At the start of a new year, I like to write an investment outlook for the year ahead as well as glance back at the year that has passed.

Summary of 2022 - one of the toughest years on record

After a number of years of writing these investment outlooks it has become apparent that investment managers fall foul of recency bias. Recency bias is defined in behavioural economics as where you incorrectly believe that recent events will occur again soon. This leads to an inaccurate and subjective assessment of the probability of events occurring in the future. In the world of investing this can lead to irrational and poor investment decisions.

This time last year I wrote how investment banks were too pessimistic in their predictions for 2021, following a dismal 2020 which was blighted by the covid pandemic. Fast-forward to 2022 and the opposite is true, with investment banks way too optimistic about how 2022 would pan out, following the strong equity market market returns of 2021.

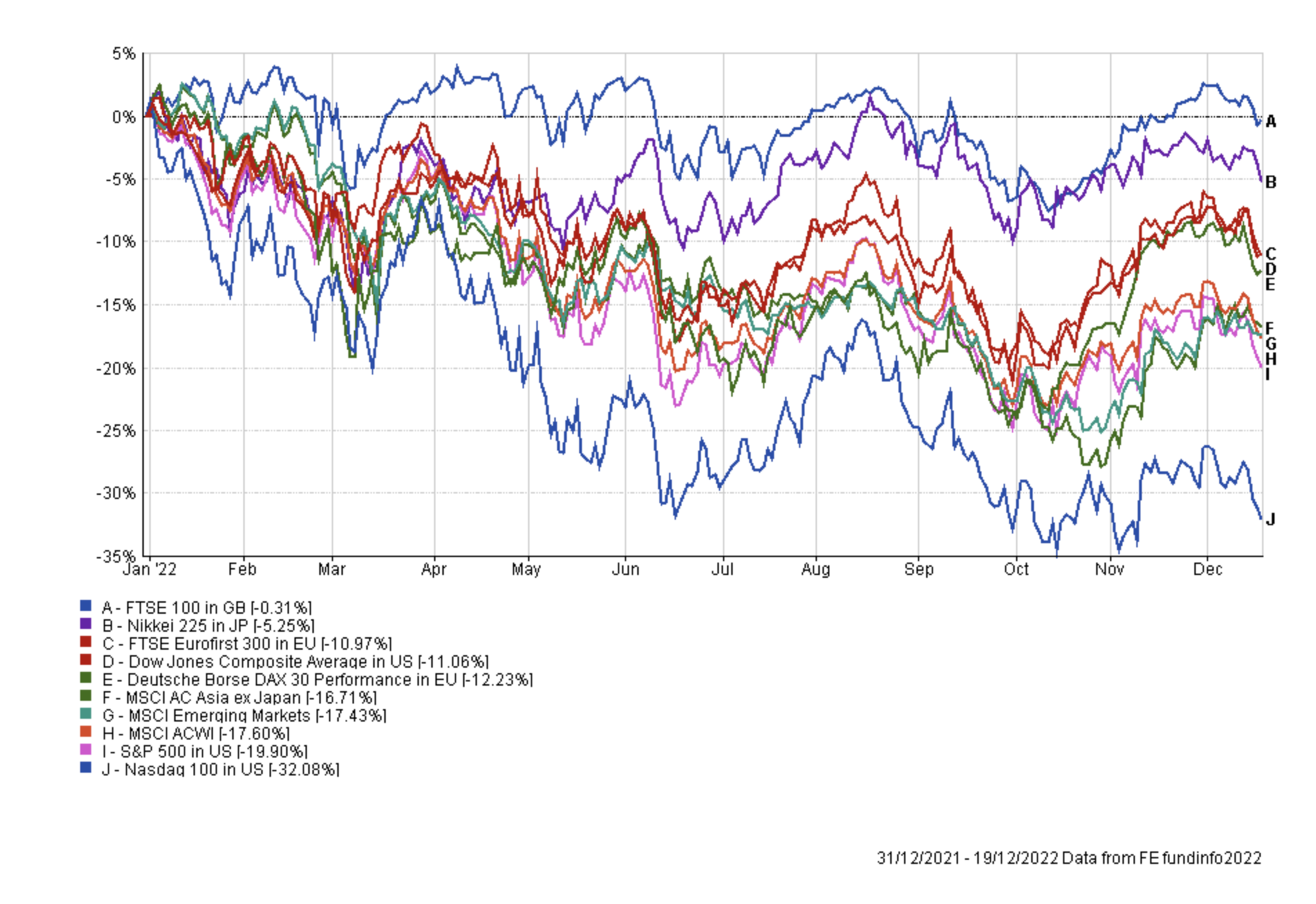

The chart below shows the performance in local currency terms of key stock market indices during 2022.

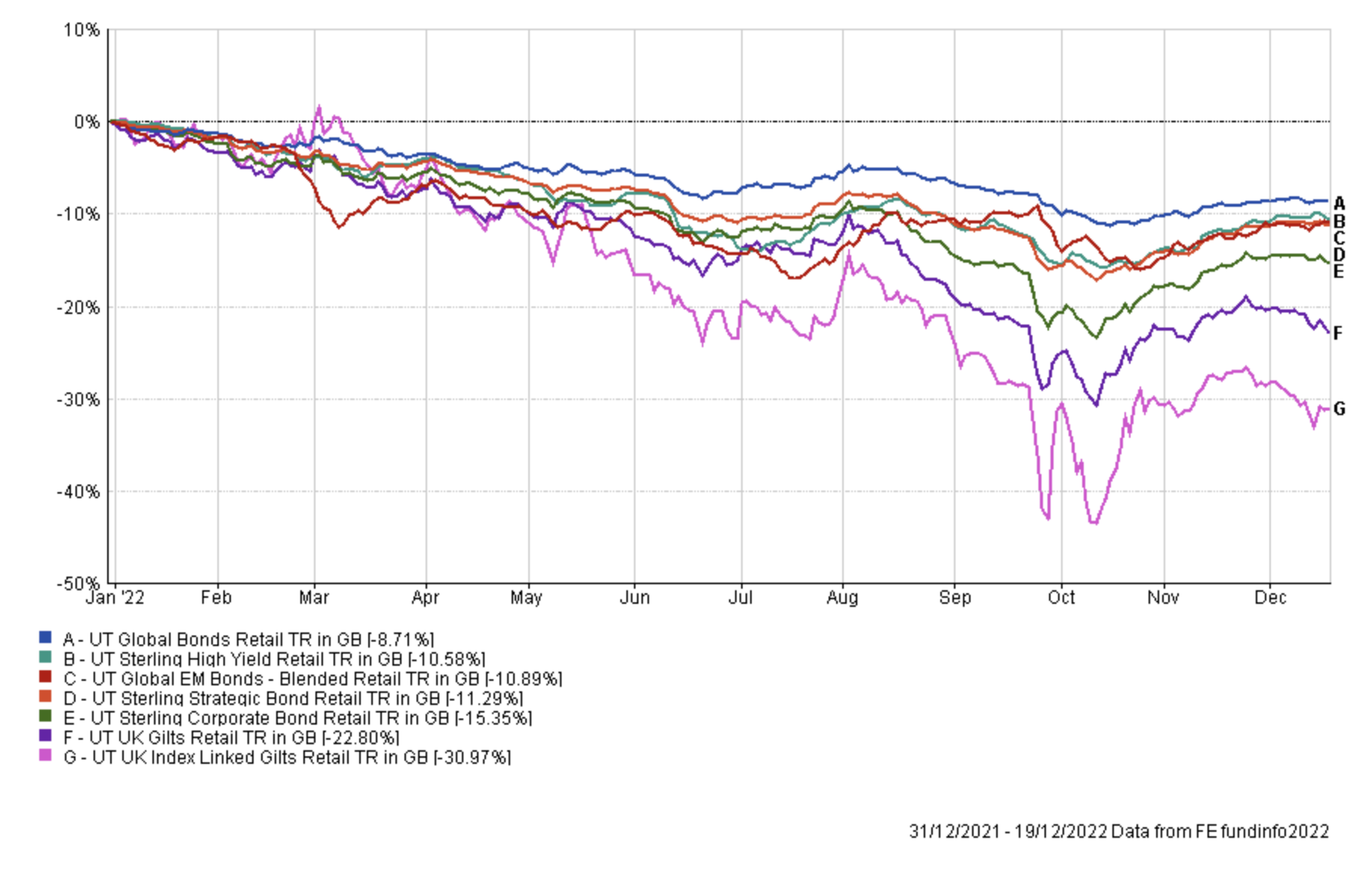

But not only did equity markets struggle, so too did bond markets. The chart below shows the average return from a range of bond fund sectors.

It meant that the traditional 60/40 portfolio had one of its worst years on record (down between 11% to 13%), proving cash, commodities and absolute return strategies to be more viable portfolio diversifiers. If you were able to minimise your portfolio falls you did well in probably the most difficult year to invest in recent memory. As I write (on 19th December) my own £50k portfolio is down just 6.5% in 2022.

Of course events like Russia’s invasion of Ukraine, probably the single biggest influence on investment markets in 2022, will always catch investors off-guard. However, investment banks clearly have a tendency to project recent history into the future. If you take the average investment bank prediction of where the S&P 500 would end 2022, they expected a rally of between 7% and 8%. As the chart above shows they were well wide of the mark with the S&P 500 down -19.9% at the time of writing.

Outlook for 2023

As I explain each year, while I usually pay little attention to investment bank predictions of where the markets will end up at the end of the following year, some people are interested in what these institutions believe will happen. Below is a round-up of the S&P 500 predictions for the end of 2023 from some of the main investment banks and research organisations. All these predictions were made on 4th December when the S&P 500 sat at 4071. Beside each forecast you can see what the prediction represents in terms of a potential percentage increase (in blue) or decrease (in red).

For reference, at the time of writing, the S&P 500 sits at 3,852.

| Institution | S&P Forecast |

| Barclays | 3675 (-9.72%) |

| Scoiete Generale | 3800 (-6.65%) |

| Morgan Stanley, CITI & UBS | 3900 (-4.20%) |

| Credit Suisse | 4050 (almost unchanged) |

| JPMorgan | 4200 (+3.17%) |

| BMO | 4300 (+5.63%) |

| Deutsche Bank | 4500 (+10.54%) |

| Average prediction | 4060 (almost unchanged) |

Yet again there is a wide discrepancy between the predictions, with almost a 20% difference between the best and worst case predictions. If you take an average of the predictions (4060) it assumes that the market will be broadly flat next year. Usually investment banks are bullish, predicting strong market growth each year. After all, it would likely be bad for business to be too pessimistic. Perhaps the prediction of a flat 2023, is about as bearish as we can expect from investment banks as a group, which goes to show the impact the 2022 bear market has had on professional investors' mindsets.

Barclays, the most bearish of investment managers, believes that despite the market falls in 2022 there is room for them to drop further in 2023. They believe “US stocks tend to bottom out 30-35% below [their] peak in the middle of a recession. That suggests fair value of 3200 on the S&P 500” will be achieved in the first half of 2023 as central bank monetary policy remains restrictive. Or in other words, we won’t see interest rates cut in 2023 and the S&P 500 could fall a further 17% from where it is currently.

If we go back to the end of 2021, Barclays predicted the S&P 500 would be at 4800 by the end of 2023, which was just below the average prediction. They were way off then so their latest view should be read with a healthy dose of pragmatism, as with any of the other predictions listed above.

In fact, the investment bank with the closest prediction last year was Morgan Stanley which predicted the S&P 500 would be at 4440 by the end of the year. If you therefore believe their crystal ball is working better than the other institutions, then 2023 could see the S&P 500 fall by -4.2%, according to the table above.

But at the other end of the scale Deutsche Bank is bullish about the year ahead stating that it is “... cautiously optimistic. [It expects] mild recessions in Europe and the US, but improving dynamics in Asia where supply chains are all but resolved. As rates stabilize and inflation abates, there should be opportunity for equities and fixed income...”

There are a range of potential investment themes or trends that investors will have to navigate in 2023 and I look at some of these below:

Ukraine war

Last year I wrote about potential geopolitical headwinds for 2022. At the time I wrote…

“Politics took more of a backseat in investors' minds during 2021… Russia’s apparent military preparations on the border with Ukraine are straining relations with the US. Putin has expressed dismay at what he sees as an increased NATO presence on Russia’s Western border and has threatened to take military action on previous occasions… if we’ve learned anything from the last 2 years, it’s that you can’t rule out black swan events from tipping the status quo on its head.”

Little did any of us truly appreciate what would unfold months later. The war in Ukraine was perhaps the defining event of 2022 which sparked risk aversion in bond and equity markets. It helped fuel the rapid rise in inflation which in turn led central banks to raise interest rates. The Ukraine war is ongoing and it’s uncertain if there will be a resolution in 2023. A steep escalation, especially if this includes nuclear weapons or NATO becoming directly involved in the conflict, would obviously be detrimental to investment markets.

But the Ukraine war has also had lasting geopolitical impacts beyond its own borders. Countries and trading blocs have responded by seeking self-sufficiency, not just in terms of energy but also in terms of economic growth. It means that 2023 could see more fragmentation globally as protectionism takes hold, which leads to increased competition. This in turn could cause supply chain issues which may put upward pressure on prices. Even if the Ukraine war is brought to an end its impact economically will be lasting and likely a theme throughout 2023.

Geopolitics

Heading into 2022, geopolitical tensions were on the radar but not the focal point of investors’ attention. A year on and the situation is different. The increasing fragmentation and drive for self-sufficiency mentioned above is increasing political tensions. As such it is likely to garner more attention in 2023. In particular, US and Chinese relations could come under further strain. China’s growing military presence in the Asia-Pacific region and Nancy Pelosi’s visit to Taiwan has brought relations to new lows. Outside of the possible flashpoint of Taiwan’s independence there is also the increased competition between the superpowers. Joe Biden’s administration recently announced export controls over exports to China of semiconductor chips to try and slow China’s technological and military developments. Retaliations are possible and if they occur we may be talking about a US-China trade war once again.

US dollar strength

At the end of 2021 the US dollar had bucked analysts' predictions that the currency would weaken by up to 20% during 2021. The higher than expected US dollar, sparked by rising inflation and a more hawkish US Federal Reserve, started to prove a headwind for commodities and emerging market assets.

2022 was no different. In my 2022 outlook I wrote that “the strength of the US dollar is likely to be a theme that plays an important role in 2022, particularly in these areas of the market and also more widely. There comes a point where a strong dollar will even become a headwind for US equities too”.

The US dollar index (which is a measure of the strength of the dollar against a basket of currencies) hit a multi-decade high in 2022 and did indeed become a headwind for US equities. When the dollar weakened the US stock market rallied. Conversely, whenever the dollar strengthened, the US stock market fell. A strong dollar not only tends to hit US stocks but also commodities (especially gold) as well as proving a headwind for Asian and emerging markets. In contrast, a strong dollar versus the Japanese yen tends to be positive for the Nikkei 225, while a weaker pound versus the stronger US dollar can provide some support for the FTSE 100.

The US dollar index goes a long way to explaining many of the market moves we saw in 2022, especially since mid-June. A change in the value of the US dollar index will not always immediately result in a textbook move in another asset's price, say for example gold or Japanese equities. But with markets hanging on every move central banks make much of this is being reflected in the movement of the US dollar index. Regular readers of my weekly 80-20 Investor newsletter will already be aware of the importance I’ve placed on the US dollar, read my newsletter titled “One chart that rules them all”. You can keep an eye on the US dollar index here.

If you get the direction of the dollar right you often get everything else right, be that currency, bond or equity markets.

At the time of writing (19th December) the US dollar index peaked in late September/early October and has been weakened aggressively since. Perhaps it is no surprise that US equities had rallied during October and November. However, after breaking below the 200 day moving average and the 105 level (both bearish) the US dollar index is attempting to break out of a downward sloping triangle, to the upside (shown below). If it manages it then this could set the tone for 2023, with the US dollar index proving a headwind for key assets, including US equities. If instead it breaks below 104 then it could prove a tailwind, and bring about a change in fortunes for most asset classes from what they experienced in 2022

Recession

Consensus opinion among economists and even central banks is that 2023 will likely see many domestic economies enter recession but not necessarily all at the same time. Indeed the Bank of England (the BOE) is already using the working assumption that the UK has entered a recession and will likely remain in one until late 2024. The eurozone is also likely in recession, this is in contrast to the US where economic data has shown a level of resilience. If the US does enter a recession, this may be delayed. Should there be a difference in economic growth prospects globally then we may see some divergence between market performance in 2023.

If the recession is worse than feared then markets will likely respond in kind, with bonds and defensive equity sectors performing better on a relative basis (read my article - How to invest for a recession). It means that investment markets will likely continue to react (or should I say overreact) to the publication of key economic data.

But 2023 may also be the year where the search for yield takes greater precedence. Aside from investing in bonds and defensive sectors one strategy for investing in a recession is to invest in companies that pay reliable dividends. That means equity income sectors. Or in other words funds that aim to produce reliable income payouts over time (see our income heatmaps - which will be updated again in January/February).

Inflation & Central bank monetary policy

This leads on to perhaps the biggest theme of 2022 which will inevitably continue into 2023, that is central bank monetary policy and inflation. 2022 will be remembered for inflation spiralling and in the case of the UK hitting double-digits. Central banks were faced with a dilemma of trying to quell inflation, by raising interest rates, while at the same time not driving their domestic economies into recession. However, it seems that the prospect of a recession is increasingly being accepted by the US Federal Reserve (the Fed), the European Central Bank (ECB) and the Bank of England (BOE) as a byproduct of maintaining credibility on bringing inflation back to target.

The Autumn of 2022 saw investment markets begin to price in a dovish pivot from central banks, particularly the Fed, which caused equity markets to rally and bond yields fall. But the final policy meetings of key central banks in 2022, caught investors by surprise with their hawkish outlooks, particularly the ECB and the Fed. But not to be outdone, the Bank of Japan, the most dovish central bank historically, even shocked markets with an unexpected tweak to its bond market controls. Analysts believed this could pave the way for monetary policy tightening in early 2023, something previously dismissed by an economy that has been struggling with deflation for two decades. The decision by the BOJ just before Christmas caused bond and equity markets to weaken.

Many investors will spend 2023 trying to front-run major central banks policy decisions, particularly the timing of their transition to monetary policy easing, such as interest rate cuts, which would provide fuel for an equity market to rally. But key to that will be the outlook for inflation. With inflation predicted to have now peaked in the UK will it give the BOE room to slow down the pace of interest rate hikes? It will be a similar situation for other economies too. How stubborn inflation proves to be will be crucial in 2023. With most central banks predicting a sharp decline in inflation towards the end of 2023, should this not materialise, central banks may be forced to keep interest rates higher for longer. It also means that should the outlook for inflation differ between countries and economic blocs we could see a divergence in monetary policies which will result in a divergence in the fortunes of equity and bond markets geographically.

Other themes

There are a number of other themes that will be key in 2023, which I will touch upon briefly.

Bond yields & 60/40 portfolio

Bond yields soared in 2022 which meant that bond prices collapsed (as shown in the earlier chart of bond fund performance). The fear of aggressive central bank policy trumped the fear of a future recession, which pushed bond yields higher. It meant that the typical 60/40 equity/bond portfolio is down between 11% and 13% so far in 2022. By way of comparison my £50k portfolio at the time of writing (19th December) is down just 6.5% which means it has outperformed 86% of the 441 professional funds managers running funds within the Mixed Investment 40-85% Shares & Mixed Investment 20-60% Shares sectors.

But if bond yields continue to fall as recession fears gather pace, or central banks turn dovish, this would fuel a surge in the performance of the 60/40 portfolio. 2022 has been one of the worst years on record for the 60/40 portfolio with some analysts consigning the concept to the bin. However, can 2023 really be as bad as 2022 for the 60/40 portfolio?

New leaders or old ones?

2020 saw new equity sectors take the lead from the old guard. Technology stocks imploded as interest rate expectations rose, meanwhile energy stocks soared as commodity prices rose and the war in Ukraine sparked an energy crisis. Those who rotated into the new leaders stemmed their losses for the year. But will 2023 see the energy crisis subside and interest rate expectations fall. Certainly ahead of a recession we might expect defensive sectors to outperform but markets are forward looking so at some point we’d expect cyclical sectors (those most sensitive to the health of the economy) and small cap stocks to outperform.

Oil and gas stocks have helped buoy the FTSE 100 in 2022. For example the FTSE 100’s largest constituents include Shell plc (at 9.38%), AstraZeneca plc (8.08%) and BP (4.75%) - all of which are up over 35% so far in 2022. The knock on effect is that we’ve seen some of the conventional wisdoms regarding active vs passive funds torn up, but also ethical funds underperform given their aversion to oil and gas stocks and their liking for tech stocks. Will ethical funds make a comeback in 2023?

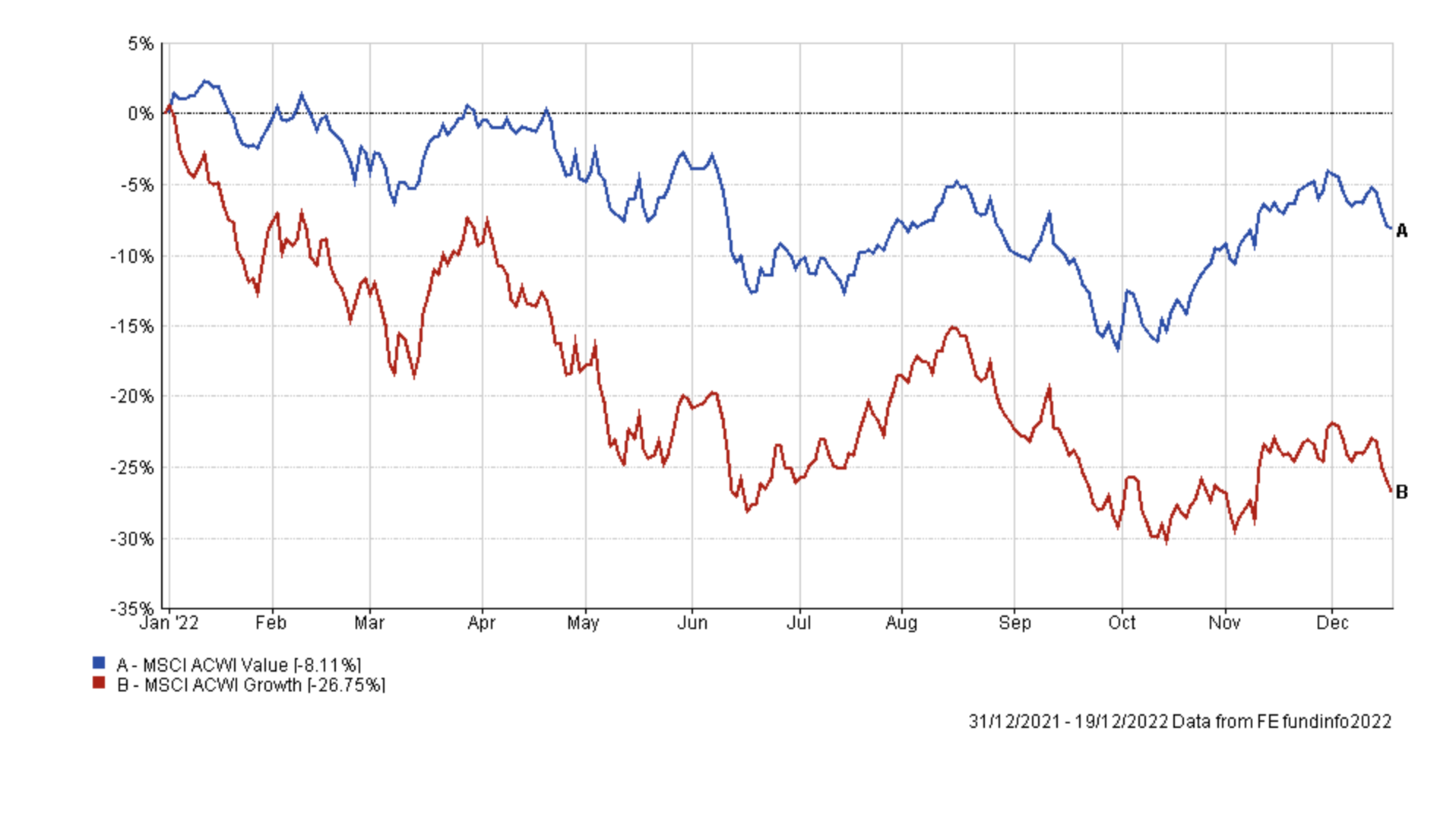

It also raises the question whether growth stocks will start to outshine value stocks again, or will we see a repeat of 2022 (shown below).

China

China could play an important role in what happens in 2023. Geopolitical tensions over Taiwan could cause market risk aversion as mentioned earlier. However, Chinese stocks had been among the worst performing asset classes up until the start of November when Chinese authorities began loosening covid restrictions. If China is able to move beyond the covid pandemic, fuelling economic growth, it could represent an interesting value opportunity for investors. It could also potentially spark a new rally in commodities. Conversely should supply chains be hampered by additional covid lockdowns or civil unrest a further slowdown in the world’s second largest economy will prove a drag on economic growth globally.

Corporate earnings

Ahead of each corporate earnings season of 2022 there were warnings of potential disappointment as consumers struggled with the cost of living crisis and companies navigated higher input costs. So far earnings seasons have fallen into the “not as bad as feared” category. However, 2023 may be a different story, as the above factors as well as tighter monetary policy (meaning higher mortgage costs) start to finally hit consumer spending and therefore company profits. If that happens then we can expect share prices to dip.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay