At the start of a new year, I like to write an investment outlook for the year ahead as well as glance back at the year that has passed.

Summary of 2024

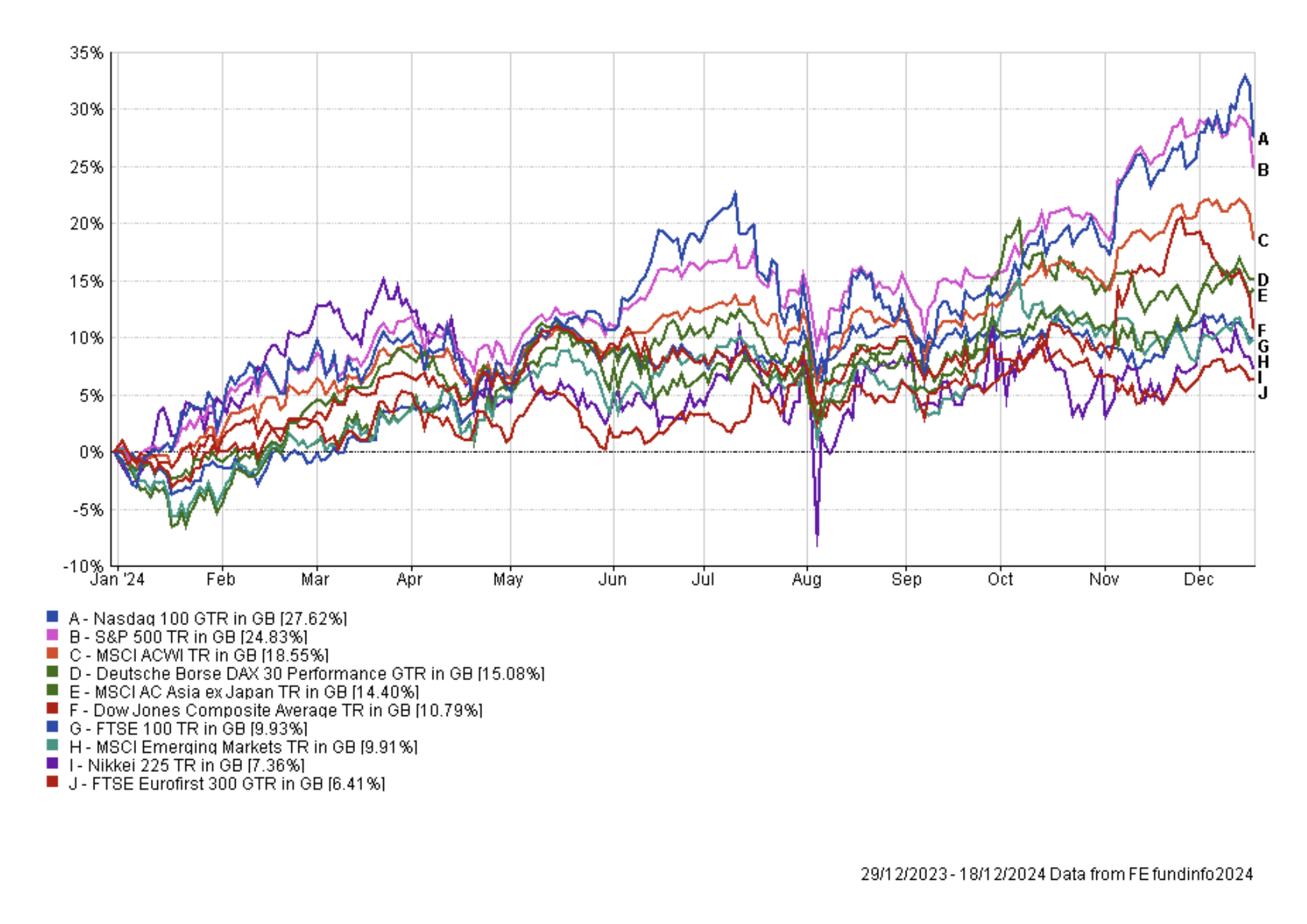

This time last year, the average prediction from the most well-known investment banks was for the S&P 500 to rise just 2.55% during 2024, to 4820. The more pessimistic investment bank, JP Morgan, predicted that the S&P 500 would fall as much as 10% during 2024. The chart below shows the performance in local currency terms of key stock market indices during 2024 and at the time of writing (19th December) the S&P 500 sits at 5900, having risen over 23%. This underscores, once again, the limitations of relying solely on professional predictions of where stock markets might head in the future. In the end 2024 turned out to be a stellar year for equity investors despite some pessimism at the start of the year.

The chart below shows the performance of the same stock market indices after taking into account currency market moves. Or in other words, the chart represents more closely what UK investors would have experienced if they had invested in the respective indices, assuming no currency hedging.

2024 was predicted to be a year where central bank monetary policy and politics collided to influence domestic stock market performance, which is pretty much how it turned out. The charts above highlight a trend whereby domestic stock market performance in 2024 generally aligned with the stability of the country's government and the looseness of its monetary policy. Those countries with stable, growth-oriented governments and central banks that pivoted towards looser monetary policy saw their stock markets generally perform better. Conversely, countries with unstable governments or those where central banks maintained a more restrictive monetary policy stance, versus their peers, generally saw weaker stock market performance.

For example, at the turn of the year the Bank of Japan (BOJ) was the most accommodative central bank, but then in August when the BOJ began hiking interest rates the Nikkei 225 collapsed. Meanwhile in France, interest rate cuts from the European Central Bank weren't enough to offset investor concern over the collapse of the French government. In the UK the FTSE 100's performance was hampered by its new government's lack of economic policy, until the Autumn Budget, which is when the announced policies spooked investors even more.

Other factors further amplified regional differences. The US stock market was fuelled by the "Magnificent Seven" tech giants and investors' clamour for exposure to the AI investment theme. The rotation towards value stocks, anticipated by some, did not fully materialise. Of course, some regions such as Europe also faced challenges from geopolitical tensions.

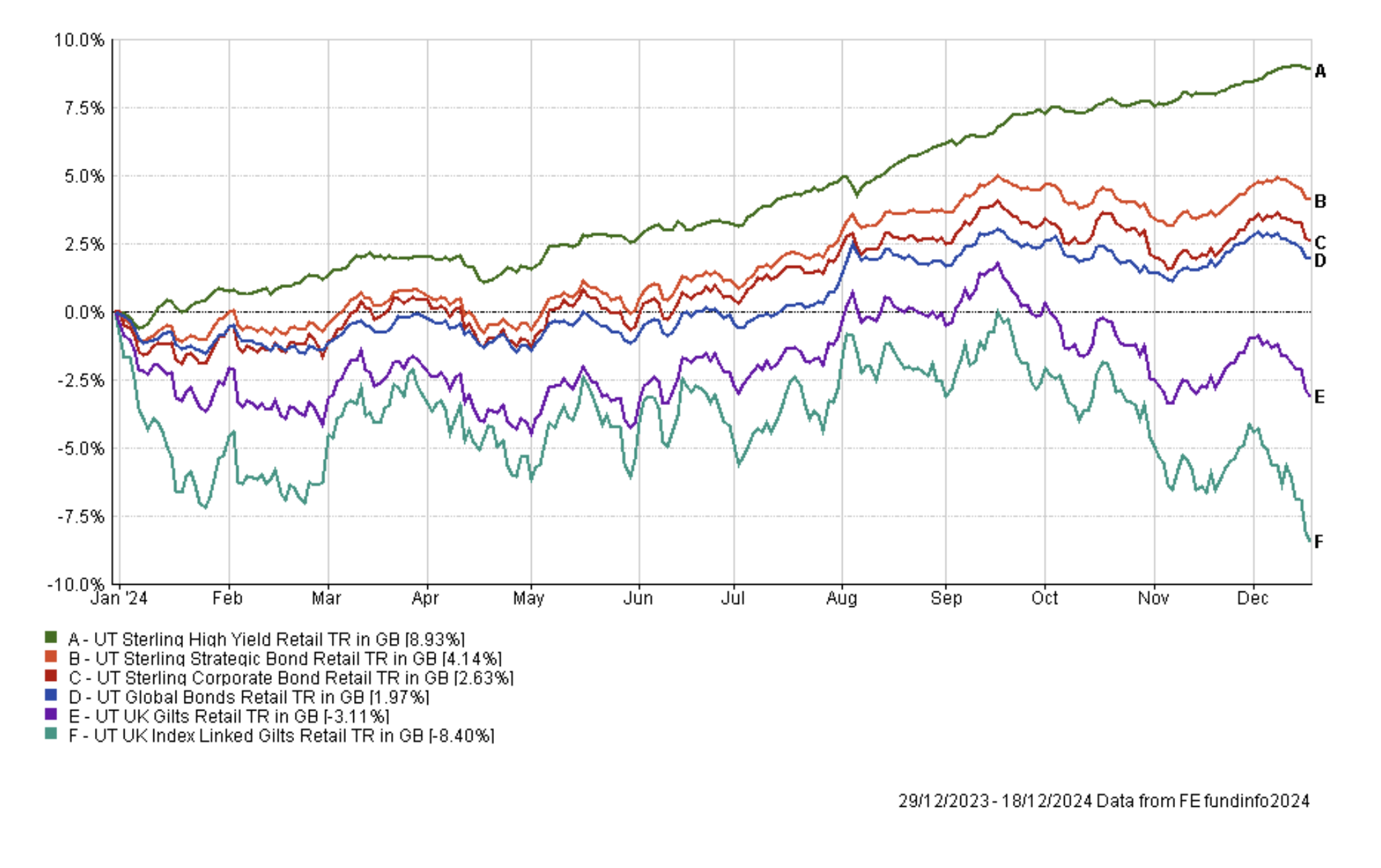

But what about the bond market? The chart below shows the average return from a range of bond fund sectors during 2024. Despite the Bank of England cutting interest rates, returns for UK investors varied wildly across different bond sectors. While high-yield bonds thrived, UK gilts and index-linked gilts suffered losses, highlighting the influence of factors beyond simple rate movements. Longer-duration bonds, like gilts, proved more susceptible to market volatility, even with falling rates. Inflation expectations played a role, with the underperformance of index-linked gilts suggesting investors prioritised factors like credit risk, given the outperformance of corporate bond funds. Also high yield bonds benefited from their high correlation to stock market performance, while global bond funds, with their significant US bias, benefited from the stronger performance of US treasuries and a slightly weaker pound. Given that you could easily secure more than 5% interest from a savings account in the UK, only those investors who invested in high yield bonds got a better return than cash.

Outlook for 2025

As I explain each year, I usually pay little attention to investment bank predictions of where the markets will end up at the end of the following year because their predictions are clouded by recency bias. Recency bias is defined in behavioural economics as where you incorrectly believe that recent events will occur again soon and leads to an inaccurate and subjective assessment of the probability of events occurring in the future. We saw this in the investment banks' predictions for 2021, 2022 and 2023, and to a lesser extent for 2024.

Nonetheless, many investors are interested in what these institutions believe will happen. Below is a round-up of the S&P 500 predictions for the end of 2025 from some of the main investment banks. Beside each forecast you can see what the prediction represents in terms of a potential percentage increase/decrease from the level of the S&P 500 at the time of writing (5900).

| Institution | S&P 500 forecast for end of 2024 | equivalent % return from current S&P 500 level* |

| Deutsche Bank | 7000 | 18.64% |

| Société Générale | 6750 | 14.41% |

| BMO Capital Markets | 6700 | 13.56% |

| Bank of America | 6666 | 12.98% |

| Barclays | 6600 | 11.86% |

| Morgan Stanley | 6500 | 10.17% |

| Goldman Sachs | 6500 | 10.17% |

| UBS | 6500 | 10.17% |

| JP Morgan | 6500 | 10.17% |

| Average | 6635 | 12.46% |

*this is based upon the level of the S&P 500 on 19th December 2023 which was 5900

Perhaps the most striking observation from the above table of predictions is the complete absence of bearish forecasts. Not a single investment bank anticipates a decline in the S&P 500. This bullish sentiment likely reflects the recent strong performance of the US market and once again demonstrates the inherent recency bias prevalent in forecasting.

Investors would be wise to approach these forecasts with the usual healthy dose of skepticism and focus on understanding the underlying investment themes and trends that will shape the market landscape in 2025. There are a range of potential investment themes and trends that investors will have to navigate in 2025, which will no doubt cause bouts of volatility, and I look at some of these below:

Trump trade 2.0

Donald Trump's re-election victory has sparked a new wave of market activity, dubbed the "Trump trade 2.0", as investors reposition themselves for a second Trump term in office. The US dollar has already shown strength, rallying almost 4% against other major currencies. This echoes the market reaction seen in 2016 following Trump's initial election victory. However, predicting the long-term impact of the "Trump trade 2.0" is complex due to Trump's unpredictable nature.

As we head into 2025, US equities have surged since the US election, mirroring the post-election moves of 2016. Pre-inauguration momentum suggests US stocks could continue to perform well into early 2025 if historical patterns hold. However, the 2024 surge is unevenly distributed across sectors. Unlike 2016 when infrastructure spending hopes boosted industrials and materials, in 2024 sectors like financials and consumer discretionary have been the standout performers thanks to hopes of lighter regulation in the financial sector as well as the influence of prominent US tech figures, such as Elon Musk, on the incoming administration.

We've also seen a decline in bonds and emerging markets as the US dollar strengthens while concerns over Trump's protectionist trade policies have hurt emerging markets as well as muddied the outlook for European equities. Looking at Trump's first term (2017-2021) provides some insight into possible long-term trends. Equities generally outperformed bonds during Trump's first term which aligns with typical market behaviour during periods of economic growth, suggesting a stronger US economy under Trump could benefit stock markets. Surprisingly, Chinese equities were the second best performing asset class despite the trade war. This highlights the influence of global factors beyond US policy.

Also, the 2017 "Trump Slump" underscores the importance of actual policy implementation over pre-election promises. The current political landscape with slim Republican majorities raises the possibility of similar legislative hurdles and potential market volatility in 2025. For more insights read my article "How to play the Trump trade 2.0".

US trade wars

Donald Trump has recently escalated his protectionist trade rhetoric, threatening significant tariffs on key trading partners when he takes office. He announced plans to impose a 25% tariff on imports from Mexico and Canada, along with an additional 10% tariff on imports from China. This comes alongside another threat of a 100% tariff on goods from BRICS nations (Brazil, Russia, India, China, and South Africa) if they proceed with plans to create a currency that could rival the US dollar. So while the size of the tariffs seems to change on a day to day basis the underlying threat doesn't

Trump also claims tariffs are a cornerstone of his plan to protect domestic industries, which would force overseas companies to move their manufacturing operations to the US. However, the economic implications of such tariffs could be substantial. For US consumers and businesses, these levies would result in sharply higher costs for imported goods, particularly those coming from North American neighbours, which are central to US supply chains. A 25% tariff on Mexican and Canadian imports would severely impact sectors like automotive manufacturing, agriculture, and industrial production, all of which rely on cross-border trade. The extra tariffs on Chinese imports could cause prices on consumer electronics, machinery and household goods to rise for US consumers, potentially driving up inflation.

Interestingly, there is some hope that the UK may escape the worst of Trump's trade tariffs. Unlike countries such as China, Canada and Mexico which export more goods to the US than they import from it, the opposite is true of the UK. Additionally, 50% of the UK's trade with the United States is in services rather than goods, a sector less directly affected by tariffs.

While the UK economy might be positioned to endure these tariffs far better than other major economies it doesn't automatically mean that its domestic stock market will outperform others hit by tariffs. As mentioned in the previous section, Chinese equities were the second best performing asset class during Trump's first presidency, despite the trade war.

Will gold continue to shine?

2024 was an amazing year for gold investors, as shown in the chart below. The price of gold has risen over 28% so far in 2024, meaning that it outperformed most major stock market indices.

Gold's rally was driven by a combination of macroeconomic and geopolitical factors, including persistent inflationary pressures and safe-haven demand. Additionally, the US Federal Reserve’s monetary easing policy, including interest rate cuts totalling 1%, weakened the US dollar, making gold more attractive to international investors. This trend was reinforced by ongoing central bank purchases and increased demand from China and India. It means that gold was an incredible diversifier to hold within your portfolio in 2024, which of course I did within my own £50k portfolio.

But will gold continue to shine in 2025? The drivers behind gold's epic rally in 2024 remain, so there is certainly the potential for further upside. However, if you look at my recent technical analysis outlook for gold, you will see that its price has stalled. And while it remains above the green uptrend line (shown above) the cup and handle pattern which predicted the rally in 2024 (you can see it via the link), points to a possible high around $3,000 per ounce in 2025. If that is so that equates to approximately 12% upside, but that is in no way guaranteed. However, after such a parabolic move in 2024, investors shouldn't be surprised if we see a pullback.

Artificial Intelligence

Last year Artificial Intelligence (AI ) was the last theme mentioned in my outlook, but its importance and prominence warrants an earlier mention in this year's note.

The surge in AI-related equities (which includes semiconductor manufacturers, cloud-computing providers and pure-play AI software companies) has been one of the defining market trends of the past two years. By late 2024, many of these stocks have soared well beyond their historical valuation ranges, raising questions about sustainability and the risk of a downturn in 2025. According to Goldman Sachs, the forward price-to-earnings (P/E) ratio for a basket of prominent US-listed AI-focused companies averaged around 40x in Q4 2024, compared to 25x at the end of 2022. This 60% increase in P/E ratio far outpaces the broader market’s expansion. In contrast, the S&P 500 currently trades at approximately 20x forward earnings (versus 18x in late 2022), illustrating that AI-related stocks are eye-wateringly expensive. Add to that the uncertain future profitability of AI as well as the spiralling costs incurred by those investing in the technology, such as Microsoft and Alphabet, it's no wonder some analysts are predicting another dotcom-style crash.

A recent J.P. Morgan research note stated that the top 10 AI-driven technology names accounted for nearly 30% of the S&P 500’s total gains in 2024. So if the AI-theme does implode so too will the wider stock market indices.

But there are other potential headwinds for the AI-theme, in the form of geopolitics and regulation. For example, escalating US-China tech tensions could disrupt supply chains or spark regulatory actions that curb the flow of critical semiconductor technologies. Given that many AI leaders rely on cutting-edge chips and stable trade relations, any policy shocks could undermine growth forecasts and hurt share prices. We've already seen this start to play out in recent weeks when China launched an antitrust probe into Nvidia, following the US restricting China's access to advanced AI chips. China also banned exports of critical minerals to the US and implemented policies favouring Chinese-made products. While some see these actions as negotiating tactics, others worry about a full-blown trade war, especially given the hawkish stance of the incoming Trump administration and China's increased willingness to retaliate.

Up until now investors have enjoyed all of the rewards (profits) from investing in AI, but 2025 could well be the year when we see the associated risks finally make themselves known.

Interest rate cycle / monetary policy / bonds

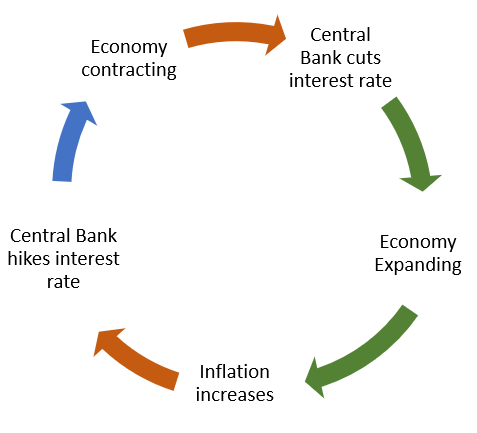

As we move into and through 2025 another driver of investment markets will be monetary policy. In last year's investment outlook I shared the image below from DailyFX to give context of where we were in the interest rate cycle.

Back then the bond market was suggesting that the US had moved from the 'central bank hikes interest rates' stage to the 'economy contracting' stage and would be heading into the "central bank cuts interest rate" phase during 2024. The same was true for the UK. As it turned out, the UK briefly entered recession at the end of 2023 and we have in fact now moved into the 'central bank cuts interest rate' part of the cycle. While the US avoided a recession, the US Federal Reserve along with the European Central Bank started cutting interest rates too. While the exact number of interest rate cuts predicted by investment markets for 2024 was way too optimistic, it's the direction of travel that was important.

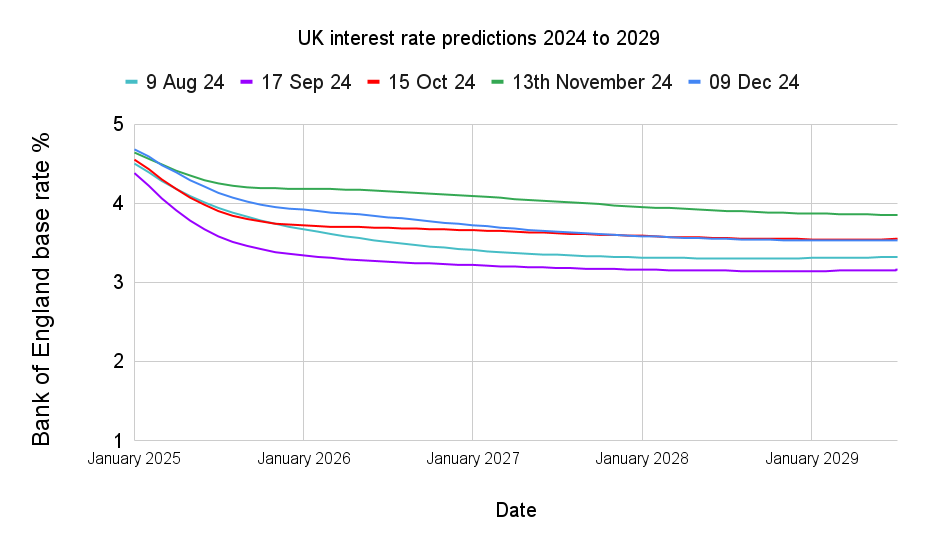

Investment markets had predicted that the Bank of England base rate would already be down to around 4%, but we are still at 4.75%. The market now thinks that the base rate in the UK will have to stay higher for longer, due to persistent inflation, as shown in the chart below, not falling below 4% until late 2025. Each coloured line in the chart represents the market's prediction made on the specified dates as to where the Bank of England base rate will be over the next five years

But it's not just in the UK where inflation concerns persist. The chart below shows how the 10-year US treasury yield hit a 16 year high of 5% on the 16th October 2023 before yields tumbled, meaning that the capital value of treasuries rallied. Yields continued to tumble into the start of 2024, driving bond prices higher, but yields rose at various points of the year meaning that 2024 wasn't as good for bond investors as they had hoped. While the overall trend is still lower, for now at least, if bond yields push higher (above the red line shown), the downtrend would be broken causing treasuries and global bond funds to struggle.

As we enter 2025, bond investors are cautious despite the prospect of further rate cuts from key central banks. But if we do see aggressive interest rate cuts by the Bank of England, perhaps over new recession fears, then it could prove a boost for overseas assets within your portfolio. Read my past article titled 'Investing throughout the interest rate cycle'. Furthermore if global central banks begin to diverge in terms of monetary policy (e.g. they don't all cut interest rates at the same pace) then that will likely influence the returns on the respective domestic stock markets. We saw a hint of that in the days before Christmas when the US Federal Reserve cut its main interest rate by 0.25%, but then projected that it would only cut rates twice in 2025 rather than the previously predicted 4 times. This caused the S&P 500 to fall almost 3% in a single day, the biggest one-day sell-off since August.

60/40 portfolio is back

The 60/40 portfolio endured a tough couple of years between 2022 and 2023. In fact, if you look at the performance over the last 3 years, then the 60% equity and 40% bond portfolio (a 60/40 portfolio) only bounced back into positive territory in April this year. While the 60/40 portfolio may be making a comeback, the lesson of recent years is that diversification beyond just shares and bonds is wise. Just look at the price of gold, which has rallied almost 50% over the last two years.

Interestingly research published on the 60/40 portfolio in the US suggests that when the 10-year US treasury yield is above 4% then it tends to benefit the performance of the 60/40 portfolio versus just investing 100% in the US stock market. Or in other words, there is a sweet spot when equities and bonds play nicely within a 60/40 portfolio rather than offset one another. At the moment the 10-year US treasury yield hovers just above the 4% level as it did for large parts of 2024, when the 60/40 portfolio returned an impressive 11%. The point is that investors don't necessarily need bond yields to tumble to make money with a 60/40 portfolio.

Geopolitics

As 2025 begins, geopolitical risks remain, keeping markets on edge which could prompt investors to seek refuge in alternative assets like gold, the US dollar and US Treasuries. The complex dynamic between the US and China goes beyond the potential for an escalating trade war, as tensions over Taiwan show no signs of easing.

The war in Ukraine continues to be a major factor influencing European energy policies and broader global markets while in the Middle East, instability has escalated, particularly following the collapse of Bashar al-Assad's regime in Syria. This has created a power vacuum, increasing regional tensions and potentially threatening global energy supplies. Coupled with broader unrest across the region, these developments heighten concerns about supply chain disruptions and their potential to amplify inflationary trends.

Inflation: Déjà Vu

Last year, I cautioned against the "return of inflation," highlighting the IMF's research that painted a sobering picture of inflation's persistence, especially following terms-of-trade shocks. I drew parallels to the 1970s and the post-2008 period, where premature declarations of victory over inflation proved misguided. Policymakers prematurely eased policy ahead of an unforeseen resurgence in inflation.

Fast forward to 2025, and the inflation narrative feels eerily familiar. Aggressive monetary tightening seems to have brought inflation under control in the EU, UK and the US. But a sense of unease lingers, fuelled by the latest official data showing UK inflation rising to 2.6% in November, quashing hopes of a pre-Christmas interest rate cut from the Bank of England. Moreover, the potential for unforeseen geopolitical or economic shocks could easily reignite inflationary pressures.

It seems that once again the threat of inflation returning will be at the back of investors' minds. Therefore, expect official inflation data releases to act as catalysts for short-term market volatility.

US dollar

The consensus among investment analysts is for the US dollar to strengthen further as we move into 2025. The strength, or weakness, of the US dollar significantly influences investment markets. A strong dollar not only tends to hit US stocks but also commodities (especially gold) as well as proving a headwind for Asian and emerging markets. In contrast, a strong dollar versus the Japanese yen tends to be positive for the Nikkei 225, while a weaker pound versus the stronger US dollar can provide some support for the FTSE 100.

However perhaps we should be wary of a consensus. In 2016, a stronger US dollar was a hallmark of the Trump trade back then. While the dollar initially surged after his 2016 election win, it peaked by the end of that year, before Trump officially took office, and then sharply declined throughout 2017.

This downturn, dubbed the "Trump slump," was largely attributed to the administration’s inability to deliver on healthcare and tax-cut reforms promised during the campaign. Some observers might highlight that in 2024, the Republicans have achieved the "trifecta" (control of the presidency, House of Representatives, and Senate), potentially enhancing Trump's ability to implement reforms this time. However, it's worth noting that the Republicans also held the trifecta in 2016. Heading into 2025, the GOP will hold the slimmest margin of control in both chambers of Congress for any president since Bill Clinton, indicating a genuine possibility of another "Trump slump" in 2025, with broader implications for investment markets.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay