We are now just one week away from the UK general election and the market is starting to get a bit twitchy. As I mentioned in May’s monthly newsletter commentary market angst was always likely to increase as the election date drew closer. When Theresa May fired the starting pistol on the election campaign she did so in the belief that a landslide Conservative victory was fairly certain. The Labour party was seen as a wounded animal with the Conservatives circling in for the final blow.

The announcement of the general election caught the market by surprise and the pound rallied more than 4%, as they priced in the possibility of a strong majority Conservative government. The logic has been that if Theresa May is given a strong mandate, by the UK electorate, in the Brexit negotiations then a softer Brexit was more likely. A soft Brexit should mean a more positive economic outlook for the UK and the prospect of interest rate rises in the future as this becomes reality. All of these are positives for the value of the pound. Conversely, a strong pound is normally bad for the FTSE 100 but that relationship broke down, albeit temporarily, as the FTSE 100 also rallied after Theresa May's announcement. The upshot is that investors have seen the value of their investments dramatically impacted by the election campaign to date. For starters all of their overseas funds are notionally worth 4% less than they were 7 weeks ago because of currency moves, ignoring any movements in the underlying asset values. Meanwhile their UK equity exposure has rallied 5%.

But now that we are on the final stretch of election campaigning how is the election likely to affect your investments? What does history tell us to expect? How might you play it?

Pre-election rally

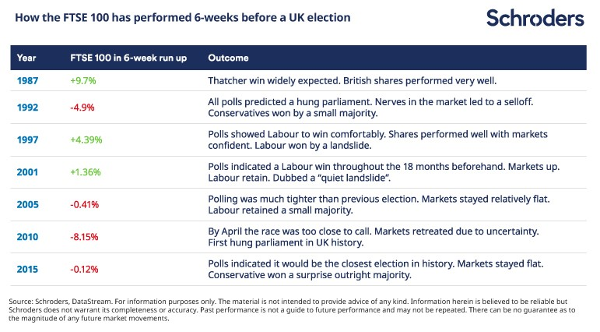

The table below, complied by Schroders, is a neat summary of how the market has reacted in the lead up to general elections since 1987 (click to enlarge).

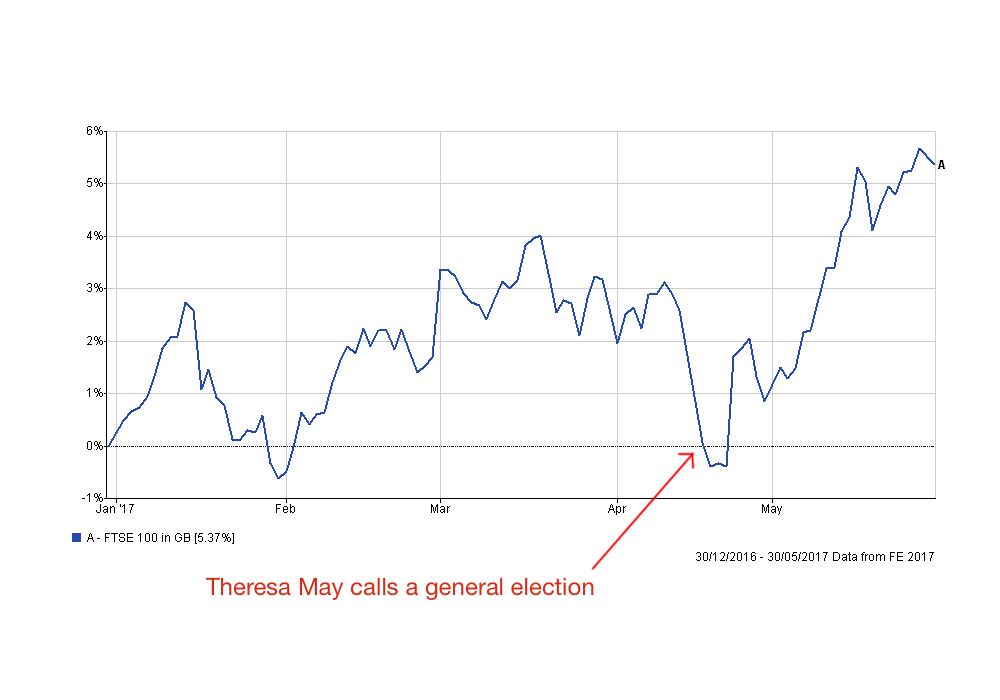

The key takeaway from this table is that the FTSE 100 does well in the lead up to a general election if there is a widely expected outcome. Theresa May called next week’s general election based upon the polls' suggestion that she would win a clear majority. If we look at the performance of the FTSE 100 since 1st January 2017 you can clearly see that all of this year’s gains have been a result of this ‘election trade’. The red arrow shows the point at which Theresa May called the election. So strong was the market reaction that the normal inverse relationship between the value of the pound and the value of the FTSE 100 snapped, as described earlier.

Post-election slump?

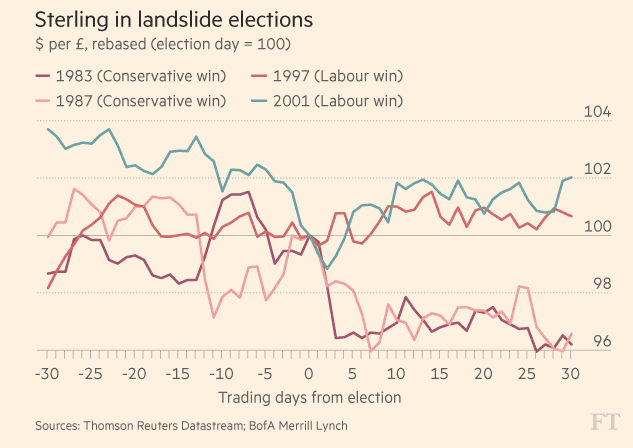

Now let’s assume that Theresa May’s gamble does pay off and she records a landslide election victory. History suggests that landslide election victories don’t necessarily translate into further equity profits. The table below summarises the outcomes after previous general election landslide victories.

| Year | Landslide winner | Notes |

| 2015 | Conservatives | While not expected it was an outright victory for the Conservatives. Markets immediately jumped 2% after the surprise result before fading. Ended the year over 9% down from the election date, mainly due to China induced sell-off in the summer |

| 1997 | Labour | Preceded by stock market gains and a further 15% gain in the second half of the year, after a 10%+ correction |

| 1987 | Conservatives | Preceded by stock market gains but soon followed by Black Monday and 30% sell-off |

| 2001 | Labour | Dotcom bubble implosion was under way & preceded 9/11 attacks - stock market was already in decline and continued |

Clearly the anticipation of a landslide victory is positive for markets in the lead up to the election but it does little to support markets afterwards. Markets rally on anticipation/hope until the result is confirmed before other macro events eventually overwhelm investors. So the above ‘landslide’ precedents do little to tell us what we can expect after June 8th. More broadly, the UK stock market has typically underperformed global stock markets by 3.4% in the three months after general elections since 1970.

How might global stock markets fare?

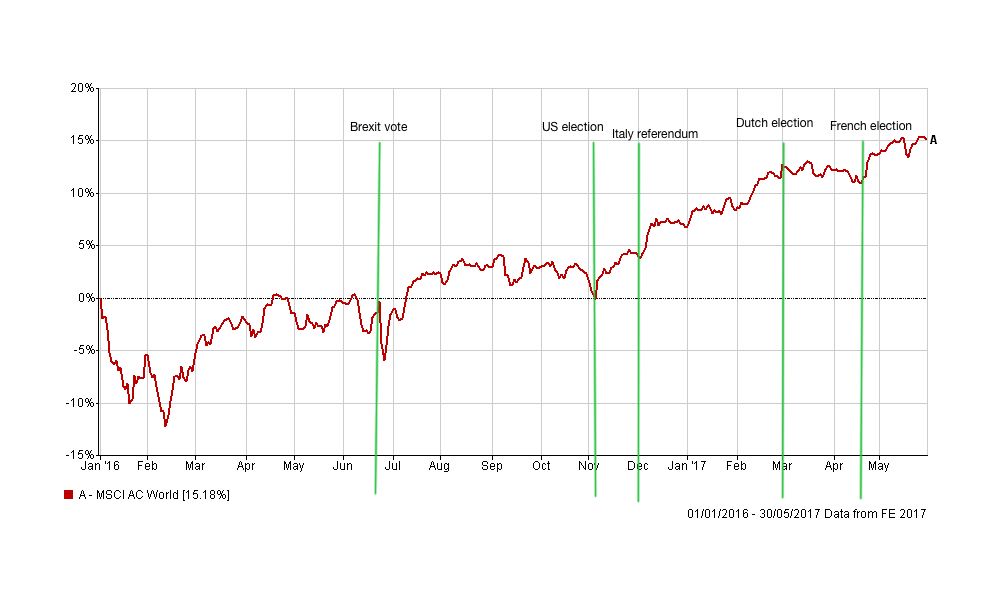

So how will global stocks be impacted by the election result? Well, since the start of 2016 there have been a series of political votes that have either had the potential to throw up surprises or actually did (in the case of the Brexit vote and the US election). The chart below shows how global equities have performed after the major political votes since the start of 2016. Once again click the image to enlarge it.

The market has continued to march higher even when the outcome was not as investors had hoped for. The speed at which markets have got over political shocks has decreased from days (in the case of Brexit) to hours (in the case of Trump) to minutes (in the case of the Italian referendum). While the market may be overlooking political risks it is still sensitive to them as I explained in this market commentary, more so than people realise. However, the ‘buy the dip’ mentality has gripped markets ever since central banks started printing money and slashing interest rates and looks likely to provide a backstop for now.

Impact of a hung parliament

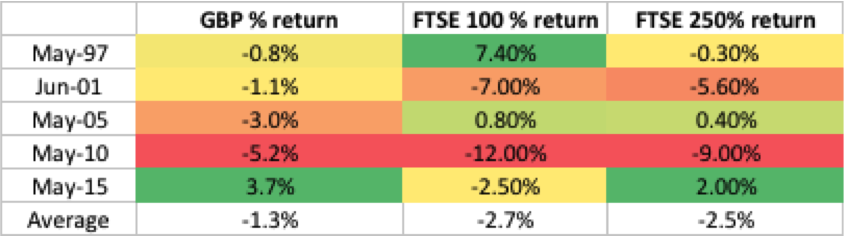

Perhaps the biggest shock would be if Theresa May doesn’t win the election. At the time of writing the latest polls are suggesting a narrowing lead for the Conservatives, with one poll even suggesting we are heading for a hung parliament. That would be a shock and we only have to go back to 2010 for a precedent of how a hung parliament could affect your investments. The table below was derived from research carried out by UBS which shows performance during the two months across the past five general elections. On the face of it a hung parliament like in 2010 would be pretty disastrous for the FTSE 100. While it would no doubt be a negative, especially with the upcoming Brexit negotiations, 2010’s figures also marked the start of the Greek debt crisis. So again, other macro events overwhelmed the impact of the UK election result on equity markets after election day.

How will the election affect the pound?

The table above does raise a couple of other interesting points. As 80-20 Investor members you are now only too aware of the importance of the value of the pound on your investments. Typically across an election you can expect the pound to fall more than 1%. However, an unexpectedly strong result (like in 2015) will be positive for the pound and that would likely be the same in 2017. But even in landslide election victories of the past a rally in the pound has rarely lasted as shown in this chart published by the FT.

Be more focused

While the absolute return of the UK stock market as a result of the election is difficult to determine based on history the relative performance of the UK equity market as a whole (as mentioned earlier) as well as facets of it show some patterns. While the UK stock market is likely to lag its global peers in the aftermath of the election, if we go back as far as 1992 (not shown in the above table) 60% of the time the FTSE 100 outperforms the FTSE 250 in the 3 months after the vote. The message would seem to be slightly favour large cap funds over smaller companies funds but it’s not a complete either/or scenario. It’s best to hedge your bets.

There is also an apparent sector bias. Banks and financials tend to underperform in the run up to a general election yet outperform after a general election. Interestingly if I analyse the UK equity funds out there with a heavy financial bias there are a number of them that are also mid cap focused (FTSE 250) which slightly contradicts the above large vs mid cap findings. Below I list the funds with the greatest financial asset exposure %.

| Fund | Financial exposure as % of assets |

| JPM - UK Strategic Equity Income | 36.5 |

| BlackRock - Mid Cap UK Equity Tracker | 34.95 |

| GAM - UK Diversified | 33.82 |

| Henderson - Global Care UK Income | 33.8 |

| HSBC - FTSE 250 Index | 33.7 |

| Invesco Perpetual - UK Focus | 33.4 |

| SVS Church House - Deep Value Investments | 32.5 |

| Schroder - UK Opportunities | 32.5 |

| Schroder - The Equity Income Trust For Charities | 32.25 |

| Fidelity - Special Situations | 32.2 |

| Invesco Perpetual - UK Strategic Income | 31.88 |

| Liontrust - UK Ethical | 31.85 |

Summary

Pulling all this together, history seems to be telling us that by election day the easy money has already been made. A landslide victory is not automatically good for the pound long term, although we will likely see a boost, and it certainly doesn’t dictate what will happen to equity markets. A tendency for a weaker pound seems to back up the findings that large cap stocks marginally outperform mid cap stocks. Either way history suggests that you'd be brave to take a bet on the fortunes of sterling. Investors and analysts trying to play the UK election are ultimately just tinkering because macro events are likely to soon swamp any influence that the election outcome has on markets. In addition, not overexposing your portfolio to UK equities for the 3 months after the election, instead favouring other global markets seems sensible. If we get a shock result such as a hung parliament (but polls are not to be trusted since the Brexit vote) then the market will likely react negatively as it doesn't like uncertainty. However, the 'buy the dip' mantra could settle things if 2016 is anything to go by.

One parting comment is that history never repeats exactly, but it's interesting that the last time we had a hung parliament the Greek debt crisis erupted. While a hung parliament is unlikely in 2017 the Greek debt crisis is starting to bubble up once again. There just hasn't been much press coverage of it yet.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay