The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

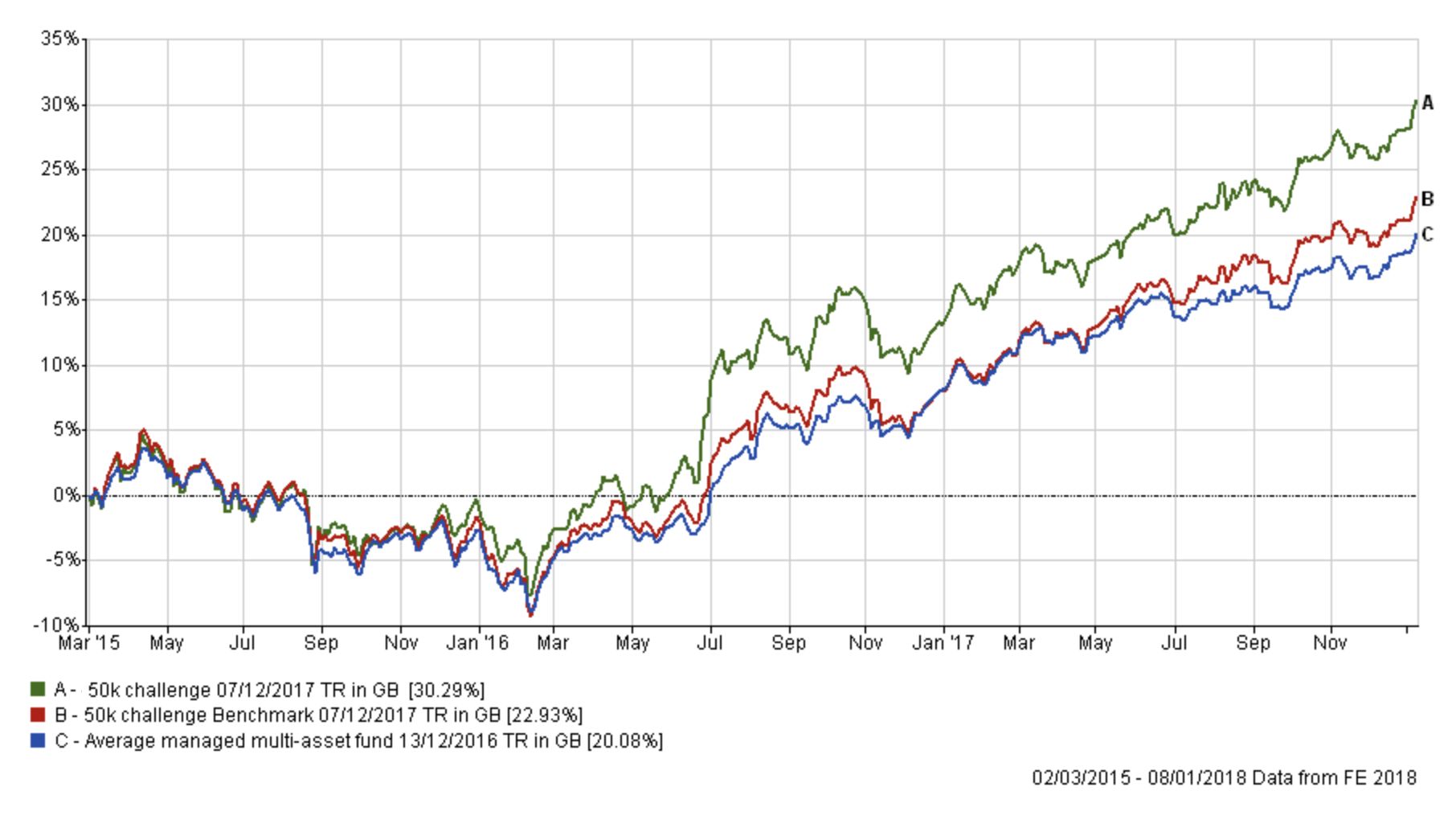

My portfolio has continued to perform extremely well while not taking excessive risks, typically around 50-60% equities. At present it has approximately 62% of the portfolio invested in equities which is the highest level for quite some time. I have produced over 26% profit despite the various crises we have experienced including a Greek crisis, a Chinese economic slowdown, a commodity crisis, Brexit vote, Donald Trump's surprise election win and the recent technology and Asian sell-off.

The chart below shows how my portfolio has outperformed since I started the challenge in March 2015. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm. At the time of writing, I have turned my original £50,000 into £65,145 which is a profit of 30.29%.

The table below shows my current portfolio, with those funds in green still in the BOTB while those in yellow are not in the BOTB but remain in the BFBS list. Meanwhile any funds in red have dropped out of both shortlists.

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code | SEDOL Code |

| 7IM US Equity Value | 13.8 | High | North America | GB00BWBSHX88 | BWBSHX8 |

| Baring Eastern Trust | 4.6 | High | Asia Pacific Excluding Japan | GB0000799923 | 79992 |

| F&C Property Growth and Income | 3.6 | Low | Property | GB00BQWJ8687 | BQWJ868 |

| Fidelity China Consumer | 6.6 | High | China/Greater China | GB00B82ZSC67 | B82ZSC6 |

| Man GLG Strategic Bond | 16.8 | Low | Sterling Strategic Bond | GB00B731HR48 | B731HR4 |

| Man GLG UK Income | 3.3 | Medium | UK Equity Income | GB00B0117B11 | B0117B1 |

| Neptune Japan Opportunities | 10.4 | Medium | Japan | GB00B3Z0Y815 | B3Z0Y81 |

| Premier Diversified | 18.8 | Low | Mixed Investment 40-85% Shares | GB00B8BJV423 | B8BJV42 |

| TM Cavendish AIM | 10.7 | High | UK Smaller Companies | GB00B0JX3Z52 | B0JX3Z5 |

| TwentyFour Dynamic Bond | 8.2 | Low | Sterling Strategic Bond | GB00B5KPRZ34 | B5KPRZ3 |

| Wise Funds Limited TB Wise Multi-Asset Growth | 3.2 | Medium | Flexible Investment | GB0034272533 | 3427253 |

The first thing that stands out is that the majority of my portfolio remains in the BOTB while Wise Funds Limited TB Wise Multi-Asset Growth and Man GLG Strategic Bond are the only funds that have dropped out of the BOTB and the BFBS sections. So looking at the portfolio there is no need for wholesale changes because so far 2018 has started where 2017 left off in terms of profitable investment trends. It is particularly good to see the F&C Property Growth & Income fund reappear in the BOTB following a strong December. You may recall that I decided to keep the fund in my portfolio despite its exclusion from BOTB last month. At the time I wrote:

"When a fund falls out of the 80-20 Investor fund lists it doesn't suddenly become a bad fund, don't forget the research behind 80-20 Investor allows for funds to be held for 6 months. Yet with December being such a short month, with trading desks closed during the Christmas holidays, I plan to look at my portfolio in January again once the dust has settled. With market volatility picking up and the outside chance of a Santa rally (fingers crossed) I don't want to make drastic changes right now, beyond those listed above. The F&C Property Growth and Income fund is a low risk fund so holding on to it for a few weeks is unlikely to be too painful, especially in a market where equities are taking a breather."

The fact that the F&C fund returned to the BOTB is testament to the fact that you do not need to knee-jerk react whenever a fund falls from the BOTB or BFBS. In a similar vein I plan to hold onto the Wise Funds Limited TB Wise Multi-Asset Growth for now despite it being highlighted in red above. The fund is a such a small part of my portfolio (around 3% just like the F&C Property fund) that any potential downside will have a limited impact on the overall return of my portfolio. However, the fund's performance since its inclusion in my portfolio last month has actually been very strong. The fund has made 4.34% in just 1 month with only my Asian and Japanese funds, along with Man GLG UK Income, outperforming it. While I don't focus too much on 1 month returns during that time it has also outperformed 8 of the 10 medium risk funds in the new BOTB list, one of which I already own. As we enter 2018 my portfolio as a whole is performing very strongly and therefore I am loathed to make too many alterations until a change in market direction, or period of poor performance, warrants it. In addition I am happy with the overall asset mix of my portfolio so it's a case of 'steady as she goes' for now.

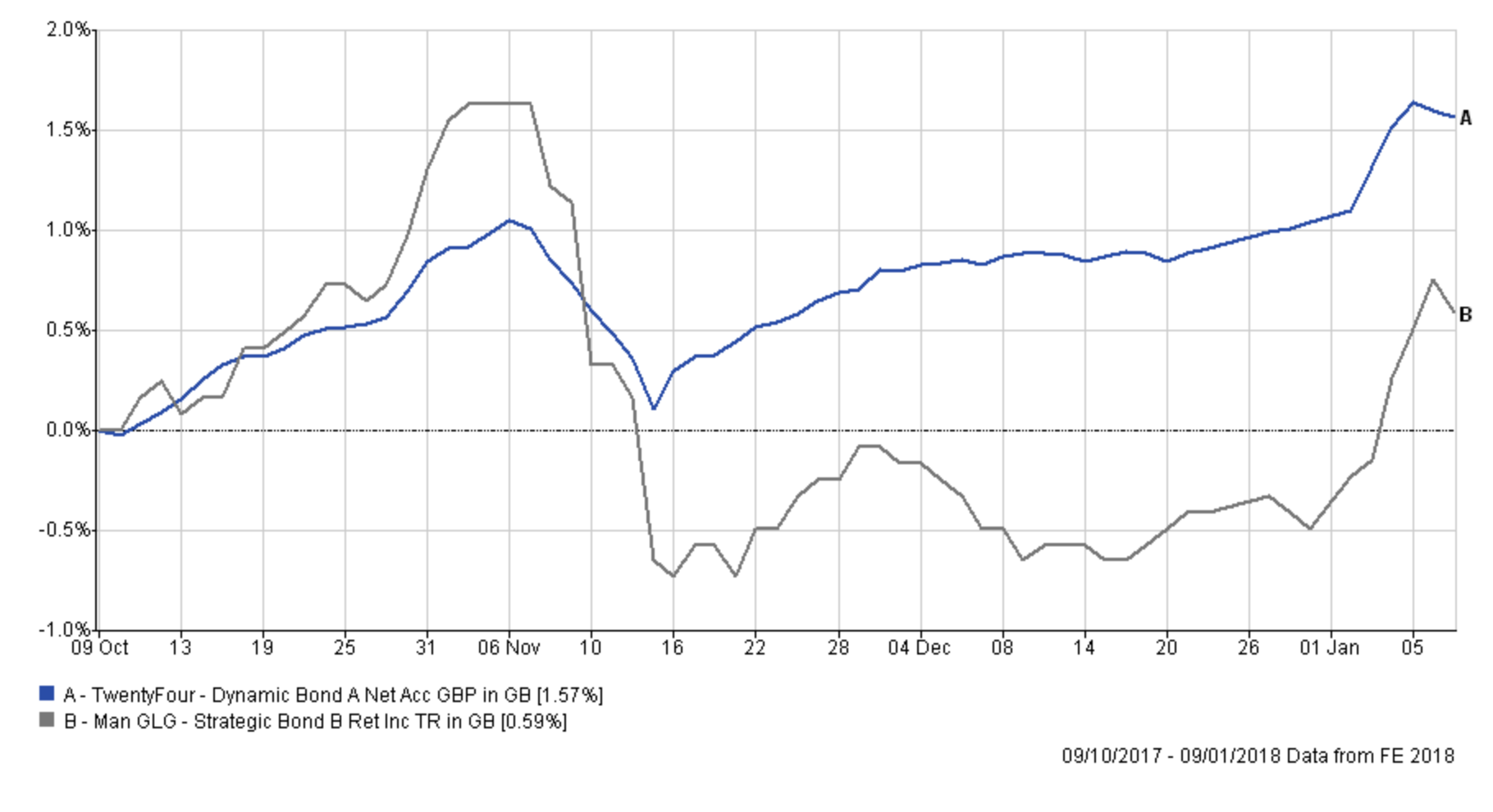

Having said that, the Man GLG Strategic Bond has been a regular in my portfolio for some time but has experienced a tough period in the last couple of months. The chart below shows the recent performance of the Man GLG fund versus the TwentyFour Dynamic Bond which is the other strategic bond fund in my portfolio. While the returns of the latter have been fairly unexciting at times, dull and steady it is what you need from a bond fund especially in the current environment.

Given that the fund is one of the largest holdings within my portfolio (it accounts for almost 17% of the portfolio) I am much more inclined to make a change given that it has now slipped out of the 80-20 Investor shortlists. The other reason is that bond markets have struggled as a result of a rise in inflation expectations and potential headwinds facing government bonds (namely central banks starting to unwind QE). Therefore I am keen to diversify the portfolio's bond exposure.

Fund switch

100% out of Man GLG Strategic Bond and 50% of the proceeds into Insight Global Absolute Return and 50% into TwentyFour Dynamic Bond

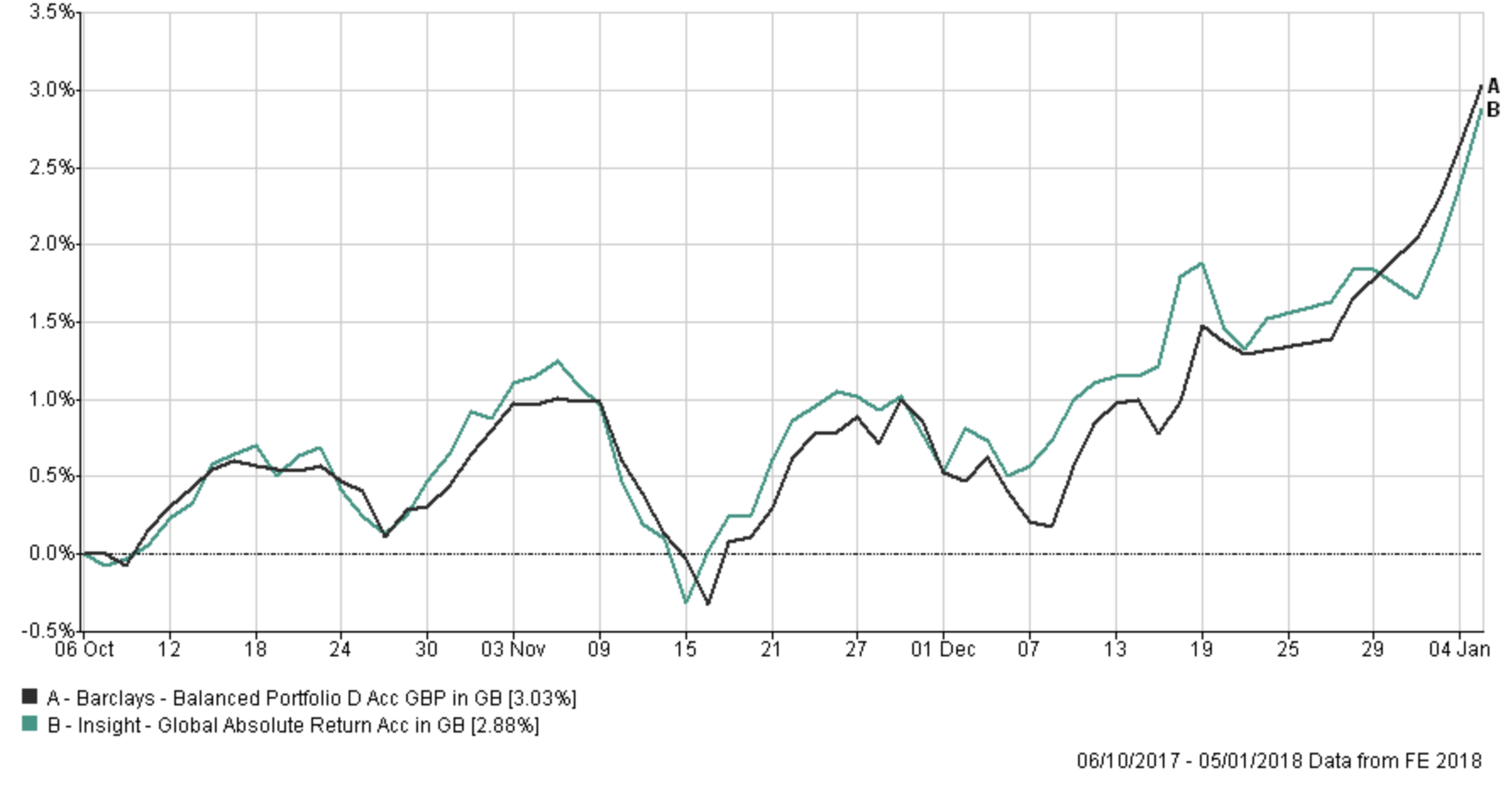

When switching out of the Man GLG Strategic Bond fund I was looking for a low risk alternative. As the chart above shows the TwentyFour Dynamic bond fund has exhibited a level of consistency in terms of performance, although it's not warranted an inclusion in the BOTB. However for the moment the fund remains in its respective BFBS list. By switching part of the proceeds into an existing fund it helps consolidate my portfolio and keeps the number of fund holdings constant. I considered investing the rest of the proceeds into the F&C Property Growth and Income fund due to its strong performance (and to diversify away from bonds) but it would have meant that I'd have over a 10% exposure to property. While not a problem in itself I try and not stray too far from the asset mix of the BOTB. So instead it became a decision between two low risk funds in this month's BOTB, namely Barclays Balanced Portfolio and Insight Global Absolute Return. Both funds invest in a range of assets including equities, bonds, property, commodities, cash and absolute return strategies. They also both tend to hedge out currency exposure which has been a positive in an environment where the pound has been strengthening. If I plot their performance there is nothing to choose between the two funds. The chart below (click to enlarge) shows the performance of both funds over the last 3 months. In the end I settled for the Insight fund because on the platform that I invest through the annual management charge is just 0.8%, exactly half that of the Barclays fund.

Overall I am only switching about 17% of my portfolio, nothing too drastic, and my new portfolio will look as follows with an equity exposure of around 65%:

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code | SEDOL Code |

| 7IM US Equity Value | 13.8 | High | North America | GB00BWBSHX88 | BWBSHX8 |

| Baring Eastern Trust | 4.8 | High | Asia Pacific Excluding Japan Ret | GB0000799923 | 79992 |

| F&C Property Growth and Income | 3.6 | Low | Property | GB00BQWJ8687 | BQWJ868 |

| Fidelity China Consumer | 6.8 | High | China/Greater China | GB00B82ZSC67 | B82ZSC6 |

| Insight Global Absolute Return | 8.2 | Low | Targeted Absolute Return | GB00B86R4N19 | B86R4N1 |

| Man GLG UK Income | 3.4 | Medium | UK Equity Income | GB00B0117B11 | B0117B1 |

| Neptune Japan Opportunities | 10.6 | Medium | Japan | GB00B3Z0Y815 | B3Z0Y81 |

| Premier Diversified | 18.8 | Low | Mixed Investment 40-85% Shares R | GB00B8BJV423 | B8BJV42 |

| TM Cavendish AIM | 10.6 | High | UK Smaller Companies | GB00B0JX3Z52 | B0JX3Z5 |

| TwentyFour Dynamic Bond | 16.2 | Low | Sterling Strategic Bond | GB00B5KPRZ34 | B5KPRZ3 |

| Wise Funds Limited TB Wise Multi-Asset Growth | 3.2 | Medium | Flexible Investment | GB0034272533 | 3427253 |

My new asset mix

This means my new asset mix is (previous asset mix is in brackets):

- UK Equities 19% (19%)

- North American Equities 17% (16%)

- Global Fixed Interest 13% (18%)

- Japanese Equities 11% (11%)

- Other International Equities 5% (9%)

- Asian equities 4% (4%)

- European Equities 0% (0%)

- UK Fixed Interest 6% (6%)

- Cash 4% (1%)

- Alternative Investment Strategies (including property) 13% (8%)

- Emerging Asia equities 8% (8%)

- Emerging Market Fixed Interest 0% (0%)

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay