The background to my £50,000 portfolio challenge

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was two-fold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance review

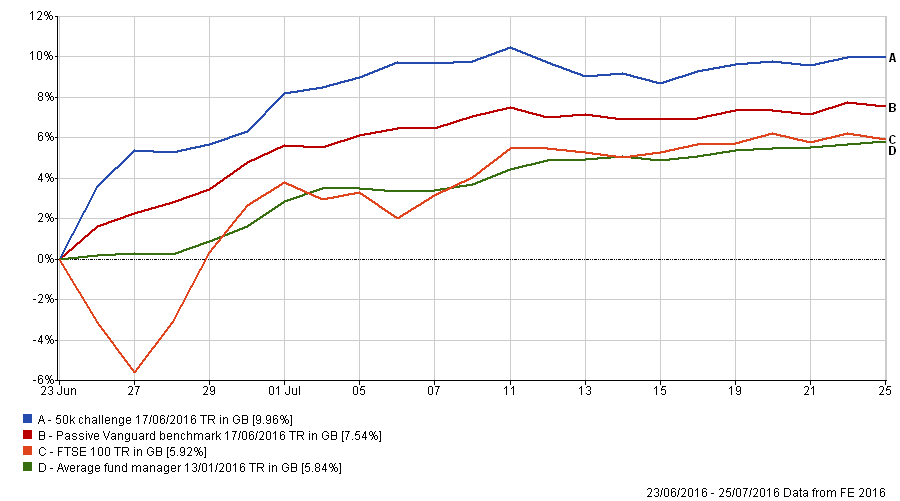

A month has passed since the Brexit vote and my last review of my portfolio so it's time for me to engage with my portfolio again. When the UK voted to leave the European Union markets went into meltdown my portfolio made 5.35% in 2 days as the FTSE 100 fell by 5.62%. But since then all we've heard is how the FTSE 100 has rebounded and that all is ok. How has my portfolio fared then in this environment? Has it been left behind?

The chart below (click to enlarge) shows that despite the market rally my portfolio is still outperforming. In the aftermath of the Brexit vote it rallied strongly and has ticked up ever since. Of the four options below I know which I would want to be invested in.

Yet that is just a snapshot in time over the last month. How is the portfolio doing since it was launched in March 2015? The table shows that despite the market turbulence and a number of market crashes in the last year my portfolio is up over 11%! I'm very pleased with that and I know a number of you have had even better results using 80-20 Investor in your own way.

| Investment | % return March 2015 to date |

| My £50,000 portfolio (using 80-20 Investor) | 11.25% |

| Passive Vanguard benchmark | 7.74% |

| Average managed fund | 5.86% |

| FTSE 100 | 2.81% |

What next for my £50,000 portfolio?

I planned to review my portfolio in the course of the last month yet all my funds remained in the 80-20 Investor fund shortlists so I was happy with the status quo.

Now that the panic that immediately followed the Brexit vote has subsided I am keen to review my portfolio once again. It may seem quite a bold thing to do and some of you will be thinking why rock the boat if things are going so well but I want to stick to a process that takes the emotional decision making out of the equation.

My current portfolio is shown below:

| Fund | % allocation |

| Fundsmith Equity Fund | 20.27% |

| Fidelity Global Dividend | 13.36% |

| Barclays - Sterling Bond | 9.88% |

| Vanguard Lifestrategy 20% Equity | 20.16% |

| Cash | 7.61% |

| First State - Global Listed Infrastructure | 13.35% |

| Jupiter Absolute Return | 6.78% |

| Threadneedle Global Bond | 8.59% |

| TOTAL | 100% |

Of all of the funds above only two of the global funds, Fundsmith Equity and Fidelity Global Dividend, have dropped out of the 80-20 Investor fund shortlists, either the Best of the Best Selection or the Best funds by Sector lists. So as things stand I will look to review their place despite their strong performance.

Similarly I want to reinvest the cash position I created selling out of Japan. Ideally I would look to invest into Japan equities again in line with the 80-20 Investor Best of the Best Selection asset mix.

However this week could be an incredibly volatile week as the company earnings reporting season peaks with a number of tech giants reporting. In addition the US Federal Reserve are meeting and crucially the Bank of Japan is expected to unleash even more Quantitative Easing on Friday. I always stress the importance of not trying to time the market however it does make sense to limit trades in a period that could experience volatility as selling a fund and buying another will mean you could be out of the market for a day or so.

As the global funds are US focused and account for a third of my portfolio my portfolio would be more exposed to extremes of volatility surrounding the US reporting season. In addition, this weekend will see the release of the latest 80-20 Investor Best of the Best shortlist which I will use to overhaul the entire portfolio. There are likely to be some significant changes now that we are a month on from the referendum and a number of funds have dropped out of the most recent Best by Sector tables, which is an indicator that they will struggle to make the grade next month.

On the flip side the cash position has been held for around 6 weeks and I need to reinvest these funds. My exposure to Japanese equities has been reduced significantly after I sold out of the Legg Mason Japan Equity fund. The plan was always to reinvest the money back into a Japan equity fund after the dust had settled following the referendum. So the proceeds from the previous sale will be invested into the AXA Framlington Japan fund which is in the current Best of the Best Selection, but perhaps more importantly as we near the end of the month, also in the Best funds by Sector list. The later is not true for a number of the other funds in my £50,000 portfolio as mentioned above. This is why I am happy to invest the cash now as opposed to waiting a few days for the new 80-20 Investor shortlists to be published.

Of course on Friday the BOJ is expected to announce more QE and interest rate cuts. While I'm not as convinced as the market the transaction is relatively small and I am happy to take a hit or benefit either way.

My new portfolio is shown below:

| Fund | % allocation |

| Fundsmith Equity Fund | 20.27% |

| Fidelity Global Dividend | 13.36% |

| Barclays - Sterling Bond | 9.88% |

| Vanguard Lifestrategy 20% Equity | 20.16% |

| AXA Framlington Japan | 7.61% |

| First State - Global Listed Infrastructure | 13.35% |

| Jupiter Absolute Return | 6.78% |

| Threadneedle Global Bond | 8.59% |

| TOTAL | 100% |

My current asset allocation

Global fixed interest - 20%

US equities - 26%

European equities - 8%

UK equities - 9%

Japanese equities - 10%

Other international equities - 0%

Cash - 5%

Property - 0%

UK Gilts - 3%

UK Fixed Interest 12%

Alternative assets/strategies - 7%

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay