The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

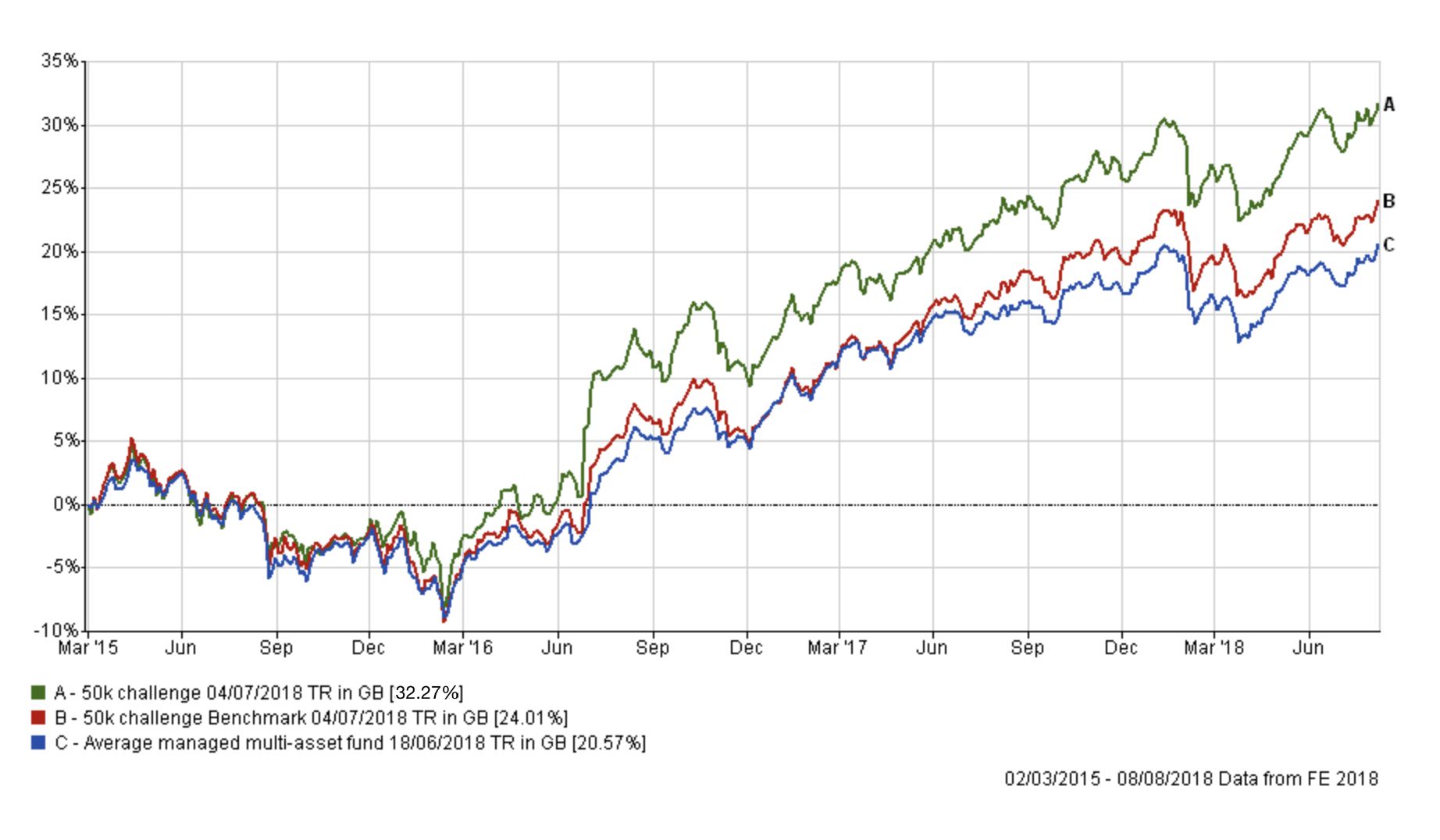

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015, three years ago. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

In my July 2018 portfolio review I commented that my portfolio had given up some of its outperformance over its benchmarks in June. However, since the changes made as a result of last month's review that outperformance has been more than regained and the portfolio now stands at a record profit of 32.67% as shown in the chart above.

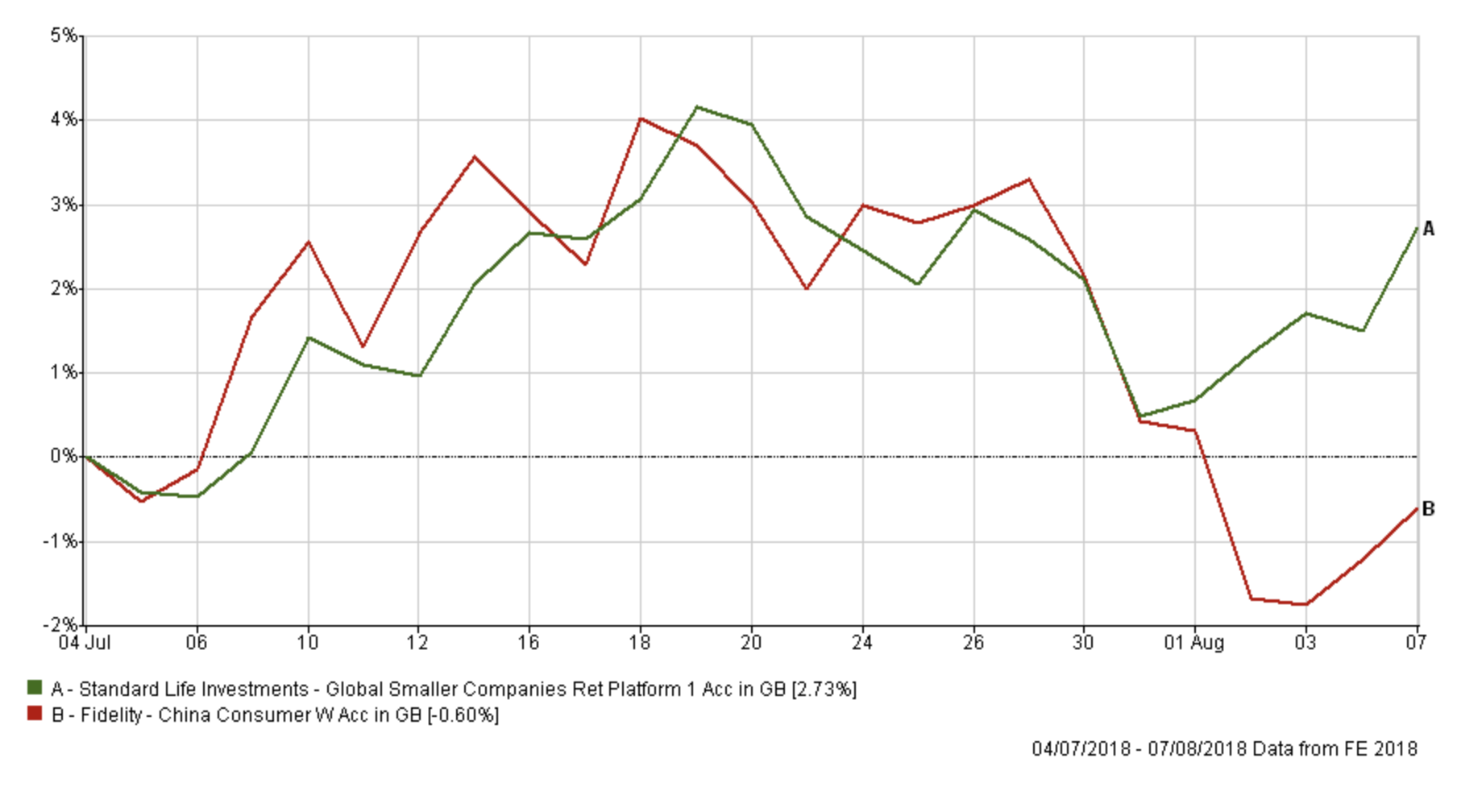

The key change from last month was to remove my Asian equity exposure, principally in China. The first chart below shows the performance of the funds I held in red alongside their replacements in green. Last month I replaced Fidelity China Consumer with Standard Life Investments Global Smaller Companies. The reasons I preferred the Standard Life fund over the Fidelity fund was because it was another high-risk fund but one which is more geographically diversified and which has been a regular in the BOTB. With its focus on smaller companies, it has fared better than many of its large-cap focused peers that have been battered by trade war fears. As the chart below shows, following a respite in the US-China trade war tensions both funds performed well in July, however, a sudden ratcheting up in trade war threats from both sides in recent days has seen Chinese equities slump while smaller companies benefited. For now at least the fund switch has paid off.

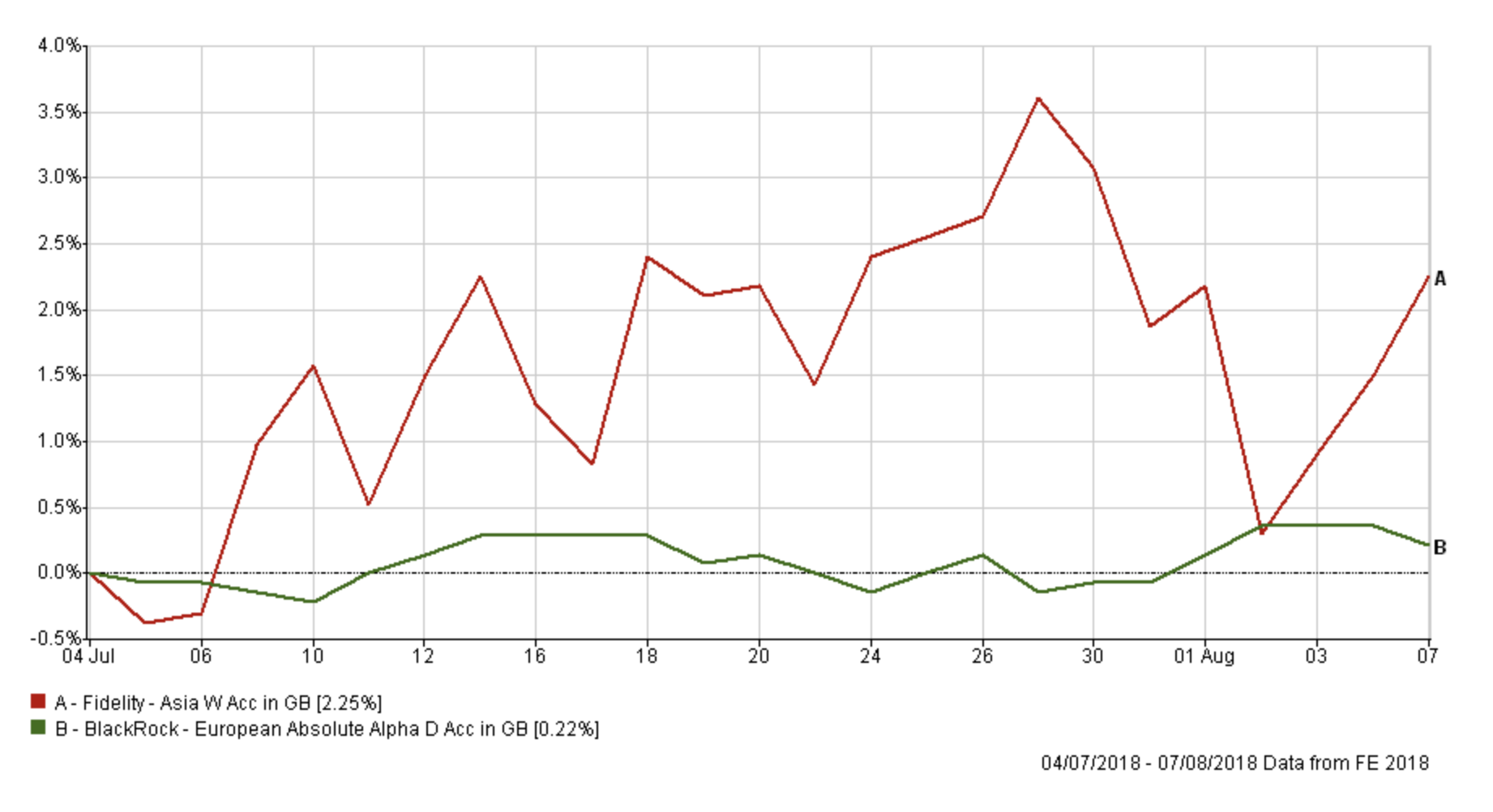

The other fund switch at the start of July was from the high-risk Fidelity Asia fund into the Blackrock European Absolute Alpha fund. The switch was not a like-for-like switch but instead was made to reduce the volatility and risk of the portfolio. You can read the full reasoning for the switch here. The chart below shows how the Fidelity Asia fund performance continued to be volatile and has only outperformed the new Blackrock fund in recent days.

Looking at the rest of my portfolio as a whole, the table below shows my current allocation, with those funds in green still in the BOTB while those in yellow are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code | SEDOL Code |

| Baillie Gifford Global Discovery | 5.5 | Medium | Global | GB0006059330 | 605933 |

| AXA Framlington American Growth | 12 | High | North America | GB00B5LXGG05 | B5LXGG0 |

| BlackRock European Absolute Alpha |

4.5 | Low | Targeted Absolute Return | GB00B4Y62W78 | B4Y62W7 |

| Standard Life Investments Global Smaller Companies |

4.8 | High | Global | GB00B7KVX245 | B7KVX24 |

| FP Pictet Multi Asset Portfolio | 6.6 | Low | Targeted Absolute Return | GB00BVYTTC41 | BVYTTC4 |

| Jupiter Japan Income | 6.6 | Medium | Japan | GB00B0HZTZ55 | B0HZTZ5 |

| Jupiter UK Smaller Companies | 7.9 | Medium | UK Smaller Companies | GB0004911870 | 491187 |

| Premier Diversified | 19.2 | Medium | Mixed Investment 40-85% Shares | GB00B8BJV423 | B8BJV42 |

| Standard Life Investments UK Real Estate | 7.8 | Low | Property | GB00BYPHP536 | BYPHP53 |

| TwentyFour Dynamic Bond | 10.8 | Low | Sterling Strategic Bond | GB00B5KPRZ34 | B5KPRZ3 |

| Allianz UK Equity Income | 7.2 | Medium | UK Equity Income | GB00B82ZGC20 | B82ZGC2 |

| LF Miton European Opportunities | 7.1 | Medium | Europe Excluding UK | GB00BZ2K2M84 | BZ2K2M8 |

Looking at the table above it is interesting to note that the funds that have been highlighted green or yellow are those investing in equities. It is a reflection of how equities are driving portfolio returns at the moment while low-risk alternatives, particularly bonds, have been lacklustre for much of 2018. I therefore plan to leave the funds coloured green or yellow as they are.

On the opposite side of the coin, most of the funds in red are those that diversify my portfolio outside of equities and provide some downside protection. While markets have put February's bond/stock sell-off behind them these low-risk funds have started to lag some of their peers taking more investment risk. As ever, when reviewing my portfolio I try and keep all changes to a minimum however given the number of funds that have slipped out of the 80-20 Investor fund tables I will run through each in turn detailing my decision.

The most pressing concern this month has been the unravelling shambles that is Brexit. In July's review I wrote about my concerns over holding bricks and mortar property funds (i.e. those that actually invest in buildings). At the time I said:

"These [concerns] centred around the uncertainties over Brexit and the danger of a repeat of the panic that trapped investors in property funds back in 2016. However........[I] will likely look to reduce [my exposure] in the coming months in favour of other low-risk assets or even cash"

Ahead of the Brexit vote in 2016 investors pulled £148m from property funds during the April and £367m during the May. The pace accelerated in June following the vote and 6% of assets across the property fund sector were withdrawn by investors. This caused a liquidity crunch for most property funds and many either suspended withdrawals altogether (as Standard Life did) or penalised investors heavily on the way out.

I ran some analysis of performance and fund size and it suggests that in the last 3 months the Standard Life UK Real Estate fund has had over £93m pulled from it. That equates to almost 3.8% of the fund's £2.4bn of assets under management. With the odds of a no-deal Brexit rising by the day this level of withdrawals has set alarm bells ringing for me. I don't want to get stuck in a property fund as some investors did in 2016. 80-20 Investor members dodged that trap back in 2016 and it would be preferable to dodge a possible repeat in the coming months. It's a shame because the Standard Life UK Real Estate fund has done exactly what I wanted. Produced a steady reliable positive return, comfortably beating cash. So I am switching completely out of the fund and into cash.

The reason why I have chosen cash is that if you look at the returns on bond funds they have been dismal. Most have lost money in 2018 or been more volatile than you'd like to see. There are some that have started to regain some form of momentum but for me it is not exciting enough yet to get involved. When investing in low-risk funds there is always the consideration of whether the risks/reward is more attractive than cash. At the moment I'm not convinced it is, so I'd rather hold cash temporarily until better opportunities present themselves.

I already have exposure to targeted absolute return funds and few such funds are making money in the current environment.

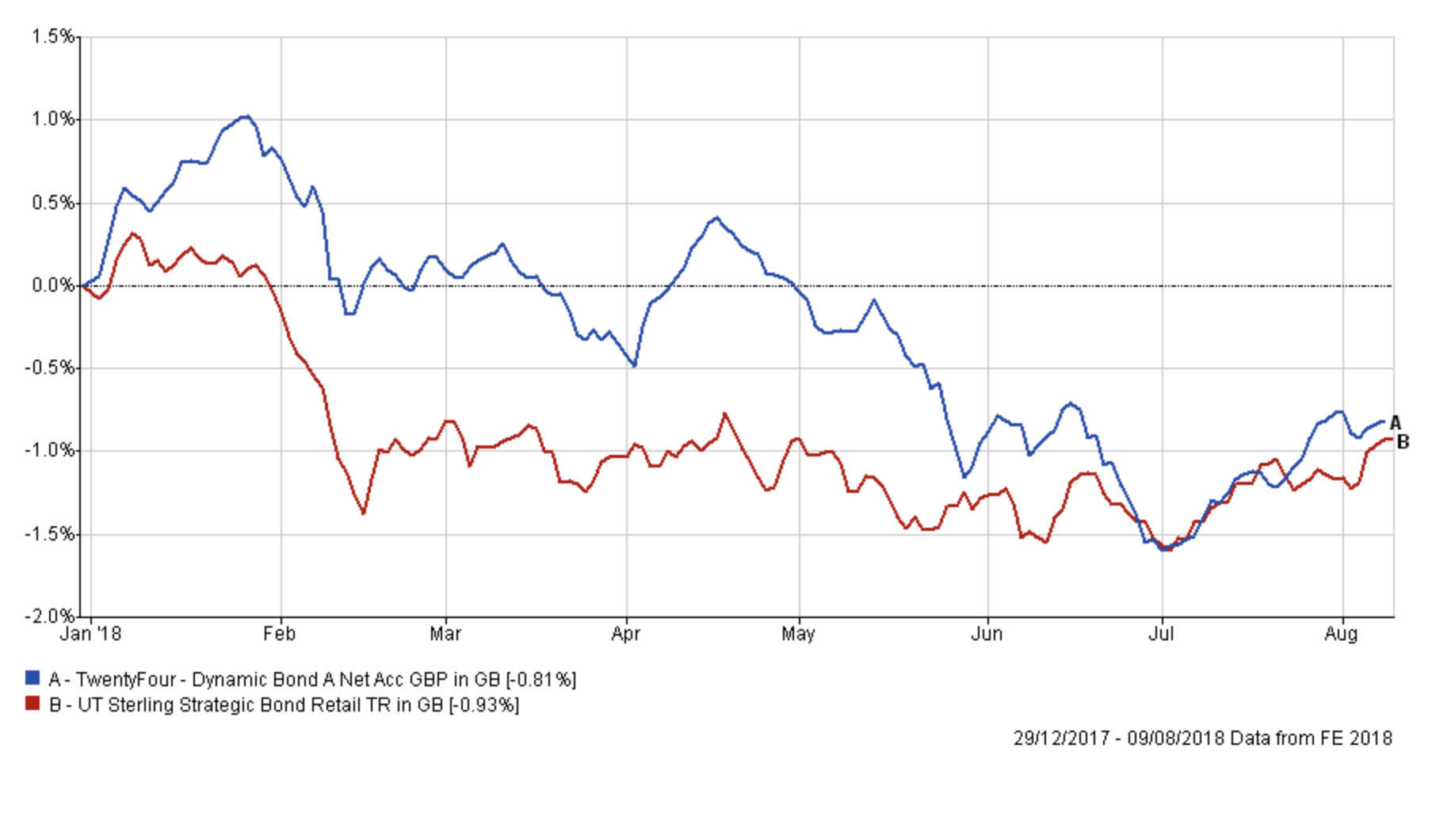

In the last few months I've been reducing my exposure to the TwentyFour Dynamic Bond fund. In fact in June I said that although it was outperforming bond funds it was slowly losing value and perhaps I'd be better off holding cash. The chart below shows how the outperformance over the last 6 months has slowly been eroded and how bond funds have underperformed cash. So temporarily at least I will sell my Twentyfour Dynamic Bond holding and move the proceeds into cash.

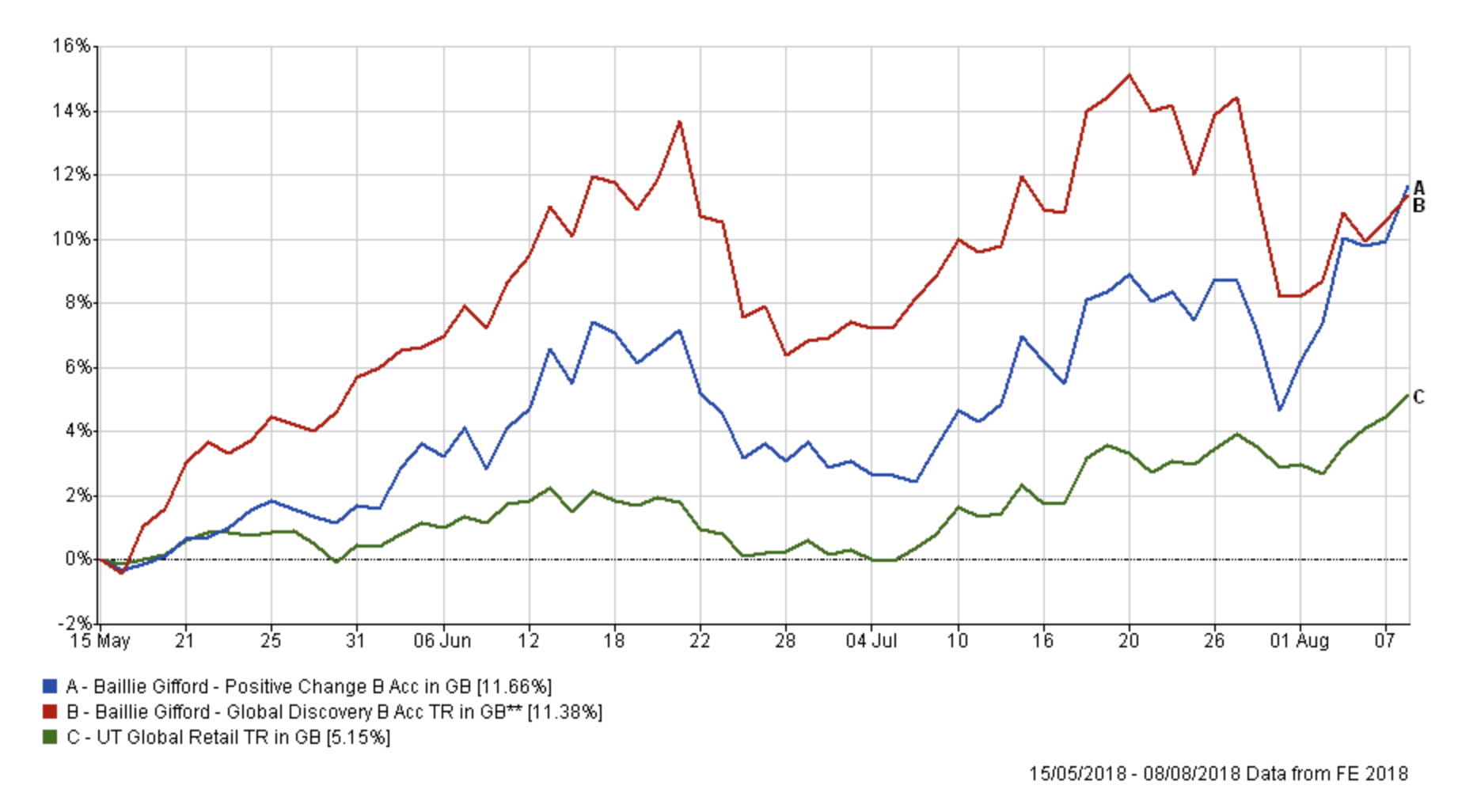

Moving on to look at the Baillie Gifford Global Discovery fund, it has been a stellar performer. It is up a staggering 11.38% in the two and half months since I've held it. That compares to 5.15% for the average global equity fund. Despite being the top performer over most recent time periods it has dropped out of the BOTB and BFBS tables due to its rising investment risk. The fund has proved volatile and 80-20 Investor is about managing risk as well as optimising investment returns. As such I am switching out of that fund into one of its stablemates within the same sector, namely Baillie Gifford Positive Change. This latter fund has been a regular in the BOTB but has also produced strong returns over the same timeframe already discussed, as shown in the chart below. The Baillie Gifford Positive Change fund has a lower max weekly fall figure (-5.91%) versus that of the Baillie Gifford Global Discovery fund (-7.01%). I have no problem taking profits and moving into a less risky strategy, especially a closely aligned one.

Blackrock European Absolute Alpha has slipped out of the 80-20 Investor tables but I plan to leave it in my portfolio for now and keep an eye on it. If you refer to the earlier chart the fund has done exactly what I had expected it would do, which is to preserve capital with opportunity for some upside. In addition, I have only held the fund for a short period of time and, given its intended role in my portfolio, it's too soon to warrant changing.

The FP Pictet Multi Asset Portfolio has remained outside of the 80-20 Investor tables for a while now and given its lacklustre performance since I've held it (my holding's value is pretty much as it was when I first invested) it is time for a refresh. I've decided to make a like-for-like switch into another Targeted Absolute Return fund rather than invest in a bond fund as the latter's performance has been disappointing in 2018. As I stated in August's monthly newsletter, bond investors must be wondering when they will ever make money again. I have therefore decided to move out of the FP Pictet Multi Asset Portfolio into the Newton Real Return fund. The Newton fund is more volatile than the fund it replaces and is more influenced by equity markets but given my portfolio's increased cash positioning, I am happy to increase the risk taken by this portion of my portfolio.

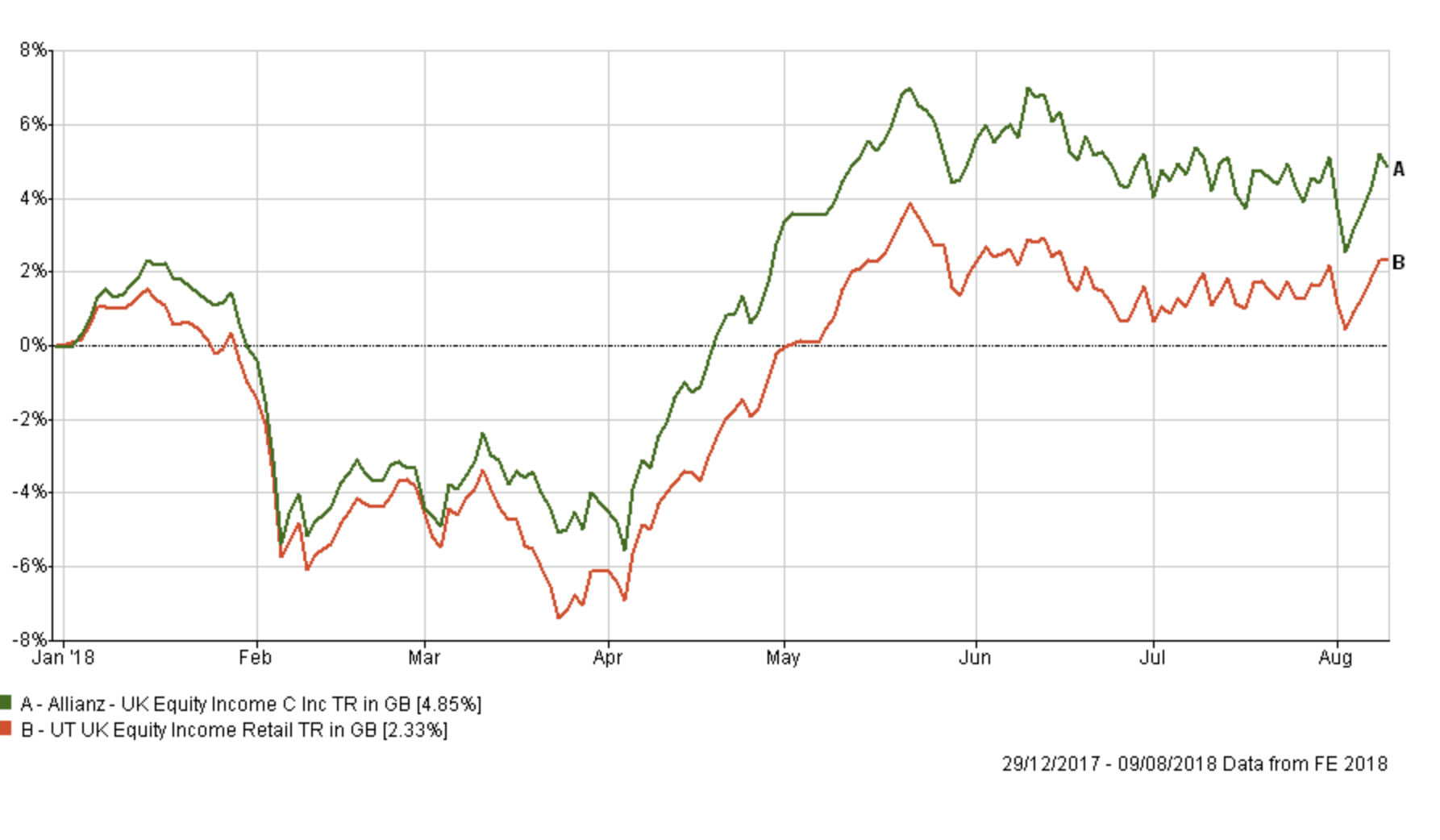

Allianz UK Equity Income has performed well this year as shown in the chart below but it has been range-bound in recent months, along with its peers.

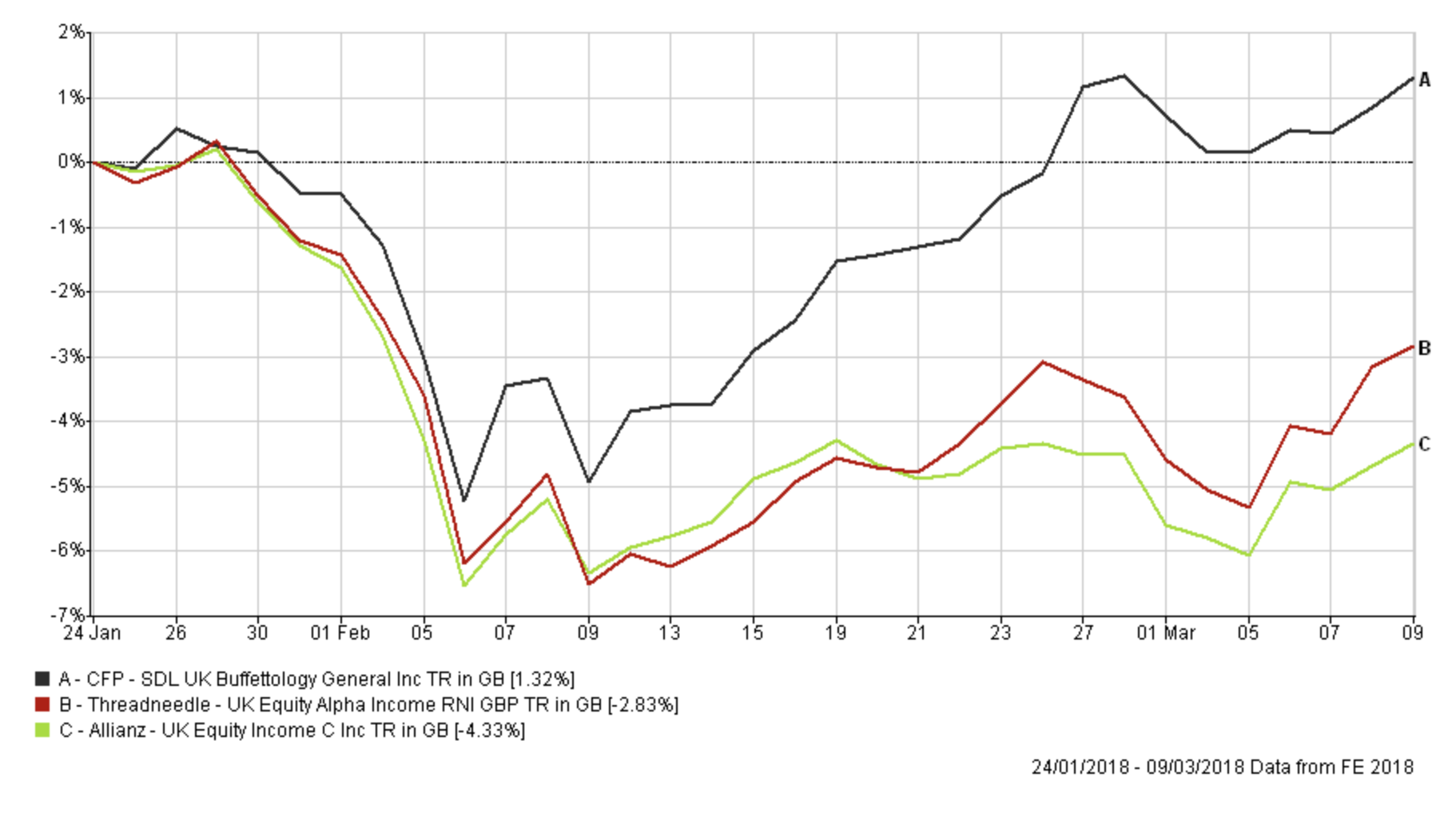

So in order to maintain my UK Equity exposure I will switch out of the fund and into CFP SDL UK Buffettology. The fund has performed well, particularly of late where its value style has gained favour as discussed in August's monthly newsletter. The fund has been a regular in the BOTB and BFBS tables. Equity income funds often have a defensive bias and so can fare better than ordinary UK All Companies funds (which the Buffettology fund is) in a sell-off. However, the chart below shows that the Buffetology fund performed admirably in the spring sell-off versus the Allianz fund and another top equity income fund (currently in the BOTB). As an investor it is sensible to be mindful of the recent correction, in case we see a repeat, even if the rest of the market is trying to forget it.

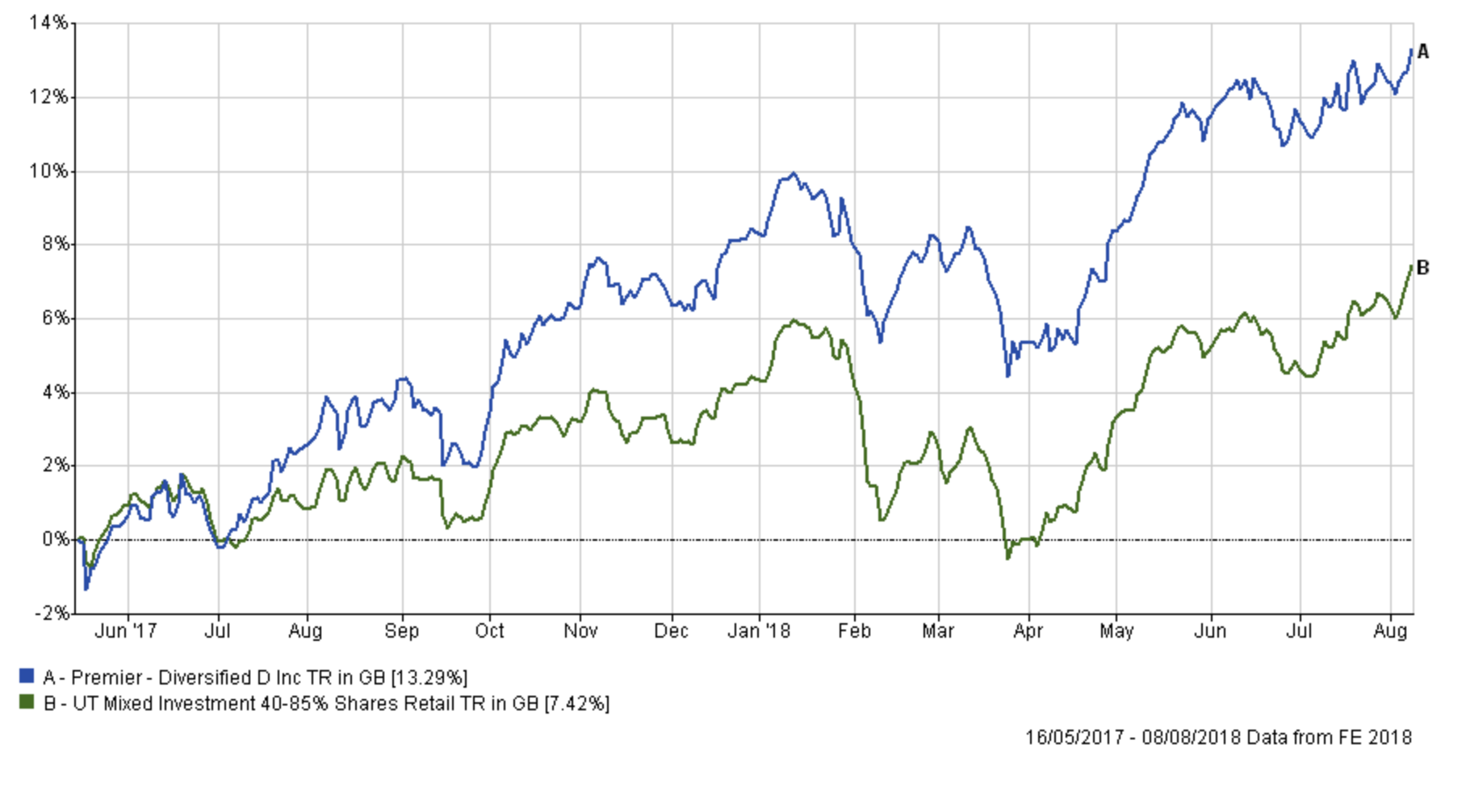

The last fund that I plan to change is Premier Diversified. It has formed a core part of my portfolio since May 2017 and has been very profitable. The chart shows the performance of the fund versus the average of its peers since I've held it.

Fund switches

Below I list the switches for ease of reference:

- 100% out of Standard Life Investments UK Real Estate and 100% into cash

- 100% out of TwentyFour Dynamic Bond and 100% into cash

- 100% out of Baillie Gifford Global Discovery and 100% into Baillie Gifford Positive Change

- 100% out of Allianz UK Equity Income and 100% into CFP SDL UK Buffettology

- 100% out of FP Pictet Multi Asset Portfolio and 100% Newton Real Return

- 50% out of Premier Diversified and 100% into Liontrust Sustainable Future Absolute Growth

In carrying out the above switches I:

- remove my exposure to bricks and mortar property funds. While the BOTB does currently have property exposure this is via equities (i.e shares in property companies)

- broadly maintained my equity asset mix as it was already, with the exception of decreasing my bond exposure in favour of cash

- I have a temporary cash weighting of 19-23% which I plan to put to work when low-risk opportunities arise

Overall I am switching about 48% of my portfolio but as most of this is in low-risk funds it shouldn't impact performance too much while the transaction goes through. My new portfolio will look as follows and still has an equity exposure of around 60%.

My new portfolio looks like this:

| Fund | Allocation | Risk | Sector | ISIN Code | SEDOL Code | Citicode / TIDM |

| AXA Framlington American Growth | 12.5 | High | North America | GB00B5LXGG05 | B5LXGG0 | 03TF |

| Baillie Gifford Positive Change | 5.6 | High | Global | GB00BYVGKV59 | BYVGKV5 | NGPB |

| BlackRock European Absolute Alpha | 4.4 | Low | Targeted Absolute Return | GB00B4Y62W78 | B4Y62W7 | EYN0 |

| CFP SDL UK Buffettology | 7 | Medium | UK All Companies | GB00B3QQFJ66 | B3QQFJ6 | MJZ1 |

| Jupiter Japan Income | 6.6 | Medium | Japan | GB00B0HZTZ55 | B0HZTZ5 | JV63 |

| Jupiter UK Smaller Companies | 7.8 | Medium | UK Smaller Companies | GB0004911870 | 491187 | JU20 |

| LF Miton European Opportunities | 7.4 | Medium | Europe Excluding UK | GB00BZ2K2M84 | BZ2K2M8 | MSED |

| Liontrust Sustainable Future Absolute Growth | 9.6 | Medium | Flexible Investment | GB0030029622 | 3002962 | CU94 |

| Newton Real Return | 6.5 | Low | Targeted Absolute Return | GB0001642635 | 164263 | BS97 |

| Premier Diversified | 9.6 | Medium | Mixed Investment 40-85% Shares | GB00B8BJV423 | B8BJV42 | GH6F |

| Standard Life Investments Global Smaller Companies | 4.7 | Medium | Global | GB00B7KVX245 | B7KVX24 | 10FZ |

| Cash | 18.3 | Low | N/A | N/A | N/A | N/A |

My new asset mix

This means my new asset mix is (previous asset mix is in brackets):

-

- UK Equities 19% (19%)

- North American Equities 21% (21%)

- Global Fixed Interest 2% (8%)

- Japanese Equities 8% (9%)

- Other International Equities 0% (0%)

- Asian equities 0% (0%)

- European Equities 11% (11%)

- UK Fixed Interest 0% (0%)

- Cash 23% (4%)

- Alternative Investment Strategies 16% (19%)

- Emerging Asia equities 0% (0%)

- Emerging Market Fixed Interest 0% (0%)

- Property 0% (9%)

Damien's high risk and low risk portfolios

Using the logic described in my post New: Damien’s Higher Risk Portfolio the higher and lower risk versions of my portfolio would like as follows:

Higher risk

| Fund | Allocation |

| AXA Framlington American Growth | 17.7 |

| Baillie Gifford Positive Change | 7.9 |

| CFP SDL UK Buffettology | 9.9 |

| Jupiter Japan Income | 9.3 |

| Jupiter UK Smaller Companies | 11.0 |

| LF Miton European Opportunities | 10.5 |

| Liontrust Sustainable Future Absolute Growth | 13.6 |

| Premier Diversified | 13.6 |

| Standard Life Investments Global Smaller Companies | 6.5 |

Lower risk

| Fund | Allocation |

| BlackRock European Absolute Alpha | 5.4 |

| CFP SDL UK Buffettology | 8.5 |

| Jupiter Japan Income | 8.1 |

| Jupiter UK Smaller Companies | 9.5 |

| LF Miton European Opportunities | 9.0 |

| Liontrust Sustainable Future Absolute Growth | 11.7 |

| Newton Real Return | 7.9 |

| Premier Diversified | 11.8 |

| Standard Life Investments Global Smaller Companies | 5.8 |

| Cash | 22.3 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay