At the start of a new year, I like to write an investment outlook for the year ahead as well as glance back at the year that has passed.

Summary of 2023

This time last year I wrote about how investment managers fall foul of recency bias. Recency bias is defined in behavioural economics as where you incorrectly believe that recent events will occur again soon. This leads to an inaccurate and subjective assessment of the probability of events occurring in the future. In the world of investing this can lead to irrational and poor investment decisions.

For example, at the start of 2021 investment banks were too pessimistic in their predictions for the year ahead, following a dismal 2020. At the start of 2022 the opposite was true with investment banks being way too optimistic about how 2022 would pan out, following the strong equity market returns of 2021.

And so, once again, recency bias caused investment managers to be too pessimistic about their predictions for 2023 following a disastrous 2022, which was one of the worst years on record for bond and equity investors.

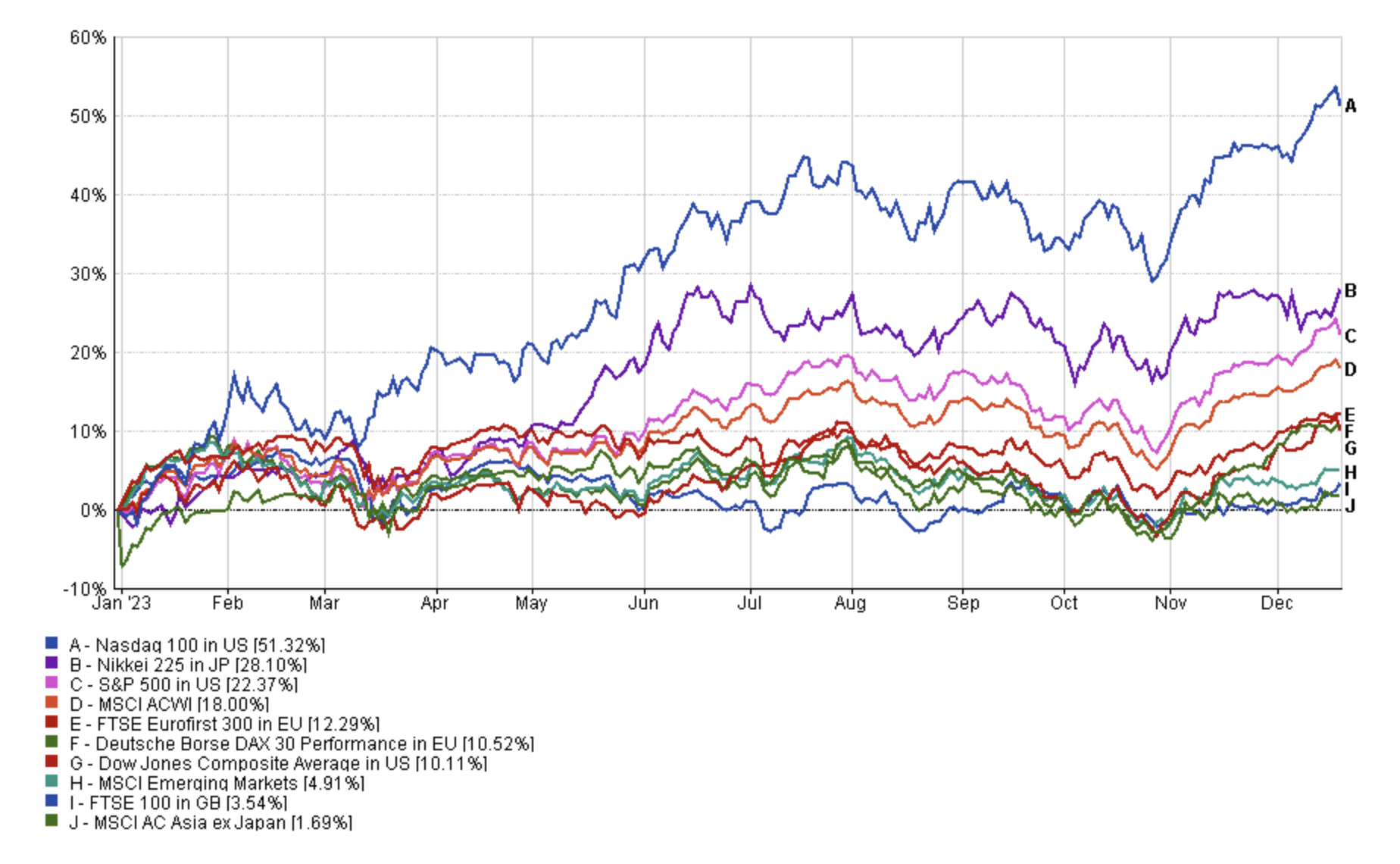

The chart below shows the performance in local currency terms of key stock market indices during 2023. The average prediction from a string of investment banks was for the S&P 500 to go nowhere throughout 2023. Well as you can see from the chart below they got that completely wrong, once again. In 2023 the S&P 500 rose over 22%.

In a large part 2023 was the inverse of 2022, with the previous year's laggards rallying strongly while 2022's winners (such as the FTSE 100) lagged.

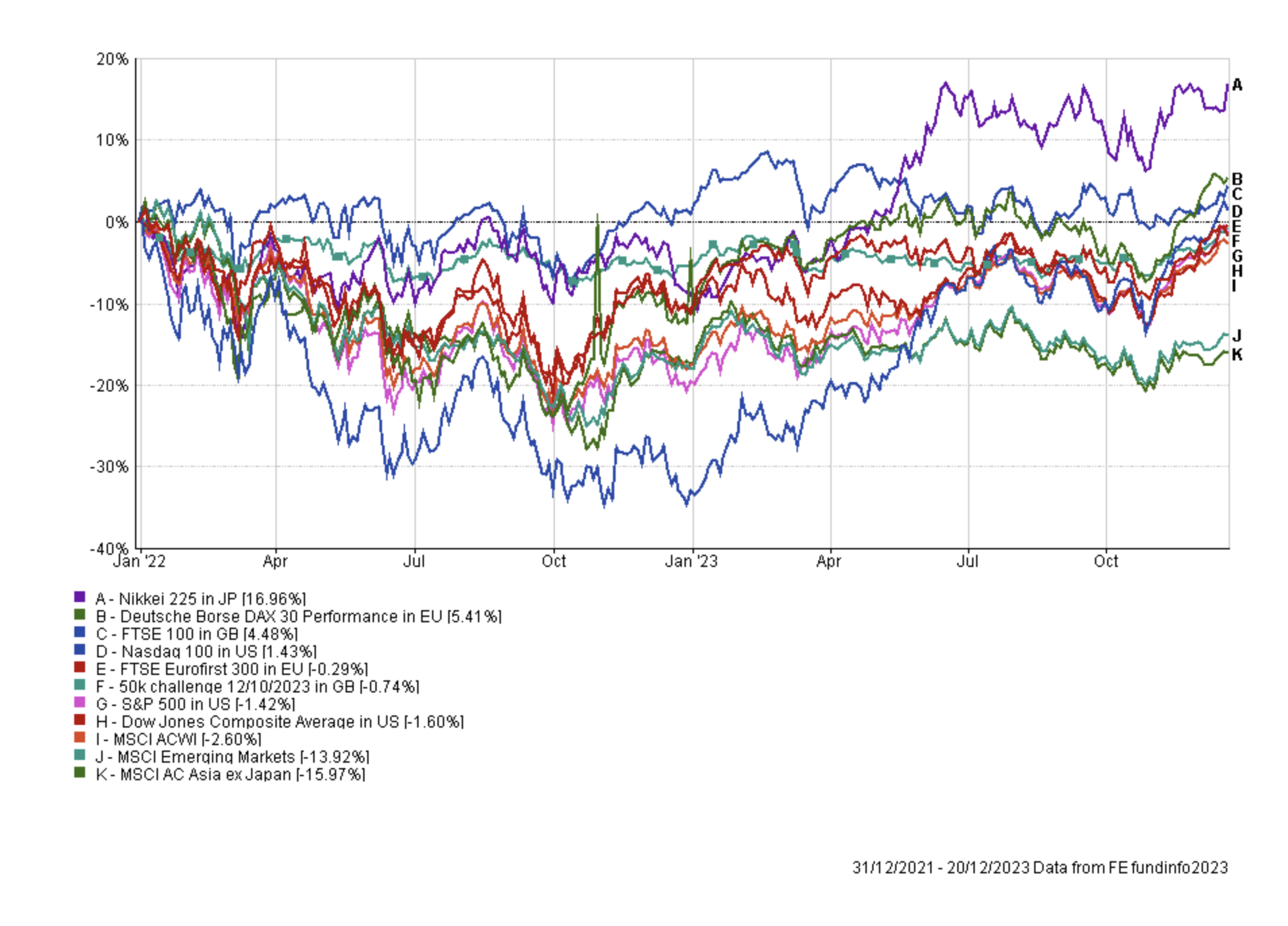

The chart below shows the performance of the key stock markets over the last two years in local currency terms, and with the exception of Japan's Nikkei 225, stock markets are either yet to break even, or if they have the gain is marginal. In other words stock markets have largely gone nowhere over the last two years.

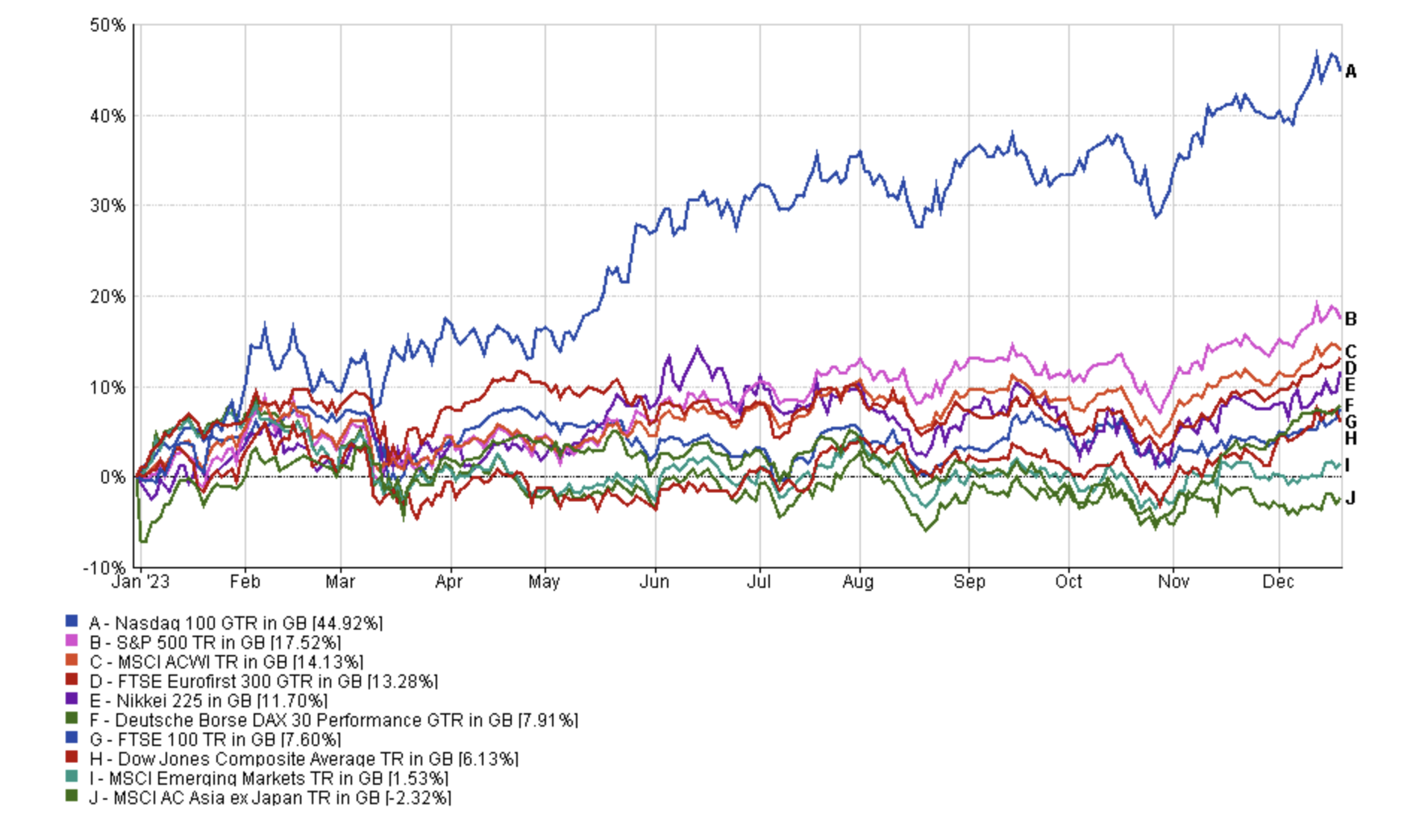

But returning to 2023, if you factor in currency moves, and in particular the recent strengthening of the pound the gains are reduced.

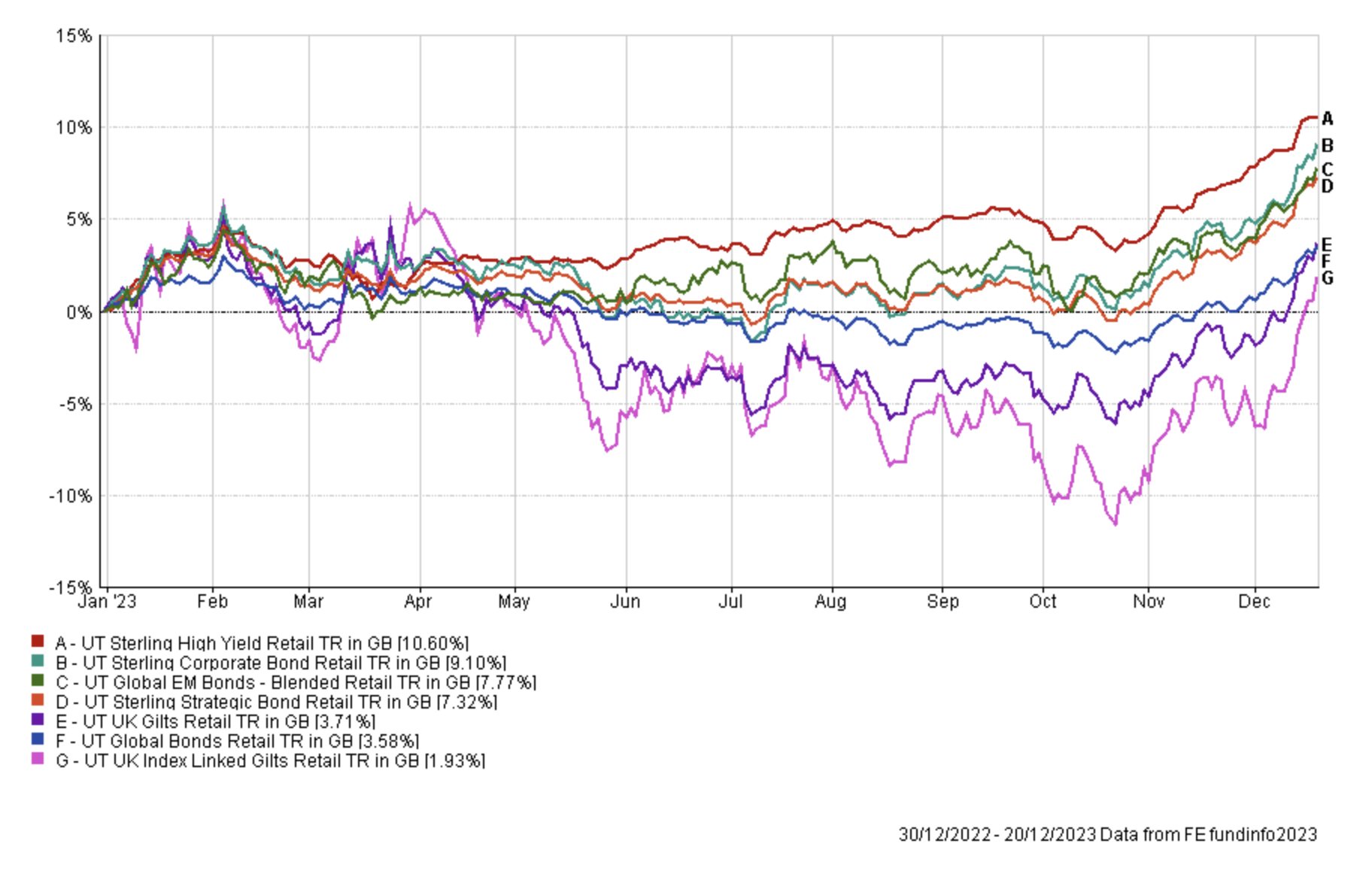

But what about the bond market? The chart below shows the average return from a range of bond fund sectors. While bonds managed to break even, those with longer duration were still sitting on heavy losses up until the end of October, when the market's inflation and rate expectations finally tumbled. This was also good news for equity/bond portfolios as both equity and bond markets rallied into the year end.

Outlook for 2024

As I explain each year, I usually pay little attention to investment bank predictions of where the markets will end up at the end of the following year because their predictions are clouded by recency bias. However some people are interested in what these institutions believe will happen. Below is a round-up of the S&P 500 predictions for the end of 2024 from some of the main investment banks. Beside each forecast you can see what the prediction represents in terms of a potential percentage increase (in blue) or decrease (in red) from the level of the S&P 500 at the time of writing (4700).

| Institution | S&P 500 forecast for end of 2024 | equivalent % return from current S&P 500 level* |

| JPMorgan | 4200 | -10.64% |

| Barclays | 4500 | -4.26% |

| Morgan Stanley | 4500 | -4.26% |

| Societe Generale | 4750 | 1.06% |

| UBS | 4850 | 3.19% |

| Bank of America | 5000 | 6.38% |

| CITI | 5100 | 8.51% |

| BMO | 5100 | 8.51% |

| Deutsche Bank | 5100 | 8.51% |

| Goldman Sachs | 5100 | 8.51% |

| Average | 4820 | 2.55% |

*this is based upon the level of the S&P 500 on 20th December 2023 which was 4700

Like previous years there is a wide discrepancy between the predictions, again almost a 20% difference between the best and worst case predictions. Interestingly some investment banks are clearly perennial pessimists (Barclays) while others are perennial optimists (Deutsche Bank).

Yet, if you take an average of the predictions (4820) it estimates that the market will rise 2.55% in 2024. However, many of the predictions were made at the back end of November, before the US Federal Reserve surprised investment markets with its dovish assessment of where interest rates will be in a year's time. It means that many of the investment banks are beginning to review their end of 2024 price targets and revise them higher. This is further evidence of how investment banks suffer from recency bias, when making future predictions.

But while "finger in the air" predictions of where the market will end up in the future are interesting they don't give any insight into how markets might behave throughout 2024. There are a range of potential investment themes and trends that investors will have to navigate in 2024, which will no doubt cause bouts of volatility, and I look at some of these below:

Interest rate cycle & monetary policy

The 16th October 2023 marked a turning point in bond markets, especially those with longer duration, as shown in the above chart where index-linked gilts began rallying strongly. The chart below shows how the 10 year US treasury yield hit a 16 year high of 5% on the 16th October 2023 before yields tumbled, meaning that the capital value of treasuries rallied. Yields continued to tumble into the year end driving bond prices higher and also boosting equity market sentiment.

The key driver of the turnaround was a shift in the market's expectations for central bank monetary policy, especially in the US. With inflation beginning to fall faster than expected, the market began increasing its bets that the US Federal Reserve (the Fed) would begin cutting interest rates in 2024. The US Treasury's decision to slow down the issuance of longer-dated treasuries provided further fuel for the rally. Then at the Fed's December meeting, the Fed's previously hawkish official rate projections suddenly suggested there could be as many as three 0.25% rate cuts in 2024! The market didn't need much encouragement to go dovish and is now pricing in over six 0.25% rate cuts next year!

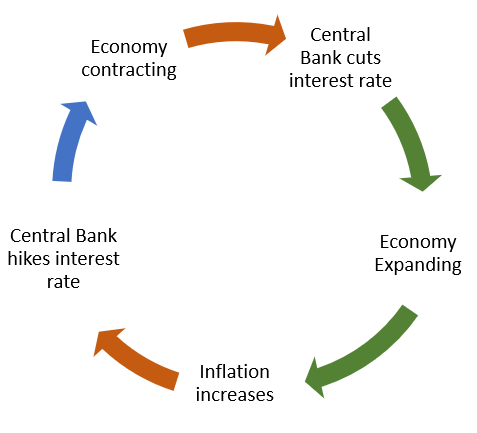

The chart below produced by Dailyfx provides a neat summary of the typical interest rate cycle. The bond market is now pricing in that we've moved from the 'central bank hikes interest rates' stage to the 'economy contracting' stage and will be heading into the "central bank cuts interest rate" phase during 2024.

But such a shift in market expectations isn't confined to the US. The market is now pricing in interest cuts in the eurozone and the UK. In respect of the latter, in the past week the market has ramped up bets that we will see up to 5 rate cuts from the Bank of England in 2024, taking the base rate to just below 4% by the end of 2024. It is currently at 5.25%.

However, it is worth remembering that rapid policy shifts (either way) can create their own problems. Events such as the collapse of Silicon Valley Bank in the spring of 2023 underscore the vulnerabilities within the financial system and the unexpected impact rapid policy shifts can have.

Recession

This brings me nicely on to the next theme that will likely preoccupy the market in 2024. If you recall at the start of 2023 the consensus view among economists and central banks was that in 2023, many economies worldwide would face a recession, albeit not simultaneously. The Bank of England (BOE) was operating under the assumption that the UK was already in a recession, which could last until late 2024. Similarly the eurozone was deemed to be in a recession at that time. Both assumptions proved wrong and neither economies officially entered recession during 2023. However, as expected, the US economy proved more resilient than most other developed world economies.

It meant that bond and equity markets see-sawed for most of the year as they wrestled with where respective economies and central banks were on the above rate cycle chart. Those who positioned their portfolios for a recession in 2023, with high bond exposure and exposure to defensive equity sectors will have been frustrated. So is that it? Has a recession been averted?

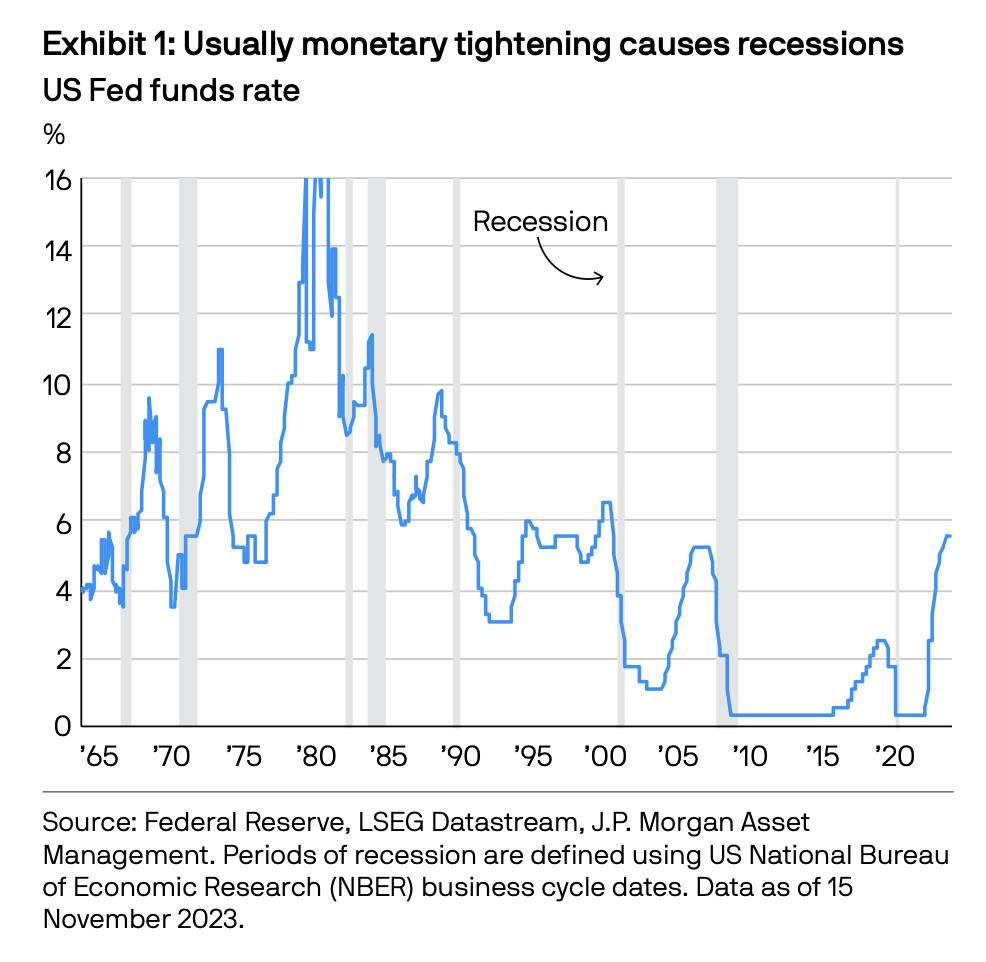

The chart below produced by JP Morgan illustrates how monetary tightening by the Fed usually causes a recession. Which means that the prospect of recession will remain a theme going into 2024. However, as you can see in the chart below, there are historical outliers where a recession didn't immediately follow aggressive rate hikes.

Interestingly, in the UK the ONS has just revised down its estimate for GDP growth during the third quarter (Q3) of 2024 from 0% to -0.1%. This means that the UK economy contracted by the same amount as the eurozone economy in Q3, setting up the potential for official recessions to be declared if both economies also contract in Q4 of 2023. Don't forget the accepted definition of a recession is two consecutive quarters of economic contraction. So the potential for recession remains.

The moves in bond markets (falling yields) since the end of October are also suggesting that bond investors are becoming increasingly concerned about the prospect of recession. But oddly, as pointed out in a recent newsletter, recession would have repercussions for equity markets, but equity investors are ignoring the threat right now.

Bonds are back

Perhaps the biggest theme gaining attention as we head into 2024 is the outlook for bonds. At least a key part of every investment bank's 2024 playbook could be summarised by the line "bonds are back". The previous two themes lead directly into why bonds have been rallying strongly into the end of 2023. The market believes that inflation has been tamed, economic growth globally is weakening and the odds of a recession have increased, which is the perfect environment for bonds to potentially outperform. In fact a number of investment banks believe that the outlook for bonds is better than for many developed world equity markets, especially US equities.

However, the end of year rally on bond markets, especially those with the longest duration which are the most sensitive to interest rate movements, has surpassed anything analysts had anticipated. But has the rally become overstretched and due a pullback? Interestingly the Financial Times reported yesterday that the 10 year US treasury yield, which has fallen from 5% to 3.89% since the end of October, is now below the end of 2024 target of 4% published by many investment banks, including Bank of America, Barclays, Deutsche Bank and Standard Chartered. Or in other words investment markets weren't expecting much more from the bond market when they made their predictions. Perhaps those predictions will now be revised.

'Bonds are back' is the consensus trade as we enter 2024, which makes it also susceptible to a sudden change in sentiment. Throughout 2022 and much of 2023, cash provided a better return than bonds and it may take a while for armchair investors to move back into bonds.

60/40 portfolio is also back

The diversified 60% equity and 40% bond portfolio (a 60/40 portfolio) had a disastrous 2022, falling -11.22%. Fast-forward to the end of October 2023 the typical 60/40 portfolio had spent much of 2023 flip-flopping but ultimately was sitting on little to no profit. However, following the Fed pivot and the market's change in outlook from 16th October 2023 onwards, the typical 60/40 portfolio rallied 6-8% into the year end, driven by the extraordinary turnaround in bond markets and the Santa rally in equity markets. Despite the strong rebound, since the start of 2022 the 60/40 portfolio is still in negative territory down around -2% to -5%. But while the 60/40 portfolio may be making a comeback, the lessons of the last two years are that diversification beyond just shares and bonds is wise. Just look at the price of gold, which has rallied more than 15% over the last two years.

Geopolitics

Geopolitical risks will remain in 2024 which means that alternative investments, such as oil and gold will garner some attention. Firstly, the U.S.-China trade tensions remain which could also impact global supply chains. 2023 will be remembered as the year of Spy balloons, the U.S. push for reshoring and diversifying supply chains (particularly in relation to semiconductor chips) as well as rising tensions surrounding China's position over Taiwan. In fact, the latest news headlines as I write this suggest that China's President Xi informed Joe Biden at their recent summit that China planned to unify Taiwan with the Chinese mainland by 2027. While there have been attempts by both sides to prevent tensions escalating, should they fail then investors will likely rebalance portfolios to reduce the impact of a trade war, much as they did during Trump's presidency.

Elsewhere, the war in Ukraine is ongoing and while Europe has looked to reduce its reliance on Russian energy it remains a potential inflationary risk should the war in Ukraine escalate. The situation in the Middle East is also a concern and has the potential to impact global energy markets and therefore produce upward inflationary pressures globally. In response to rising geopolitical risks, investors may shift towards more defensive strategies, seeking haven assets such as gold, the U.S. dollar and government bonds.

Politics

Domestic politics will inevitably play a big role in investment markets in 2024. Incredibly there are over 40 counties, representing half of the global population, that will have national elections in 2024. These include countries such as India, Taiwan, Indonesia, South Africa, the USA and possibly the UK. As we head into key elections there will be increasing pressure on incumbent governments on geopolitical issues as well as an increased likelihood of policy changes causing further uncertainty for businesses and investment markets. A number of the elections are also occurring in commodity rich countries as well as geopolitical hotspots such as Taiwan, so the possibility for global ramifications is heightened.

Of course the US election will itself garner the most attention as it always exerts a huge influence over markets in the lead up to and beyond the election date in November. Read my article from August 2020 on "What the US general election means for your investments" to gain some insights into the uncertainty we can expect. That's before we even consider the possibility of another Trump presidency and the impact that would have on geopolitics and trade tensions. The silver lining is that history tells us that the S&P 500 tends to rally over 11% in an election year, but nothing is certain.

The return of inflation

This is a theme that I wrote about in a recent newsletter and perhaps has the potential to pull the rug from under all investment markets should a second wave of inflation materialise.

In the autumn, the International Monetary Fund (IMF) published a study titled "One Hundred Inflation Shocks: Seven Stylized Facts," analysing over 100 instances of inflation shocks in 56 countries since the 1970s. The research draws attention to the enduring nature of inflation, particularly after terms-of-trade shocks, which occur when there's a sudden change in a country's export prices relative to its import prices. The Bank of England has acknowledged that the inflation issue in the UK stems from such a shock, exacerbated by a weak pound and expensive imported energy.

The IMF's report points out that only in 60% of these cases was inflation successfully reduced within five years following a terms-of-trade shock. On average, it took over three years to mitigate inflation in these instances. The concept of "premature celebrations" is also discussed in the IMF paper. Historically, initial signs of decreasing inflation have often misled policymakers into thinking the worst was over, only for inflation to stagnate or even surge again, catching both markets and policymakers by surprise. For example, post the oil shocks of the 1970s, several countries, including the UK, believed they had inflation under control. In the UK, inflation fell from 24% in 1975 to about 8% by 1978. This initial success led to a relaxation in monetary policies, but by 1980, inflation had soared back to nearly 18%, influenced by various factors such as wage-price spirals and global economic conditions.

Similarly, following the 2008 financial crisis, many economies thought they were recovering by 2010. The U.S. saw its inflation rate drop significantly in 2009, but by 2011, inflation had rebounded, driven by rising commodity prices and supply chain issues. These historical examples highlight the risks of prematurely relaxing monetary and fiscal policies in response to inflation. They also caution against early celebrations, as initial declines in inflation can be deceptive, and economies may soon face renewed inflationary pressures.

We now find ourselves in a similar position heading into 2024. Inflation appears to be abating thanks to higher interest rates. But historical evidence suggests that countries with longer-lasting strict monetary policies were more effective in resolving inflation. Yet the market, and to an extent central banks themselves, are anticipating rates to start falling as early as the spring of 2024. Are central banks and investment markets prematurely celebrating and will they pay the price?

Other themes

I just wanted to round-off this article by briefly mentioning a couple of other themes to watch out for.

US dollar weakness

I put this in the 'other' category, not because it's not important, but because I've written extensively in recent months on the influence that that US dollar has on investment markets.

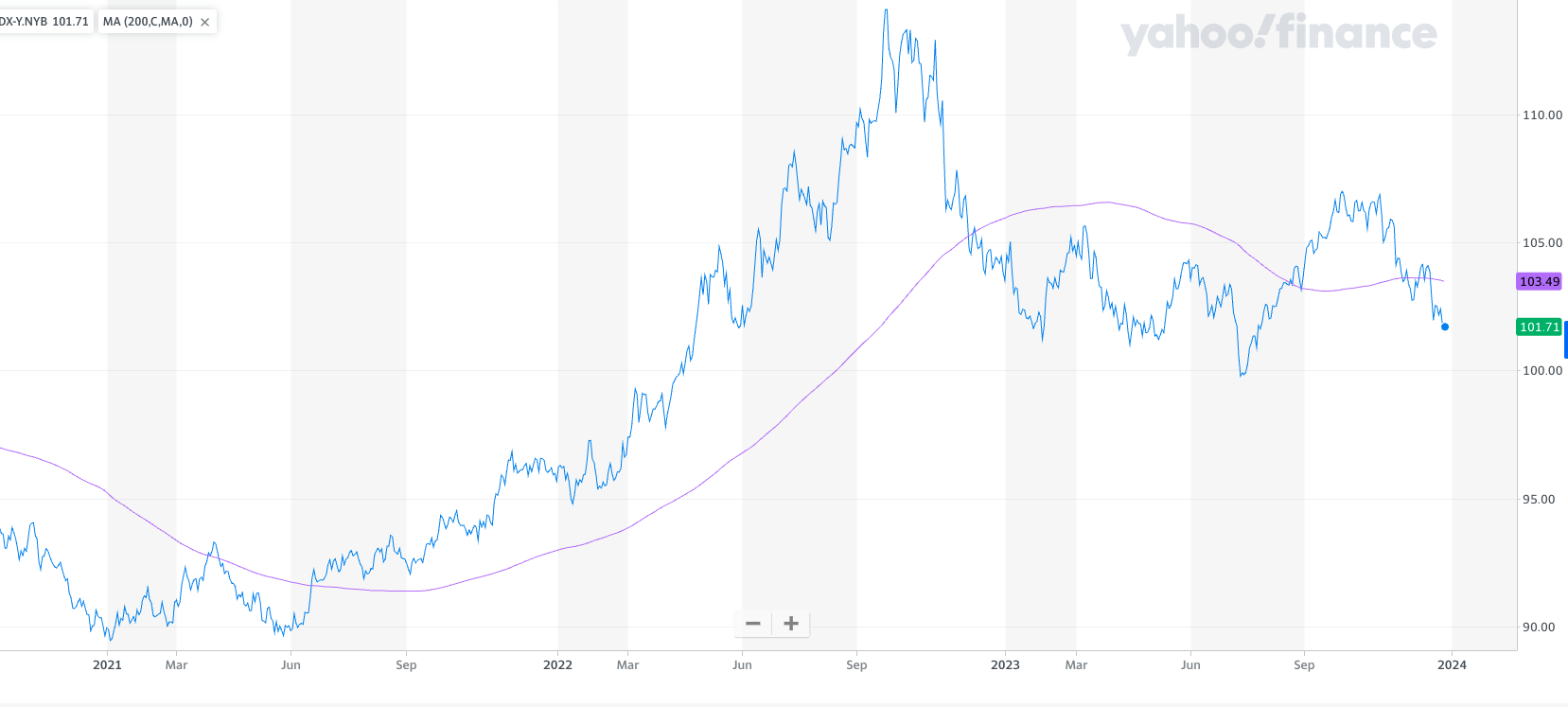

The US dollar index goes a long way to explaining many of the market moves we saw in 2023. With markets hanging on every move central banks make, much of this is being reflected in the movement of the US dollar index. If you get the direction of the dollar right you often get everything else right, be that currency, bond or equity markets.

At the time of writing (20th December) the US dollar index has plummeted since the end of October and the move has accelerated thanks to the Fed's dovish pivot. The index is fast approaching a key 101 support level and a break down from there could see further weakness. The index has also just broken below its 200 day moving average (the purple line in the chart below) which is bearish. If the downtrend continues it could prove a tailwind to assets including US equities, emerging market equities and gold. If instead the US dollar turns around and rallies hard, then expect the equity rally we've seen since the end of October to unravel.

Central bank divergence & currencies

Again this is a theme that I've touched upon in recent newsletters, but just as central banks didn't tighten monetary policy in unison, it is unlikely that they will cut interest rates in unison either. That will have significant implications for currency markets, with the most dovish central banks ultimately sending their currencies lower against their peers. Similarly, stock markets whose domestic central banks are deemed to be the most accommodative are likely to fare better. Given that the Bank of England is currently considered one of the more hawkish of major central banks right now, the resulting strength in the pound could harm UK investors' overseas returns and drive more of them to allocate their investments domestically.

China

China has been something of an enigma in 2023. Heading into 2023 Chinese stocks were among the worst performing asset classes but the hope was that China would be able to move beyond the covid pandemic, fuelling economic growth, which could represent an interesting value opportunity for investors. It was also hoped that it could spark a new rally in commodities globally. Yet these things didn't materialise. A lack of economic stimulus measures and a fragile property sector contributed to weaker than expected economic growth numbers. Unsurprisingly the Chinese stock market is down around -6.5% in 2023, as measured by the Shanghai Composite Index.

So with a sense of deja-vu many analysts are talking up the prospects of China's economy, for it to finally rebound and help drive the global economy. But we've been here before.

Artificial Intelligence

While this is the last theme mentioned in this outlook, it is by no means a footnote. This time last year AI wasn't even in the public psyche until the emergence of tools like ChatGPT, which have since started reshaping sectors such as healthcare, education, and logistics to name a few. The potential impact of AI both socially and economically is being likened to great moments in history such as the industrial revolution and the creation of the internet.

The development and application of AI is still in its infancy and while many will focus on the positives there are also challenges such as potential job losses, societal disruption and concerns over data privacy. The United States and China are both significantly investing in AI development, with China possibly taking the lead owing to its more relaxed privacy regulations. Could this be a source of further US-China tensions?

In 2024, the continued development of AI and the growth in its application will influence areas like cloud computing, the semiconductor industry and various technology sectors. There will be winners and losers (especially in the tech arena) but for investors it won't necessarily be easy to discern who they will be. This will especially be true in other sectors where AI applications will be developed, for example in healthcare and manufacturing. And of course, no comparison to the internet era would be complete without a warning that there is a danger that the foundations for another dotcom style bubble (which could ultimately burst) may be being laid already.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay