The decision comes as global events heap renewed pressure on the UK economy. The Bank noted that the ongoing conflict in the Middle East has created significant uncertainty around global energy prices, which is already beginning to impact domestic living costs.

Bank of England Governor Andrew Bailey warned that "the war in the Middle East is causing inflation to rise again this year" and an energy "supply shock" had hit the UK economy, though the country is in a different position than it was during the 2022 energy crisis.

He noted: "So far, this shock differs from 2022 as the increase in energy prices has been smaller, monetary policy started more restrictive and the labour market is weaker... For now, the softer real economy makes it appropriate to maintain Bank Rate."

What is the Bank of England base rate?

The Bank of England base rate determines how much the BoE pays commercial banks for holding money with it. This then influences how much those banks charge customers to borrow money or pay customers who deposit savings with them.

If the base rate goes down, it usually triggers a drop in the interest rate that banks and other lenders charge the public to take out loans, mortgages and credit cards, as well as the interest rate they pay out on savings. A base rate hike will usually mean interest rates are increased, and when the base rate is held, providers may still change rates, depending on the future economic outlook.

Why has the Bank of England held the base rate?

The base rate is the primary tool used by the Bank of England to help control inflation. While the government target is to keep inflation at 2%, the latest figures show that the Consumer Prices Index (CPI) measure of inflation has risen to 3.3%, with the expectation that it will rise further in the coming months.

Despite this disparity and rising global energy prices, the majority of the committee opted to freeze the base rate rather than increase it. This decision was largely driven by evidence of a weakening UK economy and a cooling labour market. The committee judged that current financial conditions are restrictive enough to help reduce inflation over time, and that raising rates now could put unnecessary strain on economic growth.

According to the BoE's April Monetary Policy Summary, the committee is carefully monitoring the risk of what it calls "second-round effects". This refers to the possibility that businesses might raise their prices further to protect their profit margins, or that workers might demand higher pay to cope with the rising cost of living.

However, the committee suggested that lower consumer demand and rising unemployment could naturally limit these additional price increases, providing time to observe how the economy reacts before making further rate changes.

Where will interest rates go in 2026?

In a complete reversal of the situation before the war in the Middle East, an interest rate increase is now fully priced in by the swaps market. A quarter-point hike by July - taking the rate back up to 4% - is expected to be the Bank of England's next move, and further hikes could follow. However, this depends on how events in the Middle East dictate UK inflation.

As the Bank's role is to work to keep UK inflation at a target of 2%, it will opt to raise rates in order to curb inflation. Oil prices are going to be a significant contributor to inflation, but if 'second-round' effects are likely to be weak, it will be more challenging for higher global costs to embed in UK pay and prices. Essentially, if unemployment is rising, wage growth is stagnating and consumer confidence is shaky, it will be harder for businesses to increase prices or employee wages.

The Bank outlined three potential scenarios for the UK economy:

- Scenario A - Oil prices peak around $110 a barrel and fall back below $80 before the end of 2026, where they stay. Inflation peaks at 3.6% in 2026 and GDP weakens to around 0.5% by the start of 2027 before recovering.

- Scenario B - Oil stays above $80 a barrel and inflation peaks at 3.7% due to second-round effects, particularly from food inflation. GDP weakens to around 0.5% by the start of 2027 before recovering.

- Scenario C - Oil prices remain above $120 a barrel for the rest of this year. Inflation peaks at 6.2% in the first three months of 2027, triggering the Bank to hike interest rates as high as 5.25%.

Andrew Bailey said: "At the moment, I place most weight on Scenario B, albeit with slightly reduced second-round effects. I place some weight on Scenario C, which would require a stronger monetary policy response. For now, the softer real economy makes it appropriate to maintain Bank Rate."

If you are interested in learning more about where interest rates might go in the future, check out our article on the latest UK interest rate predictions.

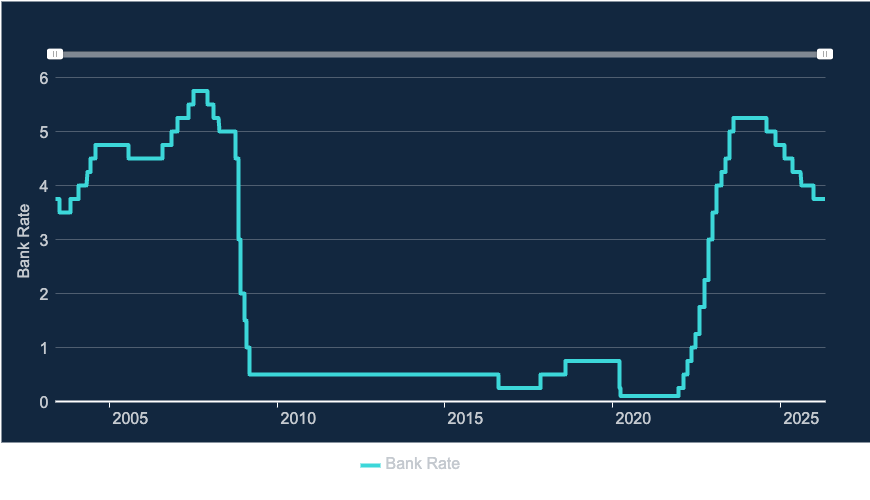

How has the BoE base rate changed over time?

The graph below shows how the Bank of England base rate has dramatically dipped and soared over time, either side of long periods of stability.

(Source: Bank of England)

Base Rate changes and how they impact you: December 2021 - April 2026

The table below shows the impact of the base rate decisions by the Bank of England since December 2021 on a £100,000 mortgage borrowed over 25 years:

| Date | Interest rate change | Previous interest rate | New interest rate | Change to average monthly mortgage repayments per £100k borrowed* |

| 16th December 2021 | +0.15% | 0.10% | 0.25% | +£8 |

| 2nd February 2022 | +0.25% | 0.25% | 0.50% | +£13 |

| 17th March 2022 | +0.25% | 0.50% | 0.75% | +£13 |

| 5th May 2022 | +0.25% | 0.75% | 1.00% | +£13 |

| 16th June 2022 | +0.25% | 1.00% | 1.25% | +£13 |

| 4th August 2022 | +0.50% | 1.25% | 1.75% | +£26 |

| 22nd September 2022 | +0.50% | 1.75% | 2.25% | +£26 |

| 2nd November 2022 | +0.75% | 2.25% | 3.00% | +£39 |

| 15th December 2022 | +0.50% | 3.00% | 3.50% | +£26 |

| 2nd February 2023 | +0.50% | 3.50% | 4.00% | +£26 |

| 23rd March 2023 | +0.25% | 4.00% | 4.25% | +£13 |

| 11th May 2023 | +0.25% | 4.25% | 4.50% | +£13 |

| 22nd June 2023 | +0.50% | 4.50% | 5.00% | +£26 |

| 3rd August 2023 | +0.25% | 5.00% | 5.25% | +£13 |

| 21st September 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 2nd November 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 13th December 2023 | +0.00% | 5.25% | 5.25% | £0 |

| 1st February 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 21st March 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 9th May 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 20th June 2024 | +0.00% | 5.25% | 5.25% | £0 |

| 1st August 2024 | -0.25% | 5.25% | 5.00% | -£13 |

| 19th September 2024 | +0.00% | 5.00% | 5.00% | £0 |

| 7th November 2024 | -0.25% | 5.00% | 4.75% | -£13 |

| 19th December 2024 | +0.00% | 4.75% | 4.75% | £0 |

| 6th February 2025 | -0.25% | 4.75% | 4.50% | -£13 |

| 20th March 2025 | +0.00% | 4.50% | 4.50% | £0 |

| 8th May 2025 | -0.25% | 4.50% | 4.25% | -£13 |

| 19th June 2025 | +0.00% | 4.25% | 4.25% | £0 |

| 7th August 2025 | -0.25% | 4.25% | 4.00% | -£13 |

| 18th September 2025 | +0.00% | 4.00% | 4.00% | £0 |

| 6th November 2025 | +0.00% | 4.00% | 4.00% | £0 |

| 18th December 2025 | -0.25% | 4.00% | 3.75% | -£13 |

| 5th February 2026 | +0.00% | 3.75% | 3.75% | £0 |

| 19th March 2026 | +0.00% | 3.75% | 3.75% | £0 |

| 30th April 2026 | +0.00% | 3.75% | 3.75% | £0 |

| TOTAL | £190 |

*assumed mortgage term of 25 years

How does the Bank of England interest rate decision affect mortgages?

Fixed-rate mortgage customers

Anyone with a fixed-rate mortgage will not see their mortgage rate or monthly repayments change as a result of a BoE decision, but if your deal is due to end soon, you should still consider how mortgage rates might change in the coming months. Our article 'Will interest rates continue to fall in 2026 or start going back up?' provides some insight into remortgaging and what to do if you are due to remortgage soon. If your mortgage deal is due to end in less than 6 months, you can start to shop around, so it may be beneficial to speak to a mortgage adviser. Mortgage interest rates have begun to move upwards, with lenders repricing frequently, so securing a good deal when it comes up could provide significant savings on your new monthly mortgage payment and the overall cost of your mortgage.

It is worth remembering that if your current fixed-rate deal was in place prior to December 2021 (before rates first started going up), then you should factor in all of the subsequent base rate rises and cuts in order to budget for the likely increase in your monthly mortgage repayments after you remortgage. As shown in the table above, this equates to a monthly increase of £190 per £100,000 borrowed, based on a 25-year mortgage term.

Many borrowers choose to extend their mortgage term when arranging new mortgages or remortgaging existing deals, in order to make monthly repayments more affordable. This may help in the short-term for those struggling with higher mortgage interest rates but it will mean that the debt is carried further into the future and will end up costing them more in interest payments over the long-term. Extending your mortgage term should be considered carefully with the help of an independent mortgage expert*.

Variable rate or tracker mortgage customers

Those with tracker or variable-rate mortgages tend to see their mortgage rates (and monthly repayments) change in line with the moves in the base rate. If you wish to see what a future rate cut or hike by the Bank of England would do to your monthly mortgage payment, you can use our interest rate calculator. You will need to know your initial mortgage term, the amount you borrowed at the start of the deal and your current mortgage rate.

Anyone wanting to know more about how rate rises and cuts impact their finances should speak with an independent mortgage adviser* as they can provide specialist advice. When considering remortgaging, always check for any Early Repayment Charges (ERC) and the remaining term of your current mortgage deal. Take a look at the best mortgage deals by using our mortgage rate comparison tool or checking out our article 'Best mortgage rates in the UK'.

Help if you're unable to afford your mortgage payments

Many mortgage holders continue to face increasing costs due to the rise in mortgage interest rates since 2021. If you are worried about how you will afford your mortgage, then you should get in touch with your lender as soon as possible. Your lender should be able to find a solution that can help ensure no repayments are missed.

Potential solutions can include extending the length of your mortgage, converting part or all of your repayment mortgage to an interest-only mortgage or allowing you to take a mortgage payment holiday.

Check out our article 7 tips for dealing with mortgage arrears, or alternatively, you may find additional support from the following organisations helpful:

If a link has an * beside it this means that it is an affiliated link. If you go via the link Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. But as you can clearly see this has in no way influenced this independent and balanced review of the product. The following link can be used if you do not wish to help Money to the Masses - VouchedFor

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay