Long-term 80-20 Investor members may remember that six years ago I embarked on a research endeavour to find the Perfect ISA Portfolio.

In simple terms, I was trying to work out the Perfect ISA Portfolio asset mix (or whether one even existed). Was there an asset mix that had always produced a positive return in every tax year historically? Of course that wasn't enough, as just investing in cash would have achieved this. So finding the Perfect ISA Portfolio also had to maximise the upside, far outperforming cash returns. So I created a number of rules that the Perfect ISA Portfolio had to adhere to. The rules were that:

- There would be no constraint over which assets could be included or in what proportions they are held

- The portfolio must have made money every tax year since the market peak back in 2000

- and not lost money

- It had to at least beat a FTSE 100 Index tracker over the entire time period and

- The asset allocation had to remain constant throughout that time (with annual rebalancing to ensure this)

So, in essence, I wanted to find the perfect 'buy and forget' asset allocation.

Just to recap...

The portfolio had to achieve the above aims irrespective of the actual funds you'd bought. So to make sure I was only looking at the asset allocation I always used the sector average return for each asset type.

To recap, my analysis covered 27 sectors (see the original article for the full list).

The number of possible combinations was mind-blowing and it took me two full days to analyse it. I revealed the Perfect ISA portfolio is split as follows:

- 9% cash

- 71% UK Gilts

- 20% UK Equity Income

Since that time I have revisited the Perfect ISA Portfolio each year to see how it has fared in the real world. While the aim of the original research piece was to determine a 'Perfect' asset allocation based on the above rules it was also to determine whether one even existed and to educate 80-20 Investor members on how to go about finding one. One of my aims with 80-20 Investor has always been to spark an inquisitive nature in members and show them how to carry out their own research. It is all about building a hypothesis, working out the best way to test it and then analysing the results. It may well be that you reach a final conclusion. Sometimes it may be that you don't. That is part of the fun and it may surprise you that some of my 80-20 Investor research never sees the light of day because I can't support the hypothesis.

Also some research never ends, such as the Perfect ISA Portfolio because it is constantly being tested in the field every year.

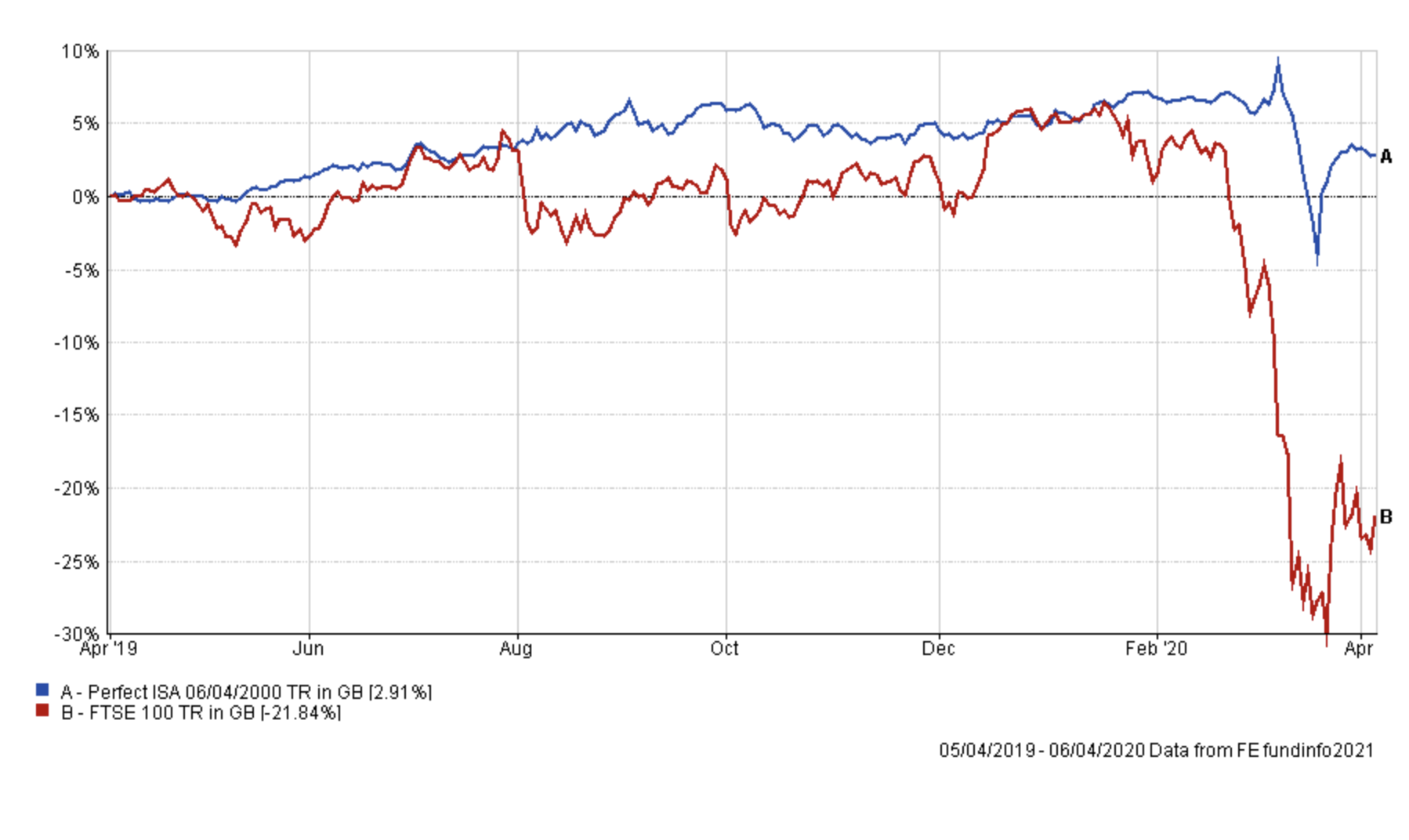

Defying the pandemic

When I revisited the Perfect Portfolio in March 2020 it was defying the pandemic equity slump, despite most stock market indices being down around 30%. However, at the time (25th March 2020) the Perfect Portfolio was sitting on a small loss of -0.6%, with just days to go until the end of the tax year. Would the Perfect ISA Portfolio finally make a loss in a single tax year?

In the days that followed, gilt funds exploded higher as investors sought safety from the stock market unease and the Bank of England embarked on a new round of gilt buying, via quantitative easing (QE). As you can see the Perfect ISA Portfolio finished the tax year up an incredible 2.91%, despite the pandemic, while the FTSE 100 was down almost -22%.

So that means that the Perfect ISA Portfolio's perfect record remains intact for the 20th year in a row, as shown by the table below.

| Tax Year (the starting year) | FTSE 100 return% |

Perfect ISA Portfolio return %

|

| 2000 | -11.13 | 3.26 |

| 2001 | -4.11 | 0.33 |

| 2002 | -24.52 | 0.51 |

| 2003 | 21.30 | 5.56 |

| 2004 | 14.46 | 6.65 |

| 2005 | 26.34 | 10.43 |

| 2006 | 9.37 | 2.17 |

| 2007 | -3.63 | 1.86 |

| 2008 | -29.94 | 0.59 |

| 2009 | 50.49 | 8.43 |

| 2010 | 7.95 | 4.67 |

| 2011 | -1.74 | 9.84 |

| 2012 | 13.44 | 7.31 |

| 2013 | 11.04 | 0.60 |

| 2014 | 5.73 | 10.96 |

| 2015 | -6.35 | 0.99 |

| 2016 | 23.44 | 7.77 |

| 2017 | 2.26 | 0.03 |

| 2018 | 8.27 | 2.78 |

| 2019 | -21.84 | 2.91 |

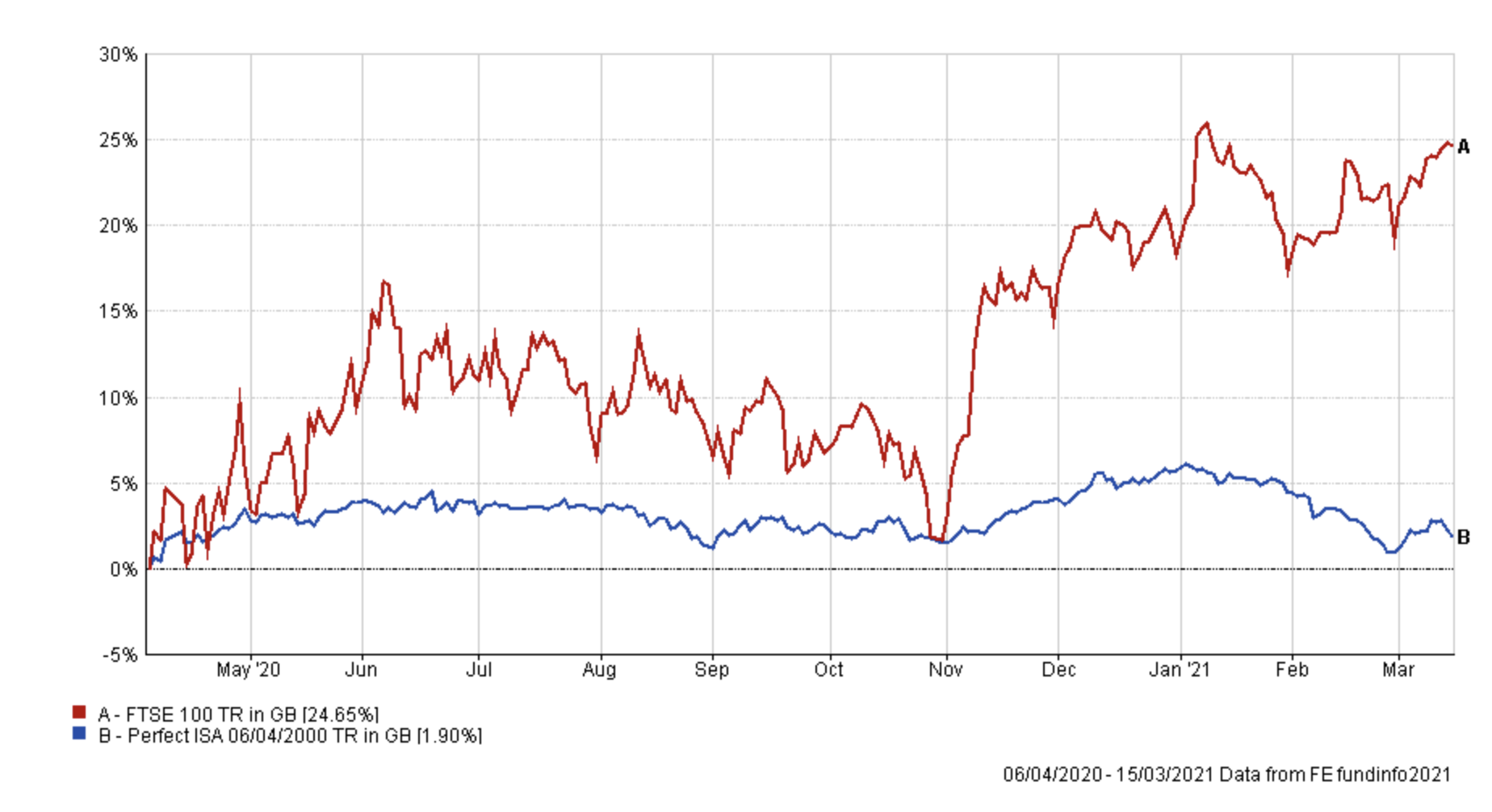

How has the Perfect ISA Portfolio fared so far in the 2020/21 tax year

The chart below shows how the Perfect ISA Portfolio (the blue line) has fared so far this tax year versus the FTSE 100 (in red).

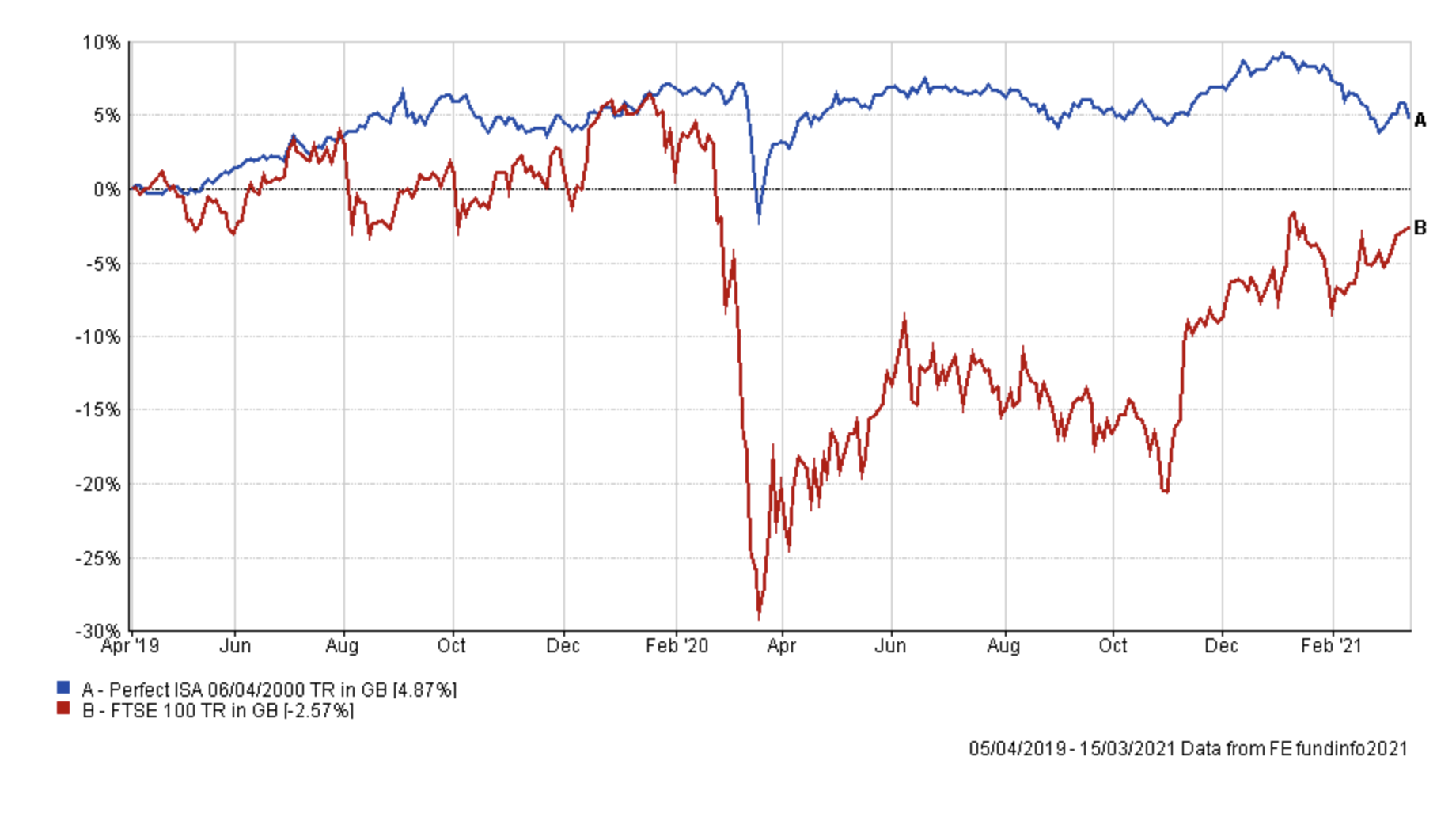

The FTSE 100 has rebounded from its pandemic-low while the Perfect ISA remains in profit despite the sell-off in gilt markets in 2021, as I've discussed in recent newsletters. However, if you put the FTSE 100's rebound into the context of its move since the start of the 2019 tax year, you can see the Perfect ISA Portfolio has outperformed, while the FTSE 100 remains in negative territory. A fantastic result.

The 80-20 Investor Perfect ISA Portfolio

Each year I also like to see what would have happened if you had used the 80-20 Investor algorithm to choose the equity funds to invest in. The assumption made is that since 6/4/2000 you would have invested £219,560 in total if you had invested your full annual ISA allowance at the start of each tax year. The result of applying 80-20 Investor to the equity content (switching equity income funds every 3 months) up until the end of the tax year in 2020 would then have been:

| Total Invested | £219,560 |

| 80-20 Perfect ISA Portfolio return | £342,772 |

| Perfect ISA Portfolio return | £321,755 |

So you would have been just over £21,000 better off with the 80-20 Investor version (i.e. using 80-20 Investor to help choose the funds to invest it).

The three UK equity income funds that would have been picked for the Perfect ISA Portfolio at the start of January 2021 were:

- MI Chelverton UK Equity Income

- TB Saracen UK Income

- Unicorn UK Income

So what are the key takeaways from this research

Once again, the Perfect ISA Portfolio has defied the market and maintained its record of making a positive return in every tax year since the year 2000, as well as maintaining its cumulative outperformance over the FTSE 100 since April 2000. The fact that its unblemished record now stretches to 20 years is a testament to the robustness of the original research carried out 6 years ago. The validity of the research continues to be tested in the field each year and I am especially proud of the results. So far in the 2020/21 tax year the Perfect ISA Portfolio looks on course to maintain its perfect record once again. Of course, I call the asset mix the Perfect ISA Portfolio but there is no reason why you could not use the same Perfect Portfolio within any tax wrapper including a pension if you so wished.

As I remind you each year, dynamism is at the heart of 80-20 Investor. By that I mean the ability to review and alter your asset mix and funds to ride the prevailing momentum in markets. However, sometimes investors will want to take a buy and hold approach with some of their money. That's perfectly fine but you can still use 80-20 Investor's research to try and improve returns. 80-20 Investor is not dictatorial and you don't have to just focus on the BOTB funds. The BFBS tables are just as important, in this instance the UK equity income sector shortlist would be particularly relevant.

Interestingly at the time of writing gilt funds are enduring a torrid time as the bond market reprices the prospect of higher inflation as the global economy rebounds from the pandemic. Understandably, at present, there are no gilt funds within the BOTB or the BFBS tables. However, the Perfect ISA Portfolio research assumes that you achieve the average return from a typical UK gilt fund. Because of their limited investment remit the range of returns achieved from gilt funds is very narrow when compared to the range of returns within other unit trust sectors. In other words the Perfect ISA Portfolio could still be applied by picking a fund that has tracked the UK gilt sector average over recent history.

For those who'd prefer to apply a Perfect ISA approach to the core of their portfolio there are passive options too. Back in 2015 a separate piece of my research was published in The Telegraph called Funds to ‘buy & forget’ in 2015. It highlighted Vanguard – LifeStrategy 20% Equity. Uncannily the fund has 20% of assets in equities globally, not just the UK, and the other 80% in fixed interest (bonds and gilts). Its global exposure does mean that it is exposed to currency moves (which my Perfect ISA Portfolio isn't to the same degree). It hasn't produced a positive return every tax year. But overall it isn't a bad proxy for my Perfect ISA Portfolio asset mix and automatically rebalances its asset mix.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay