This time last year I wrote a 2018 investment outlook which now makes for interesting reading. It is well worth revisiting the article with the benefit of hindsight and I am actually pleased with how accurate most of the outlook turned out to be.

The general theme of last year's forecast was whether 2018 could be as good as 2017 for DIY investors. The odds were always against a repeat performance for 2018 and as this year comes to a close nearly every stock market index around the world has closed firmly in the red. As we head into 2019 the question has now become whether the market can recover from the disappointments of 2018, or whether things are about to get a whole lot worse?

Despite 80-20 Investor being based upon data analysis and not crystal ball gazing it is still an interesting exercise to look at the consensus market view of what may happen in 2019, if only for curiosity. As I remind people each year, I don’t try and predict the future but the ‘smart money’ (i.e investment banks) do, partly because their clients ultimately pay them to do so.

This time last year investment banks including Morgan Stanley, JP Morgan and Goldman Sachs made predictions that we would end 2018 with the S&P 500 between 2,750 and 3,000. Given that the S&P 500 was sitting at 2,683 when they made those predictions, it was a pretty bullish forecast. It turns out that most investment banks were wide of the mark.

This time around the investment banks have not really learnt their lesson and remain pretty bullish about the prospects for 2019. The table below gives a summary of their latest market predictions.

Many of these were made when the S&P 500 was at 2760 at the start of December. Since then the S&P 500 has collapsed and at the time of writing sits at 2416. Unsurprisingly some investment banks have now rushed to amend their 2019 end of year predictions. For example, Credit Suisse, the most bullish institution on the list below cut its prediction to 2925 on the 18th December (when the S&P 500 was at 2545).

| Institution | Prediction of where S&P 500 ends 2019 |

| Morgan Stanley | 2750 |

| Bank of America | 2900 |

| Jeffries | 2900 |

| Goldman Sachs | 3000 |

| Barclays | 3000 |

| Citigroup | 3100 |

| JP Morgan | 3100 |

| BMO | 3150 |

| UBS | 3200 |

| Deutsche Bank | 3250 |

| Credit Suisse | 3350 |

However, as last year's predictions prove, investment banks are notoriously poor at predicting the future. What is probably more useful is to ponder what the key investment themes of 2019 may be.

Investment themes for 2019?

Slowing global growth

Strong coordinated global growth has been an underlying assumption for most investment strategies since global central banks eased monetary policy (by lowering interest rates and printing money) in the aftermath of the global financial crisis. During 2018 official data in the US had shown that economic growth was accelerating along with inflation. This story was replicated to a lesser extent in the UK and Europe. Chinese economic growth always remains an enigma as the authorities there pretty much make up whatever number they want. But nonetheless, the outlook was still positive. However in my recent note titled 'Growing Pains' I highlighted how bond markets have been letting off emergency flares, highlighting the possibility that global growth is now slowing. The problem is that most official economic data released globally is backward looking (i.e. looking at the economic indicators from previous quarters).

But as we moved into the third quarter of 2018 inflation showed signs of slowing, even if the US economy didn't. In the fourth quarter of 2018 (which is just coming to a close) unofficial and more contemporary data now suggests that economic growth is decelerating. This has also been seen globally, particularly in Europe and China. As we head into 2019 will this deceleration of global growth start to show up in official economic data, meaning that central banks will have to review their plans for tightening monetary policy? Worryingly those few models that predicted the economic slowdown in Q4 , which was one of the root causes of the latest stock market slump, are suggesting that economic growth will continue to slow into the third quarter of 2019. This also raises the prospect of a future recession.

Recession (and the Treasury yield curve)

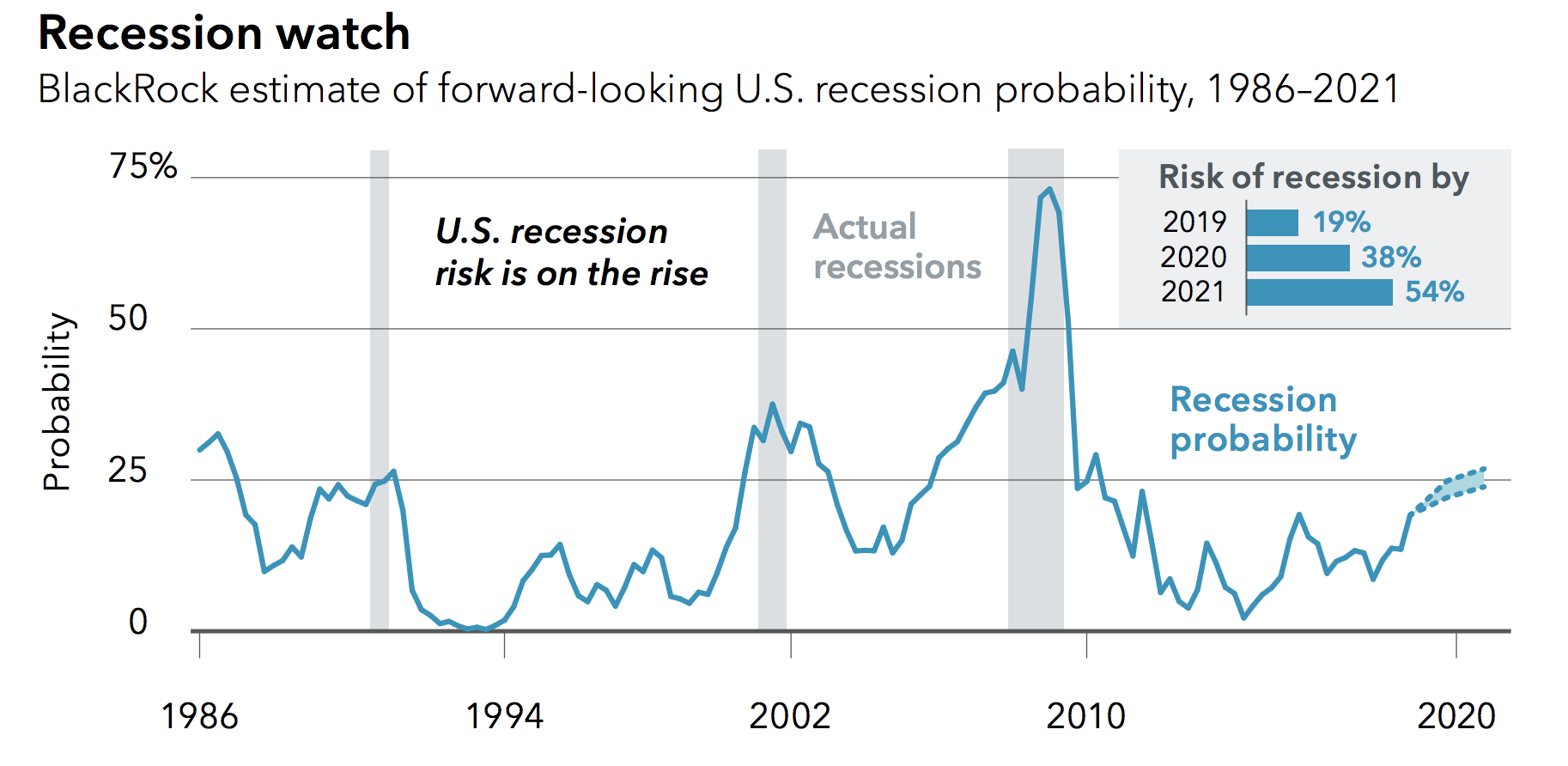

Only a few month ago talk of a possible recession would have had people laughing at you. However, the possibility of a recession has risen dramatically in recent months. The chart below, produced by Blackrock, shows the estimated probability of a recession in the US.

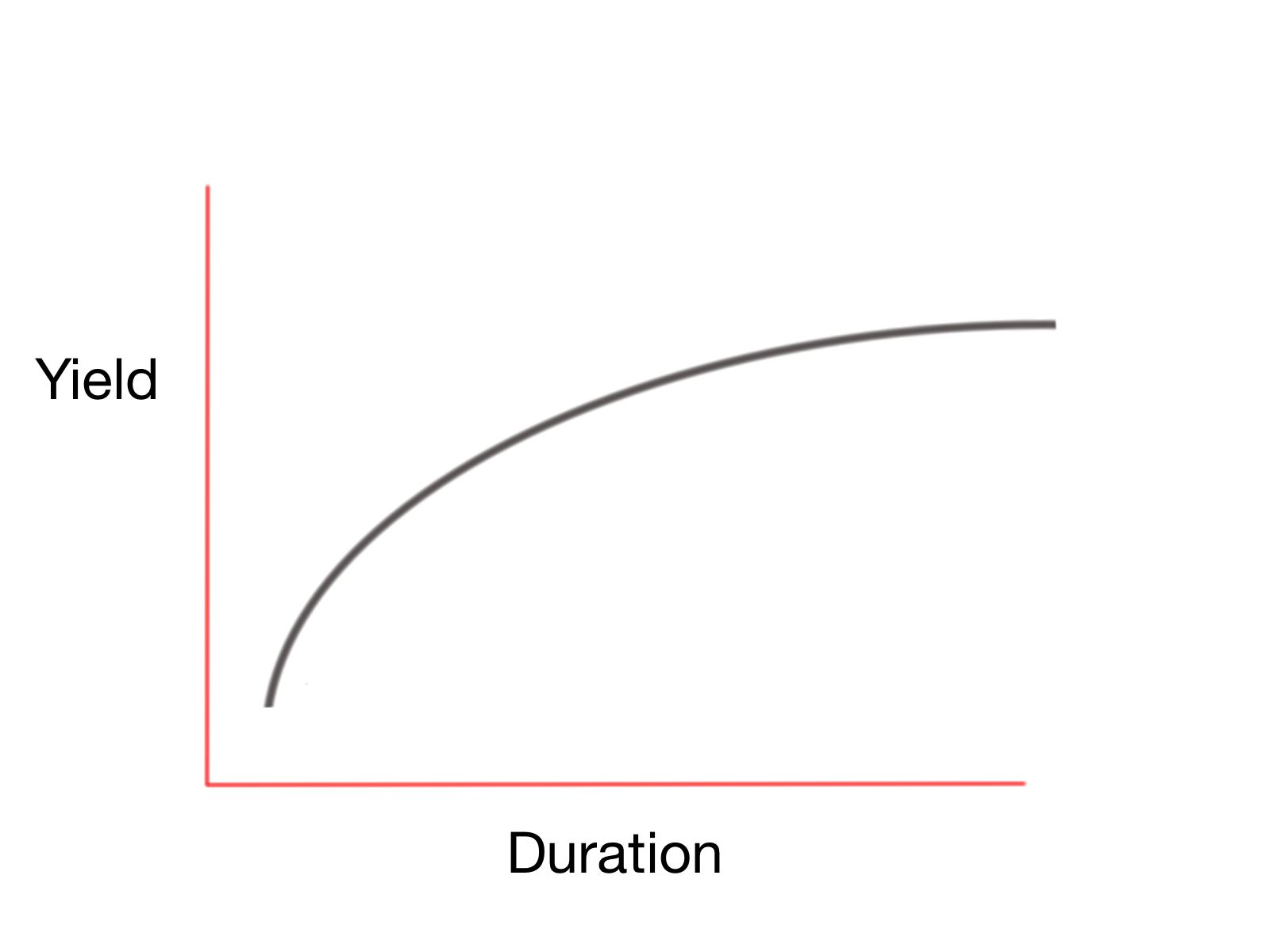

The odds have risen, in part, due to the flattening of the US Treasury Yield curve. A Treasury is a low-risk investment and is effectively a loan to the US Government. You are paid an agreed coupon (interest) on that loan until the agreed term comes to an end and you get your capital back. So a simple way of looking at the yield on a 10 year US Treasury is that it represents the interest rate you want in order to lend money to the US Government for 10 years. All being equal, the longer you lend your money to the US Government the higher the interest rate you would want, as there is an increased risk of default. If you plot the yields for each different term of US Treasury on a chart it would look something like this:

As the yield is a function of the price you pay for a US Treasury it means that supply and demand can influence the yield for a given duration. Because Treasuries and bonds give a fixed income stream they are popular when interest rates within the economy are low. This tends to be when the economy is struggling. The table below shows the current yield for US Treasuries of varying duration. The figures in red show how the 5, 3, 2 and 1-year yields do not get smaller as the term reduces as they should. This is described as the yield curve flattening and ultimately starting to invert. When the yield curve starts to invert (it can completely invert where longer-term yields are lower than short-term yields) it has tended to predict an impending recession.

| Duration | Yield% |

| 30 years | 2.973 |

| 10 years | 2.757 |

| 7 years | 2.689 |

| 5 years | 2.626 |

| 3 years | 2.628 |

| 2 years | 2.654 |

| 1 year | 2.632 |

| 3 months | 2.402 |

Of course, a recession would see economic growth contract in the US which usually also sends the global economy into recession. For investors that means that stocks can struggle and bonds tend to gain favour. Those stocks that do tend to outperform are those that provide goods and services that people buy irrespective of economic conditions, such as medicines, tobacco and food. On the flipside discretionary sectors such as clothing retailers perform badly.

Monetary policy

Leading on from economic growth, 2019 will prove a pivotal year for central banks. In the aftermath of the financial crisis, global central banks hit the panic button and slashed interest rates and launched QE (quantitative easing). As time passed the monetary policy outlook diverged across the globe with the US Federal Reserve tightening while other central banks continued to loosen their monetary policy. As we head into 2019 the European Central Bank has now ended its QE programme, choosing to follow the Federal Reserve's lead. Conversely, in China investors are hoping the authorities will add extra stimulus in 2019 to help lift its sagging economy and stock market.

The recent equity sell-off began after the Fed confirmed it planned to push ahead with raising interest rates and unwinding QE. But if economic conditions continue to deteriorate in the coming months then 2019 could be remembered as the year that the Fed caused the next bear market and/or financial crash by continuing to tighten. Alternatively, the Fed may be forced to change its stance in the face of hard data. Don't be surprised if the Fed turns more dovish in the first quarter of 2019 although it may prove too little too late to rescue the economy or the stock market.

There is also the possibility that inflation will pick up if the price of oil rises, possibly a result of geopolitical tensions, at the same time as central banks call a halt to any further policy tightening. This would cause a conundrum for central bankers. Do they raise rates to contain inflation but run the risk of causing economic growth to stall?

As I noted recently, the bull market in stocks over the last 9 years has ridden the wave of easy monetary policy from central banks (QE and low rates). Investors were happy with the Goldilocks scenario where economic growth was not too cold (slow) to cause a recession but not too hot to cause central banks to tighten monetary policy. But the bulls banking on economic growth continuing to follow the Goldilocks story should be mindful of how that story ends.... eventually Goldilocks gets eaten by a bear.

Bear market

2018 started with stock markets across the globe hitting new all-time highs as the 9 year bull market charged ever higher. Despite an equity market sell-off in the spring, equity markets seemed to regain their swagger. Certainly, this was true in the US where they set new all-time highs in September. While investors assumed the rest of the world would follow suit this never came to pass. In fact, Japanese, Chinese and European stocks merely stabilised momentarily in the summer before resuming their downtrend. If you define a bear market to be a 20%+ drop from a 52-week high then there are already bear markets all over the place, including in Germany. Those stock markets that aren't in bear market territory right now and are still down over 10% (including the US). Given the historical correlation between the German DAX and the S&P 500, which has recently become strained, 2019 could be the year when it snaps back into line finally pulling US stocks lower. Of course, as we enter 2019 things may get better for equities. However, the buy the dip strategy, that has been richly rewarded since the financial crisis, stopped working in 2018. Sell the rip (i.e. sell rallies) could continue to be successful in 2019 unless something changes. That something may have to be a new round of QE from central banks as the Powell Put has so far proved unsuccessful.

However, it is not just equities that have entered a bear market. So too has oil and some are predicting that the dollar could enter a bear market despite its rally in 2018. A weak dollar would prove a tailwind for certain asset types such as commodities and emerging markets assets.

Investing style shifts

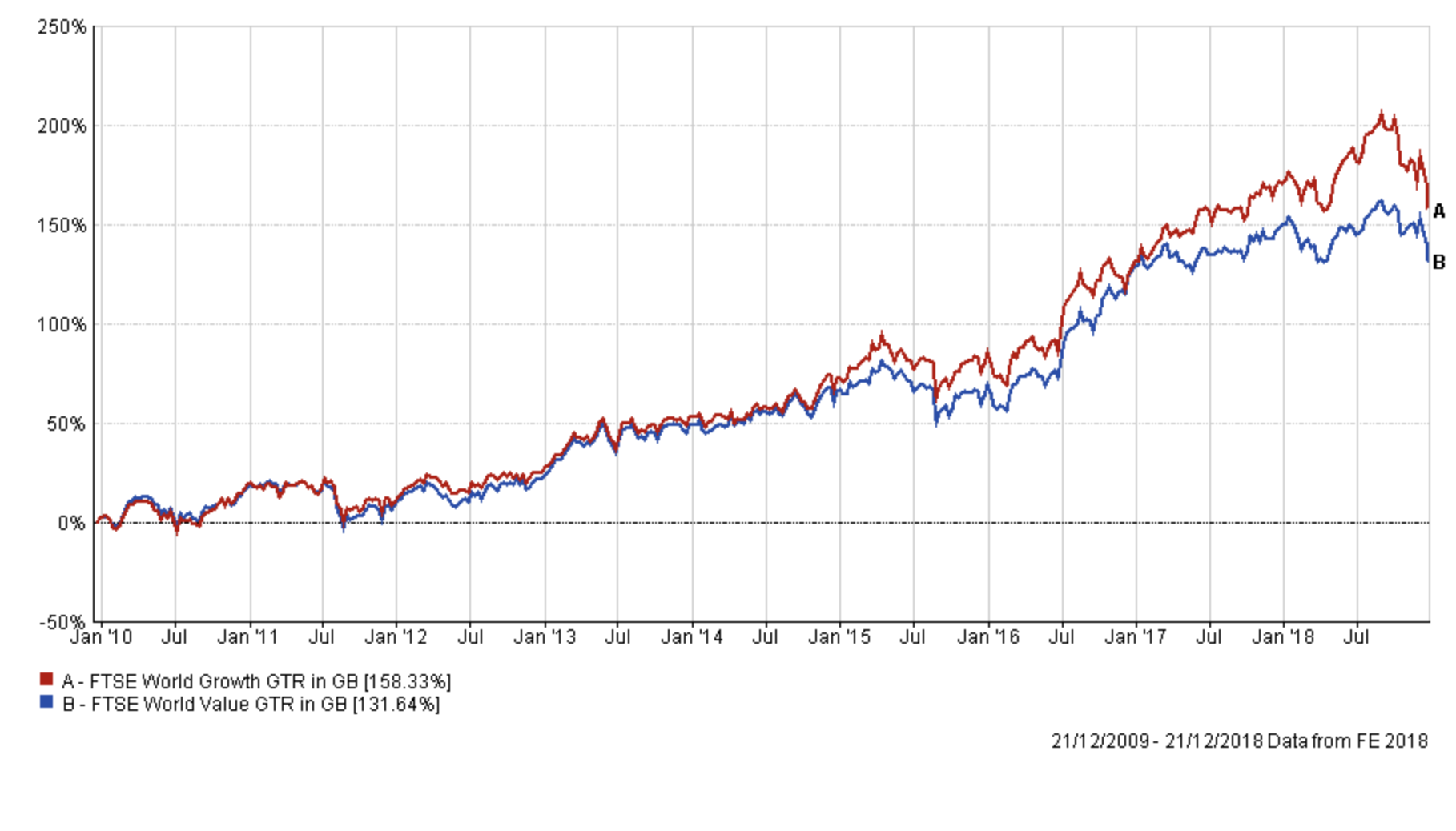

Growth stocks (such as tech) have long outperformed value stocks since the financial crisis, as shown in the chart below.

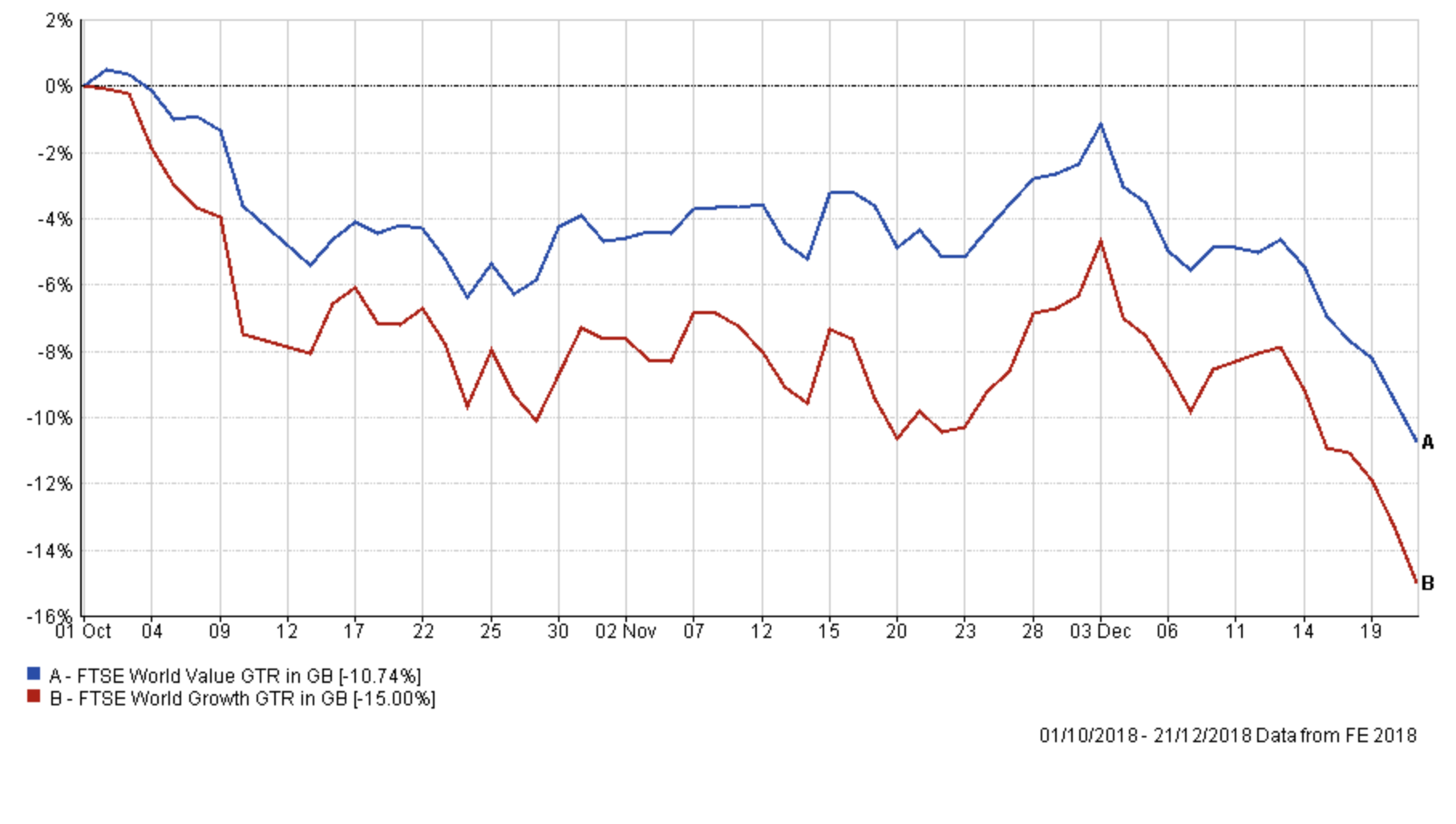

Growth stocks tend to do well in a low-interest rate environment. At the start of 2018 I wrote that "with equity valuations at high levels we shouldn't be surprised if investors finally start focusing on value at a sector level and a global level". Despite the equity market wobble in the spring growth stocks continued to outperform value stocks. The buy the dip investment approach was still working and it wasn't until October that it appeared to finally break. As the chart below shows growth stocks bore the brunt of the pain while value stocks performed better, relatively at least.

Investors are now wary of overpaying for stocks with lofty valuations and are finally looking more closely at value and fundamentals. If this trend continues into 2019 then it could finally be the year when value stocks champion over growth.

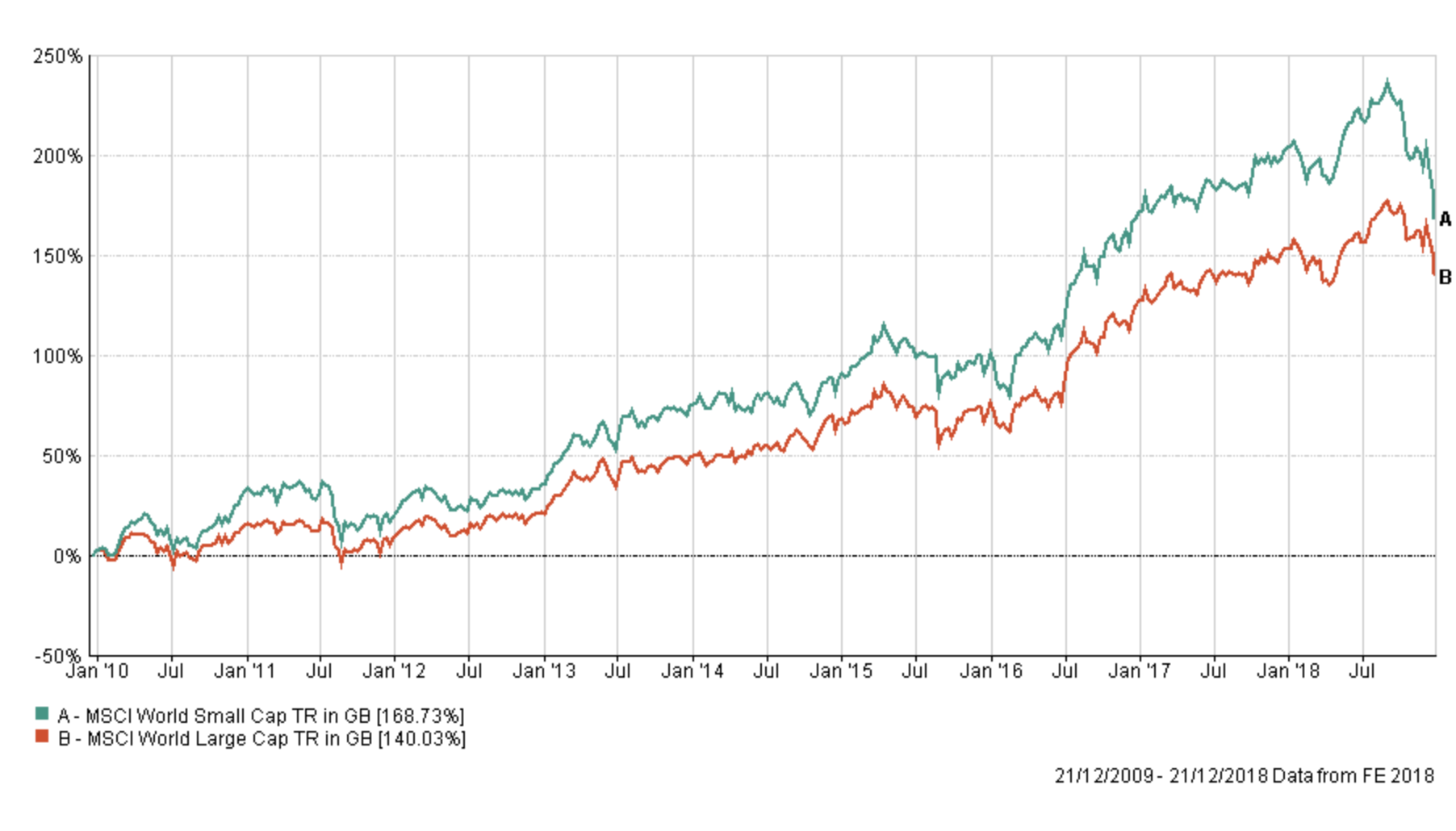

There has also been a shift in style bias in relation to market cap. Small caps have also long outperformed their large cap peers as shown below.

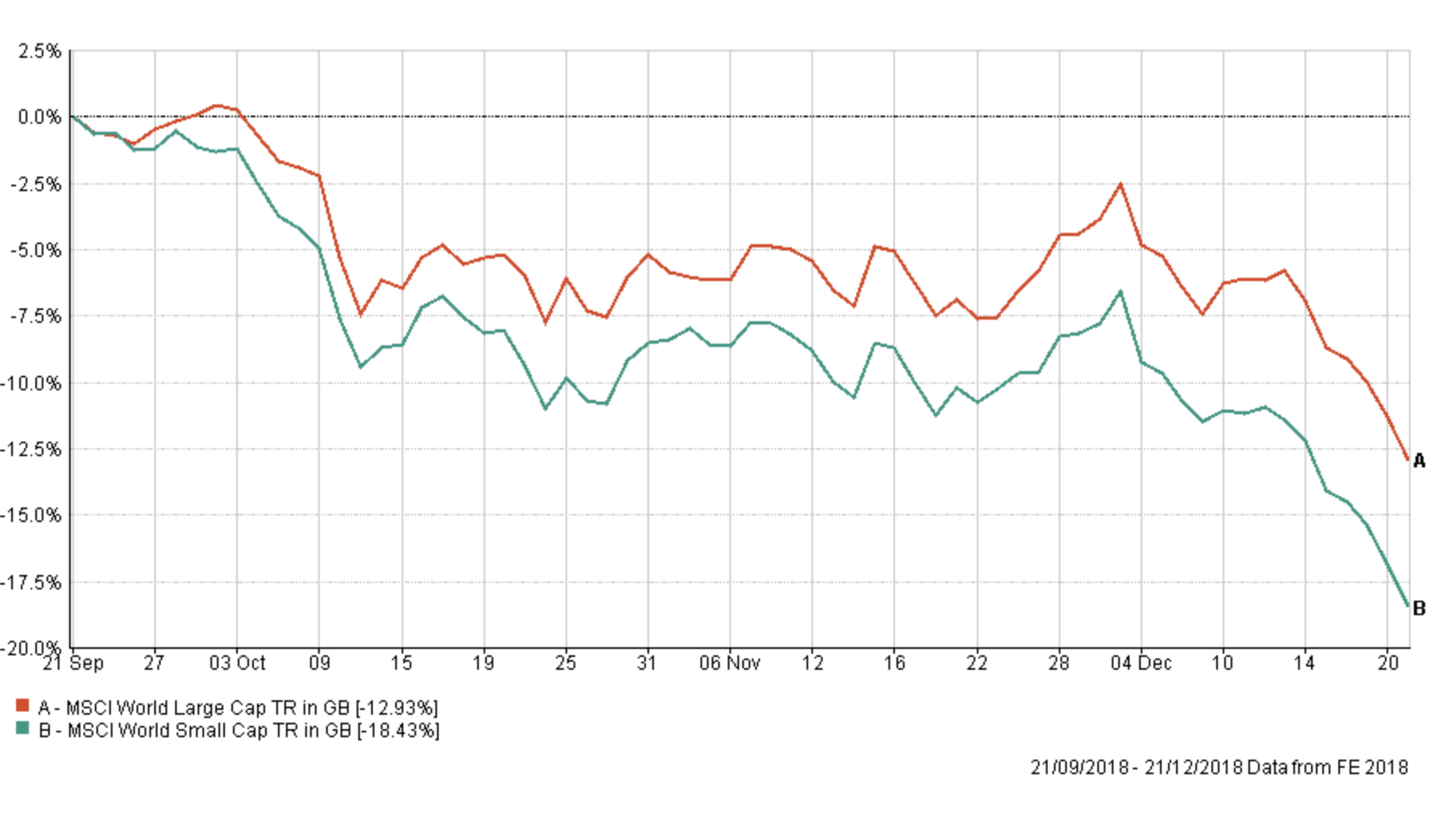

This trend gained even more traction at the start of 2018 as investors bought small caps with the view that they would be more insulated from trade war tensions. Yet again, October marked the turning point where this trend reversed and large caps started outperforming small caps (shown below). The prospect of slowing economic growth and tightening financial conditions make small caps unattractive. This is a trend to keep an eye on in 2019.

More food for thought

There are a host of other themes that will no doubt rear their head in 2019. Compared to previous years there are almost too many to list. Of course Brexit will be a huge theme, which I've discussed in my weekly notes at length. The impact on the pound is as unpredictable as Brexit itself (will we even Brexit in 2019?). A bad Brexit could see the pound fall towards $1.20 (we are currently at $1.263) or a good Brexit solution could see it bounce over $1.35 pretty quickly. The impact of a no deal Brexit on asset prices could be sizeable. Residential property prices could tumble. But so too could commercial property prices. This could lead to unit trust property funds closing again as they did in 2016 in the aftermath of the Brexit vote. I have been deliberately avoiding investing in them since the summer because of this very real risk. This could turn out to be a wise decision as I have it on good authority from industry contacts that some commercial property funds are experiencing large redemptions and are likely to close or apply penalties to investors' holdings imminently.

Trade war tensions will continue to be a huge issue in 2019 and with negotiations seeming to be going nowhere we will be talking about this topic a lot. A truce would be beneficial for stocks.

The annual discussion of whether the bond bubble will burst has been dealt a blow in the aftermath of the equity sell-off. Yields on the 10 US Treasury have fallen back below the key 3% level and their attractiveness could be enhanced further if economic growth continues to decline.

Strong company earnings growth was cited throughout 2018 as a justification for inflated share prices but there are signs that growth is already slowing which could prove a drag on stock prices.

Finally, cash has been king in recent months. 2019 could be the year where cash starts playing an increasingly important role in portfolios.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay