Since then, the odds of a cut have dropped to just 25%, and may fall even further as more key parts of the UK's energy supply chain come under threat and the full extent of the inflationary fallout takes shape.

Simon Gammon, managing partner at Knight Frank Finance, said: "The outlook for activity and rates appeared relatively benign only last week, but conflict in the Middle East has introduced fresh uncertainty. Any spike in oil prices could fuel global inflation or, at the very least, prompt central banks, including the Bank of England, to delay further rate cuts until the outlook becomes clearer."

Will there be a rate cut this month?

The expectation had been that there would be a cut to the base rate this month, with one or two more to follow in the next 12 months. However, market expectations have shifted dramatically in the last few days to the extent that just one rate cut is now anticipated this year, possibly coming as late as November.

Some are even warning that, with the ten-year gilt yield soaring above 4.5%, there could be a repeat of the 2022 energy crisis, when prices surged, and the base rate was hiked to 5.25% following the Russian invasion of Ukraine.

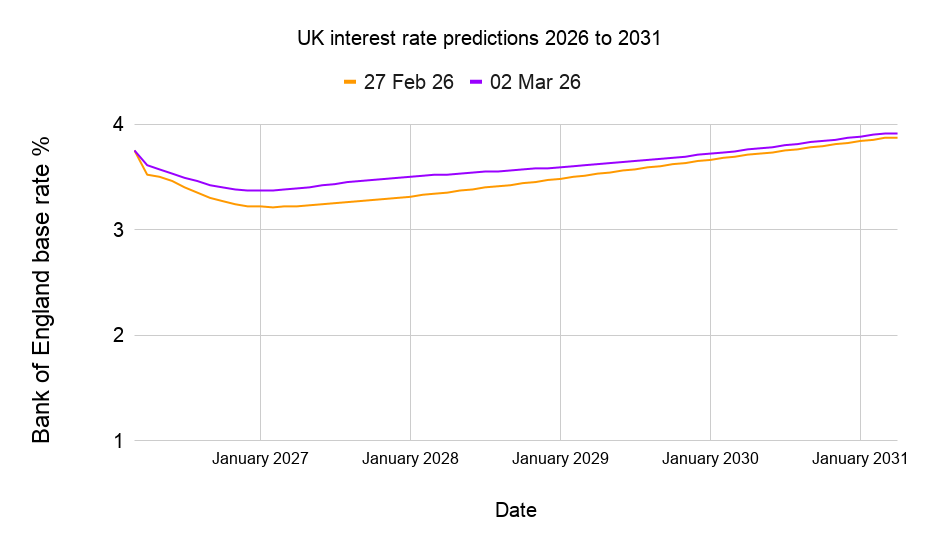

You can see from the graph below how sharply predictions on the future of UK borrowing have shifted in less than a week.

Why are rates no longer expected to fall?

The Bank of England uses the base rate to influence inflation in the UK. If inflation is too high, the Bank can raise or hold interest rates to curb consumer demand in an effort to restrict price rises. If inflation is too low or the economy is struggling, the Bank can slash rates to stimulate spending.

When rates are expected to fall, as they have this Spring, it is usually because there is something of a consensus that inflation is on a consistent downward trajectory towards the Bank's 2% target, and attention can turn to boosting the economy through cheaper borrowing.

However, just as inflation in the UK seemed to be set to dip below the Bank's target, costs for UK consumers seem set to rise once again as global gas and oil prices have risen significantly due to military action in the Middle East.

How will conflict in the Middle East impact UK prices?

This area of the world is key to the global fuel and energy market, both in terms of how it is generated and how it is transported. Crucial pieces of energy infrastructure across the Gulf states were targeted by Iran this week, including the world’s largest LNG (liquified natural gas) export plant in Qatar and a vast oil refinery in Saudi Arabia.

Meanwhile, shipping through the Strait of Hormuz, which would usually see 20% of the global oil supply passing through, has effectively stopped after tankers were warned by Iranian forces that they would be targeted.

So with processing plants, shipping lanes and production sites restricted, the cost of generating and moving key materials is skyrocketing. These costs will ultimately hit UK consumers' pockets as petrol prices rise and energy costs increase, though the Energy Price Cap will offer some short-term protection.

Once the increased cost of fuel, gas and electricity (plus higher travel costs driven by airport closures in the region) pushes up the headline rate of inflation in the UK, it will likely encourage decision-makers to avoid rate cuts.

Chris Beauchamp, chief market analyst at IG, said: "The huge bounce in European natural gas prices threatens to upset the more positive outlook for UK inflation and consumer spending.

"Hopes that pricing pressures would ease and consumers could spend more could be dashed as a price spike similar to 2022 causes a major headache for both policymakers and consumers, potentially disrupting the plan for more UK rate cuts."

How would higher inflation affect mortgages?

The odds on a March cut to the Bank of England base rate are now looking unfavourable, though there is still a 25% chance. A base rate cut would be great news for anyone looking to remortgage or buy a home in the coming months, as mortgage rates tend to follow the base rate's trajectory, though expected interest rate cuts are usually priced in ahead of time for fixed-rate deals.

Based on a loan-to-value ratio of 60%, the lowest two-year fixed-rate mortgage deal on the market currently comes in at 3.55% and the best five-year fixed-rate mortgages offer rates from 3.75%. Those looking for a two-year tracker deal can find rates as low as 3.86%, while the best five-year tracker deal is 4.35%. The top deals can be found in our regularly updated article, 'The best mortgage rates in the UK'.

If you are unsure about the best type of mortgage for you, read our article 'Remortgaging in 2026', where we examine whether now is the right time to fix your mortgage rate.

What does inflation mean for savers?

High inflation is bad news for savers. It is easy to assume that high inflation leads to higher interest rates and better returns on your savings, but that does not always work out in practice. While it is true that inflation remaining well above the 2% target means that the base rate of interest could be maintained higher for longer, high inflation is still bad news.

Firstly, banks often take much longer to pass on rate rises to savers than they do to borrowers. This means it can take a long time for high inflation figures to translate to a boost in the interest rate on your savings. Most importantly, inflation erodes the value of cash, so your money in the bank will buy you less as the cost of living goes up.

Slowing inflation is better news for savers, as what you have put away should hold its value for longer, even if it triggers a rate cut that reduces the headline interest on your account. You can find the best savings accounts in our article ‘Best savings accounts in the UK’.

What to do if you are struggling to pay your bills

Many essential household costs are still on the rise and could be set to go even higher. Food bills are going up, energy costs could be set to soar and many household incomes are not keeping pace with the cost of living. However, there is help available if you are struggling.

If you think you might fall behind on your household bills, the best thing to do is to reach out to the relevant supplier in the first instance. If you explain your situation, there will typically be steps they can take to help you come up with a payment plan that works for both parties.

It's also a good idea to make sure you are claiming all of the support you might be entitled to. You can check your eligibility for various benefits through the website entitledto.

We also have several articles that may be more specific to your situation and could offer further help:

- How to save money on your energy bills

- How to save money on your water bills

- How to save money on your mortgage

- How to save money on your council tax

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay