Even if you don't buy explicit bond funds the chances are that some of your low risk funds do buy bonds. But even then, when the lowest part of investors' portfolios is losing money they tend to run for the hills which in turn is bad for share prices. So is there nothing investors can do to protect their money other than sell up? Well there are actually a few funds out there that have a history of doing well in a bond market sell-off.

Quick guide to how the bond market works

But first let me give you a bit of background of how bonds work so you can understand what has been happening. A bond is essentially a loan to a company made by an investor. The investor lends the company a lump sum in return for a regular interest rate payment plus the return of their capital at the end of the agreed loan term. So let's keep it simple by using small numbers. Lets say I agreed to lend the company £100 for 10 years if they paid me a 4% interest rate payment (called a coupon) each year and then returned my initial £100 at the end. Simple enough!

But now lets say that I wanted my money back. One way to do this would be to sell the loan (or bond) on to someone else along with the entitlement to all future payments. So lets say I decided to sell the bond on to someone else 3 years into the loan. So the new person will get 6 more annual interest payments plus the £100 back after 10 years. The trouble is that market conditions have changed and the company the money was lent to is not doing so well. The person buying the loan thinks it's a risky investment and so rather than give me my £100 back he gives me £95. In his eyes he is lending £95 and will receive interest payments of £4 a year still and then get £100 at the end.

Now when people talk about bond yields they are simply talking about the present value of all future income payments as a percentage of what they paid for the bond. In the above example you can see that the chap I sold the bond to is getting a better yield than I did as the price he paid, for the same amount of income I got, was lower. If everyone wanted my bond then I'd probably sell it for £104 and the new buyer would have a lower yield than I had. Bond fund managers are simply doing this on a daily basis with lots of different bonds and companies - so a bond fund is just a collection of bonds which helps spread risk.

So as bond yields increase the bond price falls and vice versa

Think of it like buying a buy-to-let property, the rent you get is dictated by the house and not the price you paid. Yield is simply the rent you receive as a proportion of the price you paid. That's why landlords buy cheap houses and touch them up a bit - so that they can maximise their yields.

Now because the payments on bonds are usually fixed from outset (with an agreed coupon) as interest rates and inflation rise in the economy they become less attractive. Because unlike rent on a buy-to-let you can't increase the coupon on a bond. If the price of everything around you is rising (which is what inflation is) then the interest payments (coupons) from a bond are worth less in real terms.

So deflation (falling prices) is good for bonds - while inflation is poor for bonds and as such their prices fall

The recent bond market sell-off - which I predicted 3 days before

The above all helps to explain the recent bond market sell-off. The bond market has enjoyed a 30 year bull run where prices soared (meaning that yields fell - remember bond yields and prices move in opposite directions). More recently central banks like the European Central Bank (ECB) have been buying lots of bonds through their Quantitative Easing programme (QE or money printing). Buying lots of Government bonds is the mechanism which they print money - don't worry about the detail just accept that it is.

All of this money printing is being done to create inflation. Some inflation is good for economy - a bit like engine revs on a car. If the revs fall the car will likely stall. So too will an economy if prices keep falling (deflation) as people stop buying things because they will be cheaper tomorrow. The biggest fear globally is that deflation will set in and economic growth stall.

That's exactly what happened in Japan for much of the last two decades. It is a vicious circle that's hard to break. Would you buy a car today if the price is likely to fall tomorrow. If they keep falling when will you buy? The odds are you never will. Not buying things is bad for the economy.

Well the market consensus had been that deflation was waiting in the wings everywhere so buying bonds was the obvious thing to do. Besides the ECB was also buying lots of them so they had your back by driving up prices as well.

But at the end of April 2015 there was a wild switch in the market consensus. Suddenly oil prices were rising, as was the Euro. Everyone thought they'd actually underestimated the chances of inflation returning. As a result investors began changing their mind and thinking that inflation is now more likely than deflation - so they sold out of bonds. This caused a rapid rise in bond yields and a fall in prices as everyone headed for the exit. Think of that change in market sentiment like an earthquake. The market had been built upon an assumption that had suddenly started shaking and everything began crumbling down.

Back on 24th April I sent you all an email warning about the bond market and why it was likely to turn. Three days later it did exactly that! You can read it here.

But such a bond market earthquake has happened before and rather spookily almost 2 years previously to the day.

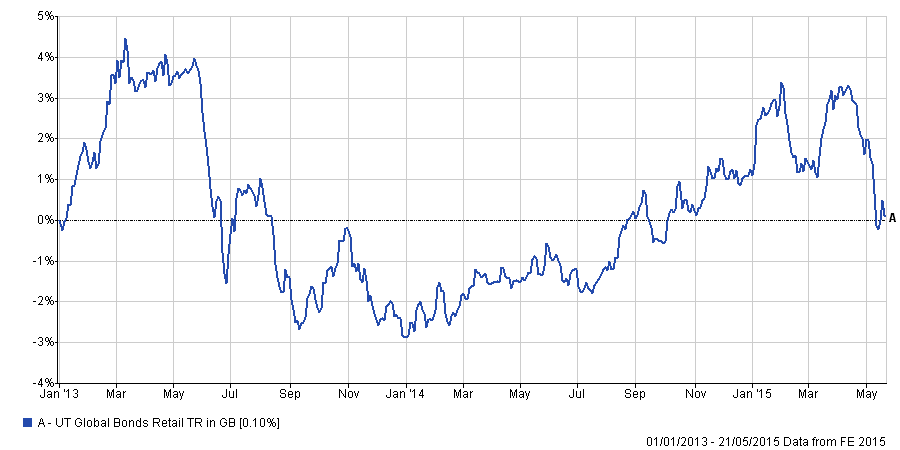

The taper tantrum of 2013

On 23rd May 2013 Ben Bernanke, the former chairman of the US Federal Reserve (the equivalent of our Bank of England) shocked markets by suggesting that they would soon stop ('taper' was the word he used) their own QE money printing programme. As I mentioned earlier, central banks buy bonds to give the effect of printing money. When the market realised that the biggest buyer in bond markets might exit there was a rout in bond markets as shown below. This has been immortalised as the infamous 'taper tantrum'. The market eventually recovered but the wobble transcended bond markets and wobbled equity markets - just like an earthquake. The same happened in this year's bond market sell-off. Let's call it 'taper tantrum II'.

Investment commentators speculating nonsense

At the time of writing taper tantrum II has quietened and markets have recovered slightly, in part thanks to the ECB announcing that it will work its printing presses harder in the coming months. But as can be seen from the taper tantrum chart above these things can have a habit of lulling us into a false sense of security before coming back for a second bite. There's been a lot of speculation and analysis over whether the bond bull market is finally over. I'm not going to go into this here but on balance most analysts think that the bond market sell-off should almost be done for now.

But the truth is that the bond market will likely collapse at some point but is there anywhere to invest other than just sitting in cash which will make money? What should you invest the lower risk section of your portfolio in, as after all even the cautiously run managed funds invest in bonds? When there is a bond market tantrum equities sell-off too. So to use an analogy, are there any funds out there that can withstand another bond earthquake?

The funds for a bond market tantrum

History won't predict the future but it does give you a good steer of what to expect. As I've said previously if you are trying to draw insights from historic data you need to dig deeper to find something useful that can be used in the near future.

So rather than just look at the recent taper tantrum, I decided to analyse the performance and behaviour of funds during the 2013 taper tantrum as well. I wanted to see if there were any low risk funds which had weathered both periods well.

In fact I started by screening every unit trust fund out there (around 3,000 of them) regardless of what they invest in, be it UK bonds or even European equities to find those that had produced a positive return during both bond market sell-offs.

What is interesting is that it confirms that certain property funds are great portfolio diversifiers. Yet it is only those that invest in actual buildings that appear, rather than the higher risk property funds which invest in property company shares. It's somewhat ironic given my analogy of looking for funds (buildings) that can withstand a bond earthquake that we end up with funds that invest in bricks and mortar.

Also a few Targeted Absolute Return funds have made the cut, a number of which invest in equities and occasionally short them (i.e they take positions to benefit from individual share price falls).

But most interesting of all is that Kames - UK Equity Absolute Return (indicated in red) makes an appearance. Back in December I wrote a piece on the Funds to ‘buy & forget’ in 2015 & the Perfect Portfolio in which I championed the fund. While the fund's returns since 2013 (up 7.27%) might not seem exciting, to put this into context this is higher than the average bond fund while the FTSE 100 fared not much better achieving 12.28% by comparison.

In the long run momentum and the 80-20 algorithm will see you through the choppy market waters over the long term but it's always worth knowing where the nearest port is in any storm.

| Fund name | Sector | Return during 2013 taper tantrum | Return during 2015 sell-off | Overall performance from start of 2013 tantrum |

| City Financial - Absolute Equity | Targeted Absolute Return | 1.09 | 5.37 | 50.22 |

| Schroder - Absolute UK Dynamic | Targeted Absolute Return | 1.19 | 2.66 | 7.66 |

| Schroder - UK Real Estate | Property | 0.53 | 0.83 | 34.19 |

| L&G - UK Property | Property | 0.38 | 0.66 | 25.31 |

| Threadneedle - UK Property | Property | 0.56 | 0.65 | 21.9 |

| M&G - Property Portfolio | Property | 0.51 | 0.55 | 22.15 |

| SJP - Property | Property | 0.64 | 0.43 | 23.11 |

| Ignis - UK Property | Property | 0.54 | 0.4 | 19.75 |

| Standard Life Investments - UK Property | Property | 0.28 | 0.31 | 22.37 |

| Kames - UK Equity Absolute Return | Targeted Absolute Return | 1.21 | 0.3 | 7.27 |

| F&C - UK Property | Property | 0.57 | 0.16 | 15.46 |

| BlackRock - European Absolute Alpha | Targeted Absolute Return | 1.05 | 0.08 | 6.81 |

Photo by David Castillo Dominici.

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay