As we move into 2017 I have already provided 80-20 Investor members with an insight into where key markets could go. In addition, in the New Year I will update the Best of the Best Selection. However, before we say goodbye to 2016 I want to reveal the important investing lessons that 2016 contained that were obscured and crowded out by the extraordinary headlines.

2016 - annus horribilis?

It may surprise 80-20 Investor members but 2016 has been written off as an annus horribilis by active investment fund managers. In fact according to Morningstar research it was the worst year for UK asset management since 2007. Just 21% of fund houses beat the market in the 11 months to the end of November. This compares with 72% for the year before.

What this shows is the importance of being able to identify those funds (active or passive) that are likely to outperform. Understandably I am very pleased with how 80-20 Investor performed during an apparent ‘annus horribilis’ which saw unprecedented political events that fund managers struggled to cope with. The Brexit vote and Donald Trump’s US election victory were just two such events. My £50,000 portfolio finished the year up over 13%, which is a fantastic achievement in a year that was apparently terrible for making money. Even legendary fund manager Neil Woodford, who some would have you believe was born under a star, made just 2.03% during 2016.

The lessons of 2016

Yet there are some important investing lessons to be learnt from 2016. Firstly the importance of diversifying. My £50,000 portfolio is invested globally (the UK only accounts for typically between 10-20% of assets) and has typically only had a 50% equity exposure. Neil Woodford on the other hand invests exclusively in the shares of small UK companies, hence why he has struggled.

Secondly, the fact that only 21% of fund houses outperformed the market is not evidence that passive investing will always outperform active fund management. Despite the headlines this simply isn’t true. Passive funds by definition will always underperform the market they track (by the time charges are taken out) while fund managers have the possibility to outperform, although most seldom do. However, every dog has its day and there will be times where fund managers, even so called legends like Neil Woodford, underperform. Equally there are times when they will outperform. Similarly there are times when passive strategies underperform actively managed funds.

Commentators overlook the fact that there are two components to being a successful DIY investor. The first part is that we have fund houses who create passive and active funds to try and beat their peers. The fact that some do better than others is inevitable. The second component is that DIY investors need to pick the right funds from this selection. Commentators and journalists spend too much time discussing the fact that there are a lot of bad funds out there. That’s a given, so lets move on. The trick is to identify the funds that are worth holding and when to hold them, regardless of whether they are active or passive.

Of course 80-20 Investor does the latter which is the hard part when it comes to investing. It should go without saying that passive vs active is not a binary choice. You can invest in both, as I often do when investing my £50,000 portfolio. I don’t care how a fund is run, I’m just concerned whether it performs for me.

Why exactly did fund managers struggle in 2016?

There are other lessons we can take away from 2016. Why was 2016 so difficult for most fund managers? For starters the way managers either dismissed or overcompensated for foreseeable risk events was a major factor. To put it simply fund managers’ emotions wreaked havoc with their portfolios. Ahead of the EU referendum most fund managers bet that the UK would vote to remain and positioned themselves accordingly. When a Brexit vote was confirmed they over-reacted to limit any potential losses. The problem was that the market rebounded quickly and many fund managers missed the boat. By contrast passive index trackers benefited from the bounce immediately. In addition, the rebound was felt mostly in large-cap stocks which isn’t the hunting ground of many active fund managers.

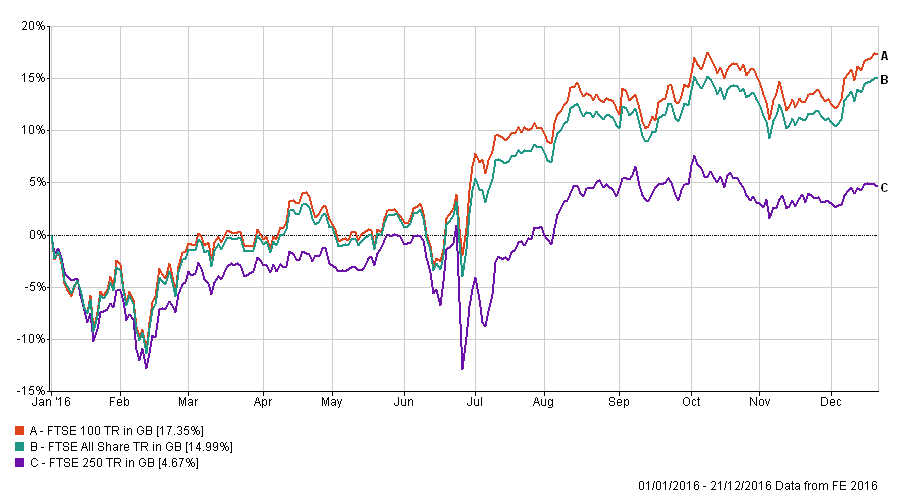

The reason this is the case is that if you want to try and outperform the market you need to fish in areas outside of those companies that have a disproportionate representation within the market indices. That has historically meant buying the shares of smaller companies. So UK equity fund managers tried to do just that in 2016. The chart below shows the performance of the FTSE 250 (which are medium sized companies) versus that of the FTSE 100 (large mega-cap companies) during 2016.

You can see that if you’d invested in smaller companies then you would have hugely unperformed. Most UK equity fund managers benchmark themselves against the FTSE-All Share index which you can see is heavily influenced by the FTSE 100. Now I’m not making excuses for them, they got it wrong but if you’d bought a passive fund that invested in mid to small cap companies you’d have also got it wrong.

Back in 2013 research showed that 90% of UK equity fund managers actually outperformed the stock market. If you look at the chart below you won’t be surprised to see that mid-cap stock outperformed large caps. In fact back then the five largest companies in the FTSE 100 accounted for 27.5% of the index market cap. Given that these companies had a torrid time it’s no wonder the FTSE 100 struggled.

At the time active managers championed the research as proof that active management beats passive investing, yet it proved nothing of the sort. I’ve picked on UK equity funds but there are other comparable trends within other asset classes.

One other issue is that fund managers tend to stick to what they know and follow the same investing patterns they have always followed. When the market favours that kind of strategy they do well, when it doesn’t they lag. The same is certainly true of passive funds which stick to an investment pattern by design. Whether active or passive they tend not to change or adapt their processes when it’s not working. For managers it’s their ego that stops them (no one likes to admit they are wrong) while for passive funds it’s the restraints placed upon them by design which stops them adapting.

Year of two halves

Also the undoing of many investors (professional or otherwise) in 2016 was their belief that they could not only predict the future outcome of a key event but also how the market would react. The Brexit vote and the US election outcome are just two examples. The phrase ‘grey swan’ has been coined to describe such events. You may already be familiar with the term a "black swan" event. For those that aren’t I’ll quote wikipedia’s definition for reference:

A black swan is an event or occurrence that deviates beyond what is normally expected of a situation and is extremely difficult to predict; the term was popularized by Nassim Nicholas Taleb, a finance professor, writer and former Wall Street trader.Black swan events are typically random and are unexpected.

The financial crisis was a black swan event. Few saw it coming, in the same way that no one expected to see a black swan until they were discovered in the wild, hence the name. A so called grey swan event is an event that is unlikely but impactful and lies outside of the base case scenarios of the market. The key point is that the market is aware of it as a possibility. So the Brexit vote is a good example. It was known to be a distinct possibility but deemed unlikely to occur and therefore dismissed by many. How you played the grey swans of 2016 dictated whether you were successful (and made double digit returns as 80-20 Investors did) or not.

Yet these grey swans meant that 2016 was a year of two halves. In the first half of 2016 the successful trade was to buy bonds and sell stocks. This was because the market was in cautious mood ahead of the EU referendum and also because it thought global economic growth would stall (both good for bonds). Yet in the second half of the year the profitable trade was to sell bonds and buy stocks as anxiety over both Brexit and Trump were brushed aside and global growth was seen in a positive light. There were similar stories in other asset classes such as Japanese equities. They fell at the start of the year and took off in the second half of 2016.

The only way you could benefit from these trends was to be flexible, assuming you’d got it wrong in the first place (which is why 80-20 Investor is not about buying and holding funds for the long term). If you take the year as a whole the top performing fund sector was US equities and the worst (aside from property and absolute return) was UK Smaller Companies (no surprise there). So the best trade would have been to avoid UK smaller companies and buy overseas equities, particularly in the US. You would have got a kicker from the fall in the pound (a result of the Brexit vote) as well as from the surge in US equities (a result of Trump). Way back in July I wrote a newsletter titled it’s all about the pound and that remained the case for the rest of 2016. Unsurprisingly global passive funds had a good year because one of their biggest limitations (they mostly invest in US assets with limited UK exposure and certainly no UK small cap exposure) became their biggest strength. What is interesting is that for most of 2016 these very funds actually struggled and Trump effectively spared their blushes. Yet the research and headlines about passive vs active overlook this fact.

So to sum this all up.

- Don’t listen to those who tell you active is better than passive investing or vice versa

- Different strategies perform well at different times

- Diversification is important

- Currency risks are having an increasing impact on investment returns

- Emotions continue to make humans bad investors

- Grey swans can be as damaging to a portfolio as Black swans

- Making emotional decisions based upon the market's consensus view of future events is often costly

- You can't predict the future or how the market will react so don't try to

- It's often far more profitable to admit you are wrong and adapt than to pursue a losing strategy stubbornly

2016 was an amazing year to be running your own money and the fact that I get emails and comments from you about how much you enjoyed running your money in 2016 (and profitably so) is fantastic. Because as the headlines suggests things aren't supposed to be this difficult apparently.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay