The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

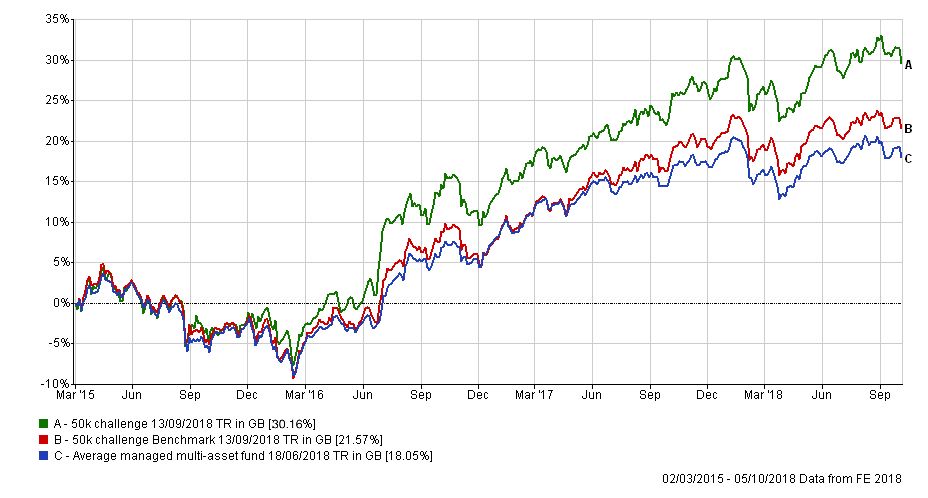

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015, three and a half years ago. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

Although it is only a few weeks since my last portfolio review I am keen to try and bring the reviews closer to the start of the month where possible, rather than the middle of the month. While my portfolio is still outperforming its benchmarks, as shown in the chart above, it did underperform them by 0.5% in the second half of September. The biggest drags on my portfolio's performance during that time were my European equity fund as well as the Jupiter UK Smaller Companies holding. This was as much a reflection of the performance of the asset classes themselves as it was of each fund's specific performance.

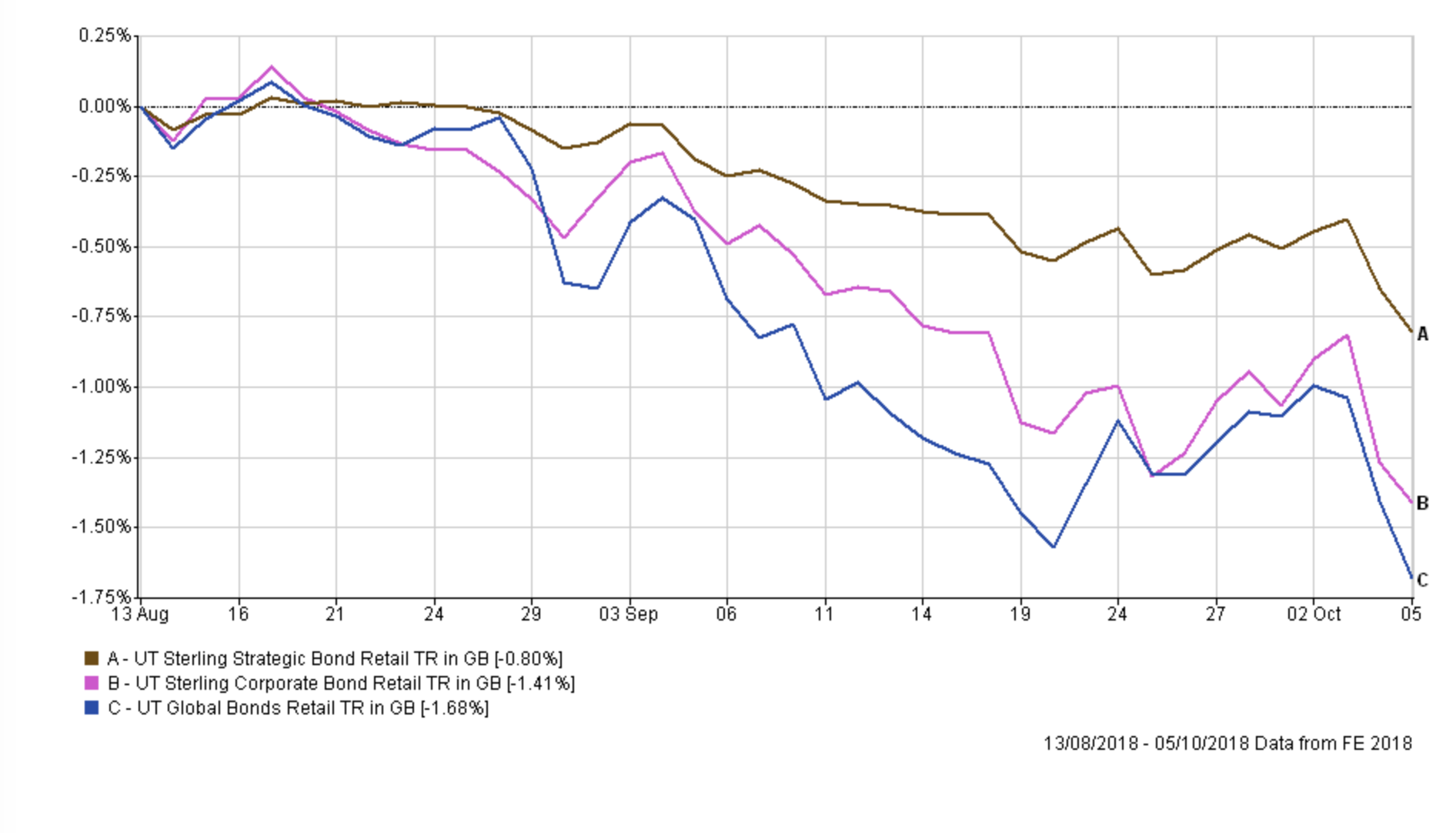

On the plus side, my large cash weighting since mid-August continues to help the lower risk end of the portfolio. The chart below shows how the average global and UK bond fund have lost money since the middle of August, underperforming cash. The only bright spot for bonds has been high yield bonds, which tend to track the fortunes of stocks more closely. That's why funds such as JPM Global High Yield Bond have managed to creep into the BOTB over the last few months.

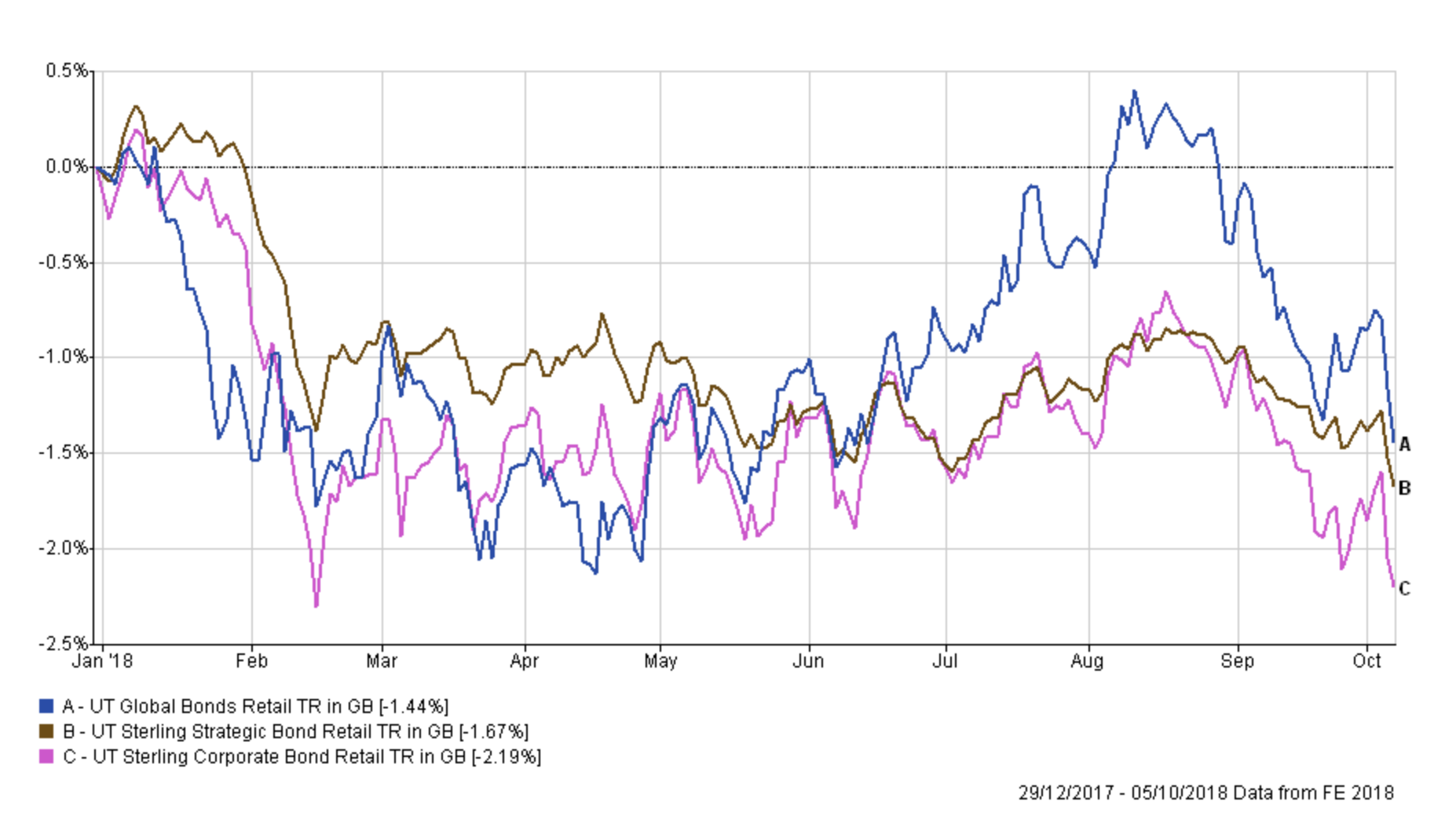

The chart below of the year-to-date performance of the same bond sectors, highlights how mid-August marked the recent high point in the bond market recovery, before the latest leg downwards.

Looking at my portfolio as a whole, the table below shows my current allocation, with those funds in green still in the BOTB while those in yellow are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Fund | Allocation | Risk | Sector | ISIN Code | SEDOL Code | Citicode / TIDM |

| AXA Framlington American Growth | 12.9 | High | North America | GB00B5LXGG05 | B5LXGG0 | 03TF |

| Baillie Gifford Positive Change | 5.8 | High | Global | GB00BYVGKV59 | BYVGKV5 | NGPB |

| BlackRock European Absolute Alpha | 7.5 | Low | Targeted Absolute Return | GB00B4Y62W78 | B4Y62W7 | EYN0 |

| CFP SDL UK Buffettology | 10.25 | Medium | UK All Companies | GB00B3QQFJ66 | B3QQFJ6 | MJZ1 |

| JPM Japan | 3 | High | Japan | GB0030879471 | 3087947 | RT06 |

| Jupiter UK Smaller Companies | 7.75 | Medium | UK Smaller Companies | GB0004911870 | 491187 | JU20 |

| LF Miton European Opportunities | 10.5 | High | Europe Excluding UK | GB00BZ2K2M84 | BZ2K2M8 | MSED |

| Liontrust Sustainable Future Absolute Growth | 12.5 | Medium | Flexible Investment | GB0030029622 | 3002962 | CU94 |

| Newton Real Return | 6.5 | Low | Targeted Absolute Return | GB0001642635 | 164263 | BS97 |

| Standard Life Investments Global Smaller Companies | 5 | High | Global | GB00B7KVX245 | B7KVX24 | 10FZ |

| Cash | 18.3 | Low | N/A | N/A | N/A | N/A |

It is interesting to see AXA Framlington American Growth back in the BOTB and BFBS lists after a brief hiatus last month. During last month's review I placed the fund on my watchlist rather than ditch it and on the face of it that was the right thing to do. However, in last month's review I also wrote that "I am conscious of the AXA fund's exposure to technology stocks, which was an extremely profitable position during the summer, but it does make the fund susceptible to a pullback if the sector takes a hit". In that same review I pondered some alternative US equity funds to hold before ultimately sticking with the AXA fund.

However, in the last few days the technology sector has taken a hit and as expected the AXA Framlington American Growth has experienced a wobble. Of course, the current bout of weakness is not confined to technology stocks and the reality is that any equity (or indeed bond fund) you hold has been under pressure in the last week.

Given the trading delays that occur when switching unit trusts you increase the chances of the market moving against you (or indeed in your favour) when there is an uptick in volatility and fear, as there is right now. So while I am investing for the long term it pays to try and avoid large market swings where possible.

Ordinarily, I may have looked to diversify my US equity position slightly away from US technology stocks but given the current market backdrop I don't want to make any significant changes. In any event, there are only three funds that are highlighted red in the above table which are BlackRock European Absolute Alpha, JPM Japan and Jupiter UK Smaller Companies. The Blackrock fund is down just 0.22% over the last month (still making it one of the best performing funds in my portfolio during the recent market slump) while the JPM Japan fund is up 1.94% in the few weeks I've held it, even after the global equity sell-off (at one point it was up 6%). For now I will bear with these funds because they've only just fallen out of the 80-20 Investor lists.

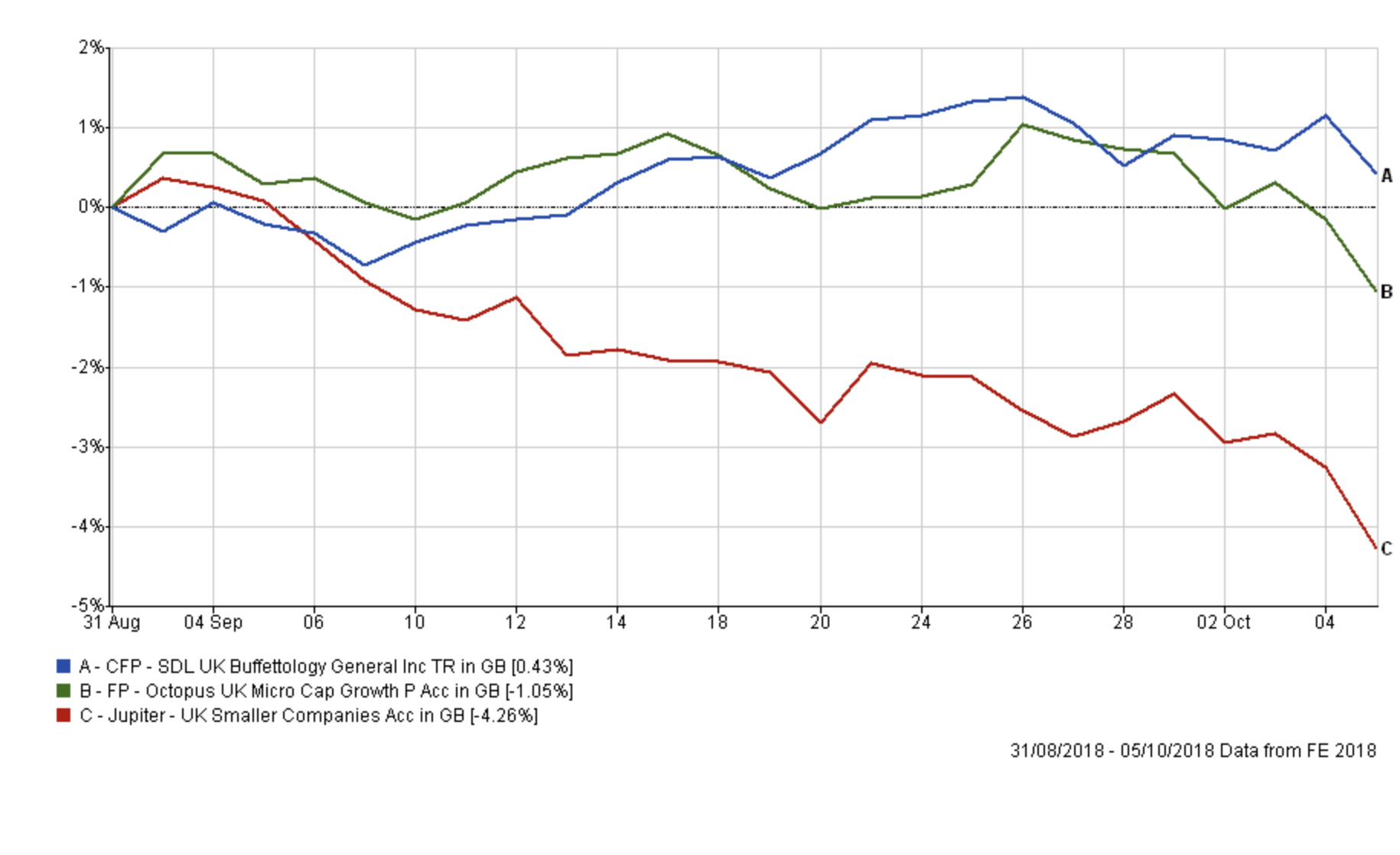

That leaves the Jupiter UK Smaller Companies fund. I have held this fund since May and it has been a regular in the 80-20 Investor lists. Indeed it was in September's BOTB list. However, as September progressed it notably fell out of the BFBS list and became one of the worst performing funds in my portfolio. The chart below shows the performance of the fund versus the sector average since I first held it in my portfolio back in May. You can see that its performance was fantastic until September when things took a turn for the worse and the fund tracked back to being average. The divergence in fortunes of the wider peer group and the fund itself raises questions which is why I am switching out of it.

In order to maintain my UK equity exposure in line with the BOTB I have decided to split the proceeds from the switch between the FP Octopus UK Micro Cap Growth fund and CFP SDL UK Buffettology which I already hold. The FP Octopus UK Micro Cap Growth fund is a like-for-like swap (i.e UK Smaller Companies) and is the only UK small cap fund from the 80-20 Investor lists available on the investment platform I use. The CFP SDL UK Buffettology fund is a large-cap fund which has performed fantastically during recent periods of equity market weakness (as shown below). I toyed with simply replacing the Jupiter fund with the Buffettology funds but felt that it would overexpose my portfolio to one fund and its fortunes.

Below I list the switch I am making this time:

Fund switches

- 100% out of Jupiter UK Smaller Companies and 33.4% into CFP SDL UK Buffettology and 66.6% into FP Octopus UK Micro Cap Growth Fund

Again, I have not chosen to tweak my cash position for the same reasons as last time. It's a temporary position awaiting better opportunities in the low-risk area. It is interesting to see that the Standard Life UK Real Estate fund has reentered the BOTB in the low-risk area but I still have concerns over the asset class generally until we have more clarity over Brexit. The best way to summarise this portfolio review is that I am letting the market dust settle.

Overall I am switching only about 7% of my portfolio. My new portfolio will look as shown in the table below and still has an equity exposure of around 61%. The number of holdings remains at 11.

My new portfolio looks like this:

| Fund | Allocation | Risk | Sector | ISIN Code | SEDOL Code | Citicode / TIDM |

| AXA Framlington American Growth | 13 | High | North America | GB00B5LXGG05 | B5LXGG0 | 03TF |

| Baillie Gifford Positive Change | 5.6 | High | Global | GB00BYVGKV59 | BYVGKV5 | NGPB |

| BlackRock European Absolute Alpha | 7.6 | Low | Targeted Absolute Return | GB00B4Y62W78 | B4Y62W7 | EYN0 |

| CFP SDL UK Buffettology | 13 | Medium | UK All Companies | GB00B3QQFJ66 | B3QQFJ6 | MJZ1 |

| JPM Japan | 3.2 | High | Japan | GB0030879471 | 3087947 | RT06 |

| FP - Octopus UK Micro Cap Growth | 5 | High | UK Smaller Companies | GB00BYQ7HN43 | BYQ7HN4 | NFZH |

| LF Miton European Opportunities | 10.2 | High | Europe Excluding UK | GB00BZ2K2M84 | BZ2K2M8 | MSED |

| Liontrust Sustainable Future Absolute Growth | 12.6 | Medium | Flexible Investment | GB0030029622 | 3002962 | CU94 |

| Newton Real Return | 6.5 | Low | Targeted Absolute Return | GB0001642635 | 164263 | BS97 |

| Standard Life Investments Global Smaller Companies | 5 | High | Global | GB00B7KVX245 | B7KVX24 | 10FZ |

| Cash | 18.3 | Low | N/A | N/A | N/A | N/A |

My new asset mix

This means my new asset mix is (previous asset mix is in brackets):

-

- UK Equities 19% (18%)

- North American Equities 23% (23%)

- Global Fixed Interest 2% (2%)

- Japanese Equities 5% (4%)

- Other International Equities 0% (0%)

- Asian equities 1% (1%)

- European Equities 14% (15%)

- UK Fixed Interest 0% (0%)

- Cash 23% (23%)

- Alternative Investment Strategies 13% (14%)

- Emerging Asia equities 0% (0%)

- Emerging Market Fixed Interest 0% (0%)

- Property 0% (0%)

Damien's higher risk and low-risk portfolios

Using the logic described in my post New: Damien’s Higher Risk Portfolio the higher and lower risk versions of my portfolio would like as follows:

Higher risk

| Fund | Allocation % |

| AXA Framlington American Growth | 19.2 |

| Baillie Gifford Positive Change | 8.3 |

| CFP SDL UK Buffettology | 19.2 |

| JPM Japan | 4.8 |

| FP Octopus UK Micro Cap Growth | 7.4 |

| LF Miton European Opportunities | 15.1 |

| Liontrust Sustainable Future Absolute Growth | 18.6 |

| Standard Life Investments Global Smaller Companies | 7.4 |

Lower risk

| Fund | Allocation % |

| BlackRock European Absolute Alpha | 13.1 |

| CFP SDL UK Buffettology | 22.4 |

| Liontrust Sustainable Future Absolute Growth | 21.7 |

| Newton Real Return | 11.2 |

| Cash | 31.6 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay