As a result of the Brexit vote the value of the pound versus the dollar has now become the proxy for investment market sentiment, particularly in the UK. The pound's problems have been compounded by those investors who are actually shorting the pound to try and offset losses elsewhere. The falling pound has provided a buffer for a lot of UK investors to insulate them from the worst of the Brexit fallout and other macro issues. The more shrewd (such as 80-20 Investor members) have even been able to make money from the fall in the pound. So will the falls continue or are we in for a shock?

Why the value of the pound matters

In last week's newsletter I explained why it's now all about the pound. It would appear that the national media are only just cottoning on to this fact. I've been contacted by a number of national newspaper journalists this week asking me how important hedging against a weak pound is for investors right now.

The reality is that for the moment the strength of the pound is having a bigger impact on UK investors' returns than they've ever likely experienced (even though they might not realise it). If you invest globally, without any currency hedging in place, then when the value of the pound falls it gives a currency kick to your overseas funds. This in turn turbo charges the investment returns, even if those overseas stock markets or assets are falling when viewed in their domestic currencies. That's exactly how 80-20 Investor members have been able to make so much money in the aftermath of the referendum.

Yet the value of the pound has even affected investors who have been solely invested in UK equities. The reason the FTSE 100 is up 5.41% since the referendum while the FTSE 250 is down 3.04% is due to the fall in the value of the pound. Approximately 70% of FTSE 100 companies' earnings are from overseas which gives their profits a currency boost when repatriated to the UK. The FTSE 250 on the other hand is mostly made up of domestically focused businesses. So people investing in large cap multinationals (FTSE 100) have benefited from the weak pound although they often don’t realise. If you want to get exposure to UK stocks it makes sense to focus on large caps with earnings overseas (think FTSE 100) as your portfolio will be supported by a weak pound.

There's no getting away from the fact the value of the pound will impact our investment returns one way or another over the coming weeks and months.

The crash after the referendum

Currencies only increase or decrease in value with reference to another currency. For the purposes of this article I will look at the value of sterling versus the dollar, given that most global assets we invest in are denominated in US dollars.

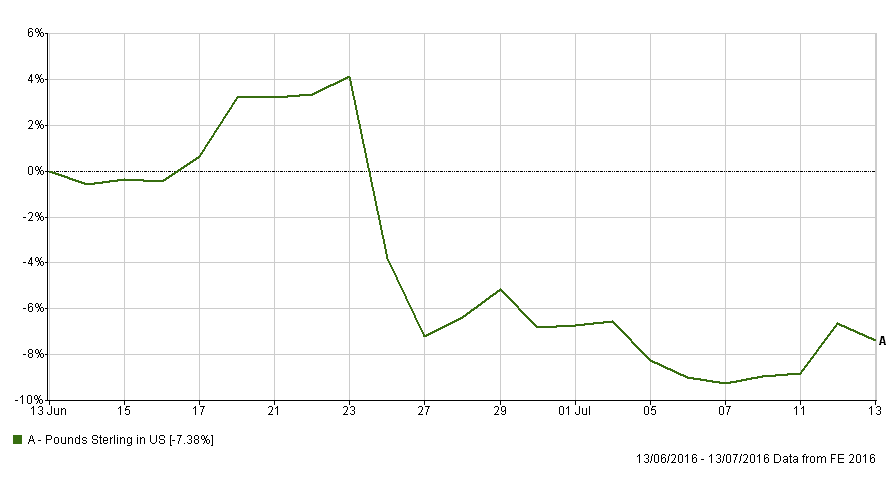

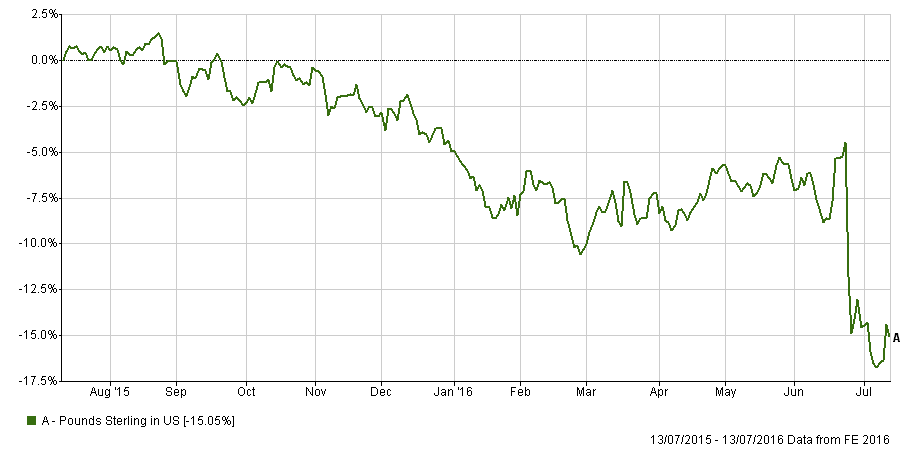

Before the referendum 1 USD was equivalent to £1.4814 as shown in the chart below (click to enlarge). However, since that time the pound has plummeted in value, down 12% and below $1.30 at its worst, to levels not seen for over 31 years.

However, the rot had set in long before the referendum as fears over a potential Brexit grew and concerns over the outlook of the sluggish UK economy versus the more buoyant US economy emerged.

End of year forecasts for the value of the pound

In the weeks following the Brexit investment banks and analysts had to tear up their forecasts for the value of the pound and reassess them. Below is a roundup of some of these forecasts which were made when the pound was roughly where it is now at around $1.33:

- According to the BBC Swiss bank Julius Baer, ranked as the industry's most accurate currency forecaster by financial data provider Bloomberg, it predicts the pound will fall to $1.16 by the end of 2016

- Standard & Chartered predicted $1.18 by the end of 2016

- Capital Economics expect a slide to $1.20

- HSBC expects the pound to fall to $1.20 by the end of 2016

- while Deutsche Bank sees it falling more than 13% further to $1.15.

I could go on but the overwhelming consensus is that the pound has much further to fall. Yet consensus worries me especially when it comes to currency markets. History is littered with examples of when the consensus was spectacularly wrong. In the last month alone markets crashed after they banked on the fact that the UK would remain in the EU. The immediate market crash was the unwinding of the bets backing the consensus view. 80-20 Investor members made so much profit precisely because they weren't following the consensus.

Then today the market had priced in a 90%+ chance that the Bank of England (BOE) would cut interest rates. Yet it didn't and the pound rallied over 1.5% to $1.332 as a result. If a central bank cuts its benchmark interest rate then investors are inclined to sell that currency in favour of one paying a higher interest rate. In addition, should the Bank of England print more money to boost the economy (known as Quantitative Easing or QE) it would mean that there are more pound notes washing around the economy chasing the same number of assets. It follows that the value of the pound will fall. Yet the BOE didn't cut rates or resort to more QE.

This released the downward pressure on the pound, for now at least. Yet the meeting notes that accompanied the BOE rate decision today stated that most members of the Monetary Policy Committee (the group inside the BOE who set the base rate) expect monetary policy to be loosened in August,” and are considering “a range of possible stimulus measures”. So this would suggest that the downward pressure on the pound could return, but only if the BOE thinks the economy is showing real signs of struggling.

Short term forecast of the pound vs the US dollar

But what about the short term? Even if you accept the consensus view that the pound could fall further (but as I say consensus makes me nervous) the movement won't be in a straight downward line. This week, for example, the pound has rallied over 3% on the back of the BOE decision and the announcement of a new Prime Minister.

In fact the pound is showing signs of more gains in the short term if you just look at technical trading patterns. There is a decent chance that we could see the pound rise towards $1.35 or $1.36. With the the next target being $1.38 which is some 3-4% higher than where we are now. This will unlikely be good news for the FTSE 100 or any assets (such as global funds) denominated in foreign currencies.

What should investors do?

80-20 Investor members have been well positioned to benefit from the weak pound following the Brexit vote. My own £50,000 portfolio is still up over 10% since March 2015. While the consensus is that the pound will fall further currency markets have a nasty habit of ignoring the consensus view. So it’s ok to diversify (using global equity and bond funds - see my £50,000 portfolio and the Best of the Best Selection for ideas) in order to hedge against a weakening pound but don't bet the house on the fact it will definitely happen and to the degree you hope. If we look at the 80-20 Investor Best of the Best Selection's outperformance over time it would suggest that you should aim for around 20-30% exposure to UK assets (across both equities and bonds combined). The rest of your portfolio should be invested globally.

It's worth keeping an eye on economic news that comes out in the coming weeks, although I will cover it of course. Bad news will push the pound lower and your global assets should receive a currency boost. If the economy is holding up better than everyone feared then the pound will rally further. There is also the outside chance that interest rates could have to rise sooner than people think if we get an inflation shock, brought about by the weak pound pushing up import costs. If rates did rise then the value of the pound would rocket.

However as a long term investor you shouldn't obsess too much over currency moves, but simply ride them when they are strong in order to boost your returns, as we have in the last month. Be comfortable with the fact that you won't predict the currency markets or time them perfectly. The 80-20 Investor algorithm and process will ensure that you review and change tact when/if currency markets turn.

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay