![]()

We have broken down this PensionBee review into sections but I suggest that you read the full review from beginning to end because, in short, I think PensionBee is suitable for certain people but not all (I explain who exactly in the full review).

If you want to jump to a particular part of this PensionBee review then use the links below.

- How does PensionBee work?

- What's the difference between the PensionBee plans

- What are PensionBee’s fees and how does it compare?

- PensionBee investment performance

- Who should consider using PensionBee?

1 minute summary - PensionBee Review

- PensionBee* can help you to find old pension pots, consolidating them into one easy-to-manage and low-cost pension plan

- Provide as much information as you can including your employer name, the dates you were employed and pension provider if known. PensionBee will track down your old pension and begin the process of transferring it, notifying you if they find any exit fees in excess of £10. You'll also be notified if your pension has any special benefits or guarantees.

- PensionBee has 7 plans of varying risk levels to choose from and includes a Sharia-compliant plan

- Fees range from 0.50% to 0.95% depending on the plan you choose. Fees are halved on all investments over £100,000

- Plans can be managed online or via the PensionBee app*

PensionBee

Combine, contribute and withdraw online. Take control of your retirement and join 315,000 customers saving with PensionBee.

- Sign up in minutes

- Make flexible contributions and withdrawals¹

Who is PensionBee?

PensionBee is authorised and regulated by the Financial Conduct Authority and has amassed 315,000 since it was launched in the UK in 2014. Based just outside of London's financial centre it is attempting to innovate the UK pension industry by making it easier for people to locate and consolidate their existing pension plans. In April 2021, Pensionbee floated on the London Stock Exchange. In February 2025, PensionBee announced a partnership with Clearscore, with the aim of providing consumers with greater visibility and control over their financial futures by integrating pension management tools directly into ClearScore’s “Credit Health” section.

What does PensionBee do?

Most UK consumers only engage with saving for their retirement when they are enrolled into their employer's pension scheme. With most adults in the UK changing employers every few years it means that they can end up having several small pension pots stuck in past employers' pension schemes. Typically people lose track of these pensions over time and forget that they even have them (or they've lost touch with the previous companies that they've worked for) when they come to retire. However, it's not just an issue at retirement. Many of these pension pots will languish in poorly performing pension funds with high charges. It is therefore important that consumers review their pension planning which includes finding and optimising their existing pension plans and consolidating them where it is appropriate. By doing so they can ensure that they minimise the impact of high investment charges while optimising investment performance and the growth of their pension pot. At present, you can trace lost pensions using the free pension tracing service but it is a long-winded process and then you are still left with deciding what to do with them.

With only 1 in 10 UK consumers seeking financial advice it means that most UK consumers are not planning for their retirement. Historically, pension products have been a minefield of high charges, hidden caveats and complex legislation. However, in the last decade, I've seen this radically change thanks to regulatory changes and increased competition between pension providers and technology.

PensionBee is harnessing all three of these to provide a service that will locate your existing pension pots and consolidate them into a new low-cost pension plan (I look at their charges and performance later in this article). The first thing to point out is that PensionBee does not provide financial advice. Where this becomes an issue is if you have an existing final salary pension or a pension with over £30,000 of guaranteed benefits then current pension rules stipulate that you have to take financial advice before you can transfer it. While PensionBee can facilitate the consolidation of any of your other pensions I would suggest that you speak to a financial adviser if you are unsure. If you don't have a financial adviser, you can arrange a FREE pension consultation* with an independent, well-rated financial adviser who is local to you.

For those people with existing personal pensions or money purchase arrangements from past employers then PensionBee can consolidate these at no initial cost, into a cheap pension plan which is managed by a third-party investment company (i.e. BlackRock, HSBC, State Street Global Advisors or Legal & General). Having grilled the founders of PensionBee, its desire to champion the consumer is central to its business. It's led to lobbying Parliament to facilitate faster pension switching (on a par with current account switching) because, despite the wave of new entrants, facilitating a pension transfer is still a time-consuming and laborious process.

It is important to point out that there is nothing to stop you from using PensionBee to consolidate your pension plans into a low-cost pension and ultimately transfer elsewhere later. PensionBee does not charge you for consolidating your pension nor does it charge exit charges. I was quite frank with PensionBee on this point but it has deliberately set its proposition up this way showing its belief in its product and services. That is probably why PensionBee's proposition has attracted over 275,000 customers in a relatively short space of time and has been scored so highly by its customers on Trustpilot.

It is worth noting that the self-employed can now take out a PensionBee plan without having to consolidate past pensions, but pension consolidation still remains PensionBee's primary focus.

How does PensionBee work?

When you first start with PensionBee you have to choose between one of seven plans.

What's the difference between the PensionBee plans

The only difference is the fund your pension pot will be invested in. These are:

- PensionBee Tracker (managed by State Street Global Advisors)

- PensionBee Global Leaders (managed by BlackRock)

- PensionBee Climate (managed by State Street Global Advisers)

- PensionBee 4 Plus (managed by State Street Global Advisers)

- PensionBee Shariah (managed by HSBC Global Asset Management & State Street Global Advisers)

- PensionBee Preserve (managed by State Street Global Advisers)

- PensionBee Pre-Annuity (managed by State Street Global Advisers)

Here is a brief explanation of how each plan is managed:

The PensionBee Tracker plan invests your money in global shares, bonds and cash, following the world's markets as they move. It is described as a medium risk plan and invests in a mix of assets, including equities and bonds. The plan is managed by State Street Global Advisors and PensioBee suggests that it should be suitable for those that want a cost effective ‘set and forget' investment.

The PensionBee Global Leaders plan was launched in February 2025 and is its default pension option for those under 50. The plan aims to grow pension savings by investing in around 1,000 of the world’s largest and most recognised public companies. It is described as ‘higher-risk' and 100% of the fund is invested in equities, 70% of which are US.

The PensionBee Climate plan (previously labelled ‘Impact') was launched in September 2023. It aims for the total carbon emissions produced by the plan’s companies to be reduced by at least 10% each year. It may be a good option for those who wish to only invest in companies that are taking action to reduce their carbon emissions and lead the transition to a low-carbon economy.

The PensionBee Shariah plan is as you would expect, a plan that invests money into Shariah-compliant companies and is aimed towards people who wish to invest according to their faith and those that want to invest responsibly.

The PensionBee 4 Plus plan is the default plan for those over 50. It aims to achieve long term growth of 4% per year (above the Bank of England base rate) by actively managing your money over a range of investments. The range of assets are adjusted on a weekly basis depending on market conditions and PensionBee say that this plan could be suitable for ‘anyone who is considering accessing their pension in the near to medium term and wishes for their returns to be actively managed by experts in the meantime'.

The PensionBee Preserve plan makes short-term investments into credit-worthy companies, focusing on reducing risk and thus preserving your money. This plan is very low risk and will typically return less as a result.

The PensionBee Pre-Annuity plan invests money in bonds to provide investors with returns that broadly correspond with the cost of purchasing an annuity.

PensionBee does not provide any risk profiling or recommendations as to which plan would suit you and so it would be wise to look at each plan to see which one is likely to help you meet your investment goals. We have analysed each of the PensionBee plans and provided the current asset mix in the table below.

Asset mix of each PensionBee plan

| Asset Type | Equity | Fixed Income | Cash | Other |

| PensionBee Sharia Plan | 100% | 0% | 0% | 0% |

| PensionBee Global Leaders Plan | 100% | % | 0% | 0% |

| PensionBee Tracker Plan | 80% | 20% | 0% | 0% |

| Pensionbee Climate Plan | 100% | 0% | 0% | 0% |

| PensionBee Preserve Plan | 0% | 100% | 0% | 0% |

| PensionBee Pre-Annuity Plan | 0% | 99% | 1% | 0% |

| PensionBee 4 Plus Plan | 57% | 30% | 8% | 6% |

PensionBee

Combine, contribute and withdraw online. Take control of your retirement and join 315,000 customers saving with PensionBee.

- Sign up in minutes

- Make flexible contributions and withdrawals¹

Consolidating your pensions

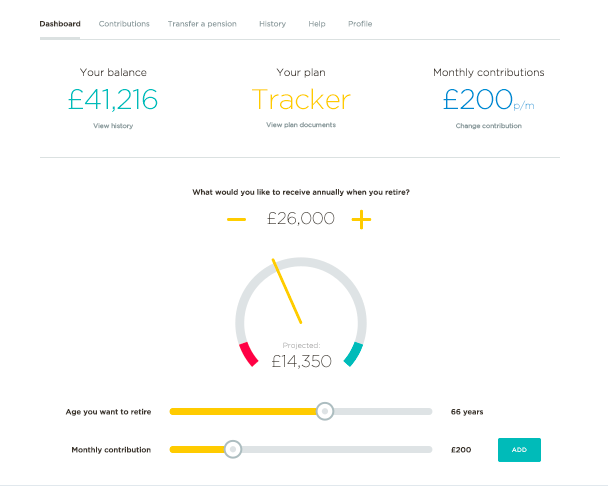

After you have chosen your desired plan you then provide as much detail as you can about your existing pension plans you wish to consolidate. PensionBee will then begin finding your existing pension plans and will notify you if any of them have guaranteed benefits or exit penalties over £10. Assuming there are no hurdles then it will get on with the task of facilitating the transfer of your pensions into the PensionBee pension plan you've selected. Once the wheels are set in motion you don't need to do anything but all the while you are free to change your mind within 30 days.

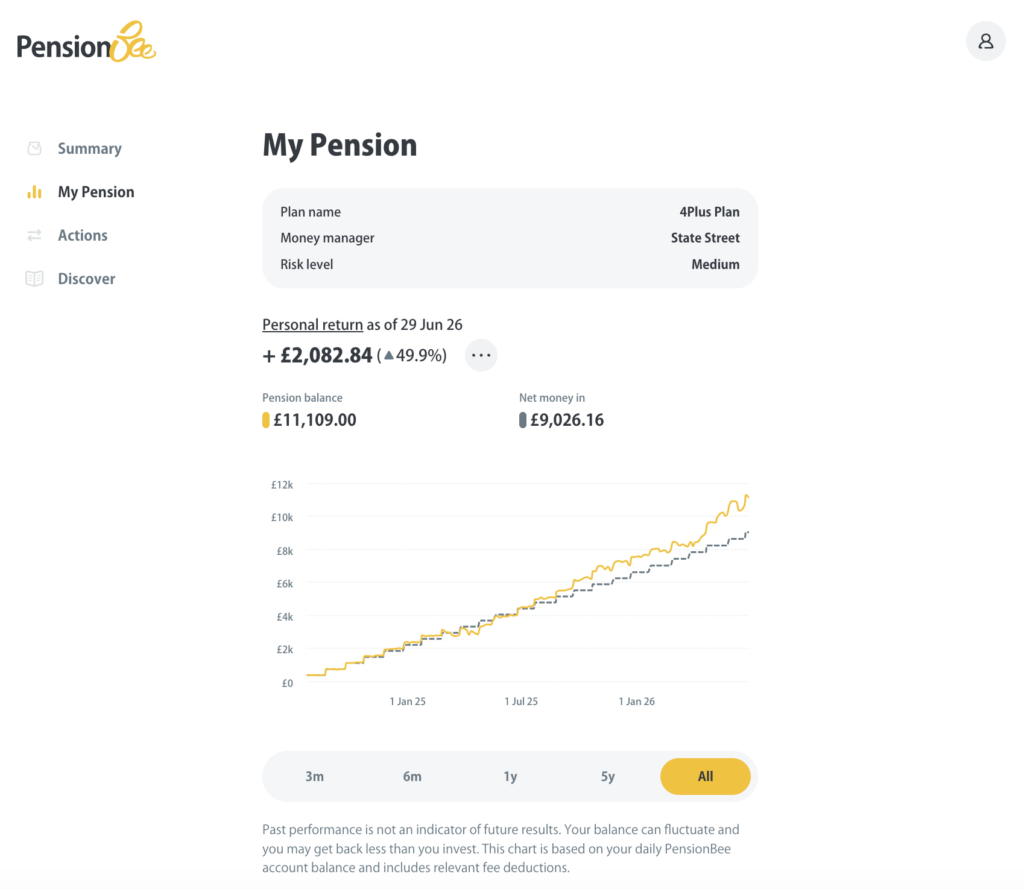

Eventually you can then manage, top-up and view your PensionBee pension online (as shown below) or via their smartphone app. The latter is particularly attractive for those who wish to make adhoc pension contributions, such as the self-employed (who in fact can now open a PensionBee pension without needing to transfer an existing pension).

What is PensionBee’s fee and how does it compare?

PensionBee's charges range from 0.50% to 0.95% a year depending on the plan you choose and it will halve the fee on all investments over £100,000 (so if you had a pension fund worth £150,000 in the PensionBee Tracker plan, you would be charged 0.50% on the first £100,000 and 0.25% on the remaining £50,000) If you click through to the PensionBee charges page* you can check the fees for each plan and they are very competitively priced, especially when compared to other pension providers such as Hargreaves Lansdown* and Nutmeg. Based on PensionBee's stated charges it would make its pension product one of the cheapest in the market. PensionBee does not charge any other administration fees or withdrawal fees. However. if your pension pot has been with PensionBee for less than a year and you wish to withdraw it in full, then a full withdrawal fee of £150 applies.

PensionBee plan fees

| Plan Name | Annual Fee (Under £100,000) | Annual Fee (Over £100,000 |

Estimated Underlying Transaction Costs*

|

| Global Leaders | 0.70% | 0.35% | ~0.04% |

| 4Plus | 0.85% | 0.43% | ~0.04% |

| Tracker | 0.50% | 0.25% | ~0.04% |

| Climate | 0.75% | 0.38% | ~0.04% |

| Shariah | 0.95% | 0.48% | ~0.04% |

| Preserve | 0.50% | 0.25% | ~0.04% |

| Pre-Annuity | 0.70% | 0.35% | ~0.04% |

*Underlying transaction costs are estimated at around 0.04% per year. These are charged by the underlying fund managers (such as BlackRock/State Street Global Advisors etc) for their trading activities and are separate from PensionBee's annual management fee

PensionBee portfolio performance

PensionBee has a number of plans which have limited performance history so it's not possible to analyse past performance to the level that I normally would in such a review. However, PensionBee provides factsheets for each fund*, which give some insight into past performance where available.

However I have been able to analyse the PensionBee Tracker plan, using third-party data, and compared it against the average active managed fund and the leading passive tracker fund with equivalent equity exposure. Active funds are those run by fund managers who make judgement calls on where to invest and typically are more expensive (between 1.5 and 2.5% per annum).

Passive funds on the other hand simply track chosen market indexes and are run by computer algorithms. Therefore they are cheaper to run (as low as 0.20% per annum). PensionBee uses passive funds. There is much debate over whether active fund managers deliver the outperformance they promise, all the while making themselves huge profits from their high fees. Over the long term they don't, but over the short term they occasionally do.

The PensionBee Tracker plan invests in the State Street Global Advisors Balanced Index sub fund. The table below compares its performance over 1 year, 3 years and 5 years.

| Fund | 1yr performance % | 3yr Cumulative performance % | 5 yr Cumulative performance % |

| Typical multi-asset managed fund | 13.00 | 7.78 | 24.53 |

| PensionBee Tracker | 17.54 | 15.87 | 33.86 |

| Passive tracker benchmark | 14.95 | 16.83 | 41.75 |

For the passive tracker benchmark I used the market-leading Vanguard Lifestrategy 80% equity fund and the Typical multi-asset managed fund was based upon the sector average for the Mixed Investment 40-85% Shares unit trust sector.

The upshot is that the underlying funds used in the PensionBee Tracker fund have outperformed the typical managed fund over 5 years. However, it has underperformed the leading passive tracker fund, but then again nearly all active and passive funds have. So to sum up:

- If you are just interested in growing your pension plans the PesionBee Global Leaders option will interest you or possibly the Climate plan if you want to invest ethically

- If you want to manage downside risks while growing your money then the PensionBee Preserve plan is likely to appeal

PensionBee vs the Government’s Pension Dashboard

One of the criticisms that have been pointed in the direction of PensionBee is whether the government's planned Pension Dashboard will make PensionBee's biggest selling point of finding and consolidating pensions online obsolete. The Pension Dashboard was earmarked for a launch sometime in 2019 and was supposed to allow everyone to see where all their pension pots are, how much they are worth and their potential retirement income. While the dashboard ecosystem is currently in its connection phase, the final deadline for all providers to connect is 31 October 2026.

It is worth remembering that even when it does fully launch, it will simply show information to consumers and won't allow any form of consolidation. Of course, an individual could take the dashboard information and use other services or a financial adviser to consolidate their pensions.

Does PensionBee have an app?

Yes. The PensionBee app is available on both iOS and Android and has recently been overhauled to streamline navigation, enhance plan visibility, and give savers a clearer, comprehensive view of their retirement goals. Among the many improvements are better visibility over what’s happening with pension transfers and a far more detailed breakdown of how and where your money is being invested,

The app offers a ‘unified' experience, meaning users will find the exact same features and layout whether they manage their pension via their smartphone or on a desktop computer.

PensionBee drawdown process

PensionBee now offers a digital withdrawal process via its app. While this provides customers with easy access to their pension fund via a digital interface, it places greater responsibility on the user to understand the implications of their withdrawal decisions, especially concerning tax and the longevity of their pension fund. The minimum age to access your pension is currently 55, but this is set to increase to 57 in 2028. PensionBee actively promotes tools like its drawdown calculator, as well as access to its BeeKeepers to provide support and guidance, however, it is important to remember that this is not regulated pension advice. Users who are not uncomfortable making retirement decisions based on the information and support provided through the platform should seek independent advice.

Is PensionBee any good?

If you don't have a final salary pension and are looking to spring clean your existing pension pots and consolidate them then PensionBee is a viable option. This is especially true if you prioritise ease of use, acceptable fund performance and low costs over investment choice and the ability to run your investments yourself. PensionBee is also the first pension provider to adopt ‘simpler annual statements', a government-led initiative to provide better transparency and control. In addition, the self-employed will also be attracted to the ease of use especially when it comes to topping up their pension as and when required via the app. The self-employed can also now open a PensionBee plan without the need to transfer an existing pension across. Have a quick look at PensionBee's FAQ tab* as it covers some important considerations.

PensionBee Pros

- Low cost

- Clear charging structure

- No exit fees or lock-ins

- Simple pension consolidation process

- Decent historical investment performance

- Good customer service and user ratings

- Neat iPhone / Android app and online dashboard making managing your pension simple

- Low hassle factor

- Nothing to stop you using them to consolidate your pensions before moving elsewhere

- Provides ‘simpler annual statements' giving investors better clarity and control

- Easy online drawdown proces

PensionBee Cons

- It doesn't offer financial advice nor can it help with final salary transfers

- Each plan has one fund so what you gain in cost savings and relative performance you lose in investment choice

- If you have been with PensionBee for less than one year, there is a £150 fee if you decide to withdraw your pension pot in full.

What protection is there if I make the wrong decision or PensionBee goes bust?

PensionBee does not give regulated advice and as such the choice to move your pensions is yours alone. However, you can change your mind within 30 days of transferring a pension to PensionBee, and it will send the money back to your previous provider, assuming they will accept it, without any charge. If PensionBee was to go bust customers would get back 100% of their pension. PensionBee pensions are protected via the Financial Services Compensation Scheme (FSCS).

PensionBee Customer Reviews

Clearly, PensionBee's customers like its ethos and product. On Trustpilot it is rated as ‘Excellent' and has an average score of 4.6 out of 5.0 from over 13,200 reviews. Below are some examples of some recent customer reviews.

‘Excellent service getting all my pension in to one easy pension can see daily how it’s all going keep in touch regularly bye emails and easy to contact bye phone calls' – Blaine

‘The set up has been easy and funds have been transferred from disparate pensions from over the years into one pot. Easy to use and hassle free' – Matthew

‘PensionBee was such a simple process for my employer and for my personal transfers. They even worked with my other providers directly on the transfers, where other companies leave the client to resolve all issues. I am really happy that PensionBee did the work for me!' – Brittney

Should you invest with PensionBee?

If you are looking for a low-cost hassle-free way to consolidate your pension pots (excluding final salary pension) then PensionBee* is worth considering especially as it does not lock you in with exit penalties. This leaves you free to move at a future date. However, its average investment fund performance, low cost and slick app interface have clearly been integral in it gaining over 275,000 customers so quickly. If you have a final salary pension that you don't know what to do with then read my article ‘Should I transfer my final salary pension‘.

When investing, your capital is at risk and you may get back less than invested. Past performance doesn’t guarantee future results.

If a link has an * beside it this means that it is an affiliated link. If you go via the link Money to the Masses may receive a small fee which helps keep Money to the Masses free to use. But as you can clearly see this has in no way influenced this independent and balanced review of the product. The following link can be used if you do not wish to help Money to the Masses or take advantage of any exclusive offers – Pensionbee, Hargreaves Lansdown, Unbiased

£200 Pension Cashback Offer

Make a qualifying deposit or transfer a pension to our partner Interactive Investor.

- Deposit or transfer a pension of at least £20k and you could earn £200 cashback

- Terms and Fees apply, Capital at risk

- New & Existing customers opening a SIPP

- Offer ends 31st July 2026

Before starting your transfer, check you won't lose any valuable benefits (such as guaranteed annuity rates or a lower protected pension age) and find out what exit fees you might have to pay