Investing is a long-term game and you shouldn't obsess about short term fluctuations. After all, that is the founding principle on which 80-20 Investor was built - Empowering to maximise your returns from minimal effort.

The power of momentum investing is irrefutable, as countless academic papers will testify (see our FAQs section), and our own 80-20 Investor research enables DIY investors to harness it's power and apply it to unit trusts, ETFs and investment trusts. But not just that, our unique stop loss alerts aim to help those concerned about losing money avoid severe market crashes. You can find more information about how they work in our short video here.

Putting our bespoke qualitative research aside, and focussing on our 80-20 portfolio and stop loss alerts how did they fare during the market sell-off in the Autumn?

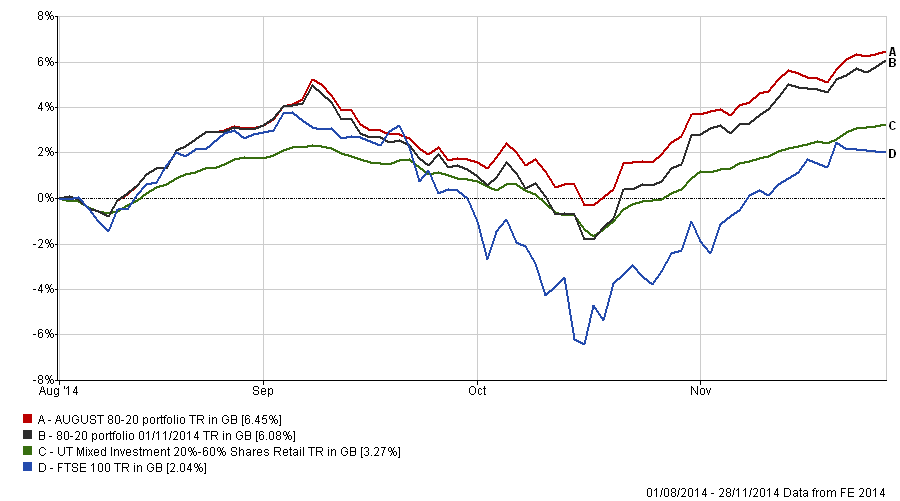

Buy & hold

Let's say you bought every fund in the 80-20 Portfolio in equal proportion on 1st August 2014. Now let's say you went on holiday for 4 months, not bothering to review your funds during that period (even when you received stop loss alerts). That is the beauty of 80-20 Investor, it is versatile and fits around your life. So how would you have done compared to the average managed fund (shown in the chart as the Mixed 20%-60% sector average)

You'd be 6.45% up versus 2% or 3% from the market or the average active fund manager. Not bad! So for your £3 a week 80-20 Investor subscription you'd would have made £6,450 if you'd had invested £100,000. Plus you were almost always in profit!

Monthly switching

While it is down to you to review your funds as frequently or infrequently as you wish (I suggest you do it at least every six months) how would you have done if you'd always bought the 80-20 Portfolio each month.

Now you can see that you would still be up over 6%, or £6,000 on £100,000!

What is interesting is how the black line (the monthly switching of your portfolio) took off once the market turned in mid-October. The point to take from this is that you can not market time yet the point of 80-20 Investor is to limit the influence on your returns. As can be seen by both 80-20 strategies performing well.

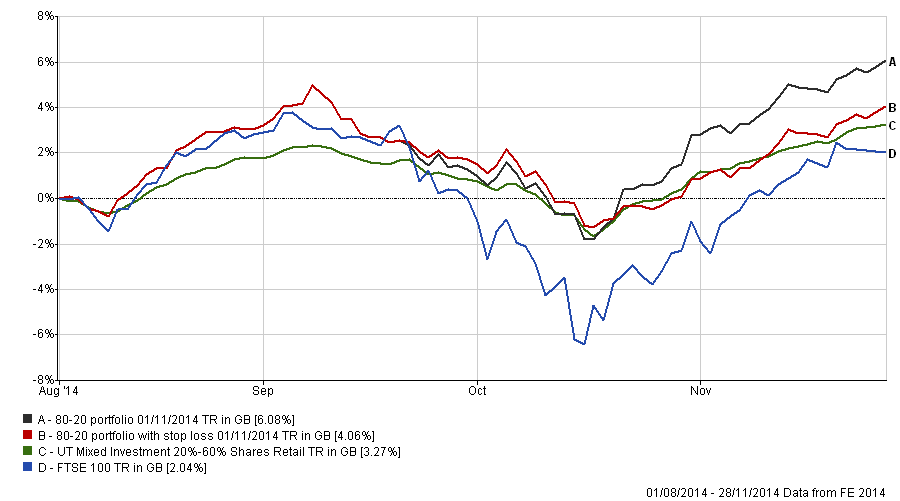

Impact of the stop loss alerts

Now obviously regularly switching money can increase volatility as you ride the latest trends. Our stop loss alerts for those employing this strategy aim to limit the downside in a market sell-off. So how did someone who used them do during the market sell-off in September/October do?

The red line now represents what would have happened if you'd bought the 80-20 Portfolio and sold funds when you received stop loss alert emails. Up until mid September the 80-20 Portfolio (in black) and the 80-20 Portfolio with stop losses applied (in red) perform identically as the market is rising. On the graph the black line is under the red line at this point (hence why you can't see it). Then when the market sell-off begins the red and black lines diverge.

The key points to note:

- The stop loss alerts would have put the 1/3 of YOUR portfolio in cash by mid-October to protect you from a severe market sell-off

- It preserved capital better than the straight 80-20 Portfolio during the sell-off.

- The stop loss version still outperformed the average managed fund (in green) over the period

Interestingly someone who had applied the stop losses would have seen their portfolio move from fully invested (i.e no cash) in mid September to having 1/3 of their portfolio in cash by mid October. Had the market continued to sell-off then the stop losses would have continued to reallocate to cash and the red line would have outperformed all the others. But when the market realised that the sell-off was over, and a more severe correction was not about to occur, then the market started to rise. The red line then marginally underperformed the average managed fund (green line) until the start of November when 80-20 Investor would have become fully invested again, once the sell-off was behind them. Then, somewhat inevitably they outperformed the market again.

Obviously past performance is no guarantees to future returns. However, I wanted to show you the warts and all charts to give you an insight into the power of 80-20 Investor and how I personally invest money.

The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay