One of the biggest risks for US equities, and to a certain extent global investment markets, is the outcome of the impending US election in November.

In this month’s Chatterbox I was asked the following question…

Hi Damien

With the US elections approaching have you done any research in the past on the impact of the election results on investments and how best to prepare a portfolio for either outcome. Should we expect “bigly” change or is it business as usual.

Thanks

To which I responded:

Hi

I don’t think I have. I have done research looking at the impact of the UK election but not the US election. Perhaps this is something I can look to cover in a future research article or weekly newsletter.

Best wishes

Damien

So true to my word I thought it was a topic worth investigating. In this article, I look at the likely impact on US and global stock markets as well as the potential impact on the dollar, commodities and bonds.

The predictive powers of the US stock market

First of all, it's worth considering the fact that the US stock market has been pretty good at predicting the winner of past US elections. Based upon research, going back as far as 1928, the performance of the S&P 500 in the three months prior to a US election is a pretty good indicator of which party will win.

On 12 of the 14 occasions when the market rose during the three months before an election the incumbent party won. Conversely, on 8 of the 9 occasions when the market fell during the three months prior to an election the incumbent party lost. The indicator even managed to predict the shock Trump win in the 2016 election.

Fast Forward to 2020 and it means that Trump needs the S&P 500 (currently sitting at 3,417) to finish above 3,271 according to the market’s predictive powers. Right now the S&P 500 is setting new all-time highs, so Trump needs the stock market to keep pushing higher. Perhaps it is little wonder that he is keen on issuing new $1,200 stimulus cheques to the electorate. The first round of stimulus cheques issued earlier this year has been cited as fuelling the stock market speculation that helped US stocks rebound from their March lows.

Does it matter who wins the US election?

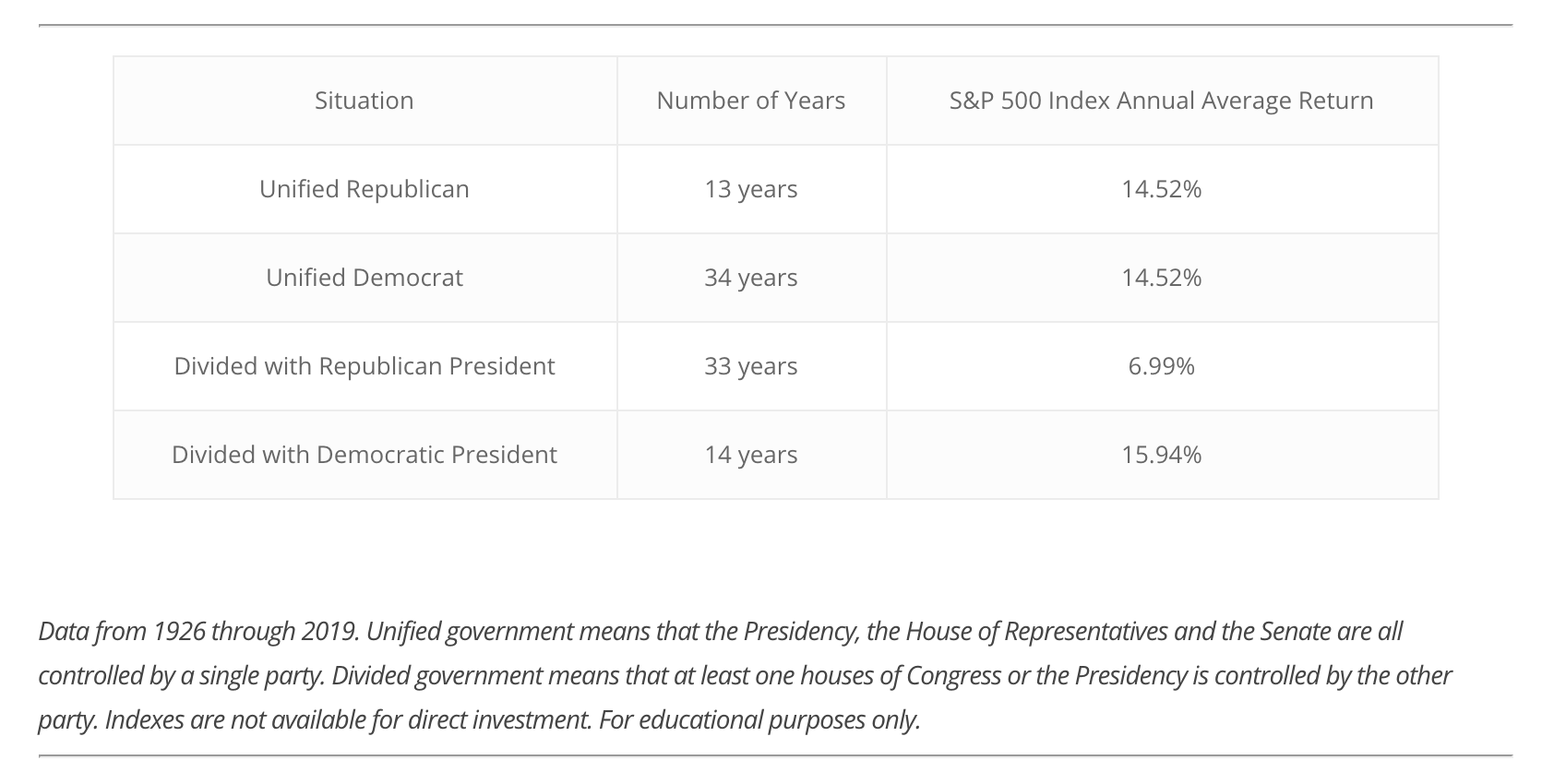

According to research published in the Financial Times "from 1952 through June 2020, annualized real [US] stock market returns under Democrats have been 10.6% compared with 4.8% for Republicans". This goes against the conventional belief that Republicans' pro-business politics should, in theory, be good for the stock market. However, the relationship between which party the President represents and stock market performance is more complex than the data suggests. Producing annualised returns causes some large distortions in the data. In July Forbes produced the following table below which shows the performance of the S&P 500 during each Presidency going back to 1945. If the table was reproduced today Trump would be two places higher with a return of 63%.

The data suggests that perhaps the biggest influence on the performance of stocks during a Presidential tenure is the macroeconomic backdrop and not which party the President represents. George W Bush, the worst US President for the US stock market, presided over two recessions following the dotcom bust and the financial crisis. However, George W Bush inherited the excesses of Clinton's tenure and a technology bubble that was in the process of bursting. Was George W Bush just unlucky or incompetent? But the table below, also based on Forbes' data, shows that Democrats have tended to enjoy tenures during periods of economic expansion. It's difficult to say whether it's cause and effect or just coincidence that Democrats have enjoyed better economic conditions. However, it seems unlikely that the Republicans have been just unlucky.

| Party | No. of economic expansions beginning during tenure | No. of recessions beginning during tenure |

| Democrat | 5 | 2 |

| Republican | 7 | 10 |

So taking the evidence in the round, the message would seem to be that a Democratic win in November would be better for US investors. Don't forget, ultimately what is good for US stocks is generally good for global stock markets too.

How the election is won matters more than who wins

According to research by Mclean Asset Management "during election years where the Presidency stayed in the same party (either the President was reelected, or the new President was from the same party), the S&P 500 averaged an annual return of 16.00%, but when the Presidency switched parties, the annual average return was only 5.14%."

This can perhaps be explained by the fact that a party switch is most likely to occur when the electorate is dissatisfied with the current economic backdrop and blames the incumbent party for the situation. In this instance, as the data earlier suggested, the incoming party is likely to have inherited the predecessor's 'mess', making the task of economic expansion (and a possible stock market rally) that more difficult to achieve.

However, there are always exceptions, Donald Trump himself being one. Interestingly, Trump is the first President to fixate on the value of the stock market, tweeting about it when it rallies while at the same time taking full credit. He has even demonstrated his willingness to talk up the market with empty promises of trade deals or coronavirus cures. Perhaps this could explain the break from the historic pattern of underachievement for the incoming party.

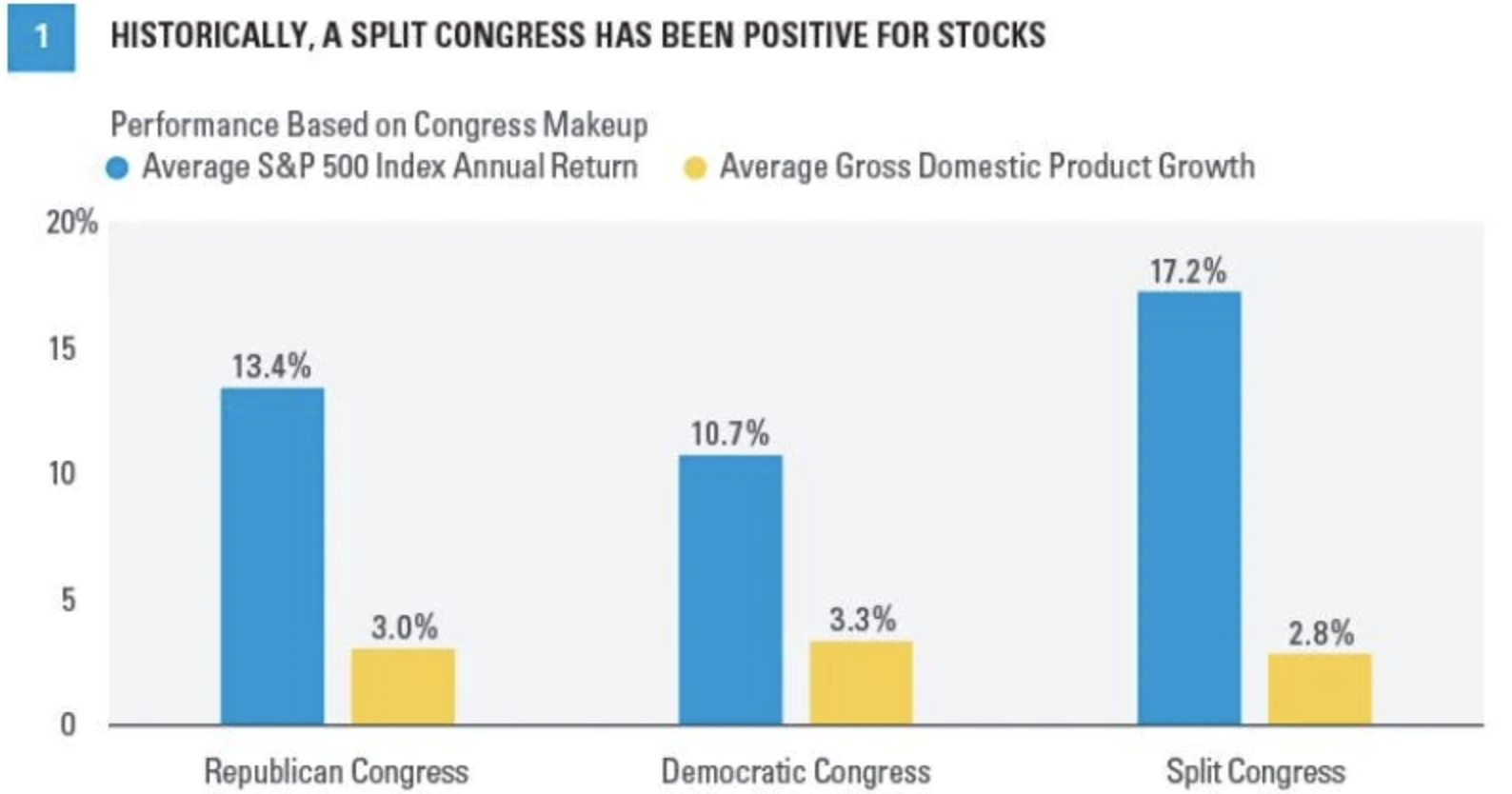

Research from LPL Financial suggests that the stock market is also far more concerned over the makeup of Congress than who actually wins the Presidency. The chart below looks at Presidencies since 1950 and shows that the stock market performs better when Congress is split (i.e. where different parties control the House and Senate).

It suggests that a divided government with a Democratic President would be preferable, but failing that a unified government of any sort will do.

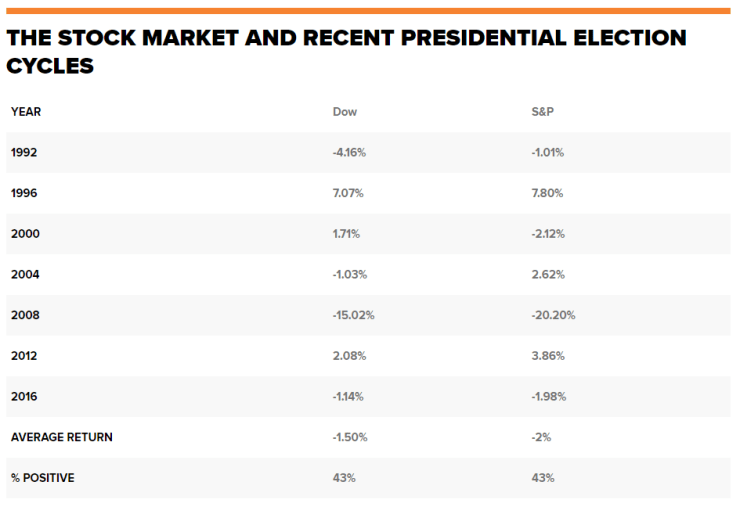

How do US stock markets perform in the lead up to a US election

As mentioned earlier the 3 months leading up to the election have a successful track record of predicting the outcome of an election. But put that to one side, how might markets behave between now and the US election on 3rd November 2020. The table below shows the performance in the lead up to elections from 1992 onwards. You can see that the odds favour a slight fall in the stock market ahead of the vote, but the financial crisis skews things. Take 2008 out of the equation and the odds of the market rising or falling are akin to a coin toss.

How do US markets perform after a US election

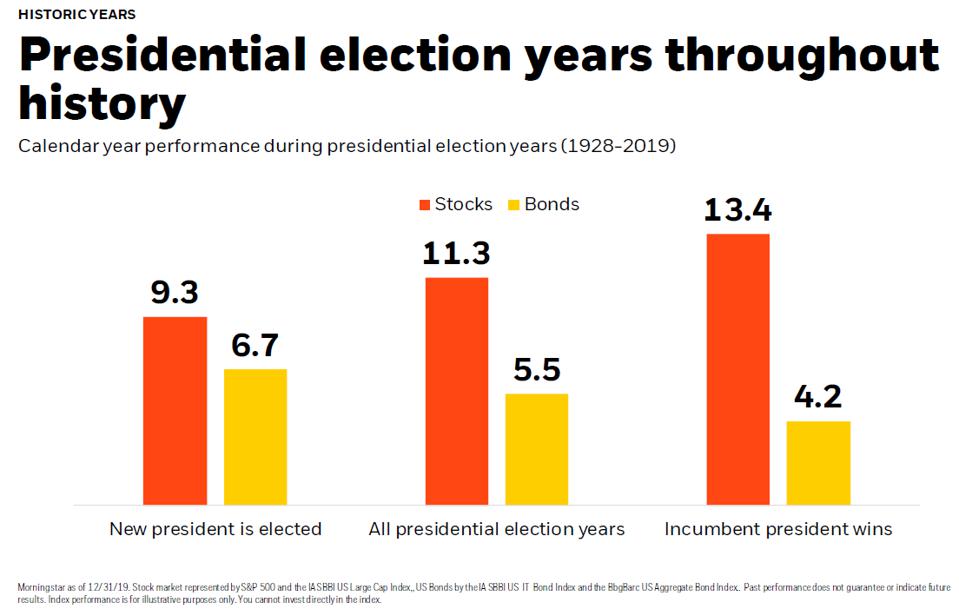

History, going back as far as 1928, suggests that should Biden be elected, that it would be good news for bonds, less so for equities. Year to date the S&P 500 is up 5.3% while bonds are already up 7.1%. History also, therefore, suggests there will more likely be more upside in stocks than bonds whatever the outcome.

Which US sectors should you invest in or avoid?

Trying to predict how individual sectors of the US stock market are likely to fare in the aftermath of the election is crystal ball gazing. While I would advise against trying to predict the future, investment banks are expected to do so by their clients. So below are the views of UBS and Morgan Stanley. I place no emphasis on either outlook, but it gives you a feel for what the 'smart money' is thinking

UBS

While UBS' outlook for markets if the election yields a divided government is fairly non-committal, it is more specific in its views of the winners and losers if there is a unified government. UBS states:

Trump Trade 2.0 (Trump win)

The main characteristics of the first Trump Trade are likely to persist in version 2.0, albeit in diminished magnitude. The expected pro-growth policy mix of tax cuts, fiscal spending targeted to infrastructure, and deregulation would be incrementally positive for growth and equities. Financials and energy could benefit both because they are key barometers of economic growth and because the uncertainty of potential regulatory changes under a Biden win would be eliminated. This policy mix could also benefit value stocks more broadly. However, the risk of a reescalation in the trade wars could temper investor enthusiasm.

The Biden Trade (Biden win)

There may be a widespread presumption that a Blue Wave would be negative for US equities, and other risk assets to a lesser extent. We acknowledge the risk, but we think a Blue Wave will have a roughly neutral effect on equities, though there will likely be winners and losers. Virtually all companies will face the prospect of higher corporate taxes. But bear in mind that tax increases could be phased in over time and higher government spending may exceed the level of tax increases. At a sector level, industrials, materials, and segments of tech and utilities could be modest beneficiaries from transportation, green, and tech infrastructure spending.

Morgan Stanley

Morgan Stanley lays out four post-election scenarios which I've laid out verbatim:

Divided Government Scenarios

The Thin Red Line (R President, R Senate, D House)

In this status-quo scenario, the recession is short-lived and President Trump benefits, as the economy rebounds from the pandemic. The likely results would include continuing deregulation, which would benefit the telecom and energy sectors, as well as asset managers, though renewables could face pressure. The report expects only minor near-term policy changes and compromised extensions to the expiring 2017 tax bill. U.S. interest rates would likely remain range-bound, or fall further after the election, depending on the path of the recovery. Reactive fiscal expansion is likely, and the dollar could face downward pressure.

Blue Tide (D President, R Senate, D House)

Themes like healthcare and leadership, where Democrats have a trust surplus with voters, dominate the campaign and deliver the election to Biden, whom most voters believe would be better at managing the ongoing crisis, based on current opinions on the pandemic response. Voter demand for change could result in increased regulation and oversight, pressuring certain sectors, such as financials, U.S. energy, telecoms, IT hardware, internet and pharmaceuticals. While early signals of a Biden win could dampen markets before November, after the election of a divided government, U.S. rates markets are unlikely to move dramatically—and may even fall slightly. As with the Thin Red Line scenario, this divided outcome could modestly weaken the dollar.

Unified Government Scenarios

Red Redux (R President, Senate and House)

A V-shaped recovery energizes Republican voters and propels President Trump to a second term and a Republican take-back of the House. Trump adopts a more aggressive, anti-China stance, amid greater U.S. voter wariness of China. A Republican sweep could mean further tax cuts and early extension of Trump's expiring tax provisions, resulting in higher deficits. Such fiscal stimulus would likely boost U.S. GDP and strengthen the dollar, but Treasury bond prices could slip on the growing deficit, pushing up interest rates and yields. In equities, telecoms, U.S. energy and asset managers could benefit from continued deregulation.

Blue Wave (D President, Senate and House)

A prolonged recession could hurt Trump, with historically high unemployment in battleground states that elected him in 2016—particularly Michigan, Pennsylvania and Nevada—undermining his claim to economic stewardship. Voters turn to Biden and the Democrats as more trustworthy on healthcare reform and managing a possible COVID-19 second wave. Such a Democratic sweep could also lead to deficit expansion, driven by healthcare and infrastructure spending. However, the demand-side stimulus would boost economic growth, pushing interest rates and inflation higher. For U.S. equities, managed healthcare organizations, transportation, non-U.S. oil and natural gas, large-cap banks and consumer finance sectors could see gains, but healthcare reform may pressure pharmaceuticals. Increased regulation could also impact the tech sector, financials, net neutrality and environmental issues.

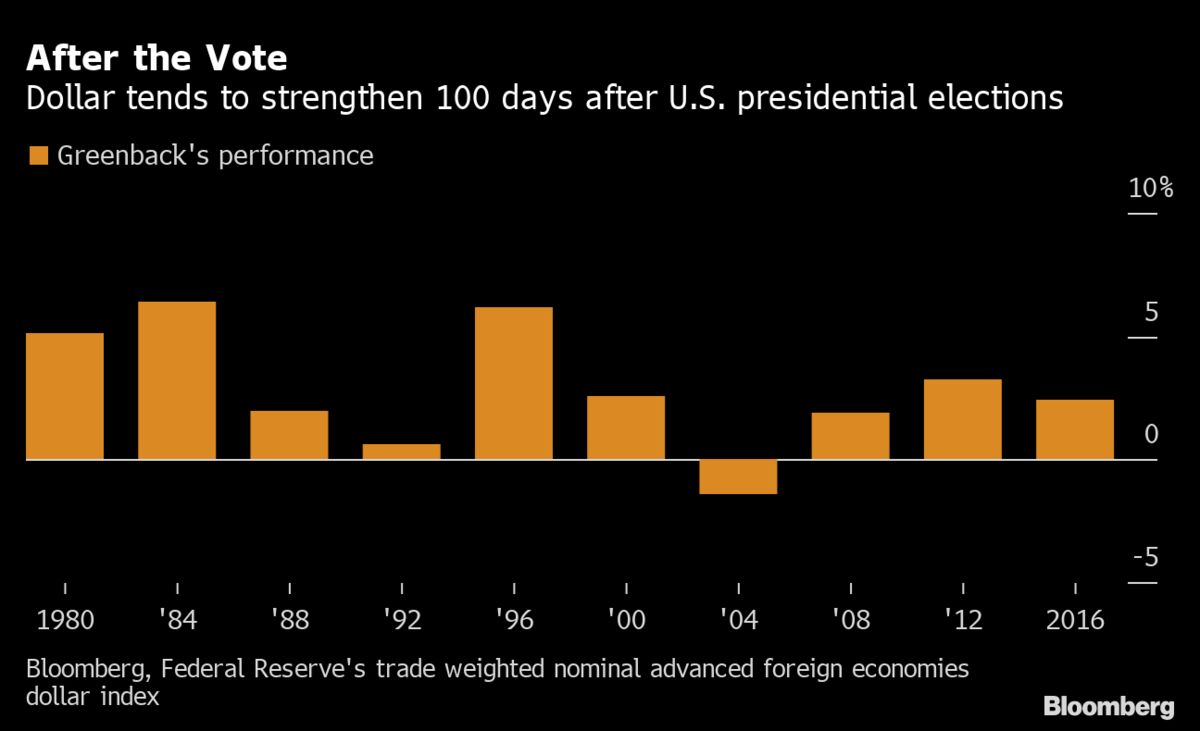

How might the dollar and global markets be impacted?

In recent newsletters, I've highlighted the influence that the value of the dollar currently has global investment markets, including equities, bonds and commodities.

Therefore the direction of the dollar across the US election will likely be important in dictating how global markets will react. History suggests that whatever the outcome the dollar will likely strengthen, which could be bad news for current momentum trends that are working right now. In other words, expect increased volatility.

What happens if the election result is contested

Perhaps the greatest unknown is what happens if the election result is contested, something that looks increasingly likely. With little historical precedent, it is uncertain how markets will react. Perhaps the closet comparison is the 2000 election when it took 6 weeks for George Bush to officially beat Al Gore following a recount of the votes in Florida.

Equity markets on both sides of the Atlantic fell with the S&P 500 down 6% in the two weeks after the election when the threat of litigation seemed likely. Equity markets don't like uncertainty which is one of the biggest risks of the 2020 US election.

Summary

So to sum up, many commentators think a Biden win could be bad for stocks, yet the historical evidence is mixed. A Democrat win is usually good news for stocks during the tenure of office but a change in Presidency may prove a drag on equity moves into the year-end. What matters more is whether we get a unified government or not. If we do then it could be positive for stocks no matter who wins, over the coming years. The outcome that would likely be the least palatable for markets is a unified Republican government. One thing that is almost certain is that volatility will pick up into the US election, especially if the dollar strengthens which it tends to do after an election. A lesson from history and in particular from 2016, is that the market volatility usually subsides quickly and often within fours days of an election result. The big unknown is what happens if the US election result is contested. If it is then markets are likely to react negatively in the short term, as they did in 2000 when they fell 6% in the two weeks after election day. However, history also shows us that ultimately it's the economic backdrop (and central bank policy) which is still likely to have the biggest sway over the direction of the stock markets in the US and globally both in the short term and during the next Presidential term. With so many unknowns, it is a brave person who tries to alter their portfolio to benefit from the US election. Those who are concerned may look to reduce their US equity exposure but it is a gamble that is uncertain to pay off.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay