The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Raising cash

Following my Damien's March 2020 Portfolio review something interesting (and worrying) happened in investment markets. In my review, I wrote how, the extreme equity market volatility means that it would probably be ill-advised to tamper with the equity content of the portfolio. I still think this is the case despite equity markets now not being in the BFBS tables at all anymore. It's a classic case of catching a falling knife when equity markets are tumbling as they are now.

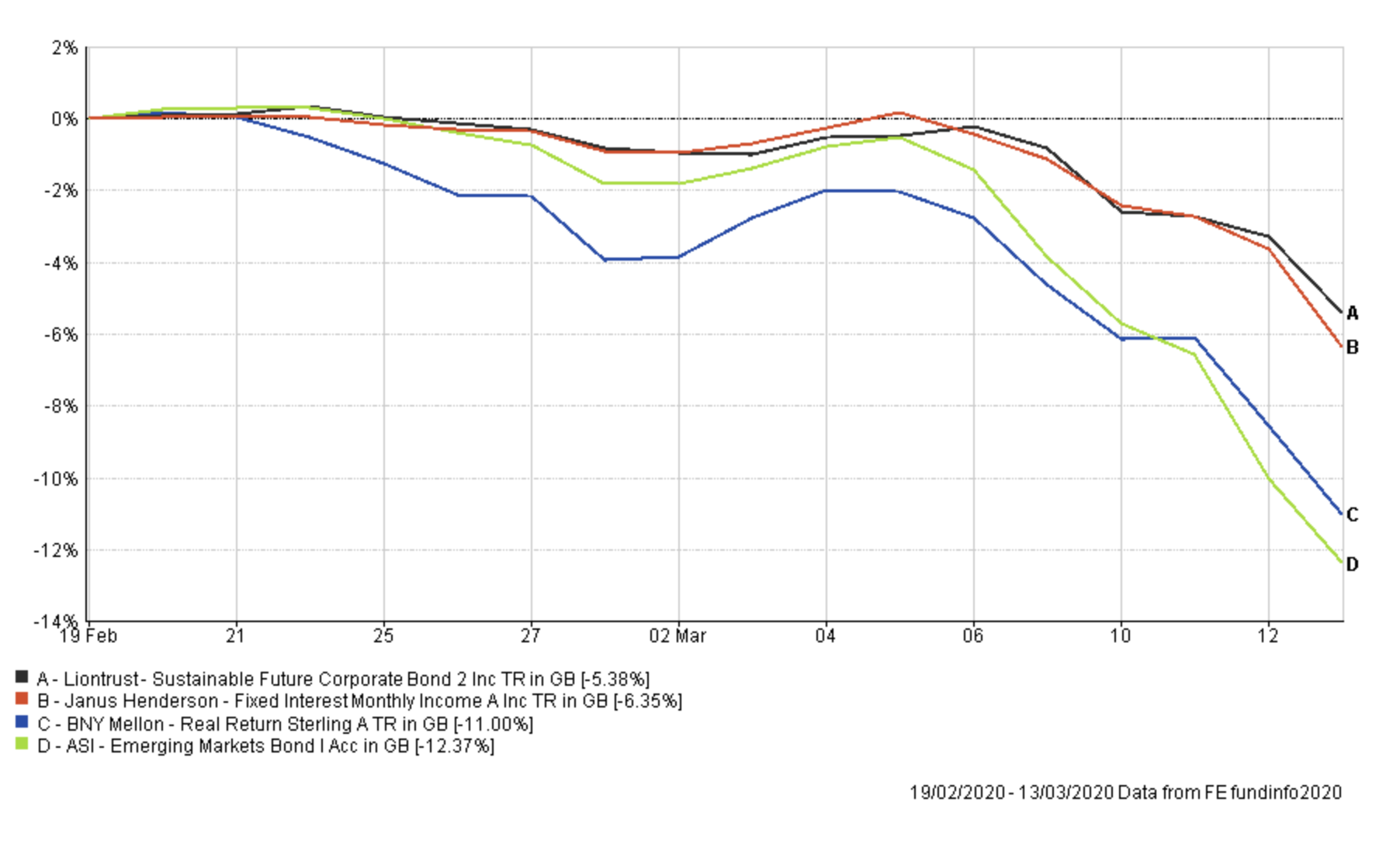

However, in the days that have passed since that review, some of the biggest detractors from my portfolio's performance have actually been the low risk funds within my portfolio. The chart below shows the performance of all the low risk funds in my portfolio since equity markets started to drop on 19/20th February. As you can see, up until 6th March my low risk holdings had at least minimised losses. However, given that stocks have been in freefall throughout that time the funds' performance has been disappointing, not even beating cash. From the 8th March onwards the scale of the current investment market collapse has meant that bonds and equities have been highly correlated. Indeed you can see how my low risk funds have lost between 5% and 12% in a matter of days. Indeed, today the stop loss alerts were triggered on a range of bond funds within March's BOTB.

While this is something of a systemic issue, as the financial system continues to implode it does beg the question what is the point of holding them, if cash fares better. Part of the reason for the bond sell-off has been the increased potential for companies to default on their loans (raising concerns over creditworthiness). Furthermore in what environment would corporate bonds now rally? When stocks rally? Seems unlikely. It would likely take a complete refutal of the potential impacts that the coronavirus may have on corporate cashflows.

Hopefully, we are nearing the bottom for asset prices soon but there is no way of knowing. So I've taken the decision to remove the following funds and sit the proceeds in cash for the time being. Cash is a destination in itself and when my low-risk funds are clearly not cutting it then there is no point in holding them.

Finally, I took the opportunity to sell my tiny holding in the ASI Global Real Estate Share as it has been my worst performing holding now since the sell-off began. While it will crystallise the loss it is a small holding and limits further possible downside as it slightly reduces my portfolio's equity content. Aside from that I am not changing my portfolio as there is little anyone can do in this environment with regard to calling the bottom or timing the market.

Fund switches

- 100% out of Janus Henderson Fixed Interest Monthly Income and 100% into Cash

- 100% out of the ASI Emerging Markets Bond and 100% into Cash

- 100% out of ASI Global Real Estate Share and 100% into Cash

- 100% out of BNY Mellon Real Return and 100% into Cash

- 100% out of Liontrust Sustainable Future Corporate Bond and 100% into Cash

My portfolio now looks like this:

| Name | Allocation % (rounded) | Risk | Sector | ISIN Code |

| Fidelity European | 4.5 | Medium | Europe Excluding UK | GB00BFRT3504 |

| Jupiter Japan Income | 5.5 | High | Japan | GB00B0HZTZ55 |

| M&G Global Listed Infrastructure | 7 | Medium | Global | GB00BF00R928 |

| Slater Growth | 9 | Medium | UK All Companies | GB00B0706C66 |

| VT Gravis Clean Energy Income | 14.5 | Medium | Global | GB00BFN4H792 |

| ASI UK Real Estate Share | 5.5 | High | Property Other | GB00B0XWNN66 |

| Premier Diversified Growth | 9 | Medium | Mixed Investment 40-85% Shares | GB00B8BJV423 |

| Royal London UK Government Bond | 6 | Medium | UK Gilts | GB00B881TW52 |

| Cash | 39 | Low |

My Portfolio asset mix

My portfolio asset mix is as shown below (the previous asset mix is in brackets) with approximately 53% invested in equities:

-

- UK Equities 17% (17%)

- North American Equities 11% (11%)

- Global Fixed Interest 0% (15%)

- Japanese Equities 5% (5%)

- European Equities 9% (9%)

- UK Fixed Interest 0% (6%)

- UK Gilt 5% (5%)

- Cash 39% (0%)

- Alternative Investment Strategies 3% (13%) (including absolute return)

- Emerging Market Fixed Interest 0% (4%)

- Commodities and energy 6% (6%)

- Property 5% (9%)

Damien's higher risk and lower risk portfolios

Using the logic described in my post: Update to Damien’s alternative risk portfolios I created hypothetical higher and lower risk versions of my portfolio below:

Higher risk

| Fund | Allocation |

| Fidelity European | 7 |

| Jupiter Japan Income | 9 |

| M&G Global Listed Infrastructure | 11 |

| Slater Growth | 15 |

| VT Gravis Clean Energy Income | 24 |

| ASI UK Real Estate Share | 9 |

| Premier Diversified Growth | 15 |

| Royal London UK Government Bond | 10 |

Lower risk

| Fund | Allocation |

| Fidelity European | 5 |

| M&G Global Listed Infrastructure | 8 |

| Slater Growth | 10 |

| VT Gravis Clean Energy Income | 16 |

| Premier Diversified Growth | 10 |

| Royal London UK Government Bond | 7 |

| Cash | 44 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay