How high will interest rates go?

The Bank of England base interest rate has been at an all time low since March 2009. There is now talk of interest rates rising, may be as early as mid 2015. If the interest rate does rise next year how quickly is it likely to rise and how high could it go? If you believe Mark Carney, the Governor of the Bank of England, the rise will be gradual, perhaps with an upper limit of around 3%.

Really? I'm not sure I believe him. Let's take a look back over recent years and see how interest rates have risen, since the Bank of England independently controlled them, to see what could happen in the future.

Please note: Average mortgage rates are around two percentage points above the Bank of England base rate.

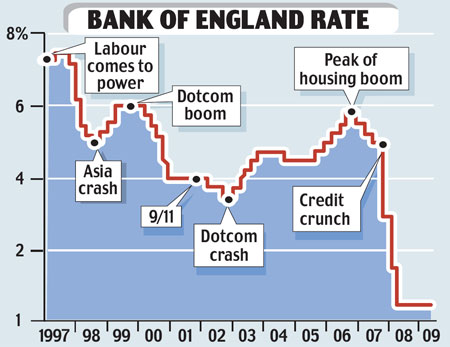

It's 1998 and Labour have just been elected and interest rates peak

In May 1997 Labour won the general election after 18 years in opposition and Tony Blair became Prime Minister. Five days after the general election the Bank of England was given the responsibility for setting interest rates independently and continues to do so up to the present day.

In June 1998 interest rates reached a modern day high of 7.5% pushing mortgage rates to an eye watering 9.5%!

Between September 1998 and June 1999 interest rates dropped by 2.5%

Due to a financial crisis, that originated in Asia, base rates were reduced by 2.5% in the space of 9 months bringing the base rate down to 5.0%.

The Dotcom boom pushes interest rates back up

Over the following 8 months (June '99 to Feb '00) interest rates rebounded to 6.0% on the back of what is now known as the 'Dotcom boom'. In the early days of the internet investors where piling into internet based start-ups hoping to make big profits.

The Dotcom bubble bursts

In 2000 some investments in technology stocks started to unravel as it became clear that the underlying companies were failing to met their ambitious growth targets. In January 2001 interest rates were still holding up at 6.0% but by the end of 2001 (post 9/11) they had fallen to 4.0%.

The housing bubble starts

After two years (2002/2003) of level interest rates at around 4.0% things were on the move again. By the end of 2004 interest rates were up to 4.75% and rose slowly over the next three years to peak at 5.75% in July 2007. Mortgage rates in July 2007 were around 7.75%.

The housing bubble bursts

As easy credit fuelled the housing market mortgage defaults forced banks to withdraw from the mortgage market. As the credit crisis unfolded interest rates fell from 5.5% in November 2007 to 0.5% by March 2009. A 5% drop in less than 18 months!

Long term interest rates are around 5% and mortgage rates around 7%

It is a fact that long term interest rates are around 5% which will make the average mortgage rate around 7%. So, this period of low interest rates we are experiencing at the moment will not last. If you have a mortgage then you need to do your calculations now to make sure your finances can survive the inevitable interest rate rises.

Once interest rates rise following a financial crisis they usually keep on rising

As you can see from the graph above, interest rates will fall following a financial crisis as the Bank of England try to get the economy on a sound footing. However, once that crisis is over interest rates will rise over the following period of years to control inflation as the economy becomes more prosperous. Interest rates will always move towards the average of around 5% and will only likely be interrupted if another crisis requires a change in direction. In recent history rates have always at least retraced half the rate cut instigated following the previous crisis.

To put that into context, rates would get back to around 3% before lurching either up or down. But interestingly, this time the Bank of England have printed huge sums of money. No one knows how this will impact future inflation. The genie is out of the bottle, we just don't know what he will do. If inflation comes roaring back then rates will have to rise more quickly. It looks unlikely at the moment, but then so did a 0.5% base rate back in 2007!

If Mark Carney can keep rates below the long term average, with only slow gradual increases and keep inflation in check, then he is defying history. Maybe he is magic, or even a genie?

Read more: Latest interest rate predictions - when will rates rise?

Fixed rate mortgage coming to an end?

Our partner Habito is a leading online mortgage broker and will recommend the best mortgage for you:

- Habito checks over 20,000 mortgages from 95 mortgage lenders

- Over 9,500 5-star Trustpilot customer reviews

- It’s completely free

- Apply online with no obligation