The background to my portfolio

Back in March 2015 I decided to invest £50,000 of my own money using 80-20 Investor. The purpose was twofold, firstly to show how you can use 80-20 Investor to invest and outperform the market with only a few minutes effort every now and then. Secondly, no other investment commentator, journalist or research provider invests their own money for fear of failing. This is a sorry state of affairs and is precisely why I committed to openly running my own portfolio for 80-20 Investor members to see.

Since then I have periodically changed my portfolio using the fund suggestions provided by the 80-20 Investor algorithm and associated research. I always disclose the changes at the time they are made.

Performance update

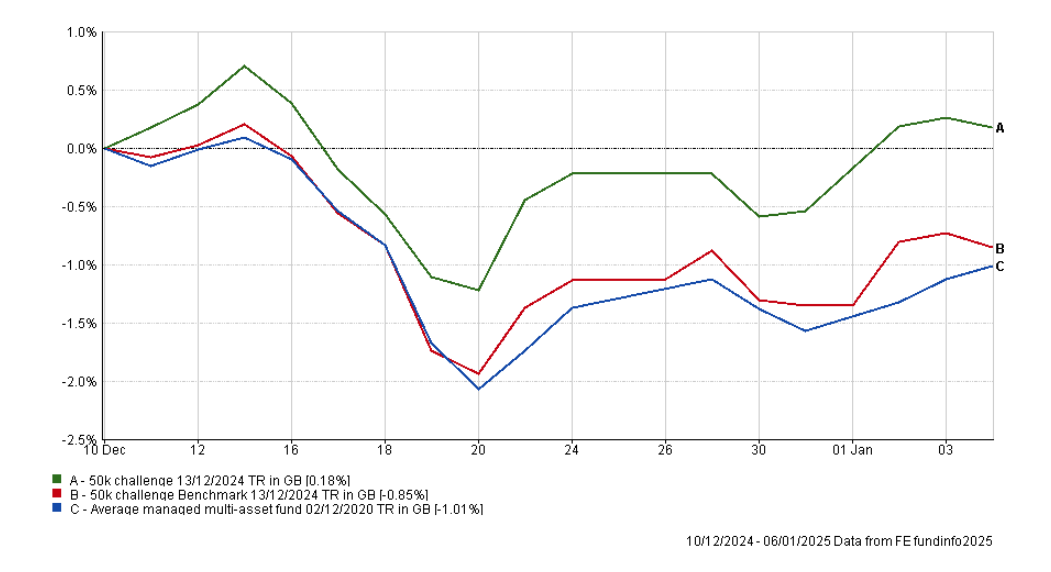

As is usual in my portfolio reviews, the chart below shows how my portfolio has outperformed since I started the challenge in March 2015. The green line is the performance of my portfolio while the red line is the benchmark showing the average return achieved by professional fund managers given the same asset mix. To accurately calculate this I have used the average return for each sector in which my portfolio invested. The blue line shows what the average multi-asset fund with comparable equity content achieved. In other words, the red line would show the extra performance added by just the asset mix of my portfolio (where I was invested i.e. European equities etc) over picking a typical multi-asset fund (the blue line). While the green line (which is my actual performance) shows the impact of being in the right funds at the right time, as identified by the 80-20 Investor algorithm.

As you can see my portfolio has extended its lead over its benchmarks since my last portfolio update in December.

My portfolio outperformed its benchmarks by posting a positive return during a difficult month for investment markets which saw both benchmarks lose money (see below).

It means that my portfolio now sits just shy of its all-time high, and my original £50,000 portfolio is now worth over £89,340 which equates to a profit of 78.68% in just under 10 years, which is a great result. But it's not just the profit that is important, so is the management of risk over that time to achieve that profit.

If my portfolio was a fund residing in the Mixed Investment 40-85% Shares sector of 262 funds (of which 143 have been in existence since my portfolio started) it would rank in the top quartile for all of the key investing statistics, namely:

Alpha

Alpha is a figure which measures a manager’s apparent skill at picking winning investments versus their benchmark. Alpha is the excess return versus the return of a fund’s benchmark (i.e. the market). So a fund/portfolio with a positive alpha indicates that the fund manager has outperformed through skill. While a negative alpha figure would indicate underperformance. The higher the alpha figure the better.

Maximum Drawdown

This is the biggest fall experienced in a given week. My portfolio is among those funds with the lowest drawdowns. If you recall my portfolio outperformed throughout 2022 by protecting its value when bond and equity markets were tumbling.

Sharpe Ratio

The Sharpe Ratio is a measure of the excess return a manager is achieving for the risk they are taking. The higher the Sharpe Ratio the better. My portfolio has one of the highest Sharpe ratios.

Sortino Ratio

This is very similar to the Sharpe Ratio but places more emphasis on the manager's ability to manage on the downside. Again my portfolio ranks in the top quartile of the sector for this statistic.

Volatility

This is a measure of a fund's dispersion of returns, or in plain English the variability in those returns. Think of it as a measure of how much a building is prone to wobble. The more prone it is (the higher the volatility) the more it will sway in an earthquake. Not only is my portfolio in the top quartile for this statistic but only 17 funds out of 143 in the sector have a lower level of volatility than my portfolio.

The takeaway is that while I am proud of how the portfolio has performed, I have achieved this by managing risk and squeezing more return from the risk that I have taken than most professional fund managers.

Bringing things back to the short term, the table below shows how individual funds performed within my portfolio since my last review in December. Funds with exposure to US equities performed well, but particularly those exposed to more defensive sectors which didn't perhaps benefit as much from the initial phase of the Trump trade 2.0. But the rally in the US dollar versus the pound played its part too. It means that at the opposite end of the scale, UK equities lagged as did funds with exposure to assets that tend to underperform when the US dollar strengthens, namely gold and emerging market equities. The exception to that was Fidelity Index Japan, which I would have expected to have fared better in such an environment.

| Name | % return over the last month (since December review) |

| Artemis Global Income | 1.27 |

| M&G Global Dividend | 1.16 |

| Vanguard FTSE Developed World ex-UK Equity Index | 0.52 |

| Thesis TM Tellworth UK Select | 0.41 |

| Aviva Inv Global Equity Income | 0.32 |

| T. Rowe Price US Large Cap Growth Equity | 0.22 |

| abrdn High Yield Bond | 0.18 |

| Schroder Strategic Credit | 0.18 |

| Barclays Global Markets Adventurous | -0.18 |

| iShares Physical Gold ETC | -0.3 |

| Fidelity Index Japan | -0.33 |

| Ninety One UK Special Situations | -1.5 |

| Liontrust India | -2.13 |

As usual, the table below shows which funds within my portfolio are in the current BOTB or BFBS tables and which are not. Those funds in blue are still in the BOTB while those in orange are not in the BOTB but remain in the BFBS list. Meanwhile, any funds in red have dropped out of both shortlists.

| Fund | Allocation | Risk | Sector | ISIN |

| abrdn High Yield Bond | 14 | Lower | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11 | Medium | Global Equity Income | GB00B5N99561 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| Barclays Global Markets Adventurous | 8 | Medium | Flexible Investment | GB00B4YPY060 |

| Fidelity Index Japan | 3 | Medium | Japan | GB00BHZK8872 |

| iShares Physical Gold ETC | 6 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| Liontrust India | 6 | Higher | India/Indian Subcontinent | GB00B1L6DV51 |

| M&G Global Dividend | 5 | Medium | Global Equity Income | GB00B46J9127 |

| Ninety One UK Special Situations | 4 | Higher | UK All Companies | GB00B1XFJS91 |

| Schroder Strategic Credit | 8 | Lower | Sterling Strategic Bond | GB00BJZ2ZC09 |

| T. Rowe Price US Large Cap Growth Equity | 10 | Higher | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Lower | Targeted Absolute Return | GB00BNY7YM73 |

| Vanguard FTSE Developed World ex-UK Equity Index | 9.5 | Medium | Global | GB00B59G4Q73 |

Below is a list of the 'red' funds that have fallen out of both the BOTB and BFBS tables (the funds in bold were also in last month's red list):

- Aviva Inv Global Equity Income

- Barclays Global Markets Adventurous

- Fidelity Index Japan

- Liontrust India

- Vanguard FTSE Developed World ex-UK Equity Index

Given the overall performance of my portfolio, as stated earlier, I am not going to make significant changes for obvious reasons. Also as I've mentioned before, just because a fund drops out of the BOTB and BFBS tables it doesn't make it a bad fund, it signals that there are alternatives that are displaying more positive momentum at this moment in time.

However, I will be making 2 changes this month, namely moving out of Fidelity Index Japan and Liontrust India. Before I get on to those let me explain my reasoning for maintaining my holdings in the other 3 funds on the red list.

As I mentioned last time, Aviva Inv Global Equity Income is a member of the current most consistent funds list, and only dropped out of the BFBS table last month. I also noted how the fund had been a laggard in the Trump trade 2.0 partly because of the threat of trade tariffs on European exports to the US (the fund has a significant exposure to European equities). The fund received a stay of execution because it also invests differently to the other global equity funds within my portfolio (such as T. Rowe Price US Large Cap Growth Equity which invests heavily in US tech stocks) so is a good diversifier. Interestingly, this helped the fund outperform in the period since my last portfolio review, a period in which we've seen some of the Trump trade 2.0 euphoria abate and sectors which had lagged start to outperform. In fact, over the last month the performance of Aviva Inv Global Equity Income would place it 17th out of the 309 funds across the Global and Global Equity Income sectors. A fantastic performance. While I don't base my decisions purely on such short time frames, the fact that it is performing well in the current environment and is a long term consistent performer is reason to maintain my holding.

Barclays Global Markets Adventurous was first introduced to my portfolio back in November and had been performing strongly ahead of last month's portfolio review. As you can see from the earlier performance chart its performance over the last month has been more measured, on an absolute basis at least. This is most likely due to the rally in the US dollar hurting the fund's sizeable emerging market equity exposure. However if you consider the fund's performance on a relative basis (i.e. comparing it to its peers from the same sector) its performance ranks 16th out of 219 funds from the Flexible sector since my last portfolio review. If you include the funds from other multi-asset sectors (namely Mixed Investment 0-35% Shares, Mixed Investment 20-60% Shares and Mixed Investment 40-85% Shares sectors) the fund's performance over the last month would see it rank 38 out of 810 funds. It is also a top quartile performer within its sector over longer timeframes including 6 months and even 1 year. The point is that for a managed fund it continues to perform well, despite dropping out of the BFBS tables in recent weeks. I therefore will maintain the fund for now.

It's a similar story with Vanguard FTSE Developed World ex-UK Equity Index. While it may have fallen out of the BFBS and BOTB tables, it was in the BOTB as recently as last month. The fund is the 3rd best performing fund in my portfolio since my last review which would place it 8th out of the 309 funds across the Global and Global Equity Income funds. As you know I don't tend to make knee-jerk reactions on funds if they fall out of the BOTB or BFBS tables, as it may just be a sign that other funds have more momentum, not that my existing fund has necessarily lost momentum or is tumbling in value. So given the overall performance of the portfolio and the fund's recent performance I will keep it for now.

That leaves me with Fidelity Index Japan and Liontrust India. Fidelity Index Japan has been on the red list for some time now and therefore I think it's time to change things, especially given that it performed worse than its peers during the recent period of US dollar strength. I try to follow the asset mix of the BOTB as closely as possibly, while not obsessing over temporary differences. The BOTB does still have exposure to Japanese equities so I am going to do a like for like switch with Man Group Man Japan CoreAlpha which is from the same sector and is in the BOTB this month.

Liontrust India was the worst performing fund within my portfolio since my review in December. Despite a rally in November, the fund is now the worst performing fund within my portfolio over the last 1, 3 and 6 month periods. The fund has actually been the top performer within the India/Indian Subcontinent sector, but its recent lacklustre performance is perhaps more reflective of the fortunes of pure Indian equity funds generally. The BOTB now has no exposure to Indian equities at all, for the first time since 2023. So I am going to move out of a pure Indian equity fund and into Schroder Asian Discovery, which is in this month's BOTB. The Schroder Asian Discovery still has some exposure to Indian equities but also a significant exposure to Chinese equities, something that my portfolio has been lacking after I reduced my exposure to the region a few months ago. The Chinese equity exposure will equate to around 2% of my total portfolio which, although lower than that of the BOTB, starts to bring it back in line.

The rest of the funds within my portfolio remain in the BFBS and BOTB tables so I will maintain them as they are.

Fund switches

- 100% out of Fidelity Index Japan and 100% into Man Group Man Japan CoreAlpha

- 100% out of Liontrust India and 100% into Schroder Asian Discovery

My portfolio

My portfolio looks now like this:

| Fund | Allocation | Risk | Sector | ISIN Code |

| abrdn High Yield Bond | 14 | Lower | Sterling High Yield | GB00B79RR984 |

| Artemis Global Income | 11 | Medium | Global Equity Income | GB00B5N99561 |

| Aviva Inv Global Equity Income | 10 | Medium | Global Equity Income | GB0030441918 |

| Barclays Global Markets Adventurous | 8 | Medium | Flexible Investment | GB00B4YPY060 |

| iShares Physical Gold ETC | 6 | Medium | Commodity & Energy ETF | IE00B4ND3602 |

| M&G Global Dividend | 5 | Medium | Global Equity Income | GB00B46J9127 |

| Man Group Man Japan CoreAlpha | 3 | Higher | Japan | GB00B0119B50 |

| Ninety One UK Special Situations | 4 | Higher | UK All Companies | GB00B1XFJS91 |

| Schroder Asian Discovery | 6 | Medium | Asia Pacific Excluding Japan | GB00B5ZS9V71 |

| Schroder Strategic Credit | 8 | Lower | Sterling Strategic Bond | GB00BJZ2ZC09 |

| T. Rowe Price US Large Cap Growth Equity | 10 | Higher | North America | GB00BD5FHW12 |

| Thesis TM Tellworth UK Select | 5.5 | Lower | Targeted Absolute Return | GB00BNY7YM73 |

| Vanguard FTSE Developed World ex-UK Equity Index | 9.5 | Medium | Global | GB00B59G4Q73 |

My Portfolio asset mix

My portfolio asset mix has approximately 65% exposure to equities. Last month's figures are shown in brackets.

-

- UK Equities 12% (13%)

- North American Equities 27% (26%)

- Asian Equities 5% (2%)

- Chinese Equities 2% (0%)

- Emerging Market Equities 0% (6%)

- Japanese Equities 6% (5%)

- European Equities 8% (8%)

- Other International equity 5% (6%)

- Commodities and energy 6% (5%)

- UK Fixed Interest 4% (4%)

- Global Fixed Interest 18% (18%)

- Cash 0% (0%)

- Alternative Investment Strategies 7% (7%)

Damien's higher risk and lower risk portfolios

Using the logic described in my post: Update to Damien’s alternative risk portfolios I created hypothetical higher and lower risk versions of my portfolio below:

Lower risk

| Fund | Allocation % |

| abrdn High Yield Bond | 17 |

| Artemis Global Income | 13 |

| Aviva Inv Global Equity Income | 12 |

| Barclays Global Markets Adventurous | 10 |

| iShares Physical Gold ETC | 7 |

| Schroder Asian Discovery | 7 |

| M&G Global Dividend | 6 |

| Schroder Strategic Credit | 10 |

| Thesis TM Tellworth UK Select | 7 |

| Vanguard FTSE Developed World ex-UK Equity Index | 11 |

Higher risk

| Fund | Allocation % |

| Artemis Global Income | 15 |

| Aviva Inv Global Equity Income | 14 |

| Barclays Global Markets Adventurous | 11 |

| Man Group Man Japan CoreAlpha | 4 |

| iShares Physical Gold ETC | 8 |

| Schroder Asian Discovery | 8 |

| M&G Global Dividend | 7 |

| Ninety One UK Special Situations | 6 |

| T. Rowe Price US Large Cap Growth Equity | 14 |

| Vanguard FTSE Developed World ex-UK Equity Index | 13 |

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay