Stagflation - a portmanteau of the terms “stagnant” and “inflation” - refers to an economic pattern when inflation is high or increasing despite high unemployment and slow economic growth. After the reflation trade in the spring (which I discussed in an 80-20 article earlier this year), optimism over the global economic rebound post-COVID started to falter. By May there was increasing concern that economic growth would start to slow, partly a result of economic supply constraints which are a legacy of national lockdowns, but also due to rising Delta variant cases around the world. Yet at the same time aggressive quantitative easing has meant that investors have started to worry that signs of rising inflation won't be transitory, despite most central banks insisting that they will.

Recent figures from the Office for National Statistics showed that UK unemployment reached 4.7% in August - 0.8% higher than before the pandemic - while analysts hold firm on their expectation that inflation will reach 4% by the end of the year. If economic growth continues to slow then a stagflationary environment becomes more likely.

Perhaps it should be unsurprising that in recent weeks (and months) there have been signs that some institutional investors are starting to position their portfolios to potentially benefit from a stagflationary environment, certainly in developed economies in the West.

Investing in a stagflationary environment requires an attitude change. A stagflation-proof portfolio will usually have some exposure to physical assets which historically weather economic turbulence well. Precious metals, for example, tend to perform well in stagflationary environments. Gold, in particular, rocketed during the 1970s stagflation crisis in the US, rallying from $100 in late 1976 to around $650 by 1980 - that’s a 550% increase in just 4 years, at a time when US inflation was at an eye-watering 13.5%. Much has changed since the 1970s, but with gold’s less-than-stellar performance over the previous quarter, some believe that the yellow metal is due a resurgence.

Stagflation can also be good news for assets that track inflation - like inflation-linked government bonds (sometimes called index-linked bonds). The bonds' capital value and income payments are designed to move in line with inflation which means that demand for them tends to increase during stagflation scares. For example, Legal & General’s All Stocks Index-Linked Gilt Index, which tracks a number of government-backed bonds linked to inflation, has risen almost 8% in the year-to-date.

In terms of equity sectors, utilities and Real Estate Investment Trusts (REITs) tend to weather stagflation better than other sectors. Schroders published research on US equity sector performance in high (3% on average) and rising inflation environments between 1973 and 2020, and found that REIT stocks outperformed inflation 67% of the time and posted an average real return of 4.7%. The reason this happens is that price rises typically filter through to the value of properties, even when unemployment rates are high. REITs can also generate generous dividends. The average annual return, according to the MSCI U.S. REIT Index, was 10.32% as of June 2021.

Large-cap technology stocks can also be a surprising stagflationary option for shrewd investors. In a stagflationary environment, it can be difficult for central banks to raise interest rates, for fear of sending the domestic economy into a recession, something that happened in the US in the 1970s. Low-interest rate environments tend to be positive for technology stocks as often the lion's-share of their projected earnings are far off into the future. When interest rates are low then the discounted value of these earnings into today's money (which is ultimately what a share price is) is therefore higher.

Healthcare stocks have also proven to be good inflation hedges, as demand for medicine and healthcare services tends to be resilient when economic growth slows.

Obviously, the above suggestions are not hard and fast rules and there is no guarantee that the aforementioned assets will outperform sectors that have historically struggled during periods of stagflation, such as financials, materials and consumer discretionaries (as opposed to consumer staples) if we see stagflation in the near future. However, it is worth paying attention if history is to be our guide.

Funds for the stagflation trade

How would you go about trying to build a portfolio which might weather a stagflationary storm. Yes, you could start with the above commentary as a basis but then you would need to trawl through every fund to try and find out their percentage exposure to different fund sectors. Not only is this information not readily available but it isn't searchable at scale, not even on sites such as Morningstar.

There is the added complexity that not all economies behave in unison, you could have a stagflationary environment in one economy while having a full-blown recession in another. Add to that the fact that recognised periods of stagflation have often existed in the distant past it is difficult to back-test funds, as most didn't exist at the time.

However, we can try to apply a similar approach as to that used in the reflation trade research piece to at least gain some insight into the funds that might benefit. The chart below shows the 10 year US treasury yield, which you will recognise from recent newsletters.

The reflation trade really began to break down in May, but accelerated on the 25th June when the 10 year US treasury yield hit the upper downtrend line and then crashed to its recent low. While inflation expectations remained elevated, concerns started to rise over the possibility of slowing growth. Of course, there will have been other factors that have impacted bond and equity markets during this period. Also it wasn't explicitly a period of stagflation, so funds with exposure to some of the traditional stagflation beneficiaries won't necessarily have topped the performance charts during the timeframe. But during the time period some of those sectors, mentioned earlier, showed signs of outperformance and started rising to the top.

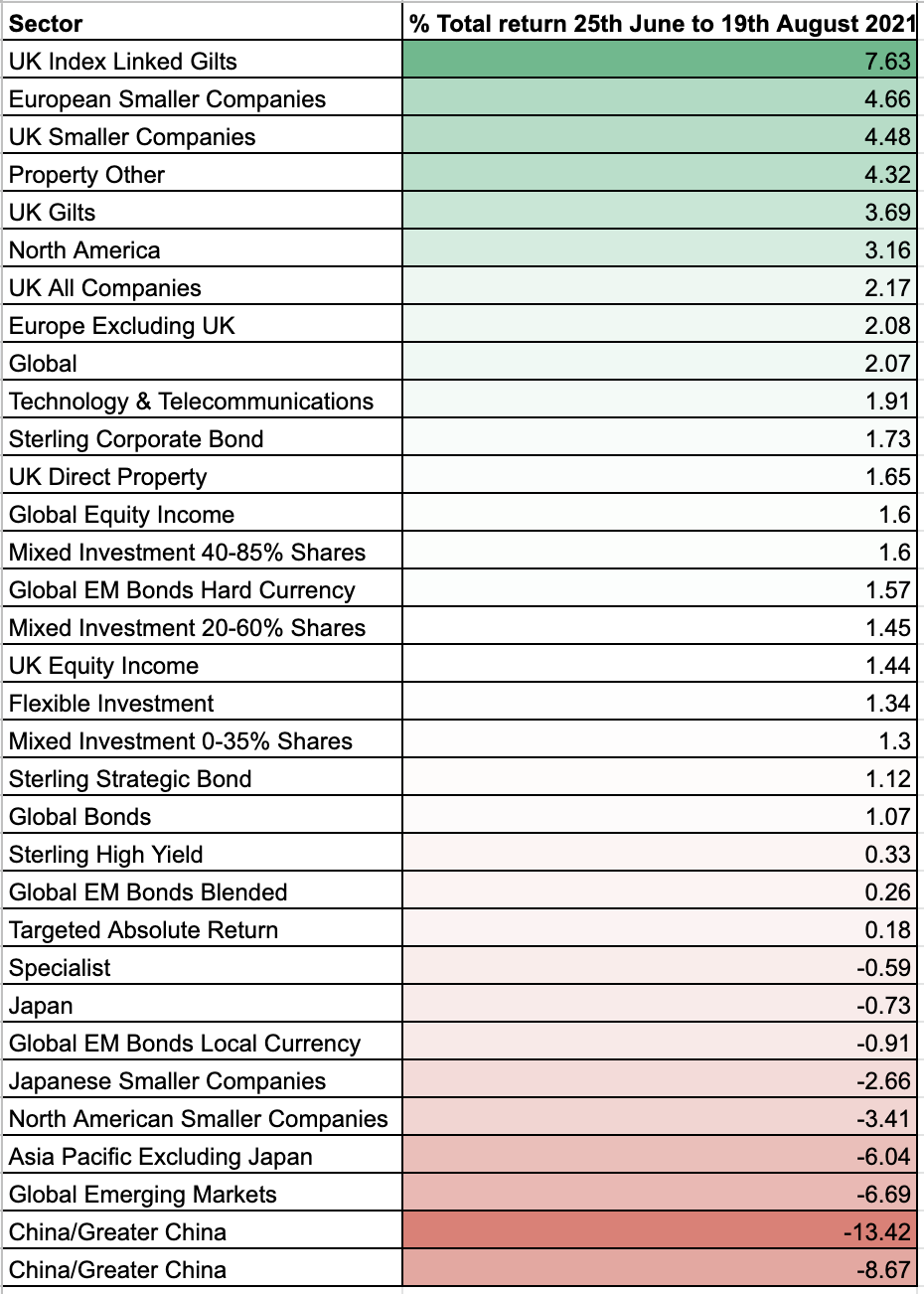

If we use the period 25th June to 19th August when bond yields were falling despite rising inflation, and determine the average percentage return from each unit trust sector it provides an interesting table (click to enlarge):

You can see that UK Index-linked Gilts are top, with Property Other (REITs) sitting in fourth. We also see UK Smaller Companies, North American equities and Global equities near the top. The latter two are often quasi big-US tech funds. Technology & Telecommunications sit 10th. So the result backs up what we might expect to see given my earlier commentary. It suggests that there are tentative signs that stagflation trades have started to gain some traction. However, within each sector, there will be nuances as no two global funds are alike.

Interestingly Asian equities are the biggest laggards, which is partly a reflection of economic growth concerns and partly a result of central banks looking to tighten monetary policy.

So focussing on Western economies, where concerns/signs of stagflation are more evident, I have compiled shortlists of potentially the best and worst stagflation funds based on their performance during the aforementioned periods. These lists can give you a starting point of the funds to look at and the ones to then scrutinise what they are invested in. So for example, the Schroder Global Recovery fund makes the "avoid" list. If you look at its portfolio it is focused on Financials and Consumer Discretionaries.

Click on the links to download the pdfs. The tables are colour-coded like a heatmap with the best performers in dark green and the worst in dark orange.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay