Thursday 18th June is a crucial date in the ongoing talks between Greece and its creditors, who happen to be the International Monetary Fund (IMF), the European Central Bank (ECB), the European Financial Stability Facility (EFSF) and anyone who holds Greek Government bonds.

The IMF, the ECB and the EU first bailed out Greece in 2010 and Greece has been having to repay the debt ever since. It is an incredibly complex situation that few people truly understand.

To use an analogy, imagine if Greece was a person who couldn't get finance or loans from the mainstream creditors. It was therefore forced to go to payday lenders and loan sharks as a last resort. In the case of Greece these were the aforementioned institutions. These three institutions are collectively referred to as the Troika (which is derived from the Russian word for a group of three which strangely adds to the gangster feel of the whole thing).

Unsurprisingly the Troika periodically send the heavies (inspectors) in to Greece to make sure that they are keeping up their end of the bargain (financial reforms etc) to make sure they would get their money. All the while the Troika also release new funds (in tranches) as part of the original loan agreement.

Greece's debt pile

So how much does Greece owe? Something like €245 billion and the repayments are now crippling the country. If you look at 2015 alone Greece has repaid around €17 billion but still has to repay more than 20 billion before the end of the year.

Like anyone in debt Greece is having to 'rob Peter to pay Paul'. Some of the money received in each tranche of the loan goes on interest payments on the loans that are already owed to the Troika. Bonkers I know! Each tranche of money delays the day of Greek bankruptcy and means that public sector workers might get paid. The government is raiding every stash of cash to keep it's head above water. It is even demanding that hospitals hand over cash on account while there are reports of the Greek fire service having to go door-to-door with cap in hand.

When each new tranche of bailout money is due to be paid to Greece, the heavies put the frighteners on them and Greece tries to squirm out of its commitments. Usually at the 11th hour both sides reach a compromise and the tranche is paid and Greece avoids bankruptcy for a while longer.

Crunch time - this time is different

In January 2015 a new Government was elected in Greece with an anti-austerity mandate. Since then the new Greek Government has been pushing back against any reforms agreed by the previous Government as part of the original bailout.

So we now find ourselves at a point where Greece has taken it upon itself to delay the four regular payments owed to the IMF, due in June, until the end of the month. That means it has until the 30th June to find €1.5billion. Yet it also needs to find €2.2 billion to pay pensions, social security benefits, public sector salaries as well as keep public services going.

Meanwhile Greece needs a final €7.2 billion payment from the agreed bailout package which is also now due. But obviously tell a loan shark you are not going to pay him but I need to borrow even more money and you can imagine what happened. Rather than kneecaps being broken, in the world of politics the Troika walked away from the negotiating table and both sides seem further apart than ever before.

So metaphorically Greece is threatening to jump off the precipice (default on its debts) and the Troika are nervously watching on while the rest of the world (even Obama) are shouting from the sidelines 'come on Greece stop being so stupid and get down form there!'

So is Greece about to exit the euro?

If I was a betting man and wanted to put money on the possibility of Greece exiting the Euro then I couldn't, as William Hill actually stopped taking bets on that outcome a while ago. Of course a bookmaker's odds only reflect punters' opinions of what is likely to happen rather than reality itself. Yet it gives a good sense of that things are looking ominous.

On Thursday 18th June 2015 there is a Eurogroup meeting which is one of the last realistic chances of a deal being reached between Greece and its creditors. In the absence of an agreement being reached then there would need to be some form of emergency summit to thrash out a deal before the end of the month. Even if there was it might be tough for the various European Parliaments to put the necessary legislation in place by the end of the month.

So if an agreement isn't reached then in theory Greece would have to default on its repayments to the IMF at the end of June. In reality it would have four weeks grace to find the money. But again other repayments come thick and fast. On 20th July it has to pay €2 billion to the ECB and if it ends up defaulting on that as well then the problems really start because the ECB is currently propping up Greek banks. Upset the ECB and they might stop propping up the Greek banks altogether.

If that happened then people would withdraw their money from Greeks banks in panic (over €30bn has already been withdrawn in the 6 months to April). Capital controls would probably be enforced (i.e stopping people withdrawing money) which never ends well and Greece would likely be forced to leave the Euro and ultimately the eurozone

Is a Greek exit likely? Never underestimate the capacity for politicians to fudge something together. Interestingly the Financial Times recently reported that a third of institutional investors (investment banks and the like) think a Greek exit will happen..... but by the end of May 2016. So they are clearly not panicked just yet.

What should investors do?

You'd think that the market would have already priced in the possibility of a Greek exit, after all the Greece saga has been like a slow-motion car crash. Markets have fallen since their highs back in April and in fact Germany's Dax is officially in correction territory having fallen by more than 10%.

However, research by Bank of America Merrill Lynch found that fund managers are unprepared for a Greek exit from the euro. In fact 43% still expect a deal to be done at the 11th hour while 42% think that Greece will default on its debts but won't exit the eurozone.

Or in other words don't expect a fund manager to protect your money in the event of Greek exit. If you are worried about the impact of a potential Greek exit on your portfolio then the only safe place to be is in cash (but clearly not in a Greek bank).

But what could happen if Greek did default and exited the eurozone? Truth is that we don't actually know. The world won't implode that is for sure nor will it stop spinning. The poor people of Greece will of course have a tough time with the likelihood that salaries and pensions would go unpaid. A new currency would likely be needed which would cause rampant inflation (rising prices) and a deep recession.

As for investment markets if Greece defaults on its debts (loans and bonds) then anyone holding Greek bonds would be hit. That would include banks right across Europe. While the banking system is supposedly in better shape than when Lehman Brothers collapsed in 2008. Imagine a giant Jenga puzzle where you had to remove a bunch of blocks without the whole thing falling down. That is what a Greek exit looks like.

It is hard to say what would happen for every type of asset. Certainly you'd expect equity markets, particularly in Europe, to fall heavily as well as bond markets. Bonds and Government debt in peripheral countries in the eurozone would be particularly hard hit because of the fear of contagion and defaults by these countries

What might do well in a Greek exit inspired market wobble? In a market in risk aversion mode then investors tend to revert to basics and head for perceived safe assets. The main candidate would be the dollar especially if the US Federal Reserve make even more noises about raising interest rates over there. The Yen is another potential safe haven.

Funds for a Greek exit

While the safest thing to do is hold cash perhaps an alternative would be to consider The funds to buy for the bond market tantrum. Yet the recent bond market tantrum wasn't just about Greece. It was mostly about investors suddenly believing that inflation and higher interest rates were more likely in the future which was bad for bonds.

So are there any funds that seem particularly prepared for a Greek exit, or at least better placed than their peers to navigate one. How might you even find them given that we've never experienced a Greek exit before?

What I want to do is share with you how I went about answering that question. One of the benefits of being an 80-20 Investor member is that I teach you the process to go about answering these sorts of questions.

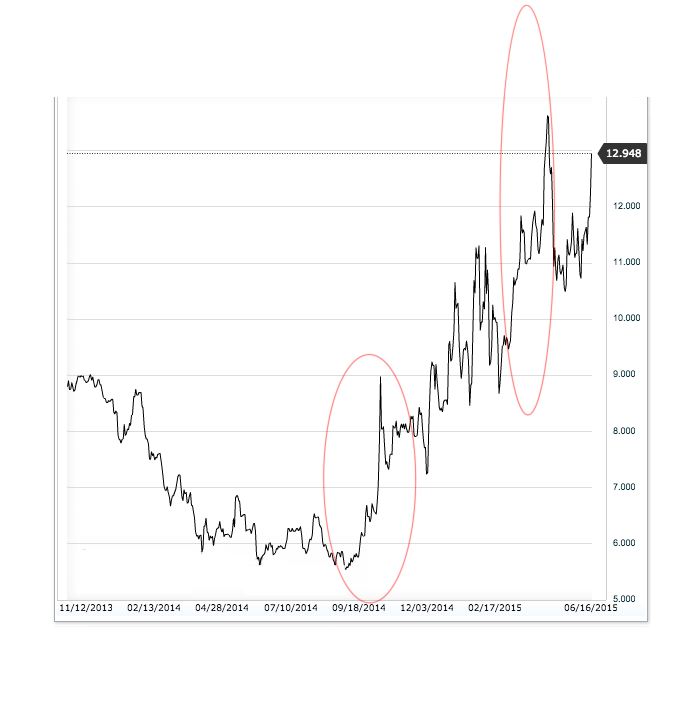

So first thing is to have a look at the chart below (click to enlarge). This is a chart of the yield on a 10 year Greek Government bond since November 2014. Or in other words it shows the interest rate investors would charge to lend money to the Greek Government, on a given day, for the following 10 years. If something spooks the market naturally the interest rate you would need to offset the risk of lending money to Greece for 10 years would go up (after all you might not get their money back). You can see this by the line jumping. I have circled two key points when the yield jumped hugely which were sparked by Greece either being difficult in talks with its creditors or concerns that Greece might simply default.

So these two periods are of interest to us. While we don't know what will happen in a full blown Greek default it is likely to reflect what occurs when the market 'thinks' there is about to be a default.

Yet a Greek default is such a macro theme (a big theme) that it moves the whole market. So what you really want is a fund that when the market moves it doesn't automatically follow. Most funds do but there is a useful statistic, called Beta, that you can use to find those that don't.

Beta is a measure of the sensitivity of a fund to general market movements. The market has a beta of 1 by definition. If a fund has a beta of 1.5 then that means that the fund’s return moves in the direction of the general market but to a larger degree. So if the market goes up by 2% the fund will go up by 3%. Conversely if the market falls 2% then the fund will fall 3%. Clearly, an index tracker fund should have a beta of 1. Yet a fund can have a negative beta figure. If a fund has a negative beta then it indicates that as the market falls the fund tends to rise.

Now during the first highlighted period equity markets sold off strongly while during the second period they didn't. This suggests that markets, while aware of the Greece issue, were not overly concerned in the latter period, which backs up the aforementioned research by Bank of America Merrill Lynch. So if we simply focussed just on the funds that performed well in this second period we might just end up with those funds that are the most complacent - which is not what we want. So that is why I screened every unit trust/OEIC out there (around 3,000 of them) and compared them against their peers. I was looking for:

- those funds with a beta of less than 0.7 (which is low) during the first period

- those funds with a beta of less than 0.7 during the second period

This left me with the funds where the returns don't simply follow the market macro themes.

- I then looked for those funds in this subset that made money in the first period (Autumn period 2014) when the market reacted violently.

This left exactly 20 funds which are listed below. These funds returns are less in line with the fortunes of their peers. When the markets sold off these funds made money. When the market appeared complacent these funds steered their own course.

Interestingly a number of property funds that invest in actual buildings (rather than shares) make an appearance again. Yet there are also a couple of Global Bond funds in there. You will also notice that there are a few short-dated UK bond funds. These funds buy bonds which are about to mature which means that they aren't as affected by bond market swings because the fund manager will be getting his/her money back in due course when the bonds mature.

So it would seem to be that message is that if there is a Greek exit then those things most likely to weather the storm are:

- short dated bonds (i.e those which are just about to mature)

- the best quality bonds (from companies and countries unlikely to bust - i.e UK)

- bricks and mortar property funds

- funds that use hedging strategies to avoid such events (Insight Absolute Insight)

- and certainly not equities

Think of these like the life buoys you might cling to if/when the storm comes. Alternatively you can simply surf the waves up and down, as I plan to do with my own portfolio, using the 80-20 Investor algorithm. It might be unpleasant at times but ultimately you will be rewarded over the long term.

| Fund name | Sector | Beta 05/09/2014 to 16/10/2014 |

Beta 23/02/2015 to 20/04/2015 |

Performance 05/09/2014 to 16/10/2014 |

Performance 23/02/2015 to 20/04/2015 |

| FP - CAF Fixed Interest | Global Bonds | 0.24 | 0.3 | 0.12 | 1.42 |

| JPM - Global Ex UK Bond | Global Bonds | 0.27 | 0.52 | 0.82 | 1.63 |

| Aberdeen - Property Trust | Property | 0.41 | 0.14 | 0.19 | 1.28 |

| Aviva Inv - Property Trust | Property | 0.57 | 0.2 | 0.75 | 0.52 |

| F&C - UK Property | Property | 0.54 | -0.01 | 0.43 | 0.83 |

| Henderson - UK Property OEIC | Property | 0.44 | 0.1 | 0.6 | 1.24 |

| Ignis - UK Property | Property | 0.41 | -0.03 | 0.86 | 1.23 |

| M&G - Property Portfolio | Property | 0.66 | -0.01 | 1.19 | 1.12 |

| Standard Life Investments - UK Property | Property | 0.33 | 0 | 0.64 | 1.08 |

| Threadneedle - UK Property | Property | -0.61 | -0.05 | 1.42 | 1.05 |

| SJP - Property | Property | 0.51 | -0.03 | 0.97 | 1.51 |

| FP - Brown Shipley Sterling Bond | Sterling Corporate Bond | 0.37 | -0.01 | 0.52 | 1.21 |

| AXA - Sterling Credit Short Duration Bond | Sterling Corporate Bond | 0.37 | 0.12 | 0.55 | 0.27 |

| Invesco Perpetual - Corporate Bond | Sterling Corporate Bond | 0.28 | 0.41 | 0.12 | 1.04 |

| M&G - Short Dated Corporate Bond | Sterling Corporate Bond | 0.63 | -0.03 | 0.08 | 0.06 |

| AXA - Framlington Managed Income | Sterling Strategic Bond | -1.34 | 0.41 | 0.25 | 1.39 |

| Scottish Widows - Strategic Income | Sterling Strategic Bond | -1.29 | 0.61 | 1.74 | 1.14 |

| Insight - Absolute Insight | Targeted Absolute Return | 0.49 | 0.69 | 0.07 | 0.49 |

| Aberdeen - Defensive Gilt | UK Gilts | 0.21 | 0.15 | 0.61 | 0.43 |

| SJP - Index Linked Gilts | UK Index - Linked Gilts | 0.65 | 0.21 | 0.51 | 1.07 |

Photo by Sailom - via freedigitalphotos.net

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay