Listen to Episode 553

In this week’s episode, I share some of the essential rules and concepts I have used in order to build lasting financial habits. These include practical ways to manage your budget, the importance of paying yourself first and avoiding lifestyle creep to help provide a comfortable financial future.

Next, we look at recent research on the interest that is applied to monthly car insurance premiums and share straightforward, practical tips for spreading the cost without paying exorbitant fees.

[AD] Thank you to our sponsor Interactive Investor

New customers can receive £100 in free trades when they open an Interactive Investor Trading Account before 31st July 2026. Terms & fees apply. Capital at risk. https://moneytothemasses.com/redir/ii-podcast

Support the podcast

Remember to like, subscribe and follow us on all our socials. You can also support the Money to the Masses podcast by visiting our dedicated podcast page.

Every time you use a link on the page we may earn a small amount of money for our podcast. We only use affiliate links that give you an identical (or better) deal than going direct. Thank you for being an incredible part of our community. Your support means the world to us.

Watch the video version of the podcast below:

You can also listen to other episodes and subscribe to the show by searching 'Money to the Masses' on Spotify or by using the following links:

Listen on iTunes Listen on Spotify via RSS

Support the podcast!

You can now support the Money To The Masses podcast by visiting this page when making any financial decision

- Save money

- Earn cashback

- Exclusive offers for listeners

Episode 553 Podcast Summary

My 10 commandments of money

Summary:

I explain the 10 core rules and concepts I use to run my own finances. These high-level commandments inform the daily actions and habits necessary for building wealth. From "dividing and conquering" your budget to "starving your ego" to prevent lifestyle creep, I outline how to implement robust financial systems. I also discuss the importance of remaining flexible, continuously educating yourself, and understanding when you have "enough" money.

Key Insights:

- Divide and conquer - Break down your finances into manageable parts. Tackle one bill at a time when trying to cut costs, and use budgeting apps or bank "pots" to silo your money and control your spending.

- Harness the power of time - Utilise compound interest by committing to regular, automated investments or savings contributions, paying yourself first before other expenses.

- Starve your ego - Avoid "lifestyle creep" and high-interest consumer debt. Stop buying things just to keep up with others, and learn the difference between good debt (like a mortgage) and bad debt.

- Shatter the ceiling - There is a limit to frugality. Once your finances are optimised, shift your focus toward increasing your income through upskilling, promotions, or a side business.

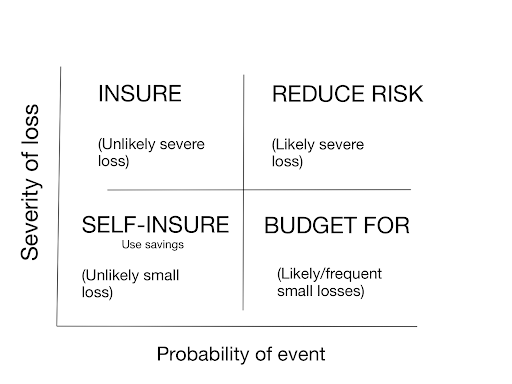

- Protect what you have - Build a robust defence by maintaining a 3 to 6-month emergency fund and purchasing necessary protection products like life insurance and income protection.

- Understand what "enough" is - Avoid greed and chasing unrealistic investment returns. Focus on defining your personal goals and the exact amount of money you need to achieve your own comfortable lifestyle or retirement.

The hidden cost of monthly car insurance

Summary:

We look at the expensive reality of paying for car insurance on a monthly basis. Recent research indicates that some providers are charging an Annual Percentage Rate (APR) of up to 30% when customers choose to spread the cost, treating the monthly payments as a high-interest loan. We provide practical ways to avoid these excessive interest charges and secure the best possible premium.

Key Insights:

- Monthly payments are loans - When you pay monthly for car insurance, you are effectively taking out a loan for the annual premium, which the insurer applies interest to.

- Interest rates are soaring - Research shows the average APR charged for paying monthly is 23%, with some providers charging nearly 30%, rivaling expensive credit cards.

- Pay annually if possible - The simplest way to avoid these charges is to pay your premium upfront in one lump sum if you have the savings available.

- Utilise 0% purchase cards - If you need to spread the cost, consider using a 0% purchase credit card to pay the annual fee upfront, ensuring you clear the balance before the promotional period ends.

- Shop around carefully - A small number of providers do not charge interest for monthly payments. Always look at the total amount payable, rather than just the monthly figure, when comparing quotes.

Resources

Links referred to in the podcast:

- Sign up to our weekly newsletter

- Best budgeting apps available in the UK

- Money to the Masses budgeting spreadsheet

- Life insurance guidance

- Income protection guidance

- Critical illness insurance guidance

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay