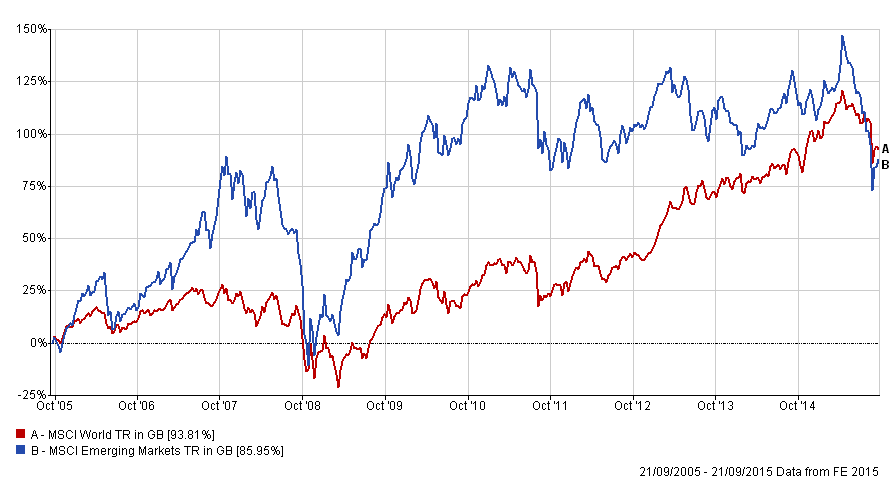

It's a brave person that invests in emerging markets right now. The chart below shows how emerging equities have performed versus their developed word counterparts in recent history.

Emerging market equities vs developed world equities over the last 10 years

Emerging market equities vs developed world equities over the last 5 years

Emerging market equities vs developed world equities over the last year

A year or so ago, if you had asked a bunch of investment commentators to pick a long term investment play most of them would have picked funds with an emerging market bias. If you consider the long term fundamentals of emerging markets the argument for investing in them stacks up. They have huge untapped populations with youthful demographics, unlike the west where rapidly ageing populations mean fewer workers which is bad for economic growth. Add to that the increasing consumer wealth as millions are lifted from poverty as emerging countries develop economically. Unsurprisingly emerging markets have long been heralded as future drivers of global economic growth.

Yet the promise of strong future growth doesn't always equate to strong investment returns, as shown by the charts above. If you look at the 10 year chart you can see that emerging market equities massively outperformed developed world equities after the financial crisis. That reflects the fact that emerging markets tend to outperform after a crisis, but perform badly during it.

Why have emerging markets underperformed recently?

During the last 4 years, and especially over the last 12 months, emerging markets have lagged developed world equities. The reasons for this include 1) concerns over global growth, 2) the prospect of interest rates rising in the West plus 3) the amount of money printing (known as QE or Quantitative Easing) that has occurred in the developed world.

If we start with global growth concerns first, generally speaking emerging market economies often export commodities or products to the rest of the world. A slump in global growth will mean a fall in demand for emerging world exports and a fall in their economic output. This inevitably hits their stock market as the earnings prospects of their exporters are hit. For example, if you are an emerging country which exports a lot of oil then if global growth slows the demand for oil will also fall. Less products will be bought meaning less goods need to be transported which leads to less demand for petrol. But it also means less demand for all the products that refined oil is needed to make.

Then there is QE, money printing, by developed world central banks. 80-20 Investor members will know by now that when central banks print money out of thin air it works its way into risky assets (such as equities) and drives the market up. That's exactly what drove the developed world equity outperformance since the financial crisis.

We've also had 5 years of trying to guess when interest rates in the developed world (particularly in the US) will go back up. The problem is that when/if interest rates go back up in the US it means that holding the dollar or other dollar denominated assets becomes comparatively more attractive to everything else. So money tends to flow back from risky emerging markets (where investors were chasing better returns) back home to the US (where the returns on cash and low risk investments now look better). It's akin to suddenly deflating a balloon and so emerging market equities suffer as demand for them starts to evaporate.

The last 6 months have been a perfect storm for emerging markets as you can see by the downturn on the 1 year graph. Concerns over Chinese and therefore global growth has caused a commodity slump (i.e oil) at the exact same time that the US are thinking of raising interest rates for the first time in nearly a decade.

One emerging market worth looking at?

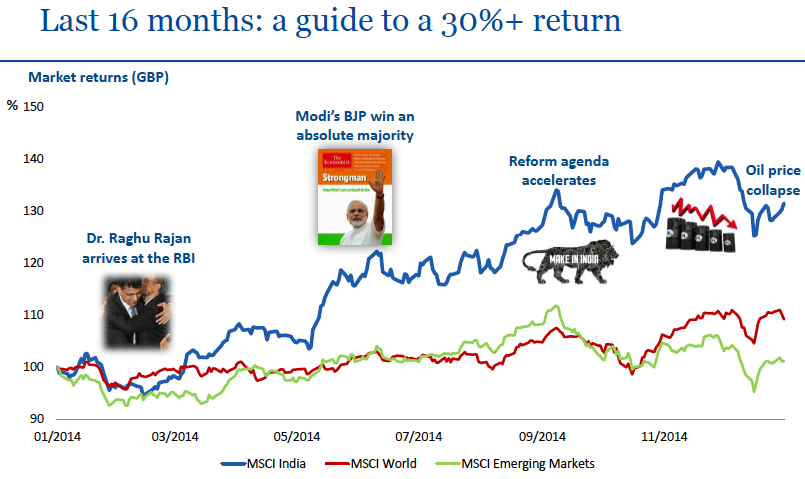

The chart below (click to enlarge) shows how India's stock market (the orange line) has performed versus the MSCI World Index (blue line) & the MSCI Emerging Markets Index (green line) over the last year.

Clearly while India is not immune to the negative sentiment surrounding emerging market equities it has fared better than many of its peers. Or in other words emerging markets are not a homogeneous group as Indian equities are not tightly correlated to either developed or emerging market equities. So why is India so different?

Why has India fared better than other emerging markets?

The chart below brilliantly sums up the sweeping changes that have occurred in India's political and financial system over the last 18 months. In 2014 India elected a majority Government for the first time in 30 years with Narendra Modi at its head. It was heralded as a watershed moment with the hope that the new Government, with its pro-growth agenda, would be able to pass new legislation and even amend the constitution of India to drive economic growth. Both of these were seen as good news for economic reform prospects. What is seen as good for future economic growth can bleed over into buoying the stock market. The market was certainly banking on the prospects of economic reform as can be seen by the steep bounce in the Indian stock market (the blue line) just before Modi won the election.

But delivering on that promise has been easier said than done, despite Modi’s majority, as there were the usual obstacles of India's state governments potentially impeding future infrastructure projects. India's politics is a messy tangle of inter-state politics with each elected State historically putting self interest over national unity. Reform is never easy, but as can be seen from the above chart, as the pace of reform accelerated so did the Indian stock market.

Falling oil is positive for India

While other emerging markets are struggling with falling commodity prices, particularly the fall in the price of oil, India is different. India imports 80% of its oil, so is unlike other emerging markets that are net exporters rather than importers.

Consequently a low oil price could be game changing for India, providing an additional economic boost. Analysts estimate that if oil stays at around $50 a barrel it will boost economic growth by 1% a year (India's economy currently grows at an eye-watering rate of around 7.5% a year). In addition the Indian Government currently subsidises the price of oil in order to stop high oil prices hampering the Indian economy. If the price of oil remains low then then the size and need of any Government subsidy will reduce. That money can be then used more effectively elsewhere to further boost economic growth.

On top of that with the price of oil so low it keeps a lid on inflation in India. If inflation remains low then that gives scope to the Reserve Bank of India to reduce interest rates if need be, for example, to drive economic growth. If inflation was high then the central bank would have to increase interest rates in order to get inflation under control which in turn would slow economic growth. But India does not have this problem. In fact India is likely to enter a period of accommodative monetary policy which is good for equities.

Outlook for India

Clearly investing in India is an indirect bet on a low oil price given its position as a global consumer rather than producer. If you believe the price of oil is about to rocket then clearly you wouldn't necessarily want to be left holding Indian equities. Yet beyond the impact of the price of oil there are a number of other economic factors that make India an interesting proposition. Over the last 3 years Indian companies on the whole have been getting their financial houses in order. This period of consolidation has meant that there is spare capacity in the economy. Companies remain prudent with the capital they spend meaning greater profit margins and earnings. This can only be good news for shareholders. So a positive growth backdrop, a central bank able to oil the wheels of the economy (if need be) and improving prospects for return on capital employed by Indian companies makes their equities appealing and has helped support their stock market over other emerging markets.

From a political viewpoint, the much needed reforms are taking shape in the background . As mentioned earlier, the self interest of individual state governments within India have previously stood in the way of reform. For example much needed infrastructure projects have been held up. However, Modi has tackled this by giving individual Indian states more autonomy which has led to states wanting to be more competitive, particularly for foreign investment, rather than being merely obstructive. If you go to any major UK airport, such as Heathrow, you will now see billboards from individual Indian states claiming to be an 'investor's paradise'.

State politicians have also cottoned on to the fact that politicians in states with economic growth above the national average have a 58% chance of re-election versus 35% chance for those with below par economic growth. The result is that the reform agenda and pro-growth message is now being driven by the states themselves as well as Modi's Government. This increases the chances of it succeeding.

China vs India

Investors are often quick to draw comparisons between India and the other emerging market powerhouse, namely China. Of course China is currently making headline news as its slowing economic growth rate looks set to dampen global growth. Part of China's problem lies in its attempt to restructure its economy, with a move away from relying on investment spending (building roads to nowhere etc) and moving towards an economy driven by domestic consumer demand. But this is proving difficult especially as all reforms are solely being driven by central Government. India on the other hand is managing to push forward with the needed reforms to secure future economic growth partly because they are being driven through by local states and not just central government. But interestingly while China seeks to stimulate more domestic demand, India already has an economy driven by domestic demand.

That is part of the reason why Indian equities (see earlier chart above) are less correlated to developed world or emerging market equities.

Is now a good time to invest in India?

India is not immune from the global slowdown, far from it. Also while there is lower correlation with other emerging market equities, valuations are not as attractive as they once were. As a DIY investor if you are looking to invest in India it is certainly a long-term play. As you will know by now my favoured indicator of value within stock markets is the CAPE (cyclically adjusted price earnings) ratio. In simple terms this can be used to give a steer of the future potential returns you can expect from a stock market based on history and current prices.

As the chart below (click to enlarge) shows a lot of what I've spoken about has been priced into the Indian stock market. Yet as a whole, the Indian stock market is still trading below it's long term average, in terms of value. So while it is not ridiculously cheap it's still offering some value. By comparison other emerging markets may seem incredibly cheap, yet there is a clear reason for it and they are likely to become cheaper still.

Which funds invest in India?

Indian equities are a long term play and despite conventional wisdom they offer diversification for a high risk portfolio. There are not many funds that invest purely in Indian equities which is why they are shoved into the 'Specialist' IMA fund sector. However there are more broader Asian or emerging market funds, which invest in a range of countries, that also invest in India (read my previous article The best funds to access the cheapest global stock markets).

For 80-20 Investor members I have analysed every fund out there and below I list the funds with the greatest Indian equity exposure along with their recent performance data. Finally remember, if you are investing in a high risk play such as Indian equities during volatile markets then it makes sense to drip your money in over a period of months, rather than invest all your money at once. That way if markets do fall you benefit from pound cost averaging which can boost your returns.

| Name | India exposure | ISIN Code | 1 month Return |

3 month Return |

6 month Return |

Max fall in 6 months | Ongoing charge |

| Neptune - India | 97.73 | GB00B1L6DT30 | -4.13 | -6.33 | -14.11 | -11.57 | 2.3 |

| Jupiter - India | 97.05 | GB00B2NHJ040 | -3.75 | -0.32 | -8.32 | -8.58 | 1.84 |

| First State - Indian Subcontinent | 81.5 | GB00B1FXTF86 | -2.36 | -1.02 | -9.05 | -8.74 | 1.96 |

| Neptune - Emerging Markets | 39.28 | GB00B2R07G10 | -1.46 | -12.21 | -16.65 | -16.88 | 2.86 |

| First State - Asia Pacific Sustainability | 32.9 | GB00B0TY6S22 | 0.27 | -7.62 | -13.62 | -13.77 | 1.7 |

| Newton - Global Emerging Markets | 30.62 | GB00BVYPP800 | -2.54 | -13.96 | -19.29 | -16.63 | 1.7 |

| Baillie Gifford - Pacific | 25.5 | GB0006063126 | 2.07 | -15.34 | -20.65 | -19.62 | 1.58 |

| F&C - Emerging Markets | 25.3 | GB0005751002 | -2.48 | -9.92 | -17.72 | -15.86 | 1.85 |

| First State - Asia Pacific Leaders | 24.6 | GB0033874214 | 0 | -9.01 | -13.83 | -13.05 | 1.55 |

| First State - Asia Pacific | 23.7 | GB0030183890 | -0.03 | -10.05 | -14.26 | -14.09 | 1.87 |

| First State - Global Emerging Markets Leaders | 21.8 | GB0033873919 | -1.09 | -8 | -12.52 | -11.62 | 1.57 |

| JPM - Emerging Markets | 21.6 | GB0030881550 | -2 | -14.04 | -20.88 | -17.88 | 1.18 |

All performance figures are net of fund charges. The material in any email, the MonetotheMasses.com website, associated pages / channels / accounts and any other correspondence are for general information only and do not constitute investment, tax, legal or other form of advice. You should not rely on this information to make (or refrain from making) any decisions. Always obtain independent, professional advice for your own particular situation. See full Terms & Conditions and Privacy Policy

Neither MoneytotheMasses.com/80-20 Investor nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Funds invest in shares, bonds, and other financial instruments and are by their nature speculative and can be volatile. You should never invest more than you can safely afford to lose. The value of your investment can go down as well as up so you may get back less than you originally invested.

Information provided by MoneytotheMasses.com/80-20 Investor is for general information only and not intended to be relied upon by readers in making (or not making) specific investment decisions.

Appropriate independent advice should be obtained before making any such decisions. Leadenhall Learning (owner of MoneytotheMasses.com/80-20 Investor) and its staff do not accept liability for any loss suffered by readers as a result of any such decisions.

The tables and graphs are derived from data supplied by Trustnet. All rights Reserved.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay