The economic outlook for the UK has shifted dramatically since the start of March, changing what markets expect to happen with interest rates and inflation. At the start of 2026, financial markets were confident that the Bank of England (BoE) was about to cut its base rate, which would have lowered borrowing costs for millions.

However, the launch of missile attacks on Iran by the US and Israel, and Iran's subsequent retaliation, has caused the market to completely change its mind. Instead of preparing for imminent rate cuts, financial institutions are now pricing in the possibility of a rate hike later this year to fight off a new wave of rising prices (inflation).

Why are interest rate expectations changing?

In January 2026, inflation fell to 3.0%, and the BoE had already reduced the base rate to 3.75%. Because of this, financial markets believed there was an 80% chance the BoE would cut rates again at its 19th March meeting.

This positive outlook was derailed following military strikes in the Middle East. The immediate result was the effective closure of the Strait of Hormuz. This narrow waterway is vital for global trade, handling roughly 20% of the world's daily oil and seaborne liquefied natural gas (LNG).

The closure triggered an instant energy shock. Brent crude oil prices jumped by 29%, reaching a peak of over $119 a barrel on Monday before prices cooled to around $90 a barrel. This is still more than 20% higher than the price of oil prior to the start of the Middle East conflict.

How have financial markets reacted?

Financial markets use complex trading data, known as Overnight Index Swaps (OIS), to predict what the Bank of England will do next. Following the oil price spike, these predictions changed overnight.

- The market previously priced in an 80% chance of a rate cut in March 2026 which has now vanished entirely.

- Markets now believe there is a 99% probability that the BoE will not cut the base rate below 3.75%.

- Traders are now preparing for a scenario where the central bank has to actually increase the base rate to 4.0% to try and control inflation.

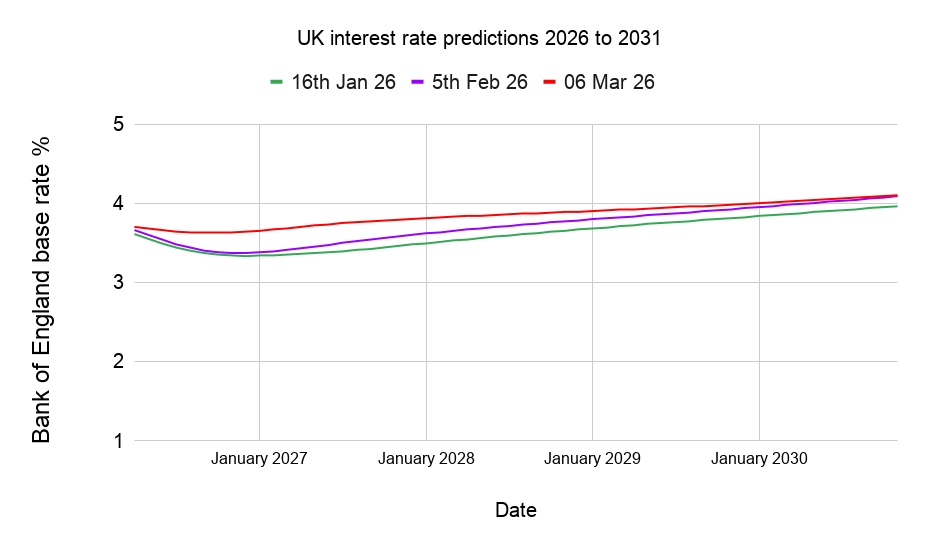

The chart below shows the dramatic shift in market expectations. Each line represents the market prediction, made on the stated date, of where the BoE base rate might be over the next five years. The red line is the latest prediction and you can see that the market believes that the base rate will likely rise towards 4.25% over the next five years.

What does this mean for your mortgage?

This sudden change in the financial markets has an immediate knock-on effect for high street borrowers, particularly those looking for a new fixed-rate mortgage.

In the UK, fixed-rate mortgages are influenced by the very same market predictions mentioned above (often referred to as 'swap rates'). When markets expect inflation and interest rates to stay higher for longer, the cost for banks to fund these mortgages goes up.

With a March rate cut no longer expected, major lenders including HSBC, Barclays, Nationwide, and Coventry Building Society quickly withdrew their cheapest mortgage deals.

- The average two-year fixed residential mortgage rate has reversed its downward trend and climbed to 4.87%.

- The average five-year fixed rate has also jumped, nearing the 5% mark to reach 4.95%.

Full details of the rise in mortgage rates can be found in our article 'Mortgage rates rise as Middle East conflict causes inflationary concerns' - along with what you should be doing now if you are due to remortgage in 2026.

Will inflation rise again?

The Bank of England's main worry is that higher energy costs will push up the price of everyday goods and services. Experts at Oxford Economics estimate that the energy shock alone, if it continues, will add around 0.5% to 0.6% to the UK's headline inflation rate by the end of the year. If the situation worsens and natural gas prices double, economists warn it could push inflation back above 5.0%.

This pressure is being made worse by a secondary crisis in global shipping.

- Commercial cargo ships are being forced to take a much longer route around the southern tip of Africa, adding 10 to 14 days to their journey times.

- Insurance costs for ships operating in the Middle East have skyrocketed, jumping from 0.25% to up to 1% of a ship's total value.

- These massive extra transport costs are already being passed on to UK importers, which could eventually mean higher prices for consumers at the checkout.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay