If you’ve been reading my weekly and monthly newsletters you will know that late summer is traditionally a bad time for equity returns. This seasonal trend forms the basis of the investment mantra ’Sell in May and go away, don't come back till St. Leger Day’. While the Sell in May adage is hit and miss others are more reliable . Take the Santa Rally for example which I’ve shown to exist. However there are lesser known investment adages and trends which traders look to exploit.

One such adage is what I call ‘Fall’s gold’. The premise is that the autumn (the Fall as our American friends call it), in particular September, is the best time of year to buy gold as a seasonal surge in demand drives up the price of gold. The seasonal demand is mainly driven by China and the Indian festival/wedding season at the end of September. But is September really the best time to buy gold? Is there even a seasonal trend in the price of gold? This question takes on even greater significance this year after the gold price rallied over 5% in August on the back of geopolitical concerns focused on North Korea. With the price of gold breaking up through the crucial resistance level of $1,300 (as set out in my article 'The outlook for Gold and Silver') could the precious metal be about to receive a seasonal boost?

Fall's gold

To answer these questioned I analysed the monthly performance of a popular gold ETF, namely ETFS Physical Gold which tracks the performance of the gold price, from 2004 to date. The chart below shows the average return for each calendar month over the 14 year period. Click on the image to enlarge it.

The evidence suggests that there is seasonality to the price of gold with August and September being strong months. In contrast, the second quarter of the year is a poor time historically to invest in the precious metal. However, based on the data the best time to invest in gold is in fact the new year (January and February).

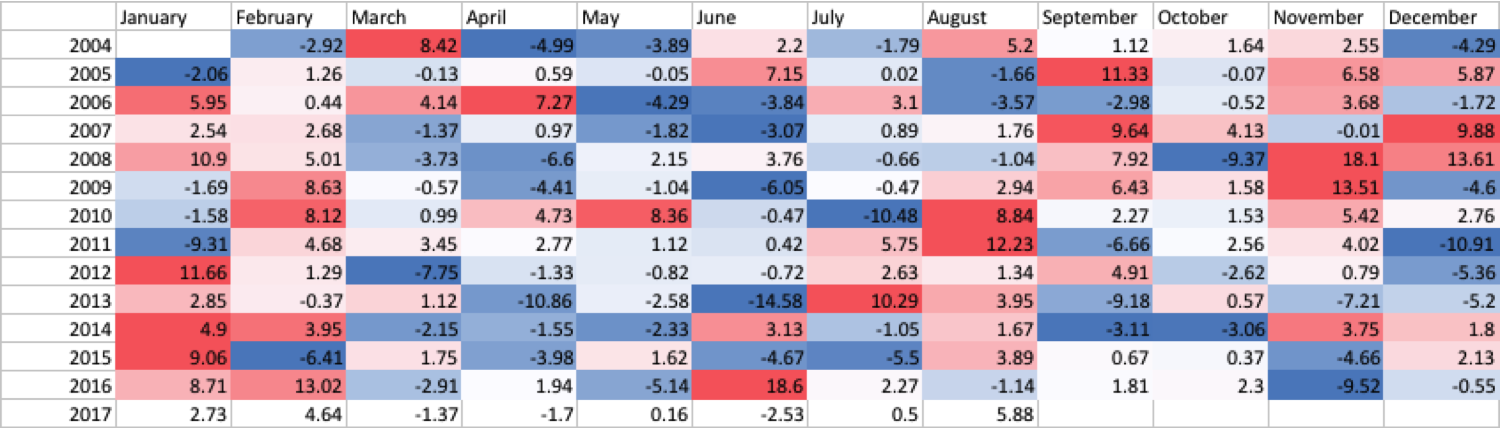

If we delve a bit deeper into the numbers the first table below (click to enlarge) shows the percentage performance of gold for each of the months analysed. In addition each year (with the the exception of 2017 as it is incomplete) has been colour coded on a scale from dark blue to dark red, in the same manner as the 80-20 Investor Heatmaps. Dark blue indicates the worst performance in the given year while dark red indicates the strongest month for gold returns in that calendar year.

If you glance along the row for each year you can quickly get a sense of the best and worst performing months. So for example in 2010 you can see that February, May and August were the best performing months of that year while July was the worst. If you almost unfocus your eyes as you look at the table you will notice that Q2 is disproportionately blue year on year. You will also notice that the autumn was historically the best time to invest in gold until around 2012. Since that time there has been a noticeable shift in the best returns being focused towards the new year. There are of course exceptions which I will come back to.

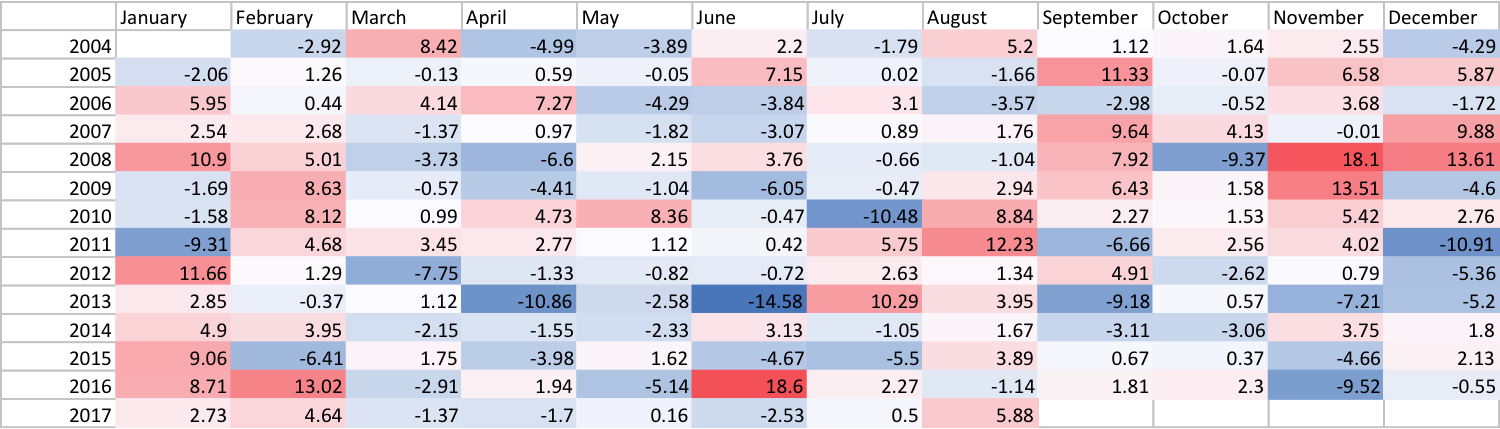

The next chart takes the same colour coding but instead applies it across all years. So in other words a dark red shows the best performing month in the entire period (January 2004 to date) while a dark blue shows the worst performing month. You can see how the incredibly strong new year performance over the last three years has helped bolster January’s overall average return shown in the first chart in this article.

This table above throws up some interesting insights into the behaviour of gold. First and foremost you can see it’s incredibly volatile with very strong months (in red) often followed by weak months (in blue) and vice versa. If you focus on the two strongest months for gold they were November 2008 and June 2016. The former was the aftermath of the financial crisis while the latter was a result of the fear over the outcome of the Brexit vote. For both of these months fear was the main driver of returns.

By contrast the worst month was June 2013, when the US Federal Reserve surprised markets and first suggested it was considering tapering its Quantitative Easing (QE or money printing) programme. This became known as the infamous taper-tantrum and it drove markets into a frenzy. With money printing ending the value of the dollar jumped which caused the price of gold to fall. The price of gold moves inversely to the value of the dollar. So good news (that the worst of the financial crisis was over) was bad news for gold.

There are interesting parallels to today. The US/ North Korea angst and the fear of a nuclear war (bad news) saw the price of gold jump in August this year (up over 5%). The tumbling dollar has also buoyed the price of gold as the market continues to discount the likelihood that the US Federal Reserve will raise interest rates quickly. As a side note, if the US Federal Reserve was to surprise markets in the coming months and suddenly hike rates (or use more aggressive rhetoric) then based on the experience of 2013 gold is likely to take a hammering.

We've recently seen the key resistance levels breached which I identified in my aforementioned technical analysis piece. Throw into the mix the likely seasonality boost along with continued geopolitical angst then gold bugs can be forgiven for getting excited about the prospects for the metal over the short term. However, gold remains a volatile asset and as such the autumn ‘buy gold’ theme can quickly reverse as shown in September 2013. Getting caught on the wrong side of a change in sentiment can be painful. By way of example November 2016 was one of gold’s worst months even though it coincided with Donald Trump’s shock election victory. The initial fear at the prospect of Donald Trump entering the White House turned into euphoria and was a catalyst for the current leg of the equity rally. The unexpected turnaround caught many gold investors off guard and despite this summer’s rally they are still nursing losses of 4.28% as shown in the chart below. Holding gold in a market not gripped by fear is painful.

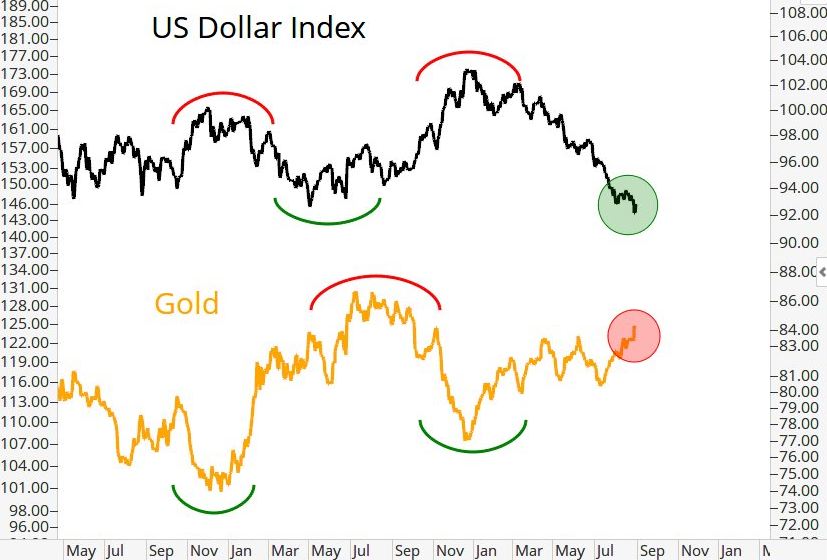

The biggest risks right now for gold enthusiasts are a drop in fear and the reversal of the most crowded FX trade right now, which is to short the dollar (i.e. everyone is betting the dollar will continue to fall). The chart below shows how closely linked the dollar and gold are and explains why investing in gold is often as volatile as investing in currencies.

Summary

History suggests that autumn and September is a typically good time to invest in gold due to seasonal demand for the precious metal as well as the increased equity market volatility we often see at the end of summer which benefits perceived haven assets, such as gold. However, the new year has recently been an even better time for gold investors. Yet it's fear and dollar weakness that are even bigger drivers of gold returns which can overpower even the strongest of seasonal trends. Gold investors will be hoping for increased geopolitical tensions in order for gold to break higher. Any hint of a delay is US rate hikes, or the tapering of QE in Europe, which are all bad for the dollar will be good news for gold. If these stars align then gold returns will gain momentum. If investors want to speculate on the outlook of gold then they should read my article Should you ever invest in gold? If so how much?

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay