80-20 Investor was designed to provide subscribers with research to empower them to make better investment decisions. The service is not prescriptive and a key aim when I originally conceived the idea for 80-20 Investor was that it would allow people to use it in a way that suited them. They could use it to help research funds in a particular sector or they could build a portfolio in accordance with their own views or risk appetite. For example, Subscriber A might want to take more risk than Subscriber B but they both could use 80-20 Investor to build portfolios that they felt would suit them

I deliberately created a product that was not a ‘one-size-fits-all’ solution. It’s a very tricky thing to do which is why the world of finance will opt for the easier ‘one-size-fits-all’ approach. Of course, in order for me to demonstrate the value of the 80-20 Investor fund shortlists I track the performance of the BOTB selection as a whole. This is a hypothetical exercise.

However, I also wanted to demonstrate how to use the research in reality which is why I have been running my own £50,000 portfolio (which is now worth £62,500) for the last three years. In doing so I document how I use the 80-20 Investor research and document all my portfolio changes as I make them. The results are not hypothetical but actual returns after all charges. Of course the aim of my £50,000 portfolio is not to say this is the best or only way to use the 80-20 Investor research but one way. I get emails from readers who say how much they enjoy 80-20 Investor and even how they have outperformed my £50,000 portfolio by using the research to build their own portfolio. That is fantastic to read.

However, my £50,000 portfolio is incredibly popular but it also brings its own issues. While I don't run the portfolio for subscribers to copy I have to be mindful that people will. Therefore I always try and keep my portfolio with an overall medium risk level. That does mean that I can't amplify the risk level of the portfolio which will hinder its performance in a market rally like we had in 2017. Interestingly I have had a number of messages from subscribers asking whether I would consider running a high-risk portfolio and how would I build one.

This formed the basis of a project I have been working on in the background for some time to produce a higher risk portfolio. The problem was that if I started a higher-risk Damien portfolio today it would be completely new and have no history. That would make a comparison with my normal £50,000 portfolio impossible. I also didn't want to launch a purely hypothetical portfolio, back-dated to March 2015, whereby I picked a portfolio from previous high-risk funds. The danger is that you could be accused of cherry-picking with the benefit of hindsight, especially when it came to allocating how much you would put into each fund. The other key aim was that I wanted the exercise to demonstrate the range of returns you could have achieved over time using 80-20 Investor's research. While I may well receive emails from subscribers describing how they have achieved a higher return than my £50,000 (or indeed lower) other subscribers don't get to see these. I want to demonstrate that 80-20 Investor (or indeed my £50k portfolio) is not a one-size-fits-all solution. On top of that, some of you have said that while you may follow my £50,000 portfolio it isn't risky enough for you.

New Damien higher-risk portfolio

In response to a recent question I received asking how I would change my £50k portfolio if I wanted to take more investment risk the answer was that I would have chosen the same funds, in all likelihood, but skewed my investment towards the high and medium risk funds. It was then that I had the idea of how to demonstrate a higher (or indeed lower) risk version of Damien's portfolio while achieving the aims set out earlier.

As I have the details of every transaction I've ever made to my £50k portfolio and a copy of every dataset since 80-20 Investor launched I was able to meticulously go back and actually recreate a higher risk version of my portfolio as if I had actually bought it. This took a hell of a long time which is why I've only just been able to publish the results. To create a higher risk version of my portfolio I apportioned any money held in low-risk funds within my £50k portfolio into medium and high-risk funds, but with the same level of conviction as in my actual £50k portfolio. To explain this consider the dummy £50k portfolio below:

- £5k in a low-risk fund A

- £5k in low-risk fund B

- £5k in low-risk fund C

- £5k in a medium-risk fund D

- £2.5k in medium-risk fund E

- £10k in medium-risk fund F

- £2.5k in high-risk fund G

- £5k in high-risk fund H

- £10k in high-risk fund I

The portfolio above has £15k invested in low-risk funds, £17.5k in medium-risk funds and £17.5k in high-risk funds. To create a high-risk portfolio I would remove the low-risk funds and invest the £15k into medium and high-risk funds (where I currently have £35k) to reflect my conviction in the original £50k portfolio.

So to work out how much to invest in Fund D, I carried out the following sum £5k/£35k = 14.29%. Or in other words fund D makes up 14.28% of my medium and high exposure. Therefore I added 14.29% from the £15k (that would have been in low-risk funds) into Fund D. This makes fund D now worth £7.1k

I repeated this exercise for all the funds which left me with a higher risk version of Damien's portfolio. Remember, all I'm doing is ditching the low risk funds and spreading the money across the medium and high-risk funds in my portfolio.

- £7.1k in a medium-risk fund D

- £3.6k in medium-risk fund E

- £14.3k in medium-risk fund F

- £3.6k in high-risk fund G

- £7.1k in high-risk fund H

- £14.3k in high-risk fund I

I repeated the process for the entire three years I've been running my portfolio ensuring that all fund switches were reflected accurately in pounds and pence. I even reflected the occasions where a fund in my portfolio changed risk categories. I also repeated the exercise and built a lower risk Damien's portfolio whereby I reallocated money (in the same manner) out of the high-risk funds into low and medium risk funds.

The results

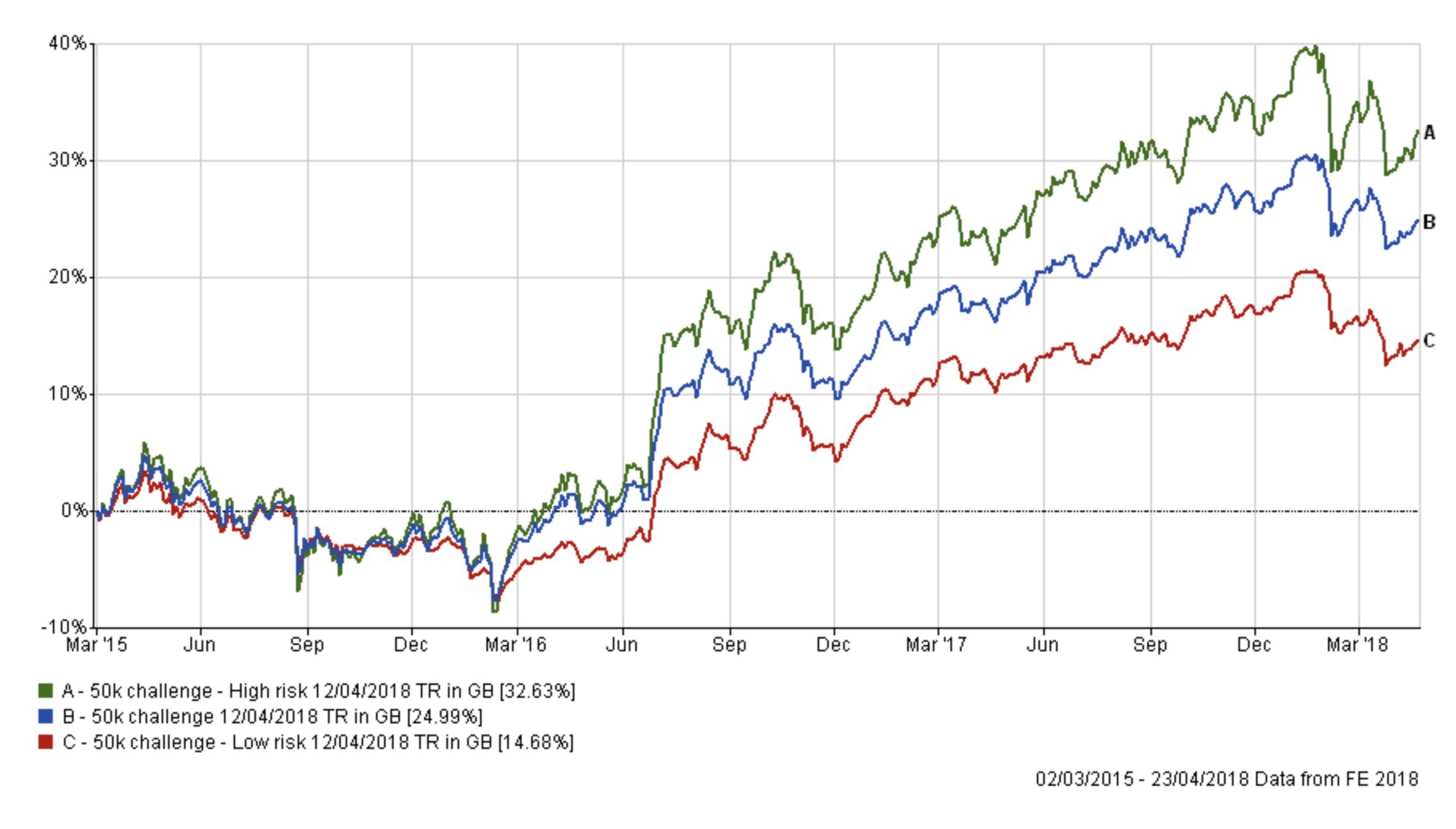

The chart below (click to enlarge) shows the performance of a Damien higher risk portfolio (in green) and lower risk portfolio (in red) against my standard £50k portfolio (in blue).

The result is a fan chart showing a range of results from low risk to high risk (14.68% to 32.63%), with my £50k portfolio in between (24.99%). It reiterates what I discussed in my previous article '80 20 Investor – High, Medium and Low-risk portfolios' that momentum really works well in the medium and higher risk arena while its impact at the low-risk end is muted.

To give the above chart some context the table below shows the average return from each of the three key managed fund sectors. Note how the various Damien portfolios have outperformed their relevant managed sectors while having less equity exposure.

| Portfolio | % Return since March 2015 |

| 50k challenge Higher risk (currently 80% in shares) | 32.63 |

| 50k challenge (currently 50% in shares) | 24.98 |

| Mixed Investment 40-85% Shares | 19.42 |

| 50k challenge Lower risk (currently 20% in shares) | 14.67 |

| Mixed Investment 20-60% Shares | 13.34 |

| Mixed Investment 0-35% Shares | 8.97 |

Using the methodology described earlier it means that the lower risk and higher risk portfolios are currently invested as follows

Lower risk portfolio

- FP - Pictet Multi Asset Portfolio - 11.2%

- Man GLG - UK Income - 5.6%

- Premier - Diversified - 31.2%

- Standard Life Investments - UK Real Estate - 9.9%

- TwentyFour - Dynamic Bond - 31.1%

- Cash - 11%

Higher risk portfolio

- 7IM - US Equity Value - 10.8%

- AXA - Framlington American Growth - 7.6%

- Baring - Eastern Trust - 7.7%

- Fidelity - China Consumer - 11%

- Jupiter - Japan Income - 8.1%

- Man GLG - UK Income - 5.5%

- Premier - Diversified - 30.7%

- TM - Cavendish AIM - 18.6%

Again this is not a recommendation of a portfolio but it demonstrates with real-world data (not hypothetical data) how the portfolios would have performed after charges because they are based on actual trades I made. Going forward I may continue to publish the higher risk version of the £50k portfolio as a guide to the range of returns and the impact (positively or negatively) of taking increased risk. The reason why I refer to the portfolios as higher and lower (rather than high and low, aside from the chart labels) is that you could just invest in high-risk funds. That really would be high risk! Whereas my higher risk portfolio has just ratcheted up the investment risk slightly but still includes medium-risk funds. The purpose of this exercise is to show portfolios that are anchored on what I actually had the conviction to invest my money in, so you can perceive them as real as my actual £50k portfolio.

Hopefully, it helps to demonstrate the range of returns I would have achieved had I decided to vary the risk level of my portfolio while at the same time inspiring subscribers who are thinking of ways to vary the risk levels in their portfolios.

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay