The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

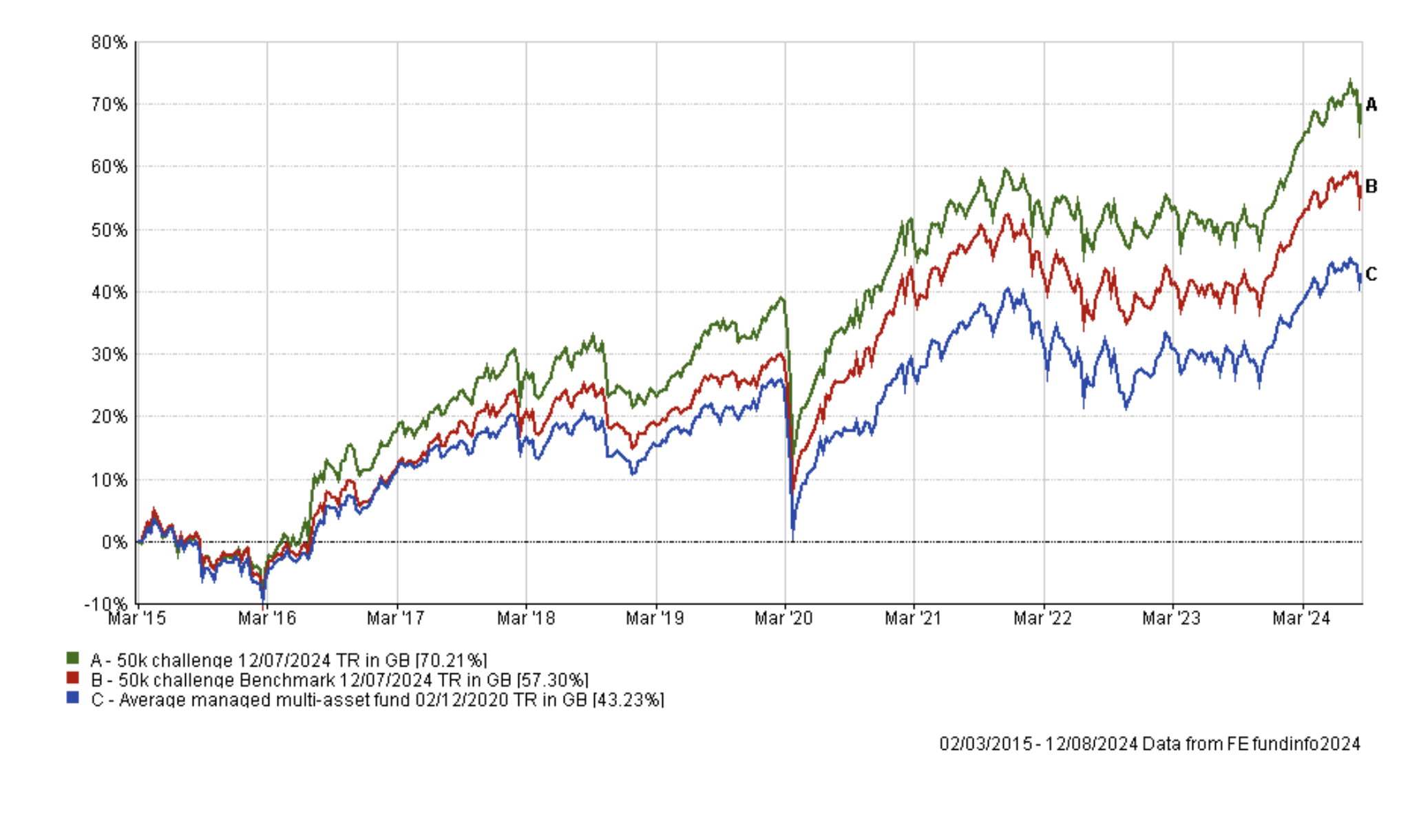

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

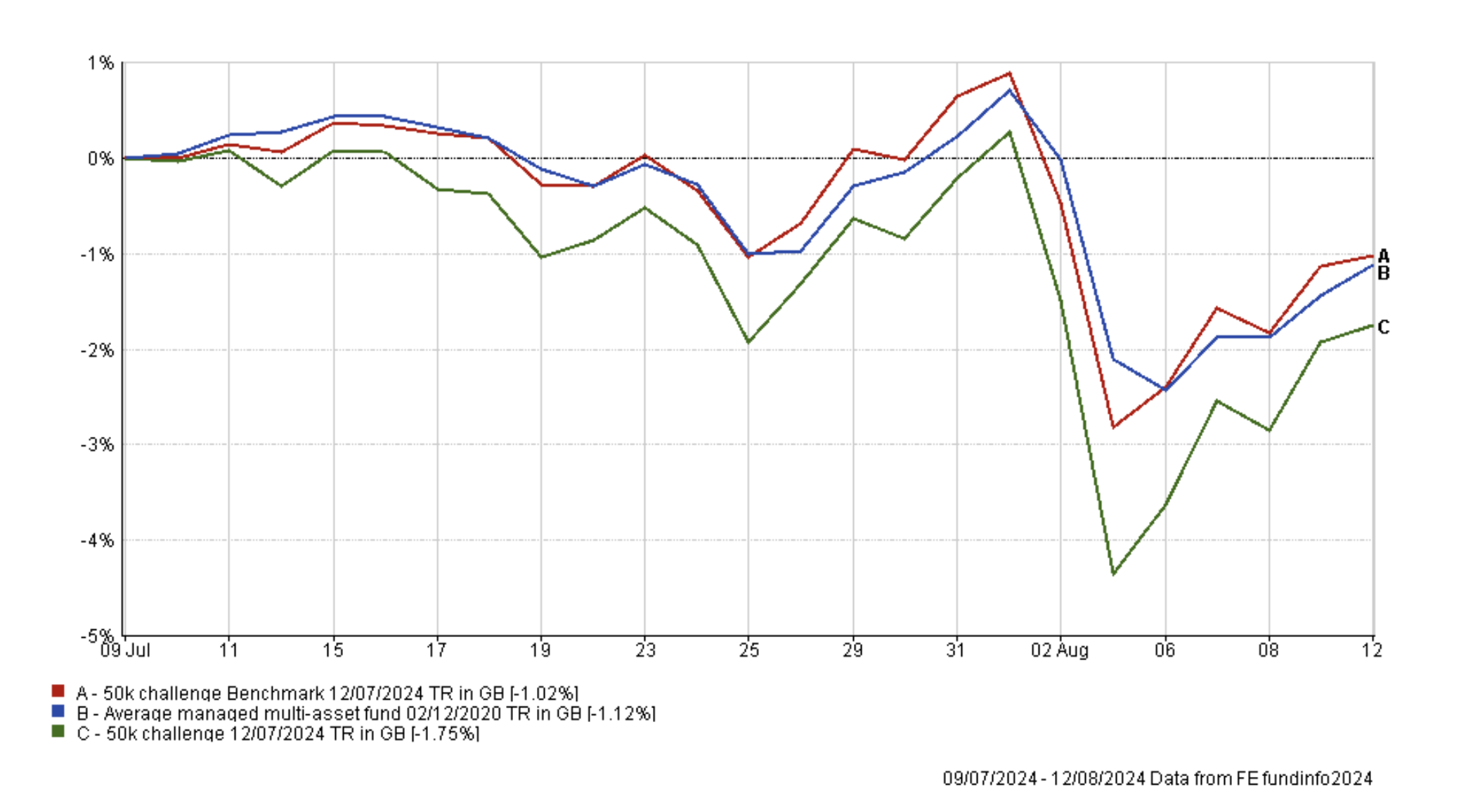

You can see how my portfolio continues to significantly outperform its benchmarks despite the market pullback we've experienced in the last few weeks. This pullback can be seen more clearly in the chart below which shows the performance of my portfolio vs its benchmarks since my last portfolio review in July. My portfolio was hit harder than its benchmarks due to the stock market wobble being centred around Japanese equities and US large tech stocks, both of which are contained within my portfolio.

Turning my attention to how individual funds performed over the last month, as you can see from the table below, those funds with exposure to US large cap tech stocks and Japanese equities were hit the hardest. The catalyst for the slump, which I will cover in more detail in my next weekly newsletter, was the market pricing in the possibility of a US recession and further interest rate hikes from the Bank of Japan. This saw investors rotate out of US tech stocks and dump Japanese equities in significant volume. In fact, the Nikkei 225 suffered its worst one day loss (-12.4%) since Black Monday in 1987. But it has since attempted to rebound as shown later.

At the other end of the scale my gold holding shone brightly while the Thesis TM Tellworth UK Select also performed well, as is typical during equity slumps. Of course, both bond funds (namely abrdn High Yield Bond and Schroder Strategic Credit) finished the month in positive territory, benefiting from investors' flight to safety. Similarly the equity income funds within my portfolio outperformed the more growth orientated funds thanks to their more defensive sector positioning.

| Name | % return over the last month (since July's review) |

| iShares Physical Gold ETC | 3.59 |

| Thesis TM Tellworth UK Select | 1.29 |

| abrdn High Yield Bond | 0.83 |

| Schroder Strategic Credit | 0.74 |

| Aviva Inv Global Equity Income | -0.34 |

| Ninety One UK Special Situations | -1.23 |

| BNY Mellon Multi-Asset Balanced | -1.3 |

| Liontrust India | -2.62 |

| Artemis Global Income | -2.89 |

| Janus Henderson European Mid and Large Cap | -2.97 |

| Fidelity Index Japan | -5.62 |

| Artemis US Select | -5.66 |

| T. Rowe Price US Large Cap Growth Equity | -5.75 |

As usual, the table below shows which funds within my portfolio are in the current BOTB or BFBS tables and which are not. Those funds in blue are still in the BOTB while those in orange are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Fund | Allocation | Risk | Sector | ISIN |

| abrdn High Yield Bond | 14 | Lower | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11 | Medium | Global Equity Income | GB00B5N99561 |

| Artemis US Select | 5 | Medium | North America | GB00BMMV5105 |

| BNY Mellon Multi-Asset Balanced | 8 | Medium | Mixed Investment 40-85% Shares | GB00B8K9JZ06 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| Fidelity Index Japan | 5.5 | Medium | Japan | GB00BHZK8872 |

| iShares Physical Gold ETC | 5.5 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| Janus Henderson European Mid & Large Cap | 5 | Higher | Europe Excluding UK | GB00BJ0LFG67 |

| Liontrust India | 6 | Higher | India/Indian Subcontinent | GB00B1L6DV51 |

| Ninety One UK Special Situations | 5 | Higher | UK All Companies | GB00B1XFJS91 |

| Schroder Strategic Credit | 8 | Lower | Sterling Strategic Bond | GB00BJZ2ZC09 |

| T. Rowe Price US Large Cap Growth Equity | 11.5 | Higher | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Lower | Targeted Absolute Return | GB00BNY7YM73 |

The market slump means that five funds have fallen out of the BOTB and BFBS tables this month (and are coloured in red). These funds are:

- Artemis US Select

- BNY Mellon Multi-Asset Balanced

- Aviva Inv Global Equity Income

- Fidelity Index Japan

- T. Rowe Price US Large Cap Growth Equity

So on the basis that I will maintain my holdings in those funds that remain in the BOTB and BFBS tables (coloured blue and orange), I'll discuss each "red" fund in turn. My recent research piece "The lazy 80-20 Investor – update 2024" was timely as it reinforced the fact that knee-jerk reactions to market wobbles can be detrimental to your portfolio's long-term performance. In addition, the article as well as my portfolio's performance since inception, is evidence that it is important to stick to your investment process through all market conditions and not get distracted by fluctuations and news headlines. After all, the minor dip we've seen in recent weeks pales into insignificance compared to some of the bear market conditions I've invested through since I've been managing my portfolio (such as the pandemic crash).

On that note, looking first at my US equity funds, I plan to reduce my overall US equity exposure to be more in line with the asset mix of the BOTB. If you've read my analysis of August's BOTB you will know that the biggest change, in terms of asset mix, was the reduction in US equity exposure (falling from 29% to 16%) in favour of UK equities (which has risen from 12% to 24%). At the time I wrote that " it's been a long time since we've seen such a dramatic reversal in the asset mix on the BOTB but it does reflect the sudden change in fortunes between stock markets on either side of the Atlantic". Don't forget that was written even before the August slump in US equities. So sticking with the 80-20 Investor investment process I am going to reduce my US equity exposure and increase the UK equity exposure within my portfolio.

To achieve that I will maintain my Artemis US Select holding by reducing my T. Rowe Price US Large Cap Growth Equity exposure by 50%, with the proceeds going into the Schroder UK Smaller Companies fund, which has been a regular in the BOTB in recent months. In doing so I am reducing my concentration risk, by not having more than 5-6% in any of the three funds mentioned. It also takes some profit I've enjoyed from the AI stock rally off the table (Nvidia alone is the largest holding in T. Rowe Price US Large Cap Growth Equity at over 9% of the fund's assets). The chart below shows the profit I've made from the fund since I've held it versus its sector average.

It means that I still have exposure to both Artemis US Select and T. Rowe Price US Large Cap Growth Equity, but don't forget neither has become a bad fund overnight and they were both in the BOTB as recently as July (i.e. two weeks ago).

I introduced Aviva Inv Global Equity Income into my portfolio last month, and despite it now dropping out of the BOTB and BFBS tables it was the best performing equity fund within my portfolio during the last month especially during the stock market wobble. The fund benefited from investors rotating into more defensive equity sectors such as healthcare. As such, it is too soon to question the fund's inclusion in my portfolio.

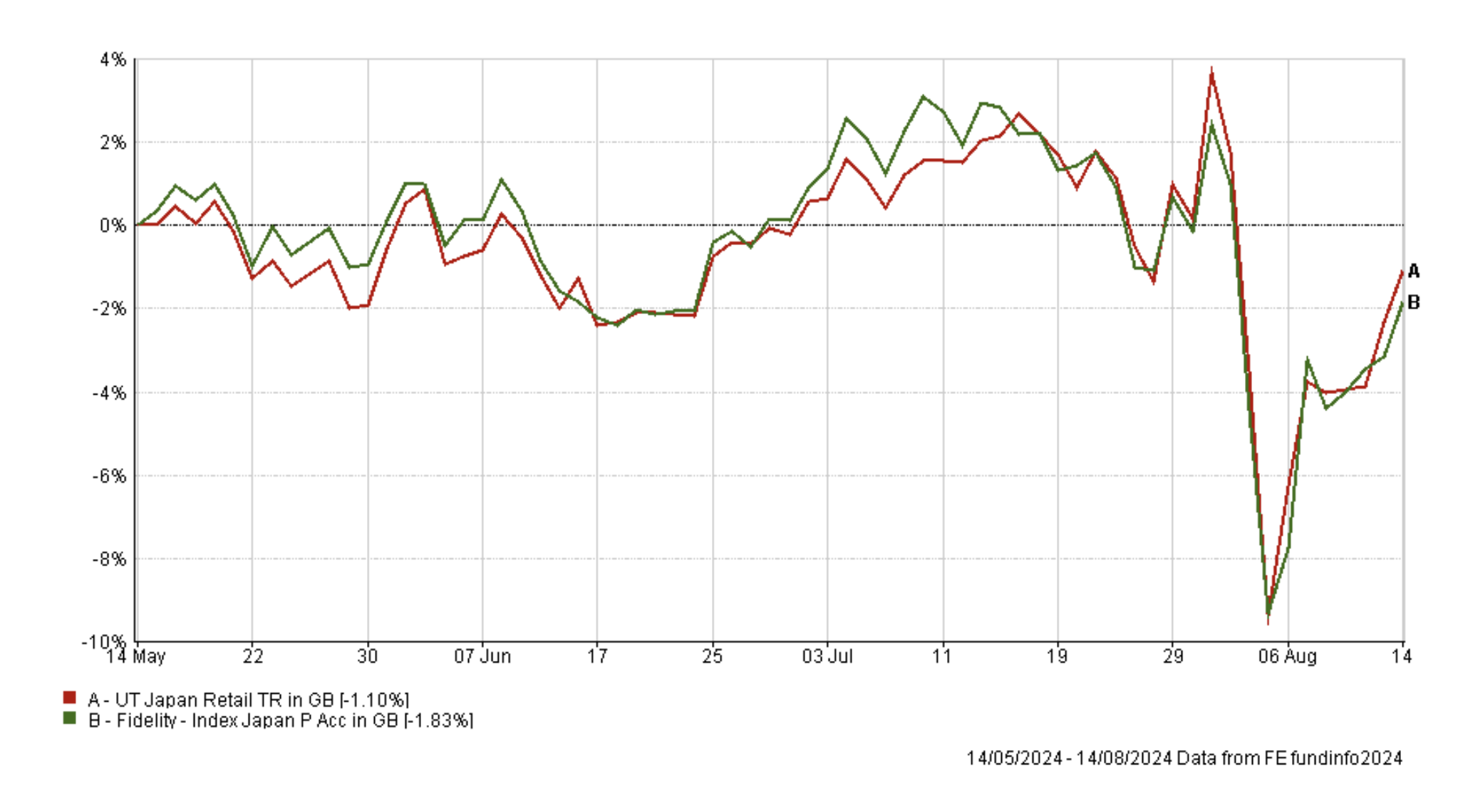

Fidelity Index Japan had a terrible month, which is reflective of the wider Japanese stock market slump. The chart shows the performance of the fund versus its sector average over the last 3 months.

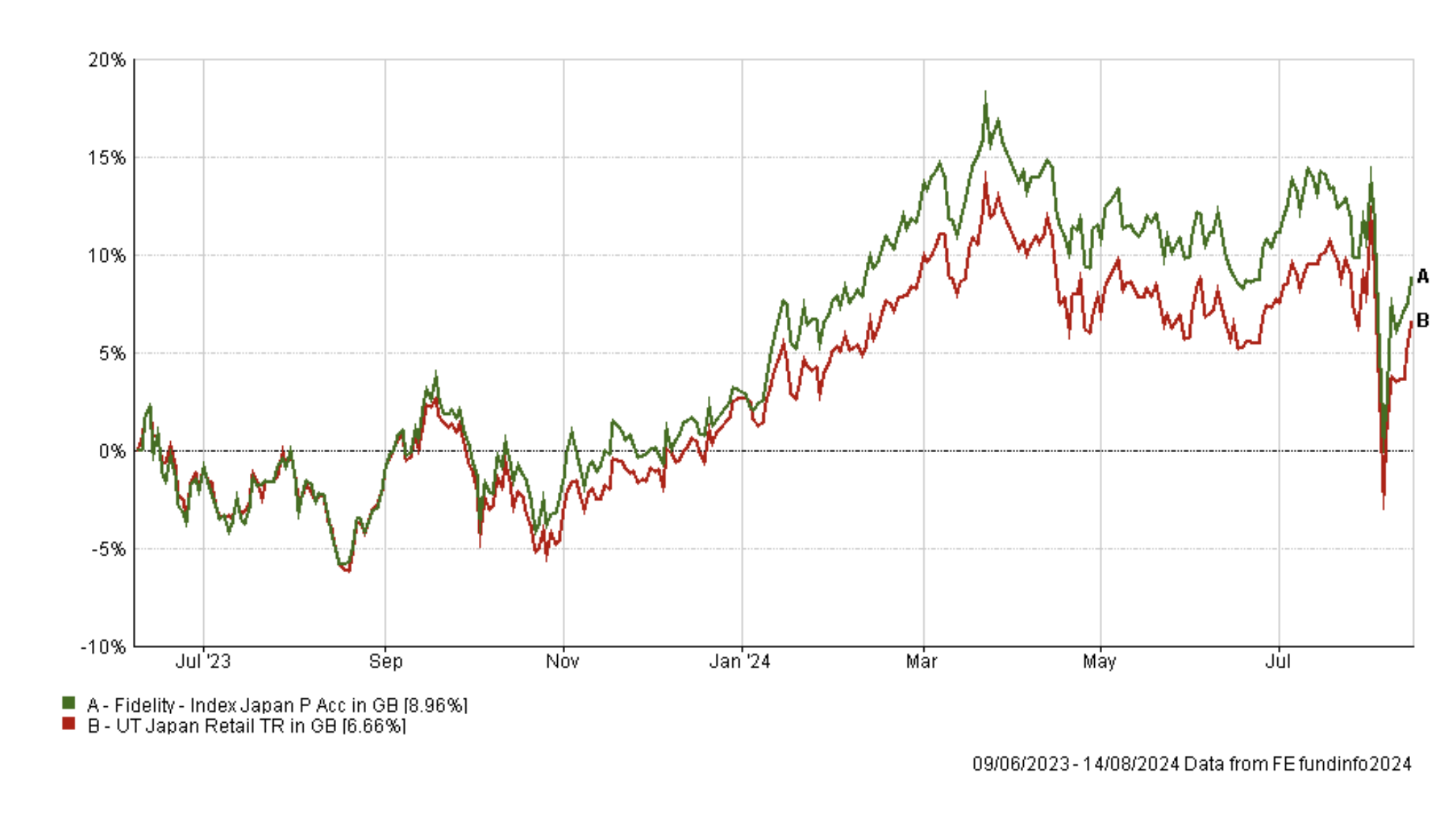

But if you go back over the time since I first held the fund, more than a year ago (see below), you can see that it has outperformed its peer group, but has lost momentum in the last few months along with the wider Japanese stock market. Given its drop from the BOTB and BFBS tables and the general downtrend that has started to emerge in Japanese equities, I will take some profits and sell half of my holding and use the proceeds to boost my UK equity exposure. I will invest the proceeds into Ninety One UK Special Situations which has been one of my stronger performers of late. The move will bring my Japanese exposure back down in line with that of the BOTB.

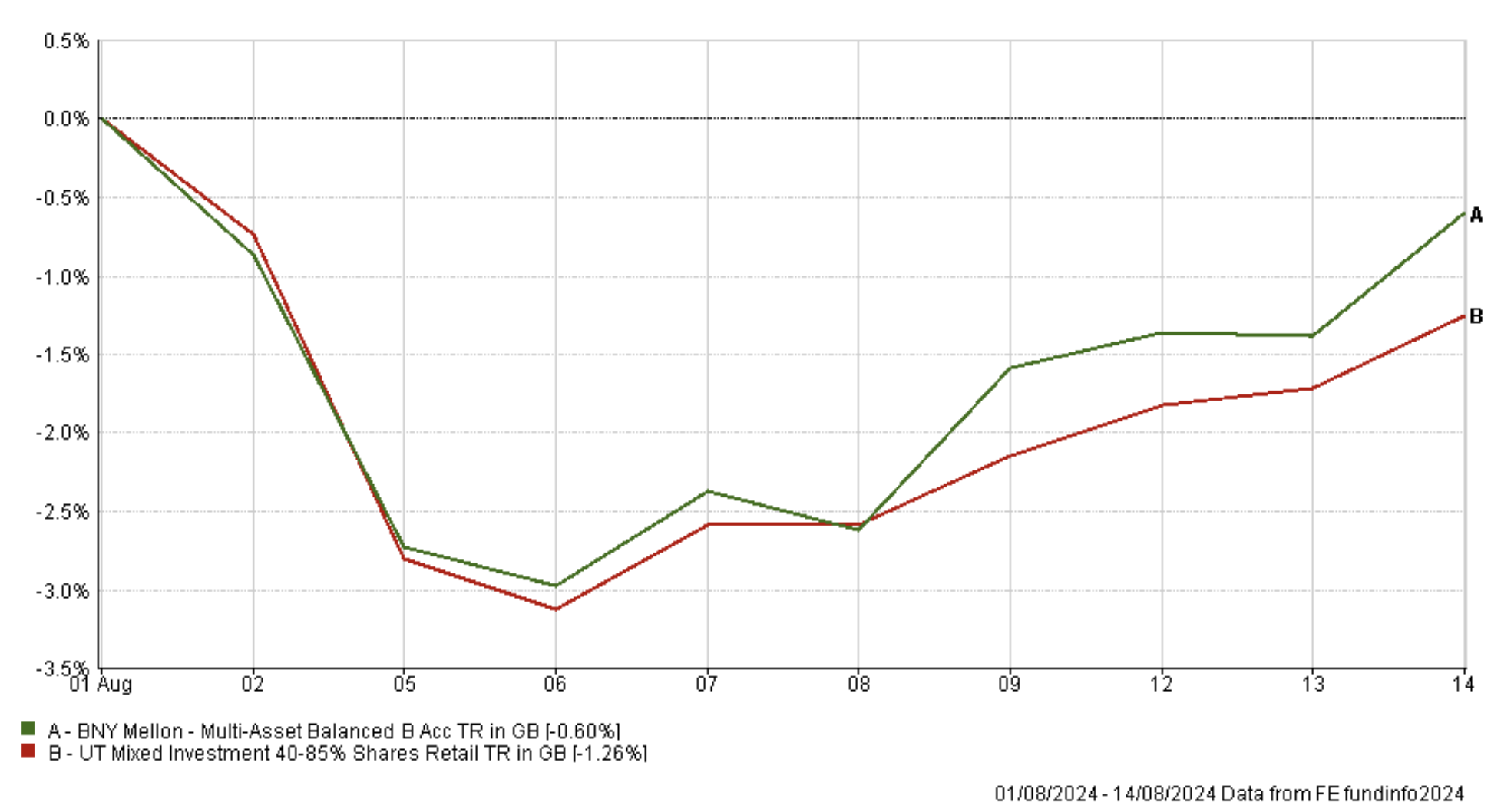

The final fund in the red list is BNY Mellon Multi-Asset Balanced, which is a fund whose consistency means that it clings onto its place in the core of my portfolio. Once again the multi-asset fund is in the top quartile of the performance tables over almost every timeframe for the Mixed Investment 40-85% Shares sector. While I don't focus on short-term time horizons, the chart below shows how the fund performed during the latest market slump versus its peer group average.

In periods of extreme volatility, such as we are experiencing now, it is prudent to keep portfolio changes to a minimum as markets could move against you while any fund switches are processed. BNY Mellon Multi-Asset Balanced continues to prove a stabiliser in my portfolio and with no alternatives in the current BOTB its removal would also require a restructure of my portfolio to ensure a diversified asset mix of global equities and bonds is maintained. So again, I will leave the fund as it is for now.

I have listed the two fund switches I am making this month below, which ultimately increase my UK equity exposure at the expense of US and Japanese equities, crystallising some profits along the way. The fund switches do mean that I have increased the number of funds in my portfolio to 14 which is a couple more than I would like, but I will look to consolidate my holdings over the coming months.

Fund switches

- 50% out of T. Rowe Price US Large Cap Growth Equity and 100% into the Schroder UK Smaller Companies

- 50% out of Fidelity Index Japan and 100% into the Ninety One UK Special Situations

My portfolio

My portfolio looks now like this:

| Fund | Allocation | Risk | Sector | ISIN Code |

| abrdn High Yield Bond | 14 | Low | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11 | Medium | Global Equity Income | GB00B5N99561 |

| Artemis US Select | 5 | Medium | North America | GB00BMMV5105 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| BNY Mellon Multi-Asset Balanced | 8 | Medium | Mixed Investment 40-85% Shares | GB00B8K9JZ06 |

| Fidelity Index Japan | 3 | Medium | Japan | GB00BHZK8872 |

| iShares Physical Gold ETC | 5.5 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| Janus Henderson European Mid and Large Cap | 4.5 | High | Europe Excluding UK | GB00BJ0LFG67 |

| Liontrust India | 6 | High | India/Indian Subcontinent | GB00B1L6DV51 |

| Ninety One UK Special Situations | 7.5 | High | UK All Companies | GB00B1XFJS91 |

| Schroder Strategic Credit | 8 | Low | Sterling Strategic Bond | GB00BJZ2ZC09 |

| Schroder UK Smaller Companies | 6 | High | UK Smaller Companies | GB00B76V7Z98 |

| T. Rowe Price US Large Cap Growth Equity | 6 | High | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Low | Targeted Absolute Return | GB00BNY7YM73 |

My Portfolio asset mix

My portfolio asset mix has approximately 68% exposure to equities. Last month's figures are shown in brackets.

-

- UK Equities 23% (14%)

- North American Equities 20% (26%)

- Asian/Emerging Market Equities 7% (7%)

- Japanese Equities 5% (8%)

- European Equities 12% (12%)

- Other International equity 1% (0%)

- Commodities and energy 5% (5%)

- UK Fixed Interest 5% (5%)

- Global Fixed Interest 18% (18%)

- Cash 1% (1%)

- Alternative Investment Strategies 3% (4%)

Damien's higher risk and lower risk portfolios

Using the logic described in my post: Update to Damien’s alternative risk portfolios I created hypothetical higher and lower risk versions of my portfolio below:

Lower risk

| Fund | Allocation % |

| abrdn High Yield Bond | 20 |

| Artemis Global Income | 16 |

| Artemis US Select | 7 |

| Aviva Inv Global Equity Income | 14 |

| BNY Mellon Multi-Asset Balanced | 11 |

| Fidelity Index Japan | 4 |

| iShares Physical Gold ETC | 8 |

| Schroder Strategic Credit | 12 |

| Thesis TM Tellworth UK Select | 8 |

Higher risk

| Fund | Allocation % |

| Artemis Global Income | 15 |

| Artemis US Select | 7 |

| Aviva Inv Global Equity Income | 14 |

| BNY Mellon Multi-Asset Balanced | 11 |

| Fidelity Index Japan | 4 |

| iShares Physical Gold ETC | 8 |

| Janus Henderson European Mid & Large Cap | 6 |

| Liontrust India | 8 |

| Ninety One UK Special Situations | 10 |

| Schroder UK Smaller Companies | 8 |

| T. Rowe Price US Large Cap Growth Equity | 9 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay