There is a recognised phenomenon in investment markets whereby, according to the Stock Market Almanac, the 1st November marks "the start of the strong six-month period of the year for stocks".

There are a whole host of theories as to why this seasonal trend may exist. They include investment managers ditching underperforming stocks at the end of the third quarter when reporting to clients, only to then bid the market up when they put cash back to work during the winter.

Other theories claim that Season Affective Disorder (SAD) could even play a part. Some researchers suggest that 'tourist' investors start taking less risk as the autumn progresses, selling out of holdings altogether in some instances. This suppresses the market during October providing value opportunities for professional investors to buy and hold throughout the winter, by which time the stocks' true market value shines through. Another theory is that it is the byproduct of the 'Sell in May' adage'

Interestingly the winter phenomenon has lead some to develop the idea of Winter Portfolios. Interactive Investor, the second largest broker in the UK, is an advocate of this approach. It claims that "data from The UK Stock Market Almanac shows that starting with £100 in 1994, an investor who had been invested in the market continuously for the past 25 years would have seen their money grow to £257 (excluding dividends). However, if they had only invested in the market between 1 November and 30 April every year, that £100 would be worth £341. Conversely, if they had chosen to only invest over the summer months they would have lost money; their original £100 would be worth just £69. Seasonality is more pronounced in some stocks than others"

So, "after five years of consistently beating the wider stock market, [Interactive Investor's ] winter portfolios are back to exploit this curious anomaly."

You can find full details here, but essentially Interactive Investor builds two portfolios made up of 5 stocks each to buy and hold between 1st November and 30th April.

Interactive Investor manages this by:

"Screening only stocks listed in the FTSE 350 index for a greater level of liquidity, the five most reliable winter performers of the past 10 years form the interactive investor Consistent Winter Portfolio. A basket of five typically higher risk/higher return stocks, which still exhibit impressive consistency over the winter months, become the interactive investor Aggressive Winter Portfolio.

Every constituent in the 2019-20 consistent portfolio has risen during the six winter months each year for at least the past decade. The average return for the period November to April, excluding dividends, is 17.8% versus an average gain of just 5.0% for the FTSE 350 benchmark index.

To access even greater potential returns, entry criteria for the aggressive portfolio for 2019-20 is relaxed slightly. That makes it a little riskier, but even now all five constituents have a 90% success rate generating positive returns over the past 10 winters. The average winter return since 2009 is 27.1%."

Obviously this is a high-risk strategy as each portfolio invests in just five stocks. So it begs the question could the same be achieved using UK equity funds instead, to mitigate some of the stock-specific risks? Funds hold tens if not hundreds of stocks from different companies which mitigate stock-specific risks. This would potentially dampen potential returns, assuming a Winter Fund portfolio is even possible, but the risk/reward potential could be appealing

The Winter fund portfolio

Inspired by the Interactive Investor Winter portfolio I decided to explore the idea of a Consistent Winter Fund Portfolio. To do this I analysed the performance of every unit trust fund from the UK Smaller Companies and UK All Companies sector across the November to April period in each of the last 10 years.

I then looked for funds that had made a positive return in each winter period, of which there was quite a number. In fact out of the 274 funds, 85 achieved this feat.

In order to identify consistency, I then ranked each fund's return for each Winter period with 1 being the best and 274 being the worst. I then calculated each fund's average position across the 10 winter periods and ranked them accordingly. I then took the most consistent 5 funds based on their average rank across the ten years. The funds that form my Consistent Winter Fund Portfolio are as follows:

- BlackRock - UK Smaller Companies

- BMO - UK Mid-Cap

- Fidelity - UK Smaller Companies

- Invesco - UK Smaller Companies Equity (UK)

- Liontrust - Special Situations

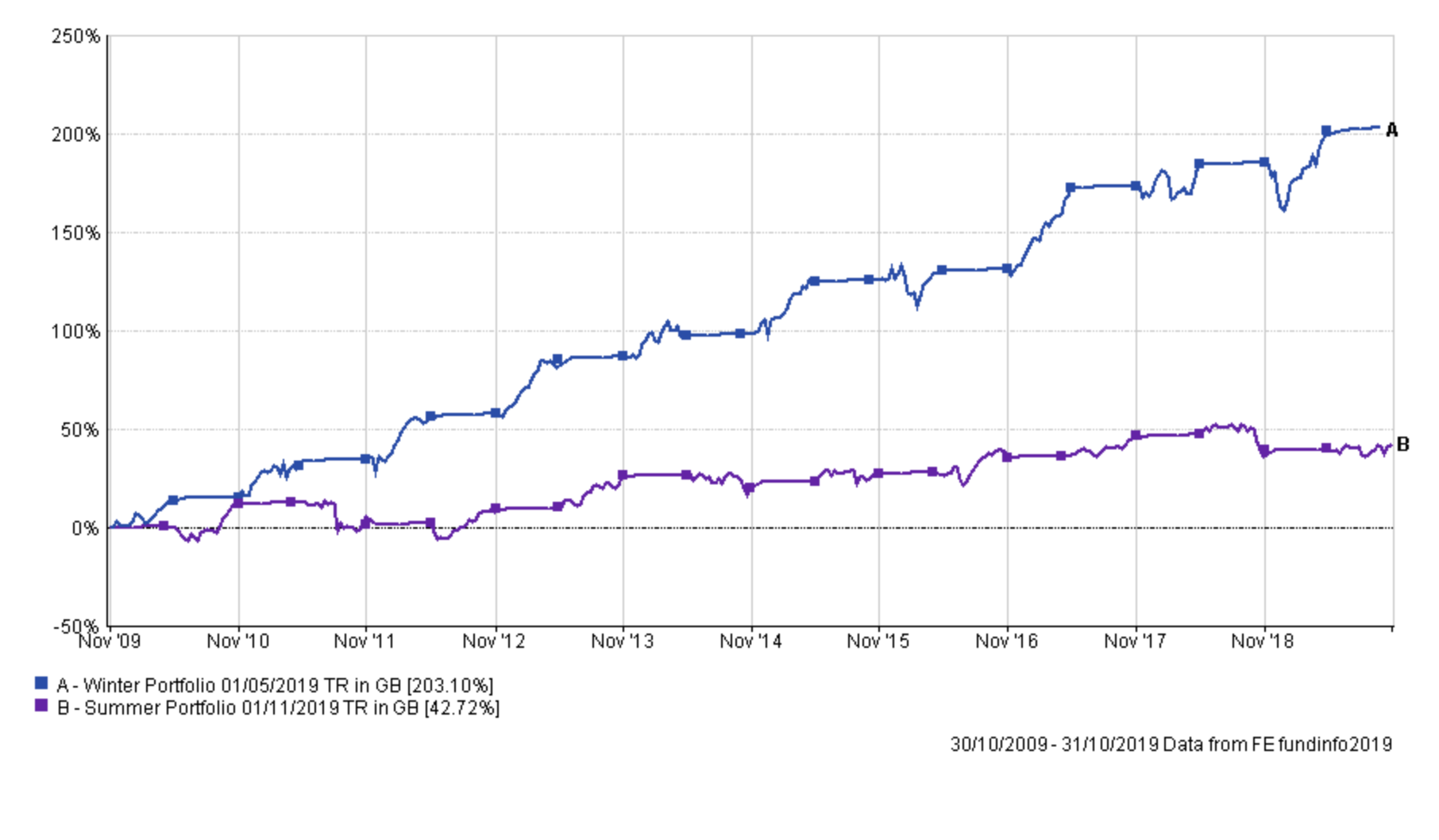

The chart below shows the performance of this portfolio over the ten years assuming that you switched into cash during the summer months. I also compare it to an investor who had invested in the FTSE 350 and the FTSE 100 for the entire period. You can see that the difference in returns is staggering, lending credence to the notion of a winter bias. The Winter Conservative Fund Portfolio (the blue line) far outperforms the market (you treble your money) but is invested in cash half of the time.

Interestingly if you compare it to the FTSE 250 (green line) the portfolio performance (total return including dividends) is more on a par, but as mentioned the Winter fund portfolio is only invested in equities 50% of the time.

The difference is even more impressive when you consider key fund metrics shown below. The alpha generated by the portfolio is far in excess of the index while the beta (how much a portfolio's moves simply reflect the wider market) is low. The volatility of the Winter fund portfolio is much lower while the Sharpe Ratio (the extra return the portfolio gets for each unit of risk it takes) is far higher.

| Name | Alpha | Beta | Max Drawdown | Max Gain | Max Loss | Negative Periods | Positive Periods | Annual Return | Sharpe | Volatility |

| FTSE 100 | 0 | 1 | -17.21 | 15.01 | -11.26 | 216 | 278 | 7.92 | 0.31 | 14.23 |

| FTSE 250 | 0 | 1 | -19.26 | 14.8 | -12.69 | 206 | 288 | 11.56 | 0.57 | 14.19 |

| FTSE 350 | 0 | 1 | -16.49 | 12.67 | -11.46 | 213 | 281 | 8.42 | 0.35 | 13.94 |

| Winter Conservative Fund Portfolio | 9.66 | 0.28 | -9.86 | 19.5 | -6.94 | 84 | 228 | 12.21 | 1.18 | 7.36 |

But what about if you had invested in the Winter fund portfolio during the summer months instead and switched to cash during the winter (i.e do the opposite thing)? Let's call this the summer portfolio. If there is a seasonal factor at play then we should see a difference between the two outcomes. The chart below shows that there is a huge difference adding further weight to the winter theory.

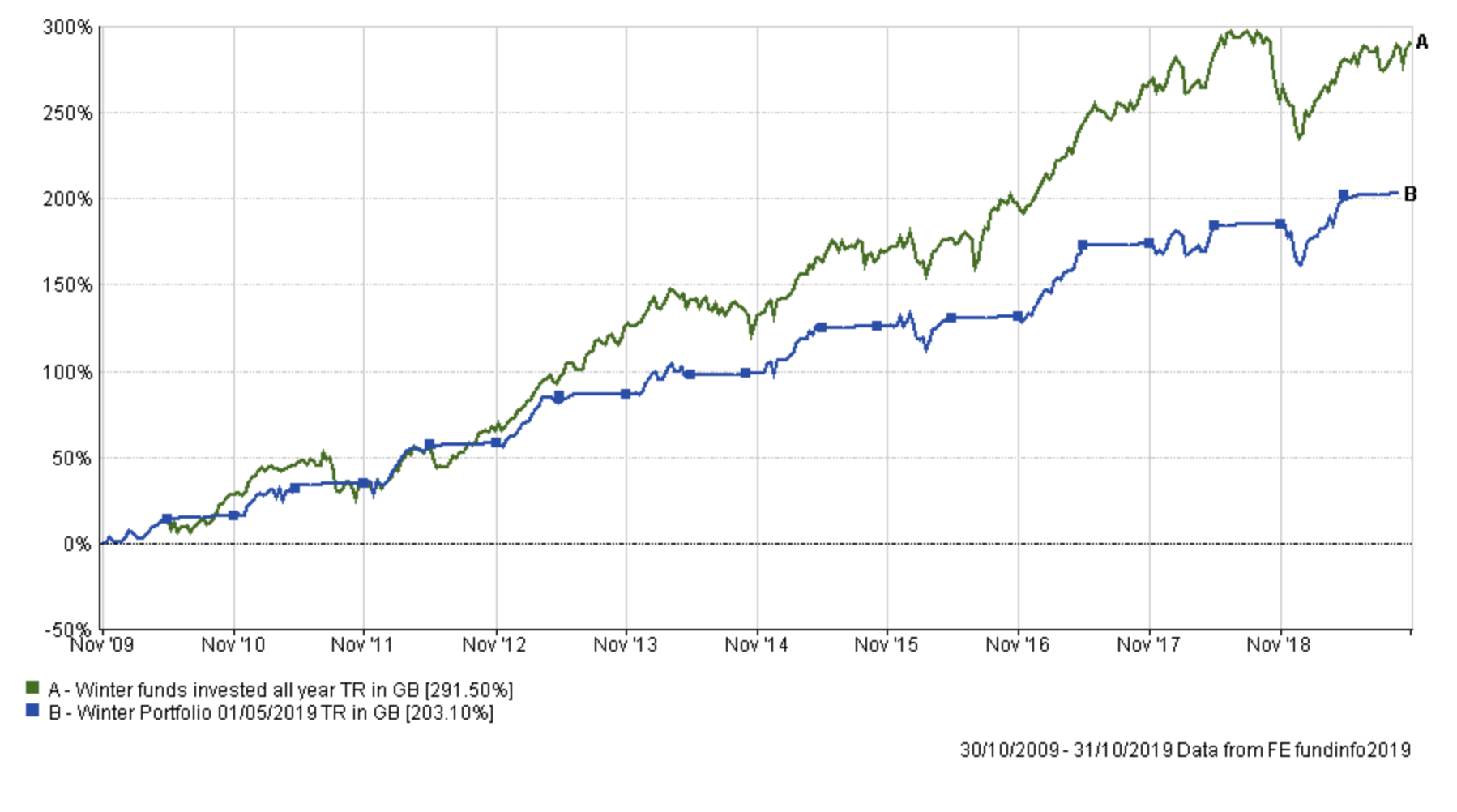

It obviously follows that if you had been invested in the Winter Portfolio continually all year round (not going into cash in the summer) then you would have made more money has shown in the chart below but the level of risk taken would have been far higher for not proportionately higher reward as reflected by the all-year-round portfolio's lower Sharpe ratio of 1.01

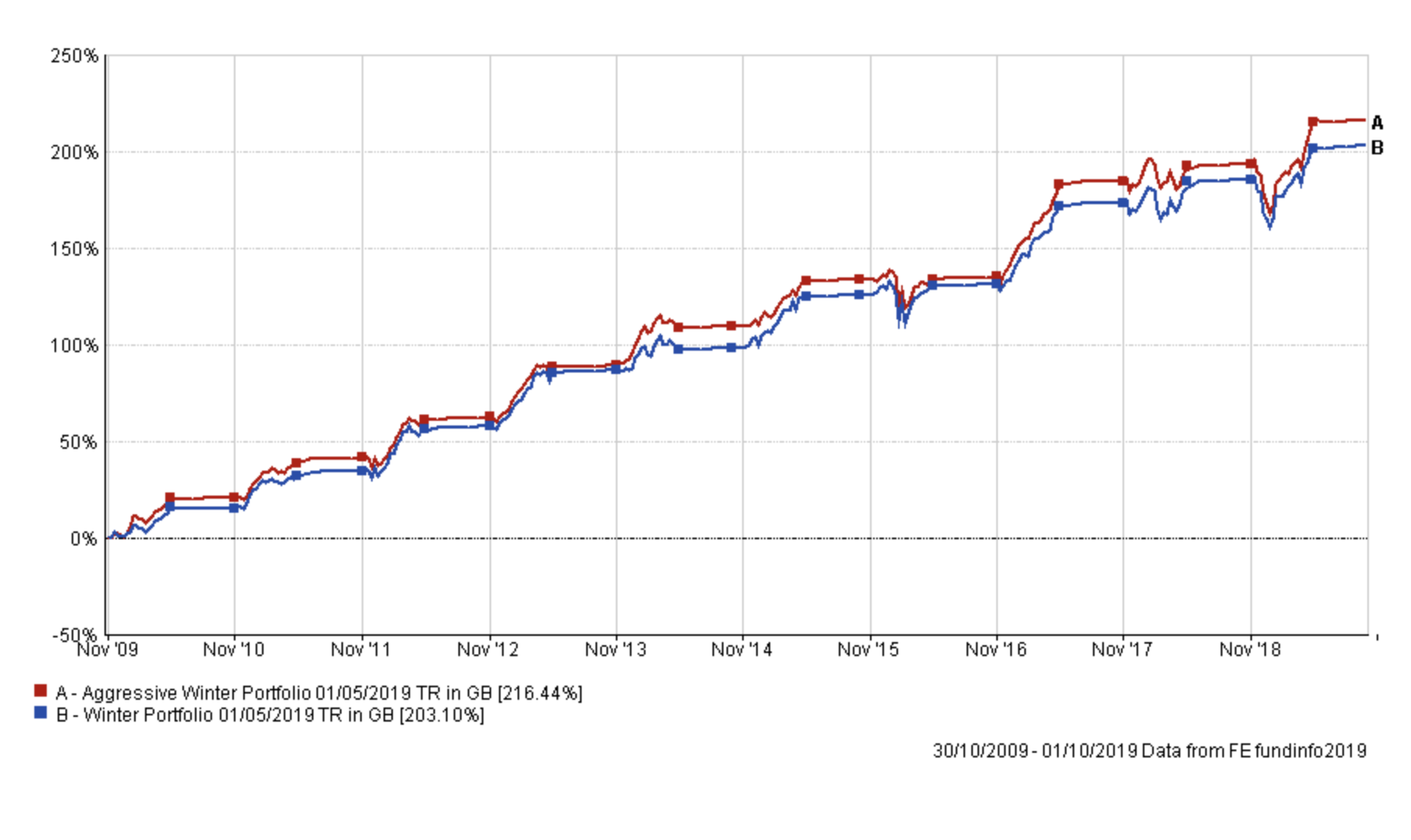

Interactive Investor also produced an aggressive version of their Winter portfolio. Using a similar methodology I created an Aggressive Winter Fund Portfolio. Funds within this portfolio made positive returns in the last 10 winter periods on at least 9 occasions but also produced the best average return. The five funds that make the portfolio are:

- Fidelity - UK Smaller Companies

- Franklin - UK Mid Cap

- MI - The MI Discretionary Unit

- Slater - Growth

- Unicorn - UK Smaller Companies

Interestingly Fidelity UK Smaller Companies appears in both of my Winter fund portfolios. The chart below shows that there really isn't much difference between the performance of the Aggressive Fund Portfolio and the Conservative Fund Portfolio to necessarily warrant the extra risk.

So to sum up there appears to certainly be something in the idea of a Winter Fund Portfolio. Of course, there is an element of 'cherry-picking' by looking at consistent performers from the last 10 years and assuming you held them throughout. In the future it would be interesting to see what would have happened if we'd applied the 10-year backward-looking process at the start of each year, meaning that the portfolio would change from year to year. That is something to ponder in the future. For now, it will be interesting to revisit the portfolio's listed above at the end of April 2020 to see what the outcome will be this winter, a winter where the UK is faced with a general election and a possible Brexit.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay