When a fund house launches a new fund it needs to attract as much money as possible from investors in order to make it successful and profitable. One way to do this is to strike a deal with a leading fund platform which results in your fund being promoted favourably by them. While the fund houses and investment platforms will deny these kinds of deals take place anyone with a cynical eye will conclude otherwise. Alternatively, a fund house can poach a star fund manager from another fund house in the hope that loyal investors will follow him/her across to the new fund. But what constitutes a star fund manager? Fund managers that outperform their peers will inevitably come to the attention of the industry press and investors through aggressive marketing by fund houses. It means that some fund managers do attain cult-like status among financial advisers and armchair investors. These are the so-called star managers who many investors follow blindly from one fund to the next.

My previous research piece 'Is fund manager performance purely down to luck?' drew some interesting conclusions. These included that:

- 90% of funds don't show any level of consistency in returns

- those that outperform normally have a strong conviction (or narrow investment mandate) which whether by luck or judgement the prevailing investment conditions favour

- you shouldn't place too much weight on fund manager tenure (how long a fund manager has managed a fund) as an indicator of a fund's propensity to outperform in the future

However, the last point I want to explore further. My previous research showed that the length of time a fund manager managed a fund was not a direct indicator of likely outperformance. In fact, some of the best performing funds had changed their managers during the period of time I analysed. But this research looked at fund managers generally. But what about if we focus just on the superstars of the fund management world? If they were to leave and set up their own fund or were poached by a rival then should you follow them? Are the true fund superstars worthy of investors' blind loyalty which they court?

Should you follow star fund managers - methodology

The initial tricky part of this research piece was determining what constitutes a star fund manager. Often such descriptions are subjective, so I looked for an objective way of assessing star quality. I could have based it upon the amount of assets in a manager's fund, on the premise that successful managers attract more client money, but in the instance where a star fund manager has left a fund their predecessor could inadvertently be classed as the star manager based on client inertia (i.e the old fund still has a lot of money in it because investors haven't moved).

In the end I opted to use Trustnet's FE Alpha Manager Rating as a starting point. To quote from their website

FE Alpha Manager Ratings, rate the performance of a fund manager over their career including all funds they have managed and places worked. They are designed to distinguish fund managers who have consistently performed well over the longer term.

The rating is also given a boost if a manager has been managing money for over four years (irrespective of the fund or fund house he/she worked for during that period). As imperfect as fund manager ratings may be (based on my previous findings) this is as good a starting point as any to find the so-called stars of the fund management world. By screening the 2000+ unit trusts out there and only picking those funds with an FE Alpha fund manager rating I was able to whittle the potential list down to 238 funds. That is a lot of supposed star fund managers! It's lucky this isn't the Oscars otherwise the acceptance speeches would drag on for eternity.

I then looked at those fund managers with a career tenure of at least 4 years in line with Trustnet's assumption that the best managers have at least a 4 year record . Why they chose four years is not clear but it does provide a sufficient time frame for me to judge a manager's performance after they have left their original fund house. That left me with 187 funds with potential star managers.

Next, I looked at the career history of every manager to see which funds they had managed and when, in order to see if they had left a fund house to join a competitor. As you can appreciate this took an incredibly long time (two days in fact) as it is a manual process. Only the managers who either left to manage a fund within the same sector (or investment remit) were included in my shortlist to ensure I was comparing apples with apples. There are a number of examples of fund managers changing jobs to manage funds operating within different investment remits to what they had done previously. Also, the previous fund had to still be in existence because there are occasions when a star manager has left a fund house causing the old fund to close. The reason that the old fund had to be in existence is that I needed to compare its performance after the star manager's departure to that of the star manager's new fund.

This left me with just 15 star managers who run a staggering £58 billion between them. Or just under £4 billion each on average which is an incredible sum and their marketing teams would no doubt argue it is a sign of their star quality. I then analysed the performance of the star manager's new fund versus the performance of their old fund which is displayed in the table in the next section.

Star managers - it's down to luck

The table below shows the star manager in the first column followed by the name of the old fund which they used to manage, then the new fund they now manage and the date they took the reigns. The second-to-last column shows how much the star manager has outperformed their previous fund since they started running the new fund. If the square is green it shows that you would have been better off following the star manager when they left for pastures new. If it is red you will have been better off staying invested in the old fund when the star manager left. The final column shows how the new star manager performed against his/her peers from the same sector over the same period. If this column is green the manager has outperformed the average of his/her peer group with their new fund, while a red square shows that the fund manager has underperformed his/her peers. Click to enlarge the chart.

One of the great things about carrying out research for 80-20 Investor is that I genuinely don't know what the outcome will be. I don't start with a preconceived idea or bias. I simply look at what the data tells me and identify any patterns.

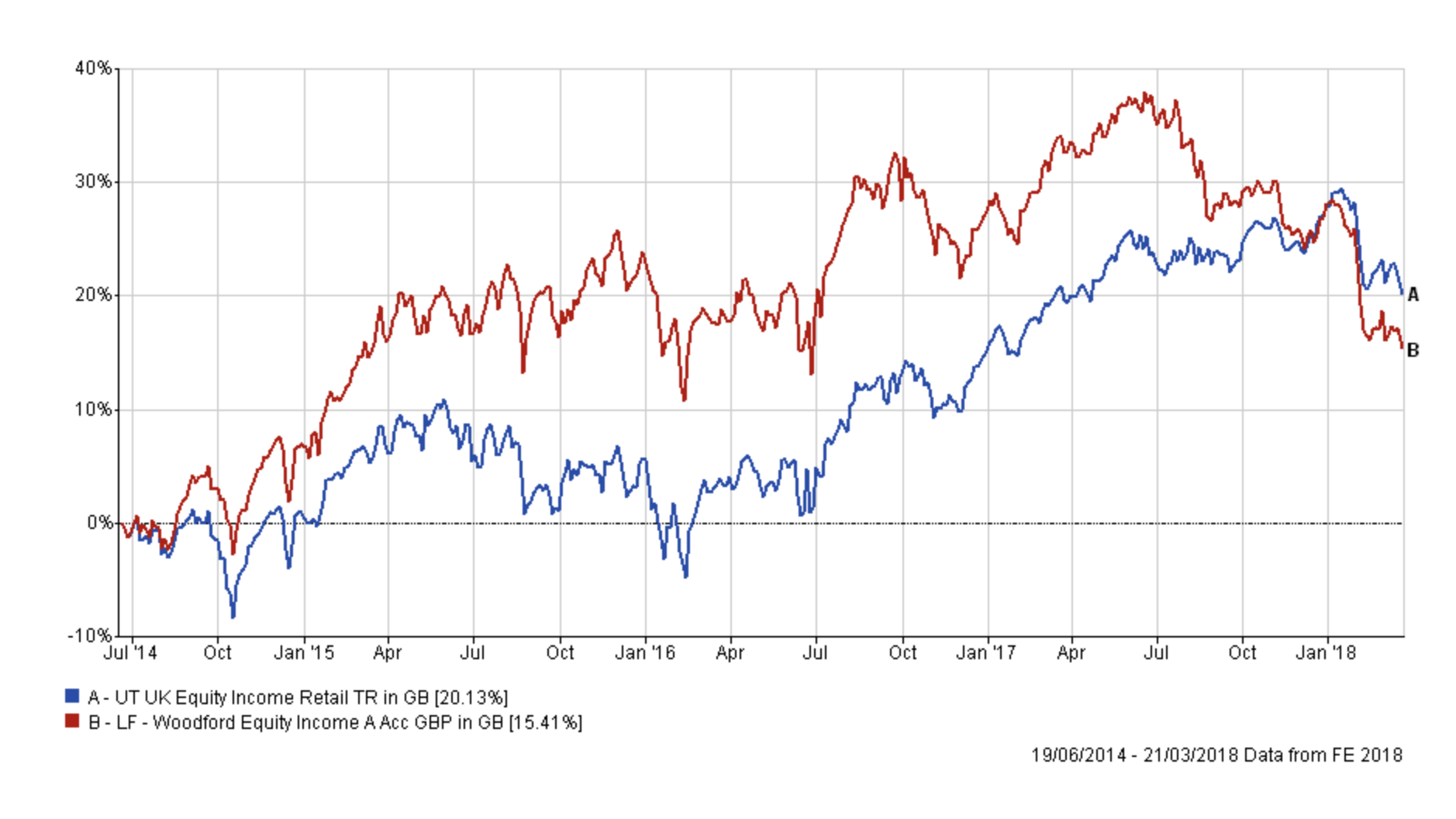

Now statistically speaking there is a 50/50 chance that a fund manager will outperform their old fund based on pure chance. Therefore if the 15 fund managers above are as good as investors have been led to believe (as demonstrated by the sums of money that they manage) you would expect most to have outperformed their old funds. Of the 15 star fund managers only 9 outperformed their old funds. However, two of the fund managers that did outperform their own fund significantly underperformed the average of their peers. Or in other words, they produced below average performance. One such manager is Neil Woodford, perhaps the most famous example of a 'star' manager with a cult following. Neil Woodford managed the Invesco Perpetual Income and Invesco Perpetual High Income funds for more than 25 years before leaving to set up his own funds. At the height of his popularity, he managed over £32 billion for Invesco Perpetual and his clients and legend has it that he sidestepped both the worst of the dotcom bubble and the financial crisis. In 2014 he left Invesco Perpetual to set up his own investment boutique and since then his fortunes have been mixed, to say the least. During the stock market rally of the last 12 months Neil Woodford's fund fell around 20%, So much so that his equity income fund is experiencing huge redemptions from institutional investors and disillusioned armchair investors who bought into the hype at the launch of Woodford's new venture. The chart below (click to enlarge) shows how his flagship equity income fund has performed versus the average of his peers since he launched it in 2014. Certainly, his star has lost its shine.

Of the 15-star managers highlighted above investors would have been better off in 8 out of 15 occasions either sticking with the original fund or choosing an alternative altogether because the manager left one sinking ship for another (Woodford falls into this category). That is not the sort of result you'd expect if following a star manager actually paid off at all. Of course, you have to accept that the ultimate sample size was small but even so there is no sign that following a star manager is justified. Neither is it conclusive that also sticking with the old fund is the best course of action. But placing blind faith in a star manager is clearly not justified.

So why doesn't following star managers work? Part of the reason is likely to be down to how fund houses run funds. Typically a fund manager will build a team of analysts behind him/her. As such the days of managers making autonomous decisions by the seat of their pants have gone. It follows then that should the fund manager leave the processes and investment remit/ethos has already been established and embedded in the team they leave behind. I've personally been in meetings with fund managers where I've been introduced to an analyst, by the fund manager, who then leads the presentation. It's an exercise in succession planning as usually that very same analyst eventually takes over the running of the fund while the original fund manager launches a new fund (normally with the same fund house). Also don't forget it is in the investment house's interest that investors buy into their brand as much as the fund manager, just in case he/she leaves. So ensuring that the investment process is carried out by a team, rather than just an individual, makes sense.

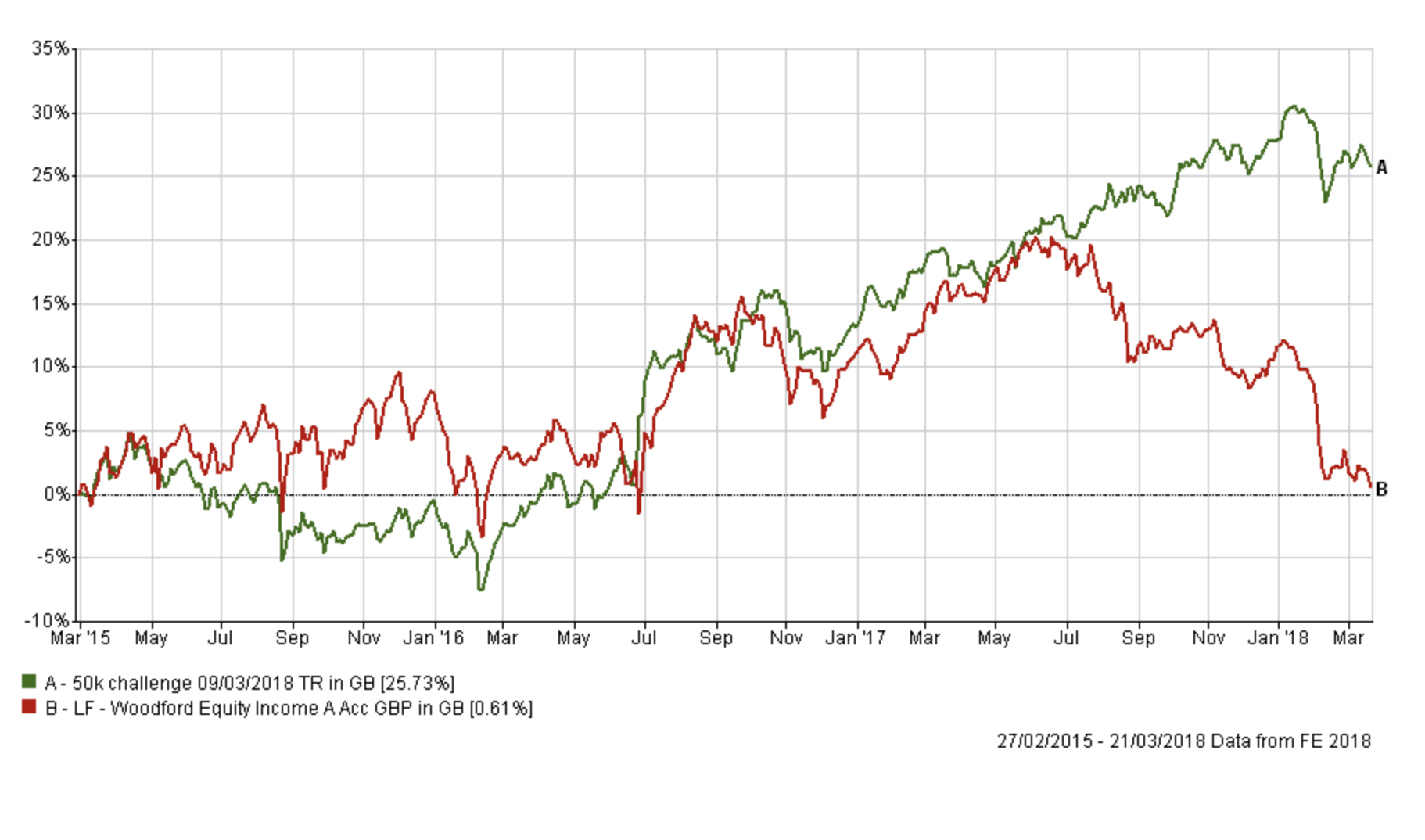

In my previous research piece on investment management luck/skill one of the factors that influenced the apparent luck/skill was the investment bias of the fund. So typically funds (or indeed managers) that had outperformed had a style bias (usually towards smaller companies) that the prevailing investment environment favoured. Indeed this is one of the reasons why Woodford has underperformed. Historically he has favoured defensive sectors that pay reliable dividends, the very sectors that have been left behind in the equity rally of the last few years. Of course, he has made some poor investment decisions over the last 12 months which the press have enjoyed highlighting but fundamentally the current environment doesn't favour his investment style. That will no doubt change at some point as every dog has its day. Yet there is no reason why investors should wait for that day. If Neil Woodford turns things around then it is likely that the 80-20 Investor algorithm will pick this up, but I'd rather invest in funds that have more chance of outperforming in the current environment. The chart below shows my £50k performance (which is usually only 60% invested in equities) versus Woodford's fund which is 100% invested in equities (so should outperform as he's taking more risk). Be quite clear, I am not a star manager, I simply follow a process to choose those funds (whether active or passive) that are working in the current environment.

Another observation is that star managers will often take their investment ethos/bias, which they will have embedded in their old fund, with them to their new fund. This explains why in the table earlier that when star managers do outperform their old fund it is often only marginally. It also helps explains why when a manager's investment style underperforms that of their peers, the chances are both their old and new fund lag their peers' performance.

Ultimately for investors loyalty doesn't pay, it only pays for the extravagant salaries of the fund manager and his colleagues. I've still yet to see any evidence to suggest otherwise.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay