Last year I updated a piece of research titled 'The Winter Fund Portfolio – exploiting a seasonal trend'. The research was inspired by a recognised phenomenon in investment markets whereby, according to the Stock Market Almanac, the 1st November marks "the start of the strong six-month period of the year for stocks".

There are a whole host of theories as to why this seasonal trend may exist. My research piece produced two Winter fund portfolios which had successfully exploited this seasonal trend over the previous 10 years. I named these the:

- Consistent Winter Fund Portfolio

- Aggressive Winter Fund Portfolio

The methodology of how I built these portfolios can be found in the original research piece. To remind you, below are the constituent funds for each portfolio:

Consistent Winter Fund Portfolio

- BlackRock - UK Smaller Companies

- BMO - UK Mid-Cap

- Fidelity - UK Smaller Companies

- Invesco - UK Smaller Companies Equity (UK)

- Liontrust - Special Situations

Aggressive Winter Fund Portfolio

- Fidelity - UK Smaller Companies

- Franklin - UK Mid Cap

- MI - The MI Discretionary Unit

- Slater - Growth

- Unicorn - UK Smaller Companies

Winter Fund Portfolios during 2019 to 2020

It is worth going back and reading last year's review of the Winter Fund Portfolios to familiarise yourself with where we were this time last year, heading into the winter. 2020 was a difficult year for the Winter Portfolios yet still the risk/return metrics of the portfolios outshone their benchmarks. In November 2020 I then wrote that "while the Winter Portfolios struggled this year (2020), this was entirely due to the arrival of COVID-19. Interestingly as we enter the winter of 2020 news of a number of COVID-19 vaccines has seen some aggressive moves in investment markets... [meaning that] this winter the Winter Portfolio is particularly interesting". This did indeed turn out to be prophetic as I highlight below.

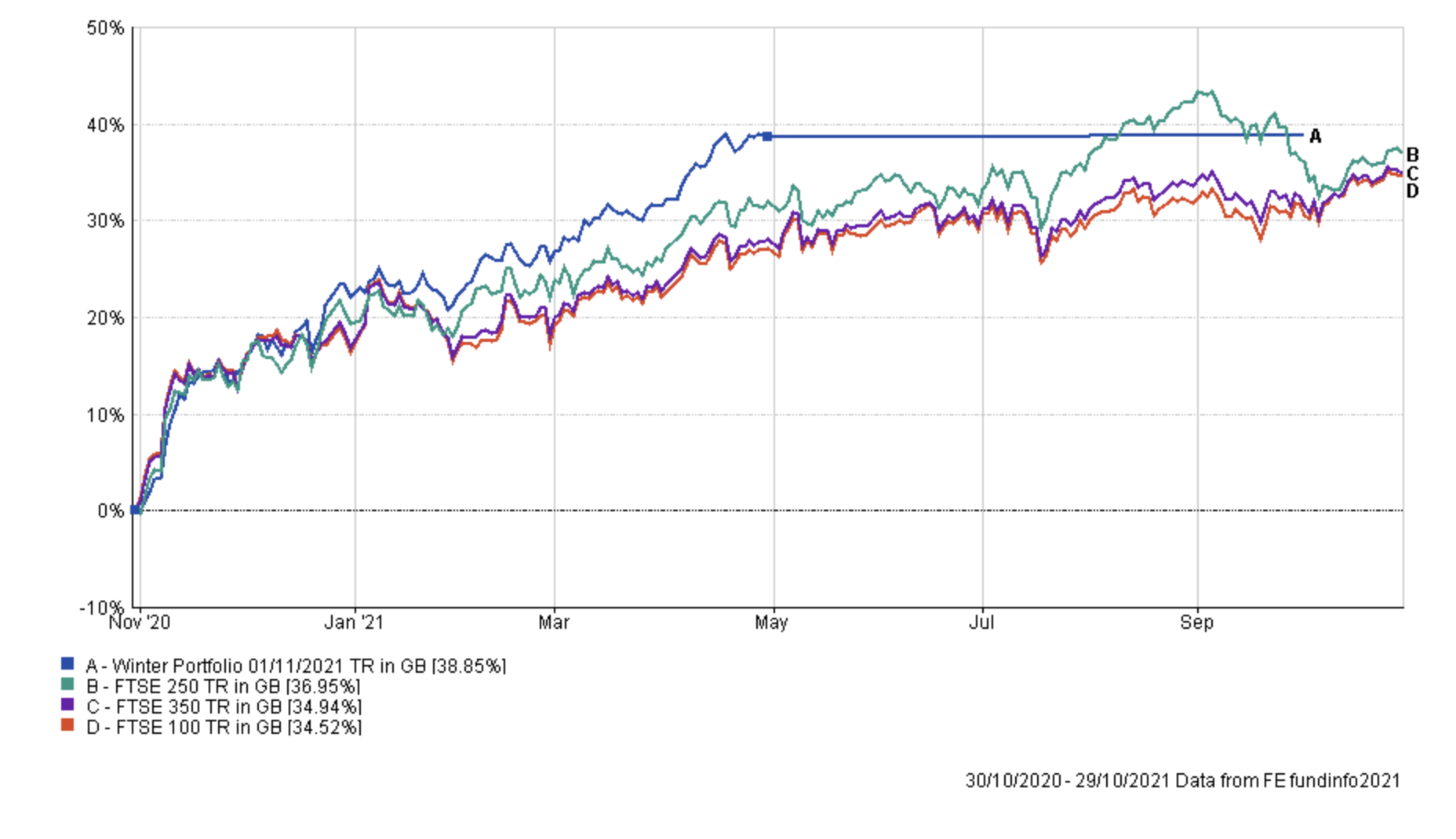

Consistent Winter Fund Portfolio 2020 to 2021

The chart below shows the performance of the Consistent Winter Portfolio versus the FTSE 100, FTSE 250 and FTSE 350 over the last year.

The performance numbers are staggering, with the Winter Portfolio outperforming the three indices and returning 38.85% despite being in cash for the last six months.

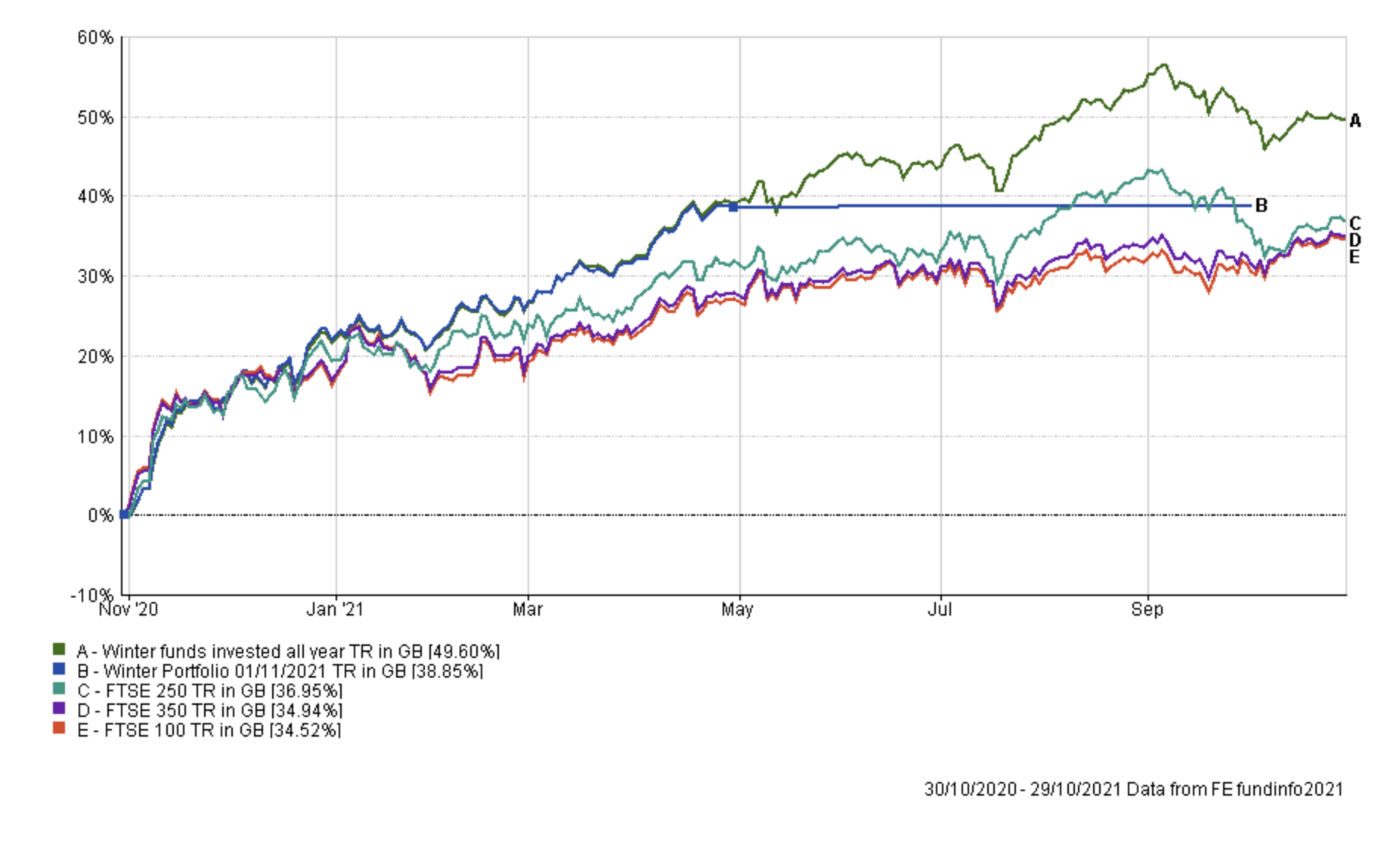

For consistency with last year's research article, the chart below shows the same chart above but with the dark green line that represents what would have happened if you remained in the Consistent Winter Portfolio without reverting to cash over the summer. It highlights just how strong the performance figures of the funds within the Consistent Winter Portfolio have been over the entire year.

In fact, the table below shows the individual performances of each of the funds in the Consistent Winter Portfolio up to the end of April (when the portfolio switches to cash) as well as the performance over the last year. The stand-out performer has been Fidelity UK Smaller Companies which I've held in my own £50k portfolio for almost a year now.

| Name | % Winter performance (1/11/20 to 30/04/21) | % 1 year performance to end Nov 2021 |

| BlackRock UK Smaller Companies | 40.91 | 52.94 |

| BMO UK Mid-Cap | 37.33 | 36.63 |

| Fidelity UK Smaller Companies | 51.56 | 68.24 |

| Invesco UK Smaller Companies Equity (UK) | 39.7 | 50.06 |

| Liontrust Special Situations | 23.51 | 31.92 |

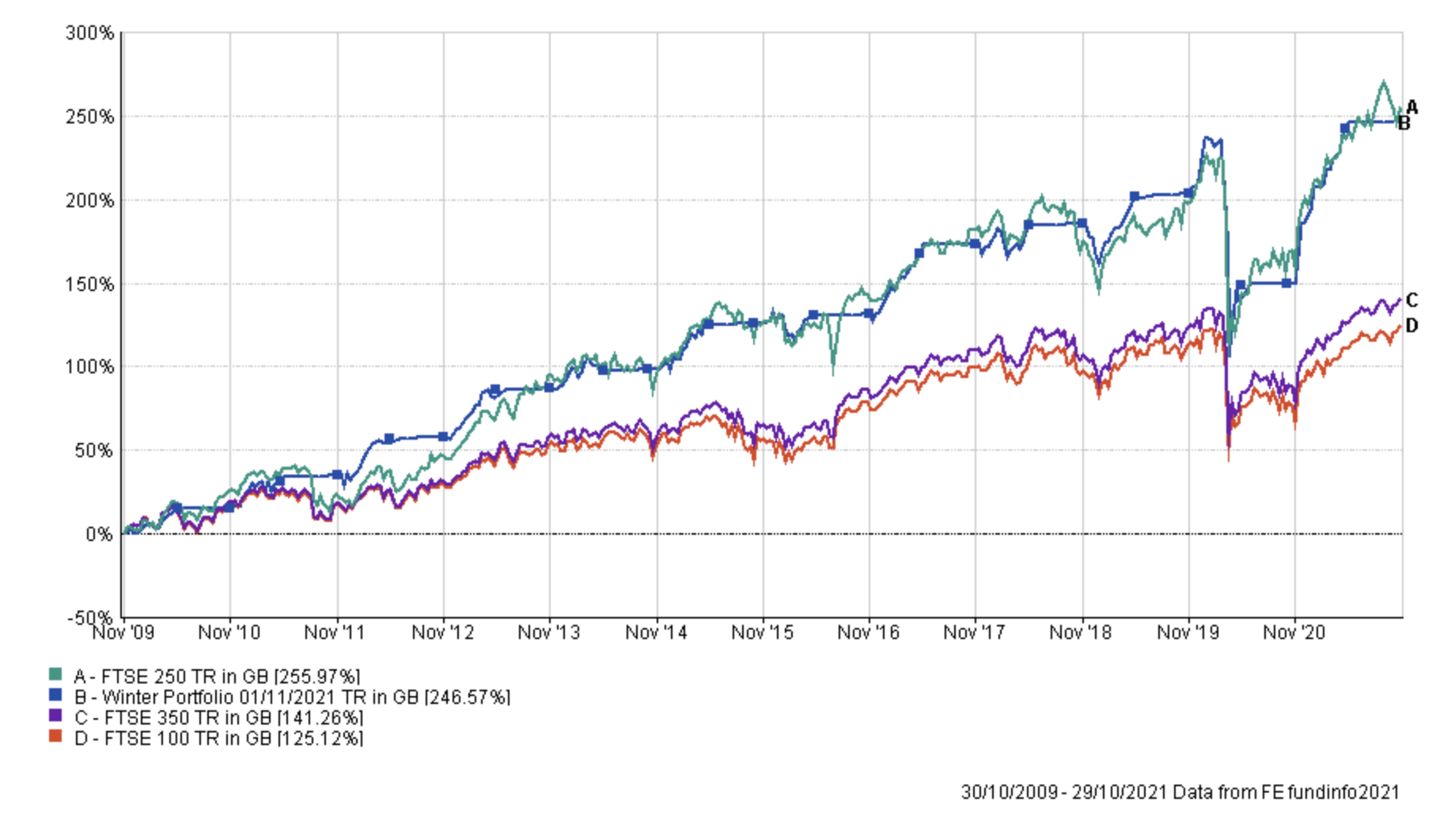

Now let's look at the performance of the Consistent Winter Portfolio, FTSE 100, FTSE 250 and FTSE 350 since November 2009, which was the starting point of the original piece of research. You can see that the Consistent Winter Portfolio was the best performing portfolio until just a few days ago.

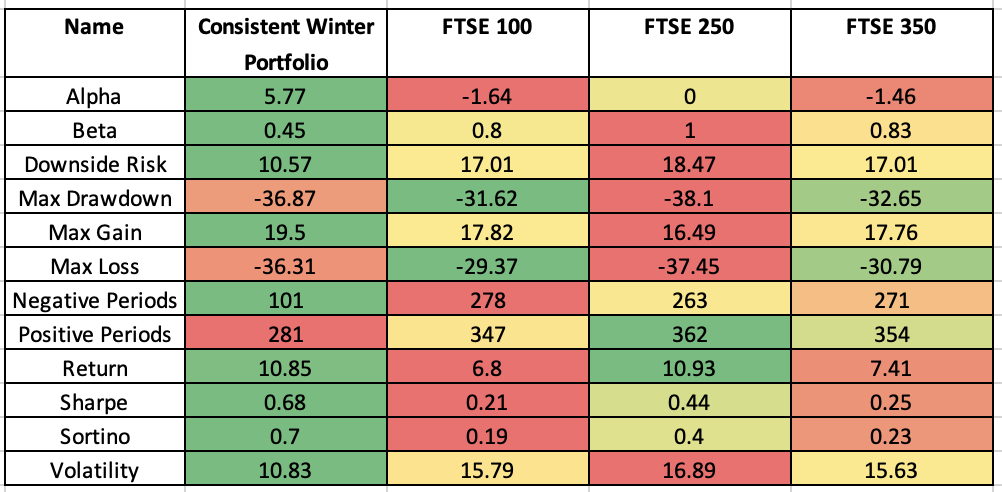

But as I highlighted last year it's not just the absolute return number that you should focus on. If we look at the key risk/reward statistics (see table below) versus the FTSE 250 benchmark (which is the leading alternative), the alpha generated by the Consistent Winter Fund Portfolio from 1/11/09 to 1/11/21 is far in excess of the other indices while the beta (how much a portfolio's movements simply reflect the wider market) is much lower. The volatility of the Consistent Winter Portfolio remains much lower while the Sharpe Ratio (the extra return the portfolio gets for each unit of risk it takes) is far higher.

What I wrote last year remains true.. "from a pure absolute return perspective, the Winter portfolio has kept pace with the FTSE 250 (which was continually invested). But from a risk/return perspective, it still wipes the floor with the FTSE 250 because it is invested in cash half of the time". The table below compares the key statistical measures. They are coloured coded by row, with green being the best and red the worst for each statistical measure. Bear in mind that when calculating the alpha and beta measures for each portfolio that the FTSE 250 is used as a benchmark, so the scores for those statistics are relative to the FTSE 250. Hence why the FTSE 250 alpha is 0 and beta is 1.

As a reminder, here is what each statistical measure means...

Alpha

Alpha is a figure which measures a manager’s apparent skill at picking winning investments versus their benchmark. Alpha is the excess return versus the return of a portfolio's benchmark (i.e the market). So a portfolio with a positive alpha indicates that the manager has outperformed through skill. While a negative alpha figure would indicate underperformance. The higher the alpha figure the better

Beta

Beta measures a portfolio's sensitivity to the general market in which it operates. The market always has a beta of 1 by definition. So if a portfolio also has a beta of 1 that would mean that if the market rose by 5% then so should the portfolio. If the portfolio has a beta of -1 then as the market rises so the portfolio falls. A well-managed index fund will have a beta of exactly 1. Portfolios that outperform the market when it does well but do even worse when the market is going down will have a beta above 1.

Maximum Drawdown

This is the biggest fall experienced in a given week.

Sharpe Ratio

The Sharpe Ratio is a measure of the excess return a manager is achieving for the risk they are taking. The higher the Sharpe Ratio the better.

Sortino Ratio

This is very similar to the Sharpe Ratio but places more emphasis on the manager's ability to manage on the downside.

Volatility

This is a measure of a portfolio's dispersion of returns, or in plain English the variability in those returns. Think of it as a measure of how much a building is prone to wobble. The more prone it is (the higher the volatility) the more it will sway in an earthquake.

Aggressive Winter Fund Portfolio 2020 to 2021

But what about the Aggressive Winter Fund portfolio? The Aggressive Winter Fund Portfolio made 41.06% over the last year despite being in cash for the last 6 months. An incredible return. It means that it marginally outperformed the more conservative Consistent Winter Portfolio as you'd expect, but it also outperformed anyone who had invested all year in an index tracker, tracking the FTSE 100, FTSE 250 or the FTSE 350 but it also took much less investment risk.

Summary

Clearly the above evidence shows that over the long term you can exploit the seasonality of stock markets, and occasionally you can profit handsomely in the short term as we did last winter. Furthermore, you are better off trying to exploit this particular market anomaly via active funds within the UK smaller companies sector rather than using a passive approach (say with either a FTSE 350 or FTSE 250 index tracker). This once again backs up another piece of 80-20 Investor research that I previously carried out titled 'The sectors where active funds beat passives' which showed that active funds hugely outperformed passive strategies within the UK Smaller Companies sector.

What is also interesting this year is that most of the funds within the two Winter Portfolios have been stalwarts of either the BOTB or BFBS tables throughout much of 2021.

Back in November 2020 I created a wider shortlist of funds based upon the fund selection process for each original Winter portfolio (which is a 10-year backwards-looking process) that could be well placed to benefit from the obvious seasonal trend during the winter months. I had to loosen the criteria to allow for funds that had had 8 positive winters in the last 10, with a strong average winter performance due to the impacts of the pandemic. The table below lists those funds alongside their return during the 6 month winter period. In addition, those highlighted green outperformed a FTSE 250 tracker over the same time period (which itself returned 31.95%).

| Name | Sector | % return November 2020 to April 2021 |

| Liontrust Special Situations | UK All Companies | 23.51 |

| ASI UK Smaller Companies | UK Smaller Companies | 17.53 |

| Aviva Inv UK Smaller Companies | UK Smaller Companies | 46.88 |

| AXA Framlington UK Smaller Companies | UK Smaller Companies | 44.52 |

| BlackRock UK Smaller Companies | UK Smaller Companies | 40.91 |

| BMO UK Smaller Companies | UK Smaller Companies | 37.07 |

| Fidelity UK Smaller Companies | UK Smaller Companies | 51.56 |

| Invesco UK Smaller Companies Equity (UK) | UK Smaller Companies | 39.7 |

| JPM UK Smaller Companies | UK Smaller Companies | 36.49 |

| LF Gresham House UK Smaller Companies | UK Smaller Companies | 52.17 |

| Liontrust UK Smaller Companies | UK Smaller Companies | 30.95 |

| Scottish Widows UK Smaller Companies | UK Smaller Companies | 34.1 |

| TB TB Amati UK Smaller Companies | UK Smaller Companies | 38.7 |

| Aegon UK Smaller Companies | UK Smaller Companies | 31.32 |

Applying the same process as last year, I've once again produced a shortlist of possible candidates for a 'revised winter portfolio' as shown below. Interestingly those funds in bold are already members of the original Winter portfolios.

- Jupiter UK Smaller Companies Equity

- LF Gresham House UK Micro Cap

- Premier Miton UK Smaller Companies

- Fidelity UK Smaller Companies

- FTF Franklin UK Smaller Companies

- AXA Framlington UK Smaller Companies

- Invesco UK Smaller Companies Equity (UK)

- Liontrust UK Smaller Companies

- MI MI Sterling Select Companies

- BlackRock UK Smaller Companies

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay