The proposed acceleration means that anyone born in the 1970s may need to adjust their retirement plans. However, the government has since clarified that an official State Pension Age Review is underway and no final decisions have been made. In this article, we explain the proposed timeline, who will be affected, and how you can prepare.

What is changing with the State Pension age?

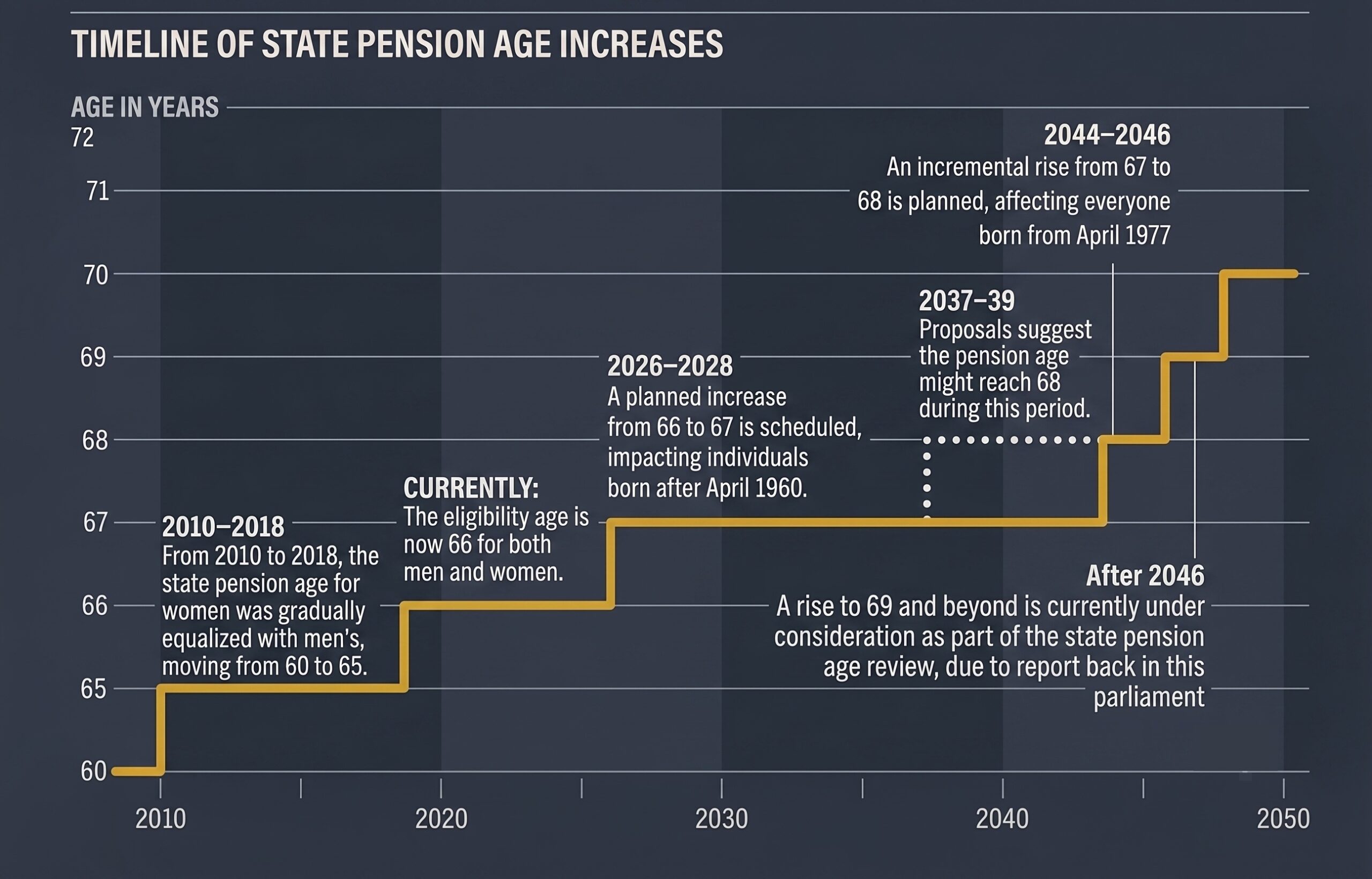

Under current legislation, the State Pension age is scheduled to rise from 67 to 68 between 2044 and 2046. However, the latest Fiscal risks and sustainability report from the OBR, published in July 2026, assumes a much faster timeline for its economic forecasts.

The report stated: 'The state pension age reaches 68 between 2037 and 2039, which the Government has confirmed is its current policy position rather than the rise to 68 happening between 2044 and 2046 as is currently legislated for.'

Despite the OBR's wording, ministers have pushed back against reports of an imminent, confirmed change. The government has clarified that no formal policy decision has been made and that an official State Pension Age Review is currently underway to assess life expectancy and system costs over the coming decades. While the accelerated 2037–2039 timeline remains a strong possibility for economic modelling, the exact schedule will not be confirmed until the review concludes.

Who will be affected by the changes?

If implemented, the accelerated timeline (shown in the chart below) will broadly impact people who are currently aged between 49 and 55. Under the previous legislation, the rise to 68 between 2044 and 2046 was set to affect anyone born after April 5, 1977.

However, bringing the date forward to 2037-2039 means a different demographic will be caught by the changes. Specifically, anyone born before 5th April 1977 could now find themselves having to work a year longer than they originally expected if they fall into this earlier window.

Missing out on one year of the State Pension can have a significant financial impact. One year of lost State Pension would cost individuals more than £16,000 by the time the change comes into force. For context, the full State Pension is currently worth £12,548.

Why is the State Pension age rising?

The government is facing significant financial pressure when it comes to funding the State Pension. The UK has an ageing demographic, which means a growing number of retirees are being supported by a relatively smaller working-age population.

According to the OBR, maintaining the current legislative timetable and delaying the rise to 68 until 2044 would cost the Treasury an additional £6 billion a year. Therefore, bringing the increase forward to between 2037 and 2039 is seen by policymakers as a necessary option to consider for the long-term sustainability of the State Pension system.

How to prepare for a later State Pension age

While the government has yet to conclude its review or pass the final legislation to officially change the date, it is wise to prepare for the possibility of retiring at 68. Below we provide some practical steps you can take to stay in control of your retirement planning:

- Check your State Pension forecast - You can easily check your expected State Pension amount and your current official State Pension age by using the free tool on the GOV.UK website.

- Review your National Insurance record - You typically need 35 qualifying years of National Insurance contributions to receive the full State Pension. If you have gaps in your record, you may be able to make voluntary contributions to increase your future payout.

- Track down lost pensions - If you have changed jobs frequently, you may have accumulated several small workplace pensions. Tracking these down and consolidating them can give you a much clearer picture of your total private retirement savings.

- Boost your private pension contributions - The State Pension is only intended to provide a basic foundation for retirement. Increasing your contributions to a workplace or personal pension now can help you build a larger pot, giving you the flexibility to retire earlier if you choose to.

- Consider your options - If you were hoping to retire earlier than 68, you may need to rely more heavily on your private pension savings or personal investments to bridge the gap until your State Pension payments begin.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay