The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

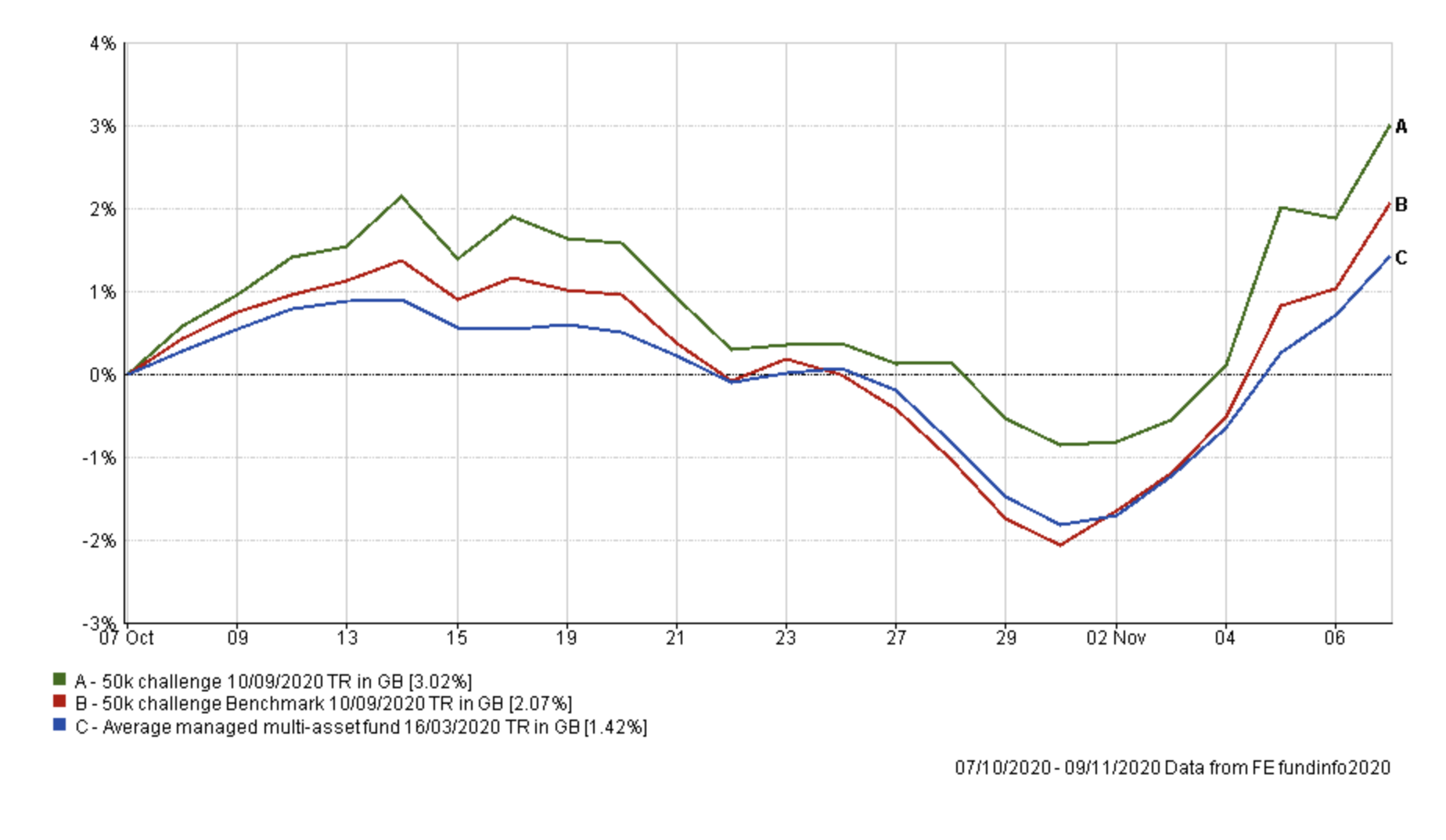

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015, which is over five and a half years ago. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

You can see how my portfolio has once again extended its lead over its benchmarks since my last portfolio review. The chart below shows the portfolio's performance since my last review.

My portfolio review last month was a tricky one, given the imminent market-moving events including the US election, Brexit and of course the constant backdrop of COVID-19. It is well worth going back and re-reading. But to summarise, at the time I decided that... "with a sense of déjà vu it therefore seems that the most sensible choice is to follow the course of action that proved successful last time around, which is to do nothing for now."

Obviously this was an uncomfortable choice emotionally, especially given the hammering that technology stocks took in the week ahead of the US election. At the time everyone predicted doom and gloom for technology stocks as well as government bonds (i.e gilts) after the election. As I explained in my weekly newsletter published in the aftermath of the US election the "smart money" had bet heavily on a Blue wave in the US election, which meant placing big bets against technology stocks and government debt. When the Blue wave didn't materialise the "smart money" panicked and rushed to buy government bonds and technology stocks. This propelled my portfolio to new all-time highs, as can be seen from the chart above. Trying to predict the future is a dangerous game and by sticking to my investing process I benefited. I had no special foresight on what would happen so I didn't try to second guess what the market would do.

Now comes the interesting bit... all of the above was written before Monday's COVID-19 vaccine news broke. I don't need to dwell on the details but it is safe to say that if a COVID-19 vaccine with a 90% effectiveness is soon available it will be a game-changer. It's potentially the antithesis of the Black Swan event that hit markets back in February when the pandemic took hold (perhaps it should be called a White Swan?).

In November's newsletter I wrote that the trend is your friend until it's not and that it pays to be humble. Little did I realise how apt the words would be less than 48 hours later when investment markets were turned on their heads. I will write about it in more detail in this weekend's newsletter, but we witnessed one of the biggest two-day changes in momentum that we've ever seen. I've updated both of the earlier charts (see below) to show the impact of the market reversal. Firstly the performance since last month:

and the performance since I began running my portfolio:

You can see the sizeable one day move as a result of the vaccine news in the first chart, but so far the move is still not that significant in the context of the portfolio's outperformance over the last five and half years. The question of course becomes, is this the start of a long term market change? Has the momentum that's been driving markets been turned on its head permanently? Of course I don't have the answer. So instead I will stick to the process that has fared me well over the last five and a half years.

As is the routine in my portfolio reviews, the table below shows which funds within my portfolio are in the current BOTB or BFBS tables and which are not. Those funds in green are still in the BOTB while those in orange are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code |

| Baillie Gifford European | 5 | High | Europe Excluding UK | GB0006058258 |

| Schroder Global Healthcare | 7.5 | Medium | Global | GB00B76V7Q08 |

| Baillie Gifford Long Term Global Growth Investment | 9 | High | Global | GB00BD5Z0Z54 |

| VT Gravis Clean Energy Income | 5.5 | Medium | Global | GB00BFN4H792 |

| Premier Diversified Growth | 9 | Medium | Mixed Investment 40-85% Shares | GB00B8BJV423 |

| Royal London UK Government Bond | 15 | Medium | UK Gilts | GB00B881TW52 |

| Allianz Strategic Bond | 16.5 | Low | Sterling Strategic Bond | GB00B06T9362 |

| Troy Asset Management Ltd Trojan Ethical | 10.5 | Medium | Flexible Investment | GB00BJP0XX17 |

| Baillie Gifford Positive Change | 5.5 | High | Global | GB00BYVGKV59 |

| Liontrust Sustainable Future Cautious Managed | 5 | Medium | Mixed Investment 40-85% Shares | GB00BMN90304 |

| iShares Physical Gold ETC | 5.5 | Medium | Commodity & Energy ETF | - |

| Allianz Total Return Asian Equity | 3 | Medium | Asia Pacific Excluding Japan | GB00B1FRQV53 |

| JPM Japan | 3 | Medium | Japan | GB00B1XMTP77 |

The only real change from the last time I reviewed my portfolio is that the Allianz Strategic Bond fund has dropped out of the BOTB (but remains in the BFBS tables) while the Royal London UK Government Bond has now dropped out of the BFBS completely.

Although I didn't make any changes to my portfolio last time around I wrote that..."I would normally consider increasing the equity exposure of my own portfolio to be more in line with the BOTB (now at 60% versus 48% for my portfolio), perhaps looking to reduce my exposure to technology stocks which have had a fantastic run. But with my portfolio's concentrated exposure to US equities and technology stocks I think it prudent to offset this by again maintaining my portfolio's overall equity exposure as it is for now (i.e. lower than that of the BOTB's 60% right now). That means maintaining my gilt exposure too, but as my recent research piece identified it is a good diversifier for my US tech holdings".

Interestingly this month's portfolio review coincided with receiving stop loss alerts for four funds within my portfolio, namely:

- Baillie Gifford Positive Change

- Baillie Gifford Long Term Global Growth

- Baillie Gifford European

- JPM Japan

These were all triggered by the rotation out of growth (especially tech stocks) into value sectors (such as financials) caused by the news of a COVID-19 vaccine.

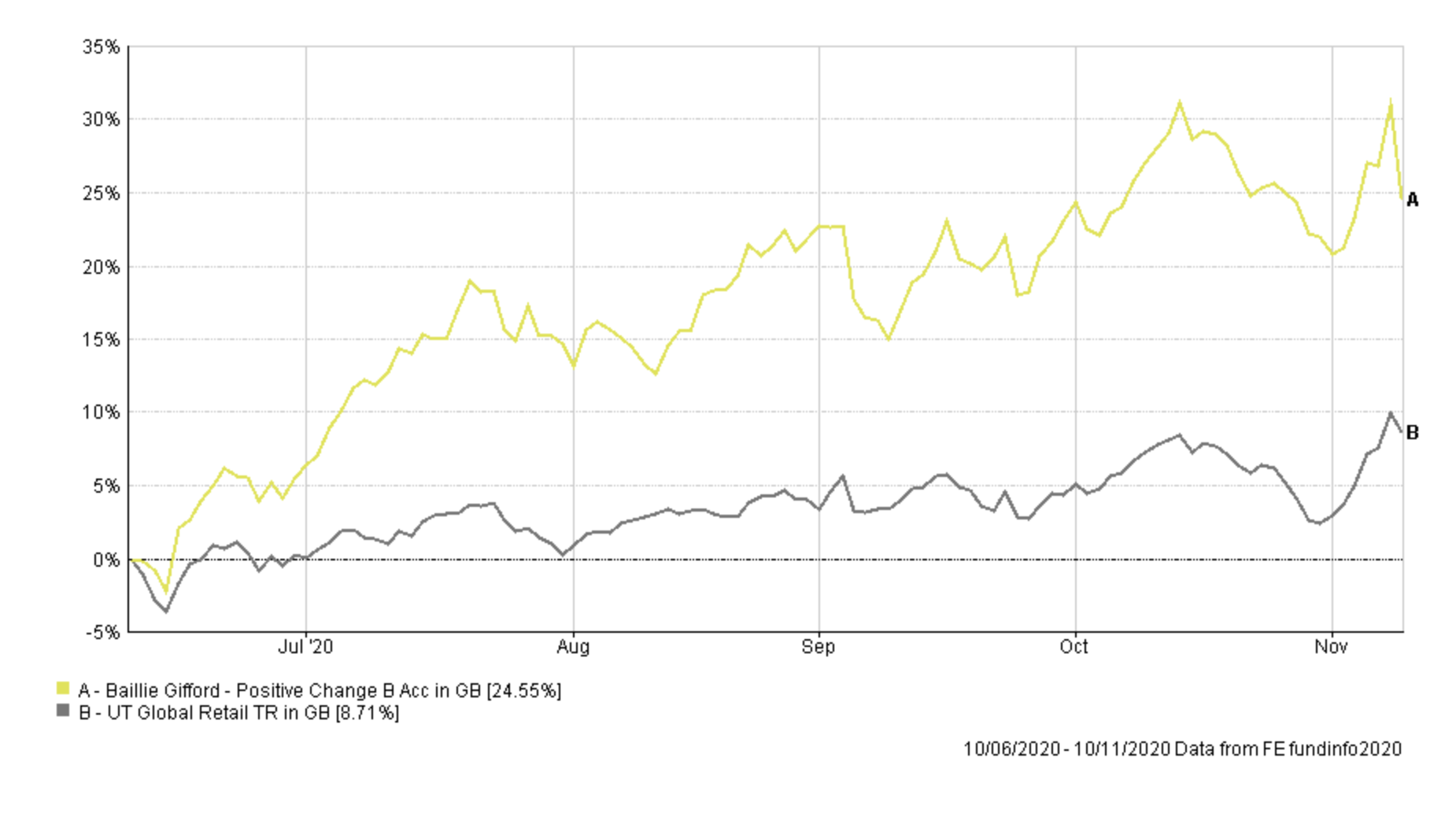

Big US tech and Asian tech companies have had a stellar run this year. The charts below show you the eye-watering profit I've made from my Baillie Gifford Long Term Global Growth and Baillie Gifford Positive Change holdings versus their peer group. The Baillie Gifford Long Term Global Growth funds is up over 43% since May and that's even after Tuesday's sell-off (as you can see). Before that it was up over 50%.

Similarly, the Baillie Gifford Positive Change change fund has been a stellar performer since I've owned it.

These funds helped drive my portfolio to new all-time highs despite my portfolio only having a 48% equity allocation. It's rare that a White Swan event, stop loss alerts and my portfolio review all align at the same time. Perhaps it is quite fortuitous. However, despite the turn of events since Monday, the longer-term momentum trends remain intact for now, although admittedly potentially under threat. It obviously does pose an issue. If I were to increase my equity exposure now, choosing funds from the BOTB and BFBS tables, which would I choose given that their momentum was all derived pre-vaccine? It's an impossible question given that there is a long way still to go in securing a reliable vaccine. On the face of it nothing has changed since last week as COVID-19 is still here, it's just that optimism has increased that an end is in sight. There are already signs that the initial vaccine enthusiasm is starting to fizzle out and tech stocks rebounding.

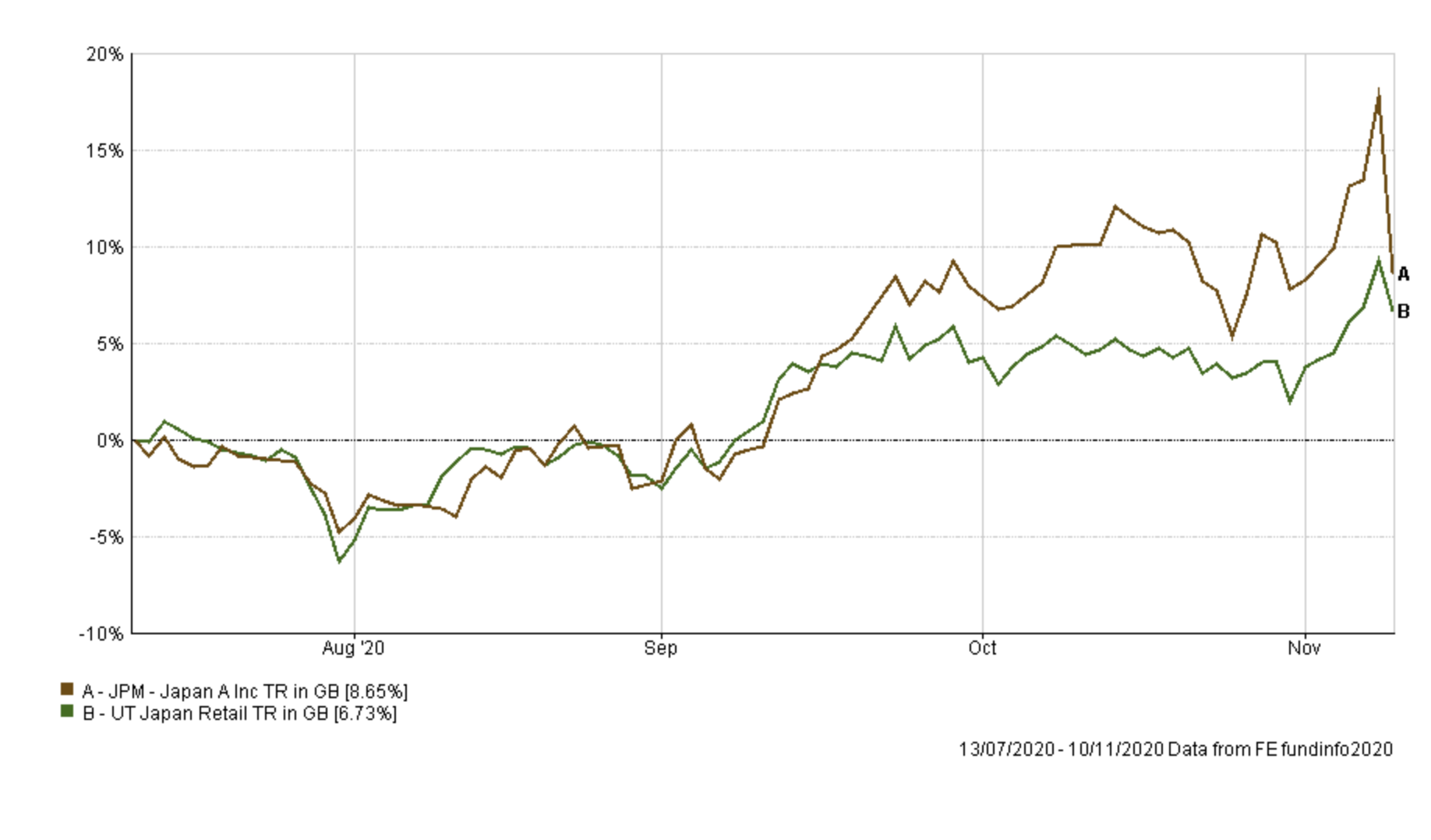

Given such uncertainty, it is perhaps wise to do little to my portfolio until we see the lie of the land. However, I am sticking to my previous plan of taking some profits from my exposure to technology stocks while at the same time getting ready to increase my portfolio's overall equity exposure to be more in line with that of the BOTB. So to achieve my aim I will halve my exposure to both the Baillie Gifford Long Term Global Growth and Baillie Gifford Positive Change and then redeploy them elsewhere. I will also take some profits on my Baillie Gifford European fund and JPM Japan fund. Both have significant-tech exposure too. In fact, as an investment house, Baillie Gifford is known for favouring technology, which is why you will have seen many of its funds struggle in this week's see-saw. The charts below show how both the Baillie Gifford European fund and JPM Japan fund have outperformed their sectors since I've held them.

JPM outperformance:

Baillie Gifford European outperformance:

Looking at the rest of my portfolio, despite this month's BOTB finally having some gilt exposure (albeit only around 4% of total assets) I had been planning to remove my exposure to the Royal London UK Government Bond altogether. Gilt yields have been spiralling in recent weeks and the fund is no longer providing the downside protection it once did. Coincidentally gilts and treasuries performed badly in this week's vaccine euphoria as optimism over future economic growth increased. But as I am reducing my technology exposure the diversification benefit of holding gilts, something that I mentioned last time, is somewhat reduced. But ultimately the fund's absence from the 80-20 Investor tables is its undoing and by removing it from my portfolio I can use the proceeds to increase my portfolio's equity content slightly

When I look at the other funds that are coloured in red in the earlier table I am loathed to change my global equity exposure just yet. The VT Gravis Clean Energy fund has continued to perform well in the short term. In fact the fund appeared in the BFBS list just a week ago. The Schroder Global Healthcare fund has also been performing adequately and only dropped out of the BOTB at the start of September. And while I might want to change things up a bit among those funds highlighted red, with markets this volatile (and rallying as strongly as they are) it seems more prudent to leave my global equity exposure alone for now. Sometimes it's better to remain invested. Furthermore, both these funds were among the best performers (along with Premier Diversified Growth, Troy Asset Management Ltd Trojan Ethical and Liontrust Sustainable Future Cautious Managed) this week. What we saw in the wider market (with recent laggards suddenly becoming today's winner post-vaccine news) was reflected in my portfolio. So those funds that had been losing momentum and were at risk of being removed were the best performers in recent days.

So to sum up I am reducing my technology exposure slightly, shuffling the decks and ever so slightly increasing the overall equity exposure of my portfolio to compensate. I am reducing the portfolio's over-reliance on the performance of tech stocks and gilts. Ultimately I am leaving most of the portfolio alone until we see how the vaccine news impacts markets going forward. There is nothing to stop me reviewing my portfolio again in the coming weeks if momentum shifts significantly. At present all the old trends are still intact and the new portfolio is more of a reshuffle. In fact if you backtested the performance of the new portfolio vs the old one the performance over the last six months is almost identical, but without as severe drawdowns when technology stocks occasionally wobbled.

Below I list the fund changes for November with more detail provided beneath each switch.

Fund switch 1

50% out of Baillie Gifford Positive Change and 100% into Sarasin Global Dividend

The Sarasin Global Dividend fund is in the BFBS tables. I picked it because it has a value focus (you can check this on Morningstar) rather than a growth focus but has also been a good momentum play (hence why it is in the BFBS table). Choosing this fund helps introduce some value/cyclical exposure into my portfolio

Fund switch 2

50% out of Baillie Gifford Long Term Global Growth and 100% into VT Gravis Clean Energy fund

This is a case of backing one the best performers in recent months within my portfolio, that isn't tech-focussed.

Fund switch 3

100% out of Royal London UK Government Bond and 40% into Sarasin Global Dividend and 60% into Fidelity Global High Yield

The Fidelity Global High yield fund is in this month's BOTB and like most high yield funds its fortunes are often closely entwined with equities.

Fund switch 4

30% out of into Baillie Gifford European and into cash

Fund switch 5

30% out of into JPM Japan and into cash

This means that my new portfolio looks like:

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code |

| Baillie Gifford European | 3.5 | High | Europe Excluding UK | GB0006058258 |

| Schroder Global Healthcare | 7.5 | Medium | Global |

GB00B76V7Q08

|

| Baillie Gifford Long Term Global Growth Investment | 5 | High | Global |

GB00BD5Z0Z54

|

| VT Gravis Clean Energy Income | 11 | Medium | Global |

GB00BFN4H792

|

| Premier Diversified Growth | 9.5 | Medium | Mixed Investment 40-85% Shares | GB00B8BJV423 |

| Allianz Strategic Bond | 16 | Low | Sterling Strategic Bond | GB00B06T9362 |

| Troy Asset Management Ltd Trojan Ethical | 10 | Medium | Flexible Investment |

GB00BJP0XX17

|

| Baillie Gifford Positive Change | 3 | High | Global |

GB00BYVGKV59

|

| Liontrust Sustainable Future Cautious Managed | 5 | Medium | Mixed Investment 40-85% Shares |

GB00BMN90304

|

| iShares Physical Gold ETC | 5 | Medium | Commodity & Energy ETF | - |

| Allianz Total Return Asian Equity | 3 | Medium | Asia Pacific Excluding Japan |

GB00B1FRQV53

|

| JPM Japan | 2.5 | Medium | Japan |

GB00B1XMTP77

|

| Fidelity Global High Yield | 8 | Low | Sterling High Yield |

GB00B7K7SQ18

|

| Sarasin Global Dividend | 8.5 | Medium | Global Equity Income |

GB00BGDF8F44

|

| Cash | 2.5 | Low |

One thing you will notice is that the number of holdings is much higher than normal and there is a small cash holding. That's because this is very much an interim portfolio awaiting more clarity over market momentum in the coming weeks. The portfolio hadn't been changed in a number of months and so we don't want to throw the baby out with the bathwater when it had been performing so well. In the future, I will look to deploy the small amount of cash in the portfolio and consolidate my holdings and increase my equity content further. It's a work in progress, much like the vaccine.

My Portfolio asset mix

My portfolio asset mix is as shown below which is now around 52 to 53% equities (up from 48%). Last month's asset mix is shown in brackets. As it is a work in progress the asset mix is different from the current BOTB, with less Chinese equity exposure and more global fixed interest exposure being the biggest differences.

-

- UK Equities 5% (5%)

- North American Equities 19% (20%)

- Global Fixed Interest 27% (23%)

- Japanese Equities 3% (4%)

- European Equities 9% (11%)

- UK Fixed Interest 0% (0%)

- UK Gilt 0% (13%)

- Cash 5% (4%)

- Alternative Investment Strategies 11% (7%)

- Asian Equities 3% (3%)

- Emerging Market Equities 2% (3%)

- Commodities and energy 11% (7%)

- Property 0% (0%)

- Other equity 5% (0%)

Damien's higher risk and lower risk portfolios

Using the logic described in my post: Update to Damien’s alternative risk portfolios I created hypothetical higher and lower risk versions of my portfolio below:

Higher risk

| Fund | Allocation |

| Baillie Gifford European | 5 |

| Schroder Global Healthcare | 10 |

| Baillie Gifford Long Term Global Growth Investment | 7 |

| VT Gravis Clean Energy Income | 15 |

| Premier Diversified Growth | 13 |

| Troy Asset Management Ltd Trojan Ethical | 13 |

| Baillie Gifford Positive Change | 4 |

| Liontrust Sustainable Future Cautious Managed | 7 |

| iShares Physical Gold ETC | 7 |

| Allianz Total Return Asian Equity | 4 |

| JPM Japan | 3 |

| Sarasin Global Dividend | 12 |

Lower risk

| Fund | Allocation |

| Schroder Global Healthcare | 8 |

| VT Gravis Clean Energy Income | 12 |

| Premier Diversified Growth | 11 |

| Allianz Strategic Bond | 18 |

| Troy Asset Management Ltd Trojan Ethical | 11 |

| Liontrust Sustainable Future Cautious Managed | 6 |

| iShares Physical Gold ETC | 6 |

| Allianz Total Return Asian Equity | 3 |

| JPM Japan | 3 |

| Fidelity Global High Yield | 9 |

| Sarasin Global Dividend | 10 |

| Cash | 3 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay