The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was two-fold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance roundup: Still well ahead

My portfolio has continued to perform well while not taking excessive risks, as currently only around 50% of the portfolio is invested in equities. Since I started the challenge I have outperformed the market, passive portfolios and professionally managed multi-asset funds. I have produced a double-digit profit despite the various crises we have experienced including a Greek crisis, a Chinese economic slowdown as well as a commodity crisis and Brexit vote.

The table below shows that my portfolio has performed brilliantly since the challenge started in March 2015:

| Portfolio | % Return |

| Damien's £50,000 portfolio | 14.45 |

| Passive Vanguard benchmark | 9.95 |

| Average multi-asset fund manager | 6.46 |

| FTSE 100 | 5.46 |

Since last month's update my portfolio has given up a small amount of ground (0.34%) to the passive Vanguard benchmark which is in part reflective of my underweight in US equities which had a stable month. Overall the FTSE 100 has fallen 3.27% since my last update.

Fund changes

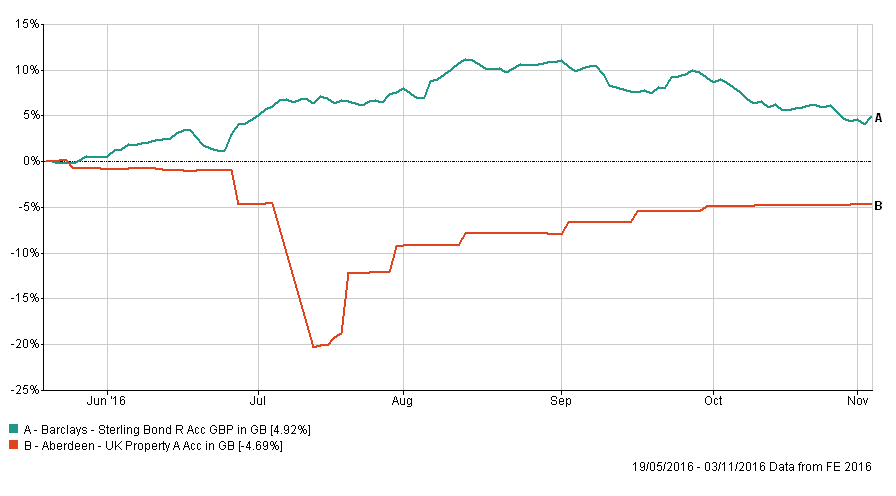

This month's changes are largely cosmetic with two 'like for like' switches. As I mentioned in my recent article (Bond funds for a bond bear market) October's bond market sell-off hit UK Fixed Interest pretty hard and my Barclays Sterling Bond holding took a hit. Fears over inflation, the positive outlook for the UK economy and concerns over the UK's credit worthiness meant that bond duration was punished (see last week's newsletter for more detail). Barclays Sterling Bond fell 4.23% versus an average of -1% for its peers. Yet that fall simply brought its returns back in line with those of its peer group. The chart below (click to enlarge) shows the performance of the Barclays Sterling Bond fund (green line) versus that of its peers (red line) since I've held it. If you recall I switched out of a property fund days ahead of the EU referendum and into the Barclays funds.

As you can see the Barclays fund has made a good profit for me and was up around 9% at the start of October. It's a great illustration of how bond duration was rewarded during the summer (something which everyone predicted would not be the case). There was no way I could tell that that would be the case (as it was counter-intuitive following the Brexit vote) but I simply followed the 80-20 Investor algorithm's selections. Interestingly the chart below shows what would have happened if I'd remained in the aforementioned property fund (the red line). As you know commercial property funds were hammered after the Brexit vote.

Nonetheless, the Barclays fund has this month dropped out of the 80-20 Investor Best of the Best (BOTB) and Best Funds by Sector (BFBS) lists so I am removing it from my portfolio.

The only other fund within my £50,000 portfolio that has fallen out of the BOTB and BFBS tables is Stewart Investors Worldwide Sustainability. It has marginally underperformed its peers, again in part because US equities have held up so well in the last few weeks. So I am replacing this fund with another globally diversified fund from the BOTB selection as it won't drastically alter my asset allocation but bring it back in line with the current BOTB's asset mix (which has reintroduced a small US exposure).

This week (and next) contains a series of events that could cause a spike in volatility. The interest rate decisions in the UK and the US have passed without too much fanfare. However, the Brexit court case defeat in the UK has thrown the cat amongst the pigeons and the US Election next week is the great unknown, especially as Trump is resurgent in the polls. Given the 'like for like' nature of the switches I could have waited until after the Election to action them in order to avoid any extremes in volatility that may arise. However, as I'm only making marginal tweaks (affecting just over 20% of my portfolio) any severe bouts of volatility will have limited impact. Besides, you can't market-time accurately, especially when investing in unit trusts. As it stands the market risks are perhaps poised more towards a market fall which would be in my favour during the fund switches, however it is in the lap of the Gods. All being well my fund switches will be completed ahead of the US Election announcement.

The table below shows my portfolio prior to today with the funds in red being those that are being removed:

| Fund | Sector | ISIN Code | % Allocation |

| IFSL - Brooks Macdonald Defensive Capital | Targeted Absolute Return | GB00B61MR835 | 8.61 |

| Threadneedle - Dynamic Real Return | Targeted Absolute Return | GB00BWWC6P48 | 5.9 |

| Henderson - China Opportunities | China/Greater China | GB0031860934 | 8.02 |

| Marlborough - European Multi-Cap | Europe Excluding UK | GB0001719730 | 13.85 |

| Invesco Perpetual - Asian | Asia Pacific Excluding Japan | GB00B8N44Q86 | 4.42 |

| BlackRock - Overseas Corporate Bond Tracker | Global Bonds | GB00B58YKH53 | 19.8 |

| Stewart Investors - Worldwide Sustainability | Global | GB00B845Y045 | 13.35 |

| Baillie Gifford - Japanese | Japan | GB0006010838 | 8.61 |

| Barclays - Sterling Bond | Sterling Strategic Bond | GB00B72Y6K08 | 8.81 |

| Franklin - UK Equity Income | UK Equity Income | GB00B7DRD638 | 8.63 |

Fund switches

Below I list my latest fund switches:

Switch 100% from Barclays Sterling Bond to AXA Framlington Managed Income

This is a straight like for like swap (both are Strategic Bond funds) with me favouring the AXA Framlington fund over the other Strategic bond fund within this month's BOTB because it fared favourably in my bond duration analysis whilst also having a lower cost and max weekly fall value.

Switch 100% Stewart Investors Worldwide Sustainability to Vanguard LifeStrategy 80% Equity

The Stewart Investors fund is useful as it has an unusually low US equity exposure. However, the BOTB selection (full analysis of the BOTB will be published in November's newsletter out on Saturday) has reintroduced some direct US equity exposure. Having said that the BOTB selection is still underweight US equities compared to the professional multi-asset funds. I've therefore chosen the Vanguard LifeStrategy 80% fund because it has some US exposure as well as a 20% bond exposure. The former adds a touch of risk ahead of the US election while the latter reduces it. However in the event of a Trump win all bets are off anyway as equity markets will likely sell-off across the board, volatility will spike and currency markets will react. The Vanguard fund has been a strong performer with incredibly low running costs and is globally diversified.

My new portfolio

New funds are in green:

| Fund | Sector | ISIN Code | % Allocation |

| IFSL - Brooks Macdonald Defensive Capital | Targeted Absolute Return | GB00B61MR835 | 8.61 |

| Threadneedle - Dynamic Real Return | Targeted Absolute Return | GB00BWWC6P48 | 5.9 |

| Henderson - China Opportunities | China/Greater China | GB0031860934 | 8.02 |

| Marlborough - European Multi-Cap | Europe Excluding UK | GB0001719730 | 13.85 |

| Invesco Perpetual - Asian | Asia Pacific Excluding Japan | GB00B8N44Q86 | 4.42 |

| BlackRock - Overseas Corporate Bond Tracker | Global Bonds | GB00B58YKH53 | 19.8 |

| Vanguard - LifeStrategy 80% Equity | Mixed Investment 40%-85% Shares | GB00B4PQW151 | 13.35 |

| Baillie Gifford - Japanese | Japan | GB0006010838 | 8.61 |

| AXA - Framlington Managed Income | Sterling Strategic Bond | GB00B6RPX228 | 8.81 |

| Franklin - UK Equity Income | UK Equity Income | GB00B7DRD638 | 8.63 |

My new asset allocation

My new asset allocation is shown below with my previous allocation is in brackets

- Global fixed interest - 24% (24%)

- US equities -6% (3%)

- European equities - 13% (16%)

- UK equities - 11% (10%)

- Japanese equities - 10% (10%)

- Other international equities - 0% (0%)

- Cash - 3% (5%)

- Property - 0% (0%)

- UK Gilts - 0% (0%)

- UK Fixed Interest - 9% (7%)

- Alternative assets/strategies - 11% (10%)

- Asia Emerging Equities - 9% (10%)

- Asia Equities ex Japan - 4% (5%)

You can see how this compares to the asset allocation for November's 2016 Best of the Best Selection above the table of this month's BOTB.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay