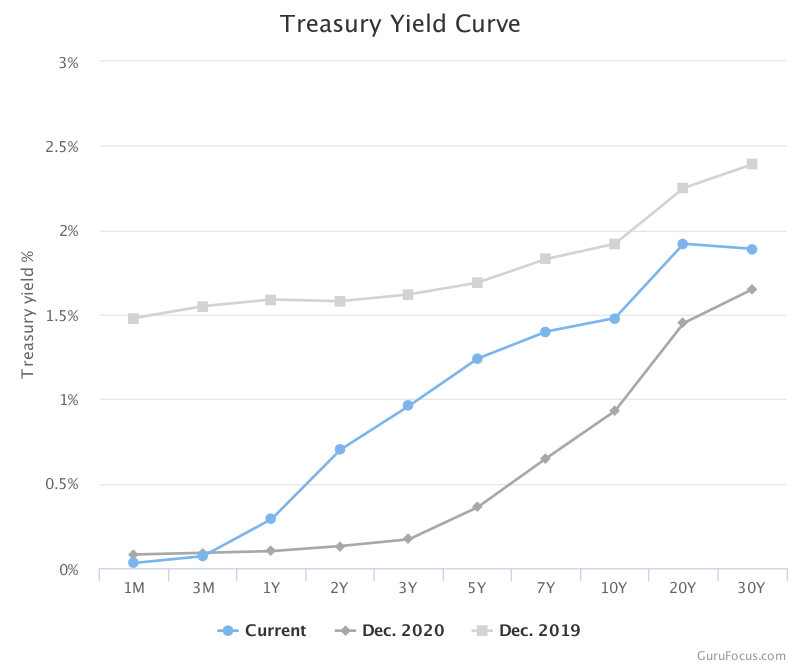

Investment markets spent much of 2021 rotating back and forth between trades that would benefit from a reflationary environment to those that would benefit from a stagflationary one and vice versa. As such a lot of focus in 2022 will likely be placed on the outlook for economic growth both domestically and globally. I wouldn't be surprised if we hear a lot more about the yield curve in the coming months. Let's take the yield curve in US Treasuries for example. As I've explained previously, a Treasury is a low-risk investment and is effectively a loan to the US Government. You are paid an agreed coupon (interest) on that loan until the agreed term comes to an end and you get your capital back. So a simple way of looking at the yield on a 10 year US Treasury is that it represents the interest rate you want in order to lend money to the US Government for 10 years. All being equal, the longer you lend your money to the US Government the higher the interest rate you would want, as there is an increased risk of default. If you plot the yields for each different term of US Treasury on a chart this is known as the yield curve, and you normally get a line that slopes upwards as the term increases.

As the yield is a function of the price you pay for a US Treasury it means that supply and demand can influence the yield for a given duration. Because Treasuries and bonds give a fixed income stream they are popular when interest rates within the economy are low. This tends to be when the economy is struggling. It follows then that if the market starts to believe that the economy will begin to struggle that demand for long term bonds increases (so the longer-term yields fall). This is described as the yield curve flattening and ultimately can mean the yield curve inverts. When the yield curve starts to invert (it can completely invert where longer-term yields are lower than short-term yields) it has tended to reliably predict an impending recession.

The chart below shows that the yield curve in the US has steepened suggesting that reflation is still currently the favoured prediction of bond investors.

But the yield curve in UK gilts has flirted with inverting in recent weeks, highlighting that perhaps in 2022, we will see a divergence in economic fortunes globally as the initial pandemic rebound fades. But it's worth bearing in mind that even if the yield curve here or in the US were to start to become a cause for concern then on average the lead time, from an inversion, until a recession is 22 months. Furthermore, stocks rally on average a further 15% over the next 18 months before a recession hits.

Strong US dollar

At the start of 2021 the consensus forecast was for the US dollar to fall in value and by as much as 20%. The chart below of the US dollar index (which measures the strength of the dollar against a basket of currencies) shows the opposite happened and the dollar strengthened.

Even so, it was not until inflation accelerated in the autumn and the Fed grew more hawkish that the US dollar strength really took hold. The narrative being that potentially higher-interest rates make the US dollar more attractive. But, usually at this stage of the economic cycle with inflation and economic growth accelerating the dollar weakens. In any event, it was the scale of the dollar rally that hit markets in the last quarter of 2021. The burst higher in October marks the high point of the rally in commodity prices too as shown in the chart below. Commodities were a great portfolio diversifier in 2021 and inflation-hedge.

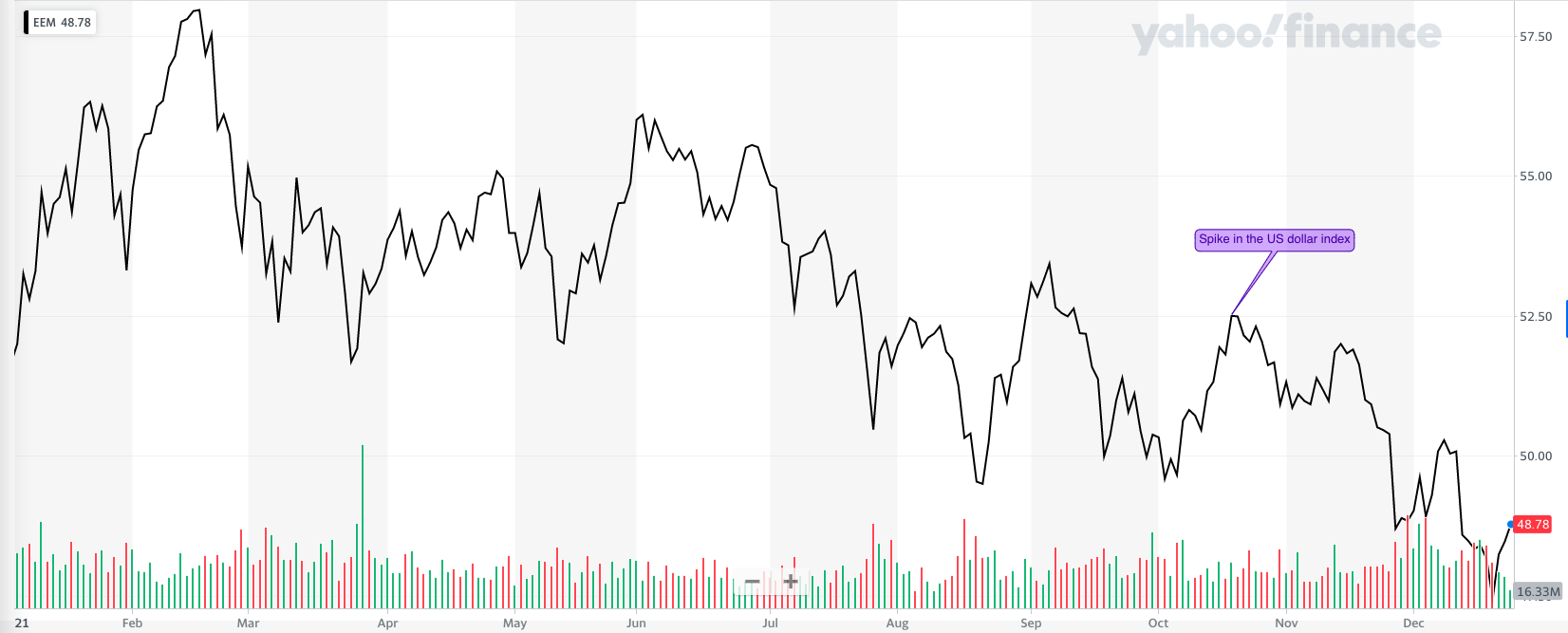

The strength of the dollar dealt a blow to not only commodity markets during the final quarter of 2021 but also emerging market equities. The chart below shows that the performance of an ETF that tracks a broad basket of emerging market equities was flat for the year until the dollar spiked in October, sending the index lower by 7%.

Commodities tend to underperform when the dollar is strong because commodities are priced in US dollars. Meanwhile, many emerging market companies/countries will have assets denominated in their local currencies but may have liabilities, such as debts denominated in US dollars. When the dollar strengthens their debts theoretically start to grow in local currency terms, making them unattractive to investors. The strength of the US dollar is likely to be a theme that plays an important role in 2022, particularly in these areas of the market and also more widely. There comes a point where a strong dollar will even become a headwind for US equities too.

Politics/Geopolitics

Politics took more of a backseat in investors' minds during 2021. The US election had passed and the UK officially left the European Union. But 2022 is already promising that politics and geopolitics will garner more attention. At the end of 2021, the US announced it would not be sending its diplomats to Beijing during the upcoming Winter Olympics in order to protest against China’s alleged human rights abuses. There are other grievances too, including the political freedoms of citizens in Hong Kong and the “fight for democracy” between democratic Taiwan and China. Not to mention the violence on the border between China and India, as guards continue to fight over territorial lines.

In addition, Russia’s apparent military preparations on the border with Ukraine are straining relations with the US. Putin has expressed dismay at what he sees as an increased NATO presence on Russia’s Western border and has threatened to take military action on previous occasions.

Returning to domestic politics there are rumours that there could be a leadership challenge in the Conservative Party, resulting in a new Prime Minister. In addition, the US mid-term elections occur in November which will inevitably gain investors' attention.

The above are just some of the themes that could play out in 2022. There are plenty of other candidates including the steady rise of climate investing. But if we’ve learned anything from the last 2 years, it’s that you can’t rule out black swan events from tipping the status quo on its head.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay