The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

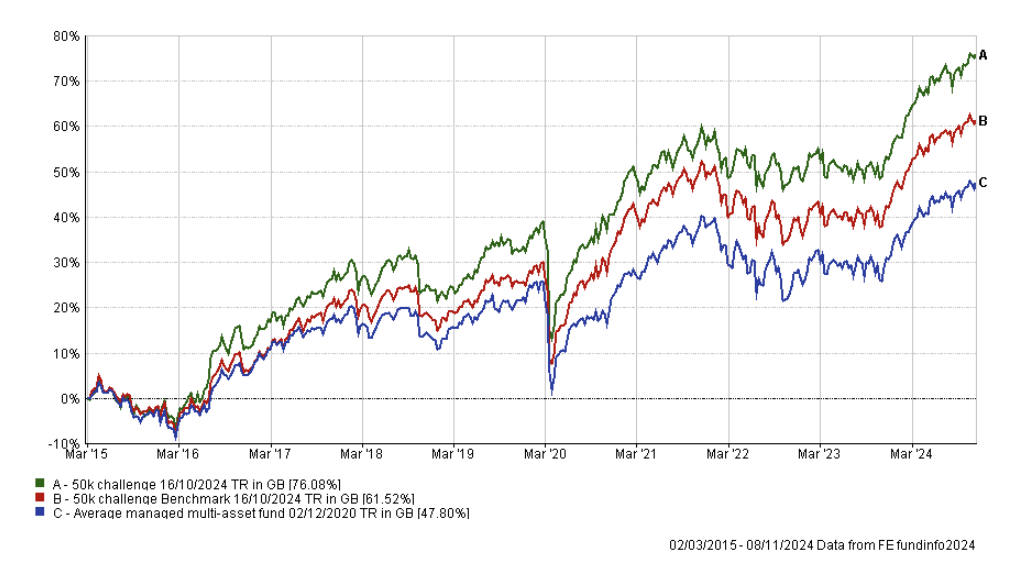

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

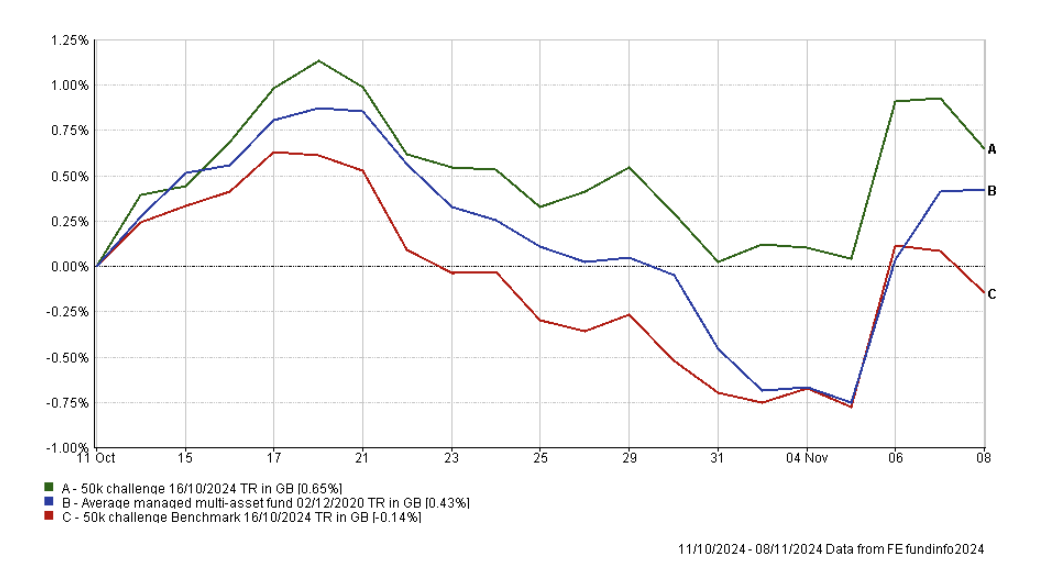

You can see how my portfolio continues to significantly outperform its benchmarks despite elevated volatility, mostly as a result of the US election. The chart below shows the performance of my portfolio versus its benchmarks since my last review a month ago.

The table below shows how individual funds performed within my portfolio during the period. US large caps and gold all enjoyed strong months once again, with the US election result and currency moves helping maintain their momentum from the previous month. At the opposite end of the scale, emerging market, Asian and European equities struggled. The latter has been particularly impacted by concerns over the outlook for the European economy but also by the fall in the value of the euro versus the pound.

| Name | % return over the last month (since October review) |

| T. Rowe Price US Large Cap Growth Equity | 5.29 |

| Artemis Global Income | 2.65 |

| iShares Physical Gold ETC | 2.65 |

| Thesis TM Tellworth UK Select | 1.27 |

| Barclays Global Markets Adventurous | 1.09 |

| abrdn High Yield Bond | 0.67 |

| Schroder UK Smaller Companies | 0.64 |

| Schroder Strategic Credit | 0.37 |

| Aviva Inv Global Equity Income | -0.05 |

| Fidelity Index Japan | -1.04 |

| FSSA Asia Focus | -1.58 |

| Ninety One UK Special Situations | -1.81 |

| Liontrust India | -2.81 |

| Schroder European Recovery | -4.62 |

As usual, the table below shows which funds within my portfolio are in the current BOTB or BFBS tables and which are not. Those funds in blue are still in the BOTB while those in orange are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Fund | Allocation | Risk | Sector | ISIN |

| abrdn High Yield Bond | 14 | Lower | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11 | Medium | Global Equity Income | GB00B5N99561 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| Barclays Wealth Wealth Global Markets 5 | 8 | Medium | Flexible Investment | GB00B4YPY060 |

| Fidelity Index Japan | 3 | Medium | Japan | GB00BHZK8872 |

| FSSA Asia Focus | 5 | Higher | Asia Pacific Excluding Japan | GB00BWNGXJ86 |

| iShares Physical Gold ETC | 5.5 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| Liontrust India | 6 | Higher | India/Indian Subcontinent | GB00B1L6DV51 |

| Ninety One UK Special Situations | 7.5 | Higher | UK All Companies | GB00B1XFJS91 |

| Schroder European Recovery | 4.5 | Higher | Europe Excluding UK | GB0007221889 |

| Schroder Strategic Credit | 8 | Lower | Sterling Strategic Bond | GB00BJZ2ZC09 |

| Schroder UK Smaller Companies | 6 | Higher | UK Smaller Companies | GB00B76V7Z98 |

| T. Rowe Price US Large Cap Growth Equity | 6 | Higher | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Lower | Targeted Absolute Return | GB00BNY7YM73 |

This month four funds are coloured red but the diversification within my portfolio has helped its overall performance once again.

Below is a list of the 'red' funds that have fallen out of both the BOTB and BFBS tables (the funds in bold were also in last month's red list):

- FSSA Asia Focus

- Fidelity Index Japan

- Schroder European Recovery

- Ninety One UK Special Situations

Looking at FSSA Asia Focus, the fund is a newcomer to the portfolio but has had a tough time. A combination of the market's disappointment at the level and pace of Chinese economic stimulus measures along with the stronger US dollar have put significant pressure on the fund, especially given its exposure to Chinese equities. Asian and emerging market equities as an asset class have come under pressure more widely, a trend not helped by the market movements since the US election. However, the BOTB was chosen before the US election and its asset allocation reflects the shift in sentiment away from Emerging/Asian equities which was already in motion. The November BOTB includes a small direct Chinese equity exposure but has a reduced emerging market equity exposure, when compared to October's BOTB.

If I am to try and reflect the shift in the BOTB asset mix then I need to reduce my Asian equity and emerging market equity exposure by selling the FSSA Asia Focus, which is one of the smallest holdings in my portfolio. This will also only crystallise a relatively small loss (at the time of writing) although that is never a factor in my decision making process.

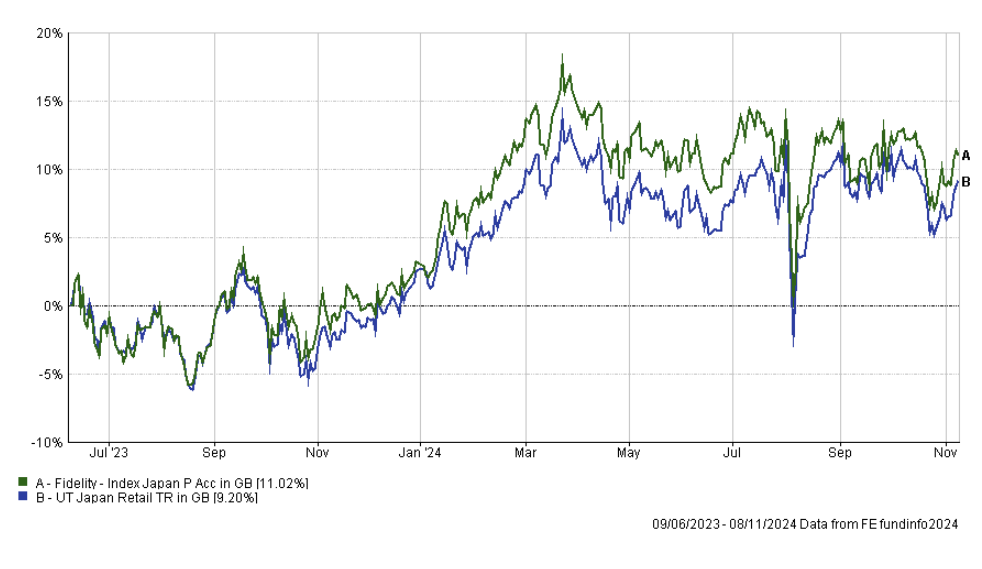

Fidelity Index Japan has enjoyed something of a rebound since the US election, thanks to the surging US dollar. Consequently the weaker yen vs the dollar has been a boost for the share prices of Japanese exporters and therefore the wider Japanese stock market. The first chart below shows the performance of the fund since I first held it back in June 2023.

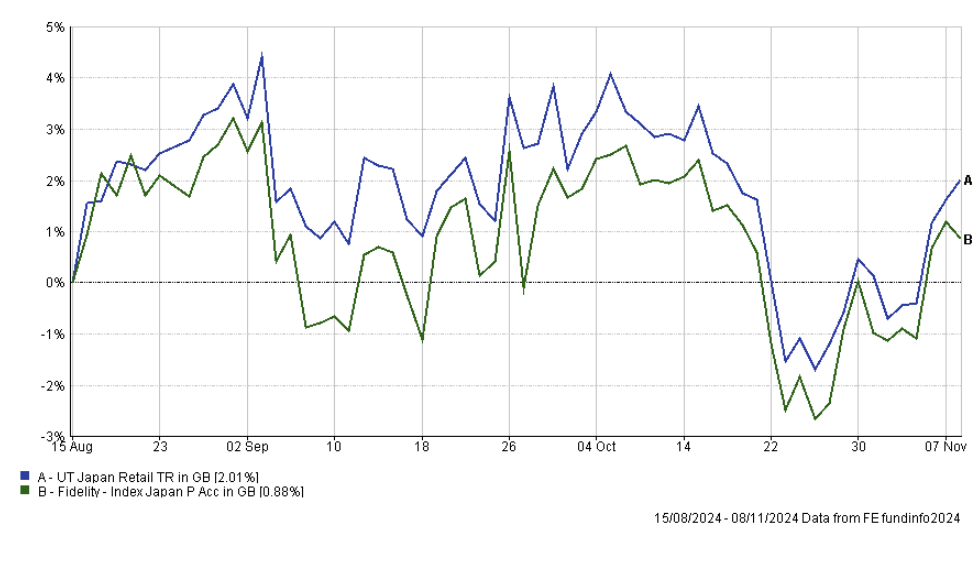

The chart below shows the performance of the fund since I halved my allocation to it back in August. As you can see it's been very volatile and has just broken back into positive territory.

Given the volatile nature of Japanese equities and the small exposure in my portfolio I will hold off making a change to this fund, as there are more pressing areas that I wish to change. It does mean that my Japanese equity exposure is higher than that of the BOTB but, as mentioned, I have already reduced it in recent months. As the fund was in the BFBS tables as recently as a few weeks ago I will place this fund on my watchlist for next month and review its position then.

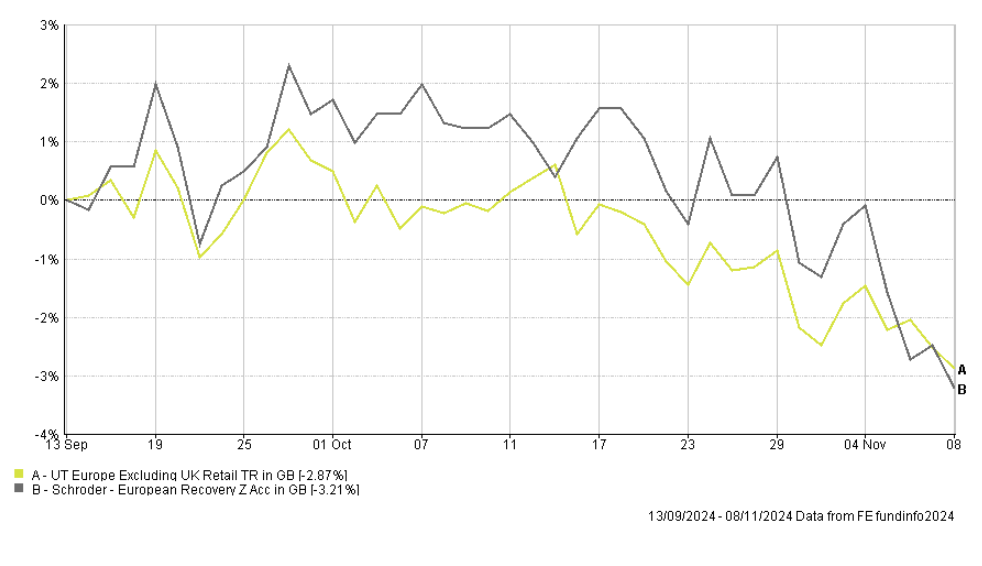

That leaves Schroder European Recovery and Ninety One UK Special Situations which have both been on the red list since last month, and their performance suggests that their momentum continues to falter. With regard to Schroder European Recovery, it had been performing strongly versus its peer group average, as shown in the chart below. However, a combination of the US election result, concerns over economic growth in the eurozone and a weakening euro have dampened the appeal of the asset class as a whole. My portfolio's European equity exposure has been significantly higher than that of the BOTB for some time. By removing this fund from my portfolio it brings my asset mix more in line with that of the BOTB while pruning one of the funds that has been on the red list for a while.

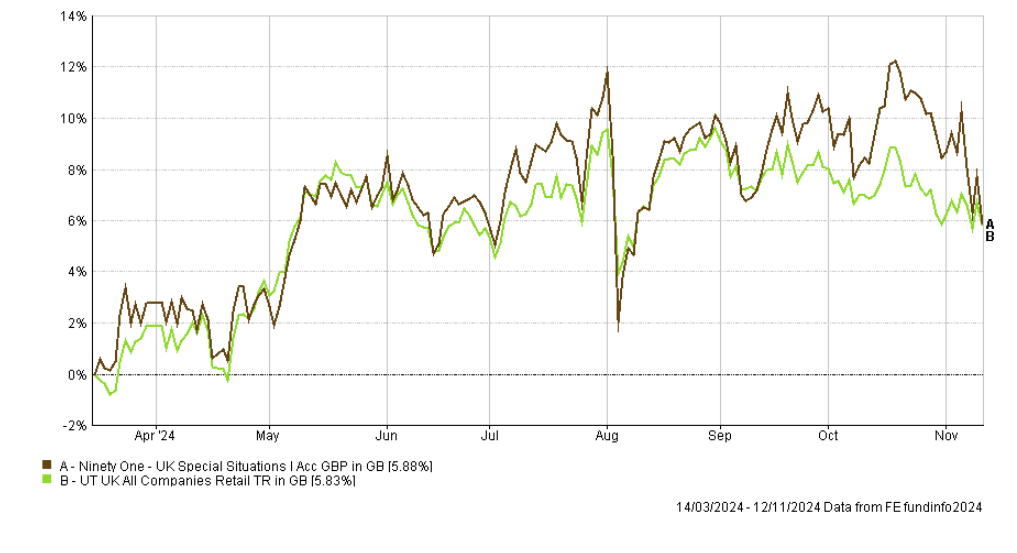

It is a similar story with Ninety One UK Special Situations. The chart below shows the fund's performance since I originally introduced it into the portfolio back in March. On the whole it performed in line with its peer group average until mid-September when it began outperforming significantly, only to give up those gains from mid-October. Given its recent performance, the fact that it remains on the red list and my desire to reduce my UK equity exposure to be more in line with that of the BOTB (which has also reduced its UK exposure in favour of US equities) I want to reduce my exposure to the fund. Having said that, my latest Winter Portfolio update suggests that we could be heading into a positive period for the fund, although it doesn't feel like it right now. Taking all of that into account I will reduce my holding in Ninety One UK Special Situations by 50% and use the proceeds to bolster my US equity exposure.

The other holdings within my portfolio remain in the BOTB and the BFBS tables so I plan to maintain them as they are for now. I have listed the three fund switches I am making this month below. These will increase my US equity exposure to be in line with that of the BOTB while reducing the number of holdings within my portfolio, something I have been looking to do for some time. You will notice that the last of the listed fund switches achieves my aim of reducing my UK equity exposure and increasing my US equity exposure, while at the same time trimming one of my worst performing positions and backing one of the best performing in recent months. US equities will once again be the largest asset allocation within my portfolio (hence this article's title).

Meanwhile, Vanguard FTSE Developed World ex-U.K. Equity Index Fund, which sits in this month's BOTB, helps give my portfolio exposure to equities globally (with a US bias), with less of an emphasis on European and Asian/emerging market equities.

Even after these changes the asset mix of my portfolio still slightly differs from that of the BOTB, mainly because I will still have a greater exposure to Japanese and European equities. However, it is an improvement on where the portfolio was, but I am happy to shift my portfolio's asset mix over time.

Fund switches

- 100% out of FSSA Asia Focus and 100% into the Vanguard FTSE Developed World ex-U.K. Equity Index Fund

- 100% out of Schroder European Recovery and 100% into the Vanguard FTSE Developed World ex-U.K. Equity Index Fund

- 50% out of Ninety One UK Special Situations and 100% into T. Rowe Price US Large Cap Growth Equity

My portfolio

My portfolio looks now like this:

| Fund | Allocation | Risk | Sector | ISIN Code |

| abrdn High Yield Bond | 14 | Lower | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11.5 | Medium | Global Equity Income | GB00B5N99561 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| Barclays Wealth Wealth Global Markets 5 | 8 | Medium | Flexible Investment | GB00B4YPY060 |

| Fidelity Index Japan | 3 | Medium | Japan | GB00BHZK8872 |

| iShares Physical Gold ETC | 5.5 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| Liontrust India | 6 | Higher | India/Indian Subcontinent | GB00B1L6DV51 |

| Ninety One UK Special Situations | 3.75 | Higher | UK All Companies | GB00B1XFJS91 |

| Schroder Strategic Credit | 8 | Lower | Sterling Strategic Bond | GB00BJZ2ZC09 |

| Schroder UK Smaller Companies | 5.5 | Higher | UK Smaller Companies | GB00B76V7Z98 |

| T. Rowe Price US Large Cap Growth Equity | 9.75 | Higher | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Lower | Targeted Absolute Return | GB00BNY7YM73 |

| Vanguard FTSE Developed World ex-UK Equity Index | 9.5 | Medium | Global | GB00B59G4Q73 |

My Portfolio asset mix

My portfolio asset mix has approximately 66% exposure to equities. Last month's figures are shown in brackets.

-

- UK Equities 17% (21%)

- North American Equities 24% (14%)

- Asian Equities 2% (5%)

- Chinese Equities 0% (1%)

- Emerging Market Equities 5% (8%)

- Japanese Equities 5% (4%)

- European Equities 8% (11%)

- Other International equity 5% (2%)

- Commodities and energy 6% (5%)

- UK Fixed Interest 4% (4%)

- Global Fixed Interest 18% (18%)

- Cash 0% (2%)

- Alternative Investment Strategies 6% (5%)

Damien's higher risk and lower risk portfolios

Using the logic described in my post: Update to Damien’s alternative risk portfolios I created hypothetical higher and lower risk versions of my portfolio below:

Lower risk

| Fund | Allocation % |

| abrdn High Yield Bond | 19 |

| Artemis Global Income | 15 |

| Aviva Inv Global Equity Income | 13 |

| Barclays Wealth Wealth Global Markets 5 | 11 |

| Fidelity Index Japan | 4 |

| iShares Physical Gold ETC | 7 |

| Schroder Strategic Credit | 11 |

| Thesis TM Tellworth UK Select | 7 |

| Vanguard FTSE Developed World ex-UK Equity Index | 13 |

Higher risk

| Fund | Allocation % |

| Artemis Global Income | 16 |

| Aviva Inv Global Equity Income | 14 |

| Barclays Wealth Wealth Global Markets 5 | 11 |

| Fidelity Index Japan | 4 |

| iShares Physical Gold ETC | 8 |

| Liontrust India | 8 |

| Ninety One UK Special Situations | 5 |

| Schroder UK Smaller Companies | 8 |

| T. Rowe Price US Large Cap Growth Equity | 13 |

| Vanguard FTSE Developed World ex-UK Equity Index | 13 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay