The news comes just a day before the Bank of England’s Monetary Policy Committee (MPC) meets to make its final interest rate decision of 2025. With the jobs market cooling and price rises slowing, markets are now pricing in a high probability that the base rate will be cut from 4.00% to 3.75% tomorrow (Thursday, 18th December).

Inflation slows faster than expected

The fall to 3.2% offers a welcome boost to household finances and suggests that price pressures in the economy are easing more quickly than anticipated.

- Headline rate - CPI fell to 3.2% in the 12 months to November 2025, down from 3.6% in the 12 months to October 2025.

- Key drivers - The slowdown was largely driven by easing food and tobacco prices, and a moderation in transport costs.

- Core inflation - Core inflation, which strips out volatile energy and food prices, also edged lower, signalling that underlying price pressures are subsiding.

While inflation remains above the Bank's 2% target, the direction of travel is encouraging for policymakers battling to bring price rises under control without causing a recession.

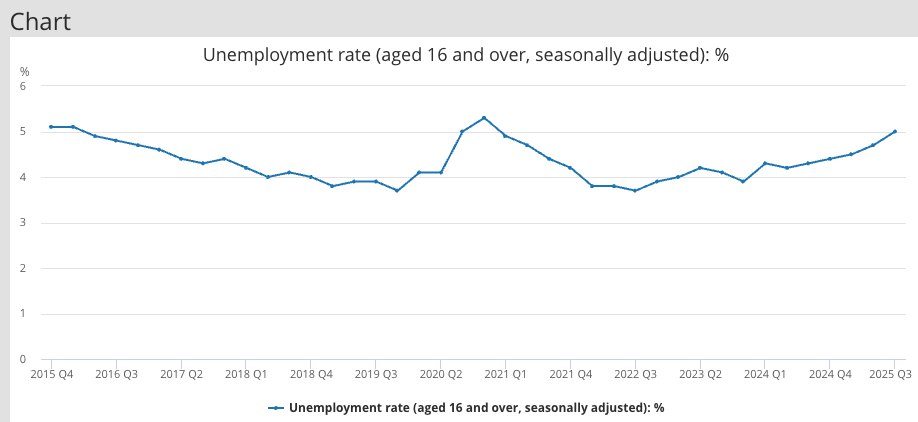

Unemployment hits post-pandemic high

While the inflation news is positive for the cost of living, the labour market paints a more concerning picture. The UK unemployment rate has risen to 5.1% in the three months to October 2025, up from 5.0% previously.

This confirms a steady upward trend in joblessness throughout the year, driven by a weakening UK economy. Employers have become increasingly cautious about hiring, citing fears surrounding the wider economic outlook and specific concerns regarding tax hikes, such as the recent increase in Employer National Insurance.

Why is unemployment rising?

- Hiring has slowed - The number of payrolled employees has fallen, with businesses putting off recruitment decisions.

- Rising costs - Higher taxes and wage bills have squeezed company budgets, limiting their ability to take on new staff.

- Youth impact - Young people are bearing the brunt of the slowdown. The Resolution Foundation warns that the number of out-of-work 18 to 24-year-olds has reached its highest level since 2015, as this group is often the first affected when employers freeze hiring.

Despite Artificial Intelligence (AI) dominating recent headlines, fuelling widespread anxiety about technology replacing human workers, it has not been cited as a factor in the current cooling of the jobs market.

Source: Office for National Statistics (ONS)

What does this mean for interest rates?

The combination of falling inflation and rising unemployment creates pressure on the Bank of England to lower borrowing costs. With inflation now closer to the target range and the jobs market clearly softening, policymakers may feel that keeping rates at 4.0% risks damaging the economy unnecessarily. A rate cut would help stimulate growth and ease the pressure on businesses and households. Most analysts now say that a 0.25% cut tomorrow is extremely likely, bringing the base rate down to 3.75%.

What it means for your money

The shifting economic landscape has practical implications for your personal finances:

- Mortgages - If the Bank of England cuts rates as expected, those on variable-rate or tracker mortgages should see an immediate reduction in their monthly payments. Fixed-rate deals, which have already been falling, may continue to edge down further as the market adjusts to the lower inflation outlook. We provide a roundup of the best mortgage deals on the market in our article 'Best mortgage rates in the UK'.

- Savings - A base rate cut typically leads to lower interest rates on savings accounts. If you have cash savings, you might consider locking in a fixed-rate now before the best deals disappear from the market. We provide a comprehensive list of the best savings rates in our article 'Best savings accounts in the UK'

- Job Security - With the jobs market becoming more competitive, now is a good time to review your financial resilience. You should aim for 3-6 months' worth of living expenses in an easily accessible emergency fund to cover you in case of unexpected redundancy. Check out our article 'Building an emergency fund - The what, the why and how'.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay