Bank of England Governor Andrew Bailey said, "I am content at the present time with holding, while accepting that risks to inflation and interest rates are on the upside...". He went on to state that he, "...would respond promptly to any signals that an extended period of elevated energy prices could be leading to stronger possible second-round effects".

What is the Bank of England base rate?

The Bank of England base rate determines how much the BoE pays commercial banks for holding money with it. This then influences how much those banks charge customers to borrow money or pay customers who deposit savings with them.

If the base rate goes down, it usually triggers a drop in the interest rates that banks and other lenders charge the public to take out loans, mortgages, and credit cards, as well as the interest rates they pay on savings. A base rate hike usually means interest rates are increased, and when the base rate is held, providers may still change rates depending on the future economic outlook.

Why has the Bank of England held the base rate?

The base rate is the primary tool the Bank of England uses to keep inflation stable and close to its 2% target. The majority of the committee judged that maintaining the rate at 3.75% was appropriate, as financial conditions have already tightened since the start of the Middle East conflict. Easing food inflation, which fell to 2.20%, and a gradual loosening of the labour market - with unemployment reaching 4.90% - have helped contain underlying domestic price pressures.

Furthermore, the recent announcement of a Middle East peace deal caused Brent crude oil and wholesale gas prices to drop to around $79 per barrel and 100 pence per therm, respectively. However, the committee remains cautious because energy prices remain volatile and higher than their pre-conflict levels.

The decision was finely balanced, with two members, Megan Greene and Huw Pill, voting for a proactive rate hike to 4%. They expressed concern that households and businesses are highly attentive to inflation, which could trigger larger "second-round" effects on wages and prices. Conversely, Governor Andrew Bailey and the remaining majority preferred to look through temporary energy shocks on the understanding that the slowing UK economy is ultimately keeping inflation in check, at least in the short term.

Where will interest rates go in 2026?

When looking at what might happen to interest rates over the next year, there are currently two different views. A recent survey of financial experts shows that most expect the Bank of England base rate to remain unchanged for the next 12 months. However, financial markets are telling a slightly different story, with market data suggesting a small rate increase of around 0.30% by the end of 2026.

The Bank of England has suggested that this slight upward trend is essentially the market 'playing it safe', stating that "the upward slope of the OIS curve was driven largely by risk premia". It has reiterated that it will closely monitor how energy price adjustments are affecting the wider UK economy, stating that it "stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term".

If you are interested in learning more about where interest rates might go in the future, check out our article on the latest UK interest rate predictions.

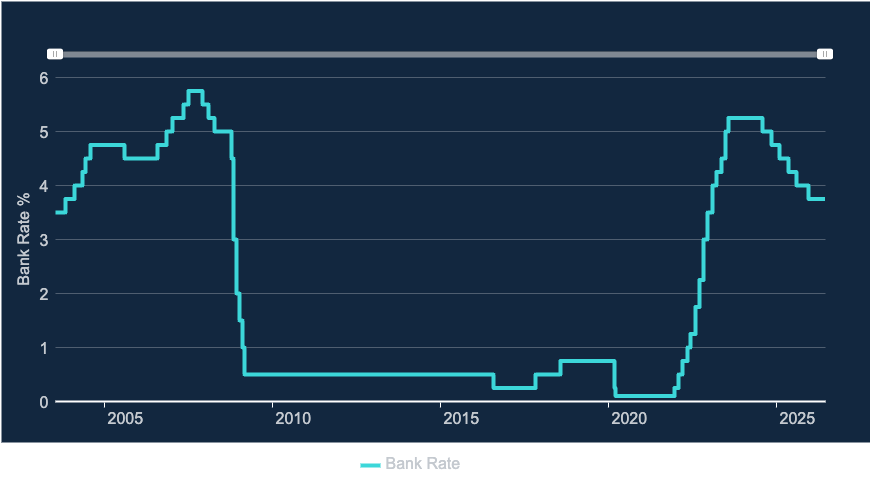

How has the BoE base rate changed over time?

The graph below shows how the Bank of England base rate has fluctuated dramatically over time, either side of long periods of stability.

(Source: Bank of England)

Base Rate changes and how they impact you: December 2021 - June 2026

The table below shows the impact of the base rate decisions by the Bank of England since December 2021 on a £100,000 mortgage borrowed over 25 years:

| Date | Interest rate change | Previous interest rate | New interest rate | Change to average monthly mortgage repayments per £100k borrowed* |

| 16th December 2021 | +0.15% | 0.10% | 0.25% | +£8 |

| 2nd February 2022 | +0.25% | 0.25% | 0.50% | +£13 |

| 17th March 2022 | +0.25% | 0.50% | 0.75% | +£13 |

| 5th May 2022 | +0.25% | 0.75% | 1.00% | +£13 |

| 16th June 2022 | +0.25% | 1.00% | 1.25% | +£13 |

| 4th August 2022 | +0.50% | 1.25% | 1.75% | +£26 |

| 22nd September 2022 | +0.50% | 1.75% | 2.25% | +£26 |

| 2nd November 2022 | +0.75% | 2.25% | 3.00% | +£39 |

| 15th December 2022 | +0.50% | 3.00% | 3.50% | +£26 |

| 2nd February 2023 | +0.50% | 3.50% | 4.00% | +£26 |

| 23rd March 2023 | +0.25% | 4.00% | 4.25% | +£13 |

| 11th May 2023 | +0.25% | 4.25% | 4.50% | +£13 |

| 22nd June 2023 | +0.50% | 4.50% | 5.00% | +£26 |

| 3rd August 2023 | +0.25% | 5.00% | 5.25% | +£13 |

| 21st September 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 2nd November 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 13th December 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 1st February 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 21st March 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 9th May 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 20th June 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 1st August 2024 | -0.25% | 5.25% | 5.00% | -£13 |

| 19th September 2024 | +0.00% | 5.00% | 5.00% | £0 |

| 7th November 2024 | -0.25% | 5.00% | 4.75% | -£13 |

| 19th December 2024 | +0.00% | 4.75% | 4.75% | £0 |

| 6th February 2025 | -0.25% | 4.75% | 4.50% | -£13 |

| 20th March 2025 | +0.00% | 4.50% | 4.50% | £0 |

| 8th May 2025 | -0.25% | 4.50% | 4.25% | -£13 |

| 19th June 2025 | +0.00% | 4.25% | 4.25% | £0 |

| 7th August 2025 | -0.25% | 4.25% | 4.00% | -£13 |

| 18th September 2025 | +0.00% | 4.00% | 4.00% | £0 |

| 6th November 2025 | +0.00% | 4.00% | 4.00% | £0 |

| 18th December 2025 | -0.25% | 4.00% | 3.75% | -£13 |

| 5th February 2026 | +0.00% | 3.75% | 3.75% | £0 |

| 19th March 2026 | +0.00% | 3.75% | 3.75% | £0 |

| 30th April 2026 | +0.00% | 3.75% | 3.75% | £0 |

| 18th June 2026 | +0.00% | 3.75% | 3.75% | £0 |

| TOTAL | £190 |

*assumed mortgage term of 25 years

How does the Bank of England interest rate decision affect mortgages?

Fixed-rate mortgage customers

Anyone with a fixed-rate mortgage will not see their mortgage rate or monthly repayments change as a result of a BoE decision, but if your deal is due to end soon, you should still consider how mortgage rates might change in the coming months. Our article 'Will interest rates continue to fall in 2026 or start going back up?' provides some insight into remortgaging and what to do if you are due to remortgage soon. If your mortgage deal is due to end in less than 6 months, you can start to shop around, so it may be beneficial to speak to a mortgage adviser. Mortgage interest rates have begun to move upwards, with lenders repricing frequently, so securing a good deal when it comes up could provide significant savings on your new monthly mortgage payment and the overall cost of your mortgage.

It is worth remembering that if your current fixed-rate deal was in place prior to December 2021 (before rates first started going up), then you should factor in all of the subsequent base rate rises and cuts in order to budget for the likely increase in your monthly mortgage repayments after you remortgage. As shown in the table above, this equates to a monthly increase of £190 per £100,000 borrowed, based on a 25-year mortgage term.

Many borrowers choose to extend their mortgage term when arranging a new mortgage or remortgaging an existing deal, to make monthly repayments more affordable. This may help in the short term for those struggling with higher mortgage interest rates, but it will mean the debt is carried further into the future and will end up costing them more in interest payments over the long term. Extending your mortgage term should be considered carefully with the help of an independent mortgage expert*.

Variable rate or tracker mortgage customers

Those with tracker or variable-rate mortgages tend to see their mortgage rates (and monthly repayments) change in line with the base rate. If you wish to see what a future rate cut or hike by the Bank of England would do to your monthly mortgage payment, you can use our interest rate calculator. You will need to know your initial mortgage term, the amount you borrowed at the start of the deal and your current mortgage rate.

Anyone wanting to know more about how rate rises and cuts impact their finances should speak with an independent mortgage adviser* for specialist advice. When considering remortgaging, always check the remaining term of your current mortgage deal and whether there are any Early Repayment Charges (ERC). Take a look at the best mortgage deals by using our mortgage rate comparison tool or checking out our article 'Best mortgage rates in the UK'.

Help if you're unable to afford your mortgage payments

Many mortgage holders continue to face higher costs due to rising mortgage interest rates since 2021. If you are worried about how you will afford your mortgage, then you should get in touch with your lender as soon as possible. Your lender should be able to find a solution that can help ensure no repayments are missed.

Potential solutions can include extending the length of your mortgage, converting part or all of your repayment mortgage to an interest-only mortgage or allowing you to take a mortgage payment holiday.

Check out our article 7 tips for dealing with mortgage arrears, or alternatively, you may find additional support from the following organisations helpful:

If a link has an * beside it this means that it is an affiliated link. If you go via the link Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. But as you can clearly see this has in no way influenced this independent and balanced review of the product. The following link can be used if you do not wish to help Money to the Masses - VouchedFor

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay